KNYJY - Kone: Up 33% From October Lows Now Even More A Bet On China

Summary

- Kone shares have rebounded 33% from October lows but are still 24% below their 52-week high. The Dividend Yield is 3.6%.

- Shares are at 24.9x 2021 EPS, but we expect EPS to decline by 22% in 2022 due to cost inflation and the construction slowdown in China.

- There are positive signs on Kone's margin and sales growth, but the near-term investment case is a bet on recovery in China.

- We assume EPS will return to 2021 levels by 2024 and grow at 7% after, but investors more bullish on China will expect higher growth.

- With shares at €48.82, we expect a total return of 32% (10.5% annualized) by end of 2025. We reiterate our Buy but prefer Otis.

Introduction

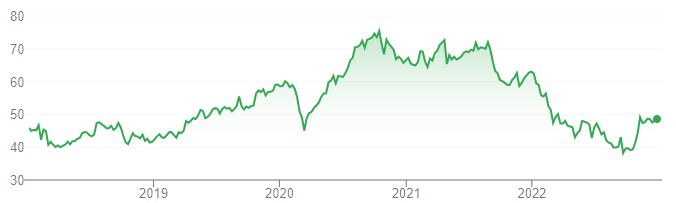

We review our investment case on KONE Oyj (KNYJY) after shares trading on their Helsinki primary exchange have rebounded 33% in euros from their October lows:

{kind=link}

We initiated our Buy rating on Kone in June 2020 . Even after the recent rebound, Kone shares have lost 13% (after dividends) since our initiation, and the share price is still 24% below its 52-week high of €64.12 (and 35% below their all-time high of over €75 in October 2020).

Kone shares now trade at 24.9x 2021 EPS, but we expect EPS to decline by 22% in 2022 (on an adjusted basis), due to input cost inflation and a decline in China New Equipment sales, offset by currency. The investment case depends on an earnings recovery, for which there are positive signs. EBIT margin has stabilized, high-margin Maintenance sales have continued growing at high-single-digits, and order book pricing improved in Q3; however, the Chinese construction market is key and remains difficult to predict. We assume EPS will return to 2021 levels by 2024 and grow at 7% annually thereafter, and that the P/E multiple will return to 28x. Under these assumptions, Kone shares will generate a total return of 32% (10.5% annualized) by 2025 year-end, including a current Dividend Yield of 3.6%. Investors with more bullish expectations on China will expect higher growth and have a higher forecasted return.

We reiterate our Buy rating on Kone but prefer Otis Worldwide ( OTIS ), which trades slightly higher at 25.7x 2021 Adjusted EPS but expects Adjusted EPS to grow by 4% in 2022 and with a 10% CAGR in the medium term.

Kone Buy Case Recap

Kone is a top-3 player in the global elevator and escalator industry. We believe Kone and its peers to be high-quality businesses, thanks to the structural growth in demand from urbanization and taller buildings, recurring Maintenance and Modernization services (which generate most of the profits, except in China), a highly consolidated competitive landscape, and a capital-light manufacturing model that sources components from a network of suppliers.

Kone is the #1 player in China and a top-3 player in every region except North America (where it is #4). Its global market share is approximately 19% in New Equipment and 10% in Services; within the latter it is a joint #2 in Maintenance.

China had historically been a major source of profits and growth for Kone, where its large construction sector generated high-margin New Equipment sales. The country represented as much as 35% of Kone's sales in 2021. However, the construction boom in China has now ended, and Kone has set out new growth targets at its 2022 investor day that rely much less on New Equipment sales:

- New Equipment sales to be "stable to low growth"

- Maintenance sales to grow at "mid to high single-digit"

- Modernization sales to grow at "high single-digit"

Kone also has a target of raising Adjusted EBIT margin to 16% (from 12.5% in 2021). As we described in our June 2022 review , the revenue growth targets, together with modest margin expansion (of, say, 35 bps annually), imply an approximately 7% annual growth in Adjusted EBIT.

In addition, Kone had historically not included automatic price adjustments in its backlog of contracts, which means COVID-related high inflation since 2021 has significantly impacted its profits. Management has been remedying this with price increases, new "dynamic" contracts pricing terms, and cost savings.

Kone Stock Valuation

At €48.82, relative to 2021 financials, Kone stock is trading at a 24.9x P/E and a 5.8% Free Cash Flow ("FCF") Yield:

| Kone Earnings, Cashflows & Valuation (Since 2019) Source: Kone company filings. |

However, as of Q3 year-to-date, Kone's Net Income is down 32% (€237m) year-on-year, while its FCF is down 54% (€556m), with the latter made worse by a €136m working capital outflow (compared to an inflow of €178m last year).

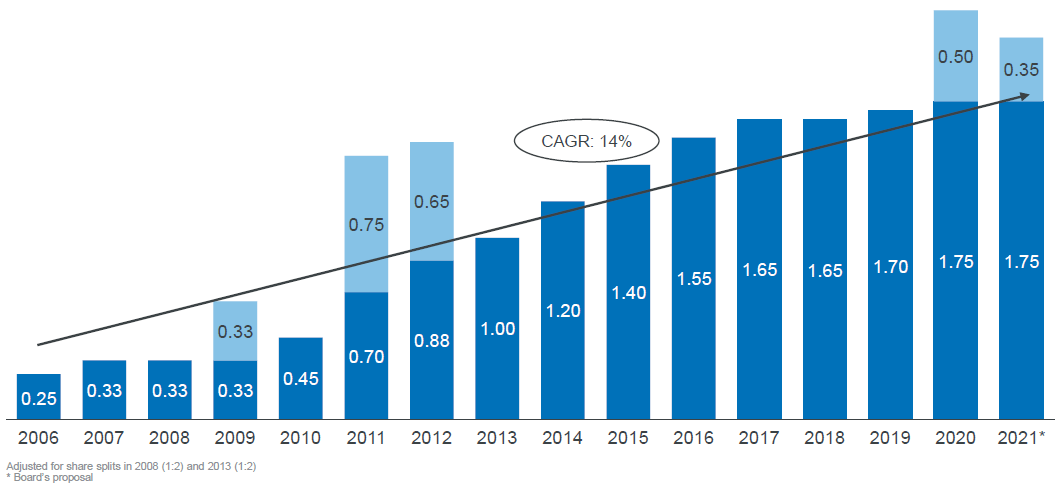

Kone paid a regular dividend of €1.75 per share and a special dividend of €0.35 per share for Class B shares in March 2022. The regular dividend alone represents a 3.6% Dividend Yield. Kone has consistently increased its regular dividend over the years, but the special dividend was reduced this year and was only infrequently paid in Kone's history:

{kind=link}

Kone's dividends cost €1,088m in 2022 (including €907m for the regular dividend), exceeding its Net Income of €1,014m in 2021. We expect Net Income to decline by 22% (on an adjusted basis in 2022), and consequently we do not believe a special dividend will be paid in 2023.

Kone 2022 Outlook

The mid-point of Kone's current 2022 outlook implies its Adjusted EBIT will decline by 20% (including currency):

| Kone 2022 Outlook Source: Kone results presentation (Q3 2022). NB. FX tailwind of 6.5% for Net Sales is our assumption. |

The current outlook dates from Kone's Q3 2022 results on October 27, and represents a downward revision from the outlook provided at Q2 results on July 20. Excluding currency, management now expects:

- Net Sales decline of -4% to -1% (the previous range was for a decline of -1% to growth of +3%)

- Adjusted EBIT of €1,010-1,090m (was €1,130-1,210m)

Within the 2022 outlook, Kone has assumed a headwind of €200m from cost inflation in materials, components and logistics (compared to €185m in Q1-3), offset by a currency tailwind of €80m (compared to €58m in Q1-3):

| Kone Adjusted E BIT Bridge (2022 vs. 2021) Source: Kone results presentation (Q3 2022). |

A key reason behind the fall in Adjusted EBIT is the decline in high-margin New Equipment sales in China, but the size of its impact has not been disclosed. Kone now expects the Chinese New Equipment market to decline by 20% in 2022, worse than the 15% expected at Q2 results, and this was the main reason behind the cut in the full-year outlook.

Kone Q3 Year-to-Date Results

The impact from the decline in New Equipment sales in China is clearly visible in Kone's results. During Q1-3, sales from Asia-Pacific fell 11.8% organically year-on-year, while sales in New Equipment fell 12.5% organically:

| Kone Net Sales By Region & Business (Q3 2022 YTD vs. Prior Year) Source: Kone results release (Q3 2022). |

China's contribution to group sales has fallen from "around 35%" in Q1-3 2021 to "over 30%" in Q1-3 2022, even as Net Sales grew 3.2% on a reported basis. The market in Asia-Pacific outside China showed "good development overall" in Q3, with India in particular having "recovered very strongly after COVID".

Kone's year-to-date results broadly support its full-year outlook. Orders Received grew 10.0% organically year-on-year (but with high-margin Chinese orders falling from "more than 40%" to "less than 40%"). Net Sales fell 3.4% organically but grew 3.2% after currency, and Adjusted EBIT was down 25.1% year-to-date (though down only 6.3% in Q3):

| Kone Orders and P&L (Q 3 2022 YTD vs. Prior Year) Source: Kone results release (Q3 2022). |

Kone does not explicitly report its Adjusted EPS, and its Reported EPS is down 32.2% year-on-year during Q1-3, about 2% worse than the decline in Reported EBIT. (The differences between reported and adjusted figures include impairments, one-off costs related to Russia/Ukraine and restructuring costs.) We expect a similar relationship to hold between the declines in Adjusted EPS and Adjusted EBIT, so for Adjusted EPS to decline by 22% in 2022.

The Kone investment case depends on an earnings recovery after 2022, for which there are positive signs.

Positive Signs for Earnings Recovery

Kone's Adjusted EBIT Margin appears to have stabilized, rising to 10.2% in Q3 after troughing at around 8% in Q1-2:

| Kone A djusted EBIT Margin By Quarter (Since 2019) Source: Kone company filings. |

Management attributes the margin improvement to pricing actions, cost savings as well as falling input costs in China.

Kone's high-margin Maintenance sales have also continued growing consistently at 7.5-9.0% year-on-year since Q3 2021, driven by unit growth, upgrades (especially with connected services) and pricing:

| Kone Sales Growth by Type (ex. Currency) (Since 20 19 ) Source: Kone company filings. |

Services, which include Maintenance and Modernization, have high but more variable growth, largely due to the volatility in the more discretionary Modernization sales. Group sales growth are even more variable due to the volatility in New Equipment sales, though New Equipment sales outside China are low-margin and have limited impact on earnings.

Pricing in the order book (which includes New Equipment and Modernization) "improved in all geographic regions … both sequentially and also in total year-over-year" in Q3. Management stated on the Q3 earnings call that:

- In Modernization orders, price increases "cover the cost increases that we have seen" as of Q3 and "should be starting to positively impact our P&L" in H1 2023

- In New Equipment orders outside China, price increases are "70% there in terms of the price covering the cost increases net of our actions"

- In New Equipment orders in China, "prices did improve like for like compared to last year", but cost savings have been the "much bigger driver" and the decline in raw material costs did "start to be a tailwind"

CFO Ilkka Hara stated that "we are booking orders on a higher margin than we're delivering right now". In addition, in Europe (where Kone has the largest part of its Services business), price increases tend to be annual, tied to specific indices like labour costs or consumer prices, and happen in Q1 - which means that current prices have not yet reflected 2022 inflation but will do so in Q1 2023.

For these reasons, we therefore expect a material recovery in Kone's Adjusted EBIT Margin in 2023.

China is Key to Kone Investment Case

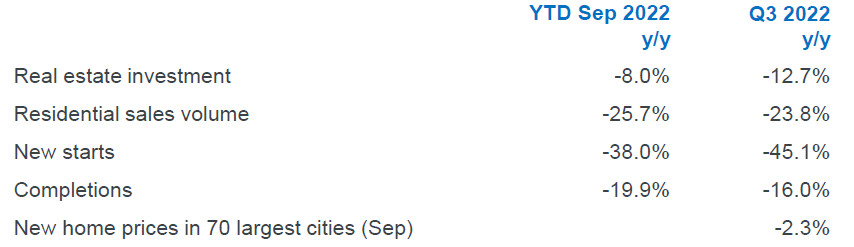

The Chinese construction market is still the key to Kone's near-term performance and remains hard to predict.

At Q3 results on October 27, new construction starts in China were down 38% year-to-date and down 45% in Q3:

{kind=link}

New construction starts in China had already fallen 11% year-on-year in 2021.

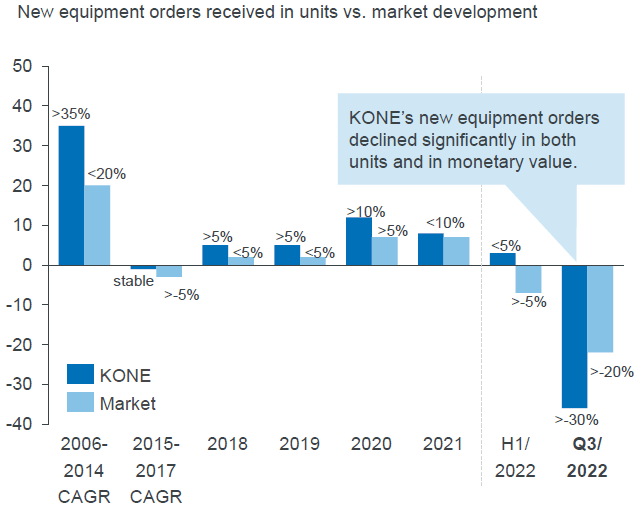

Kone New Equipment order growth had historically outperformed the Chinese construction market, but fell short by nearly 10 ppt in Q3, potentially related to management being "focused principally on price and margin":

| Kone China New Equipment Orders vs. Market (Since 2006) |

{kind=link}

Trends in order growth and order margin tend to correlate, as lower market demand typically results in manufacturers competing more intensely and accepting lower prices.

In any case, Kone management was already expecting a recovery in demand in China in 2023:

"What we are seeing in the market, we are more positive in China …We know that the need to complete many of the apartments, particularly housing that has been started already and consumers have paid a down payment, that need is high. And therefore, we would expect - and that seems to be a lot of expectation in China that - there needs to be an acceleration of completing the delayed buildings. We are not seeing that quite yet, but we said that that's something we would expect to start happening during next year at some point."

Henrik Ehrnrooth, Kone CEO (Q3 2022 earnings call)

The environment in China appears to have improved since November, with the government announcing a number of policies to support the property sector in mid-November, and abandoning significant parts of its "Zero COVID" restrictions in December. However, this part of our investment case remains hard to predict.

Kone Stock Forecasts

We have revised our Kone forecasts to incorporate a larger EPS decline in 2022 but a return to 2021 levels by 2024, after which we believe EPS will grow annually at 7%. Our assumptions now include:

- 2022 Net Income decline of 22% (was 15%)

- 2023 Net Income rebound of 15%, taking it to €910m (was €922m)

- 2024 Net Income growth of 11%, taking it to €1,010m (was €987m)

- 2025 Net Income growth of 7.0% (unchanged)

- 2022 dividend of €1.75 (was €1.67)

- Thereafter dividends to be on a Payout Ratio of 100% (unchanged)

- Share count to be flat (unchanged)

- 2025 year-end P/E of 28.0x (unchanged)

Our new 2025 EPS forecast is €2.09, 2% higher than before (€2.04), and implies an overall EPS CAGR of just 1.6% in 2021-25:

| Kone Illustrative Return Forecasts Source: Librarian Capital estimates. |

With shares at €48.82, we expect a total return of 32% (10.5% annualized) by 2025 year-end.

More bullish expectations on China will increase the forecasted return.

Is Kone a Buy? Conclusion

We reiterate our Buy rating on Kone but prefer Otis Worldwide ( OTIS ).

Otis shares currently trade at 25.7x 2021 Adjusted EPS, only slightly higher than Kone's 24.9x. However, including the benefit of buying out Otis Zardoya, Otis currently guides to a 4% growth in its Adjusted EPS growth in 2022, compared to the 22% decline we expect for Kone. Otis targets a medium-term EPS CAGR of 10%, much higher than what we expect for Kone, and has a much more modest exposure to China (20% of 2021 Net Sales).

Otis shares are likely to outperform Kone's, unless the construction market in China rebounds more than we expect.

For further details see:

Kone: Up 33% From October Lows, Now Even More A Bet On China