KKPNY - Koninklijke KPN: Room For More Margin Gains To Support Dividend Growth Plan

2023-07-27 07:39:30 ET

Summary

- "Cutting to grow" has been a good strategy in recent years for Dutch telecom firm KPN, with expanding profit margins delivering growth despite flat revenue.

- Managing the recent bout of high inflation has proved an added challenge given the upward pressure on energy and labor costs, with the margin declining in H1 2023.

- More of the same can work going ahead, with the rollout of fiber-to-the-home offering opportunities for both OpEx and CapEx reduction.

- Management's 3-5% annual dividend per share growth goal looks doable in the medium term, but I'd like to see a higher yield before pinning a Buy rating to the stock.

Revenue growth has been hard to come by for incumbent Dutch telecom firm KPN ( KKPNY , KKPNF ), but a combination of profit margin expansion and solid free cash flow generation has nonetheless supported healthy earnings and dividend growth in recent years.

The recent bout of high inflation in the Eurozone has proved an extra challenge to manage, with upward pressure being felt on the cost base and revenue growth still quite weak in real terms. Although this led to weaker EBITDA margin in the first half of fiscal 2023, price hikes feeding through from July should support margins in H2.

With KPN's EBITDA margin already expanding by over 400 basis points over the past five years into the mid-40s region, "cutting to grow" is probably reaching its limit. Still, there are some margin drivers left on the table, while the rollout of fiber-to-the-household ("FTTH") broadband should free up some extra cash flow over the next few years that can further be spent on growth enhancing measures.

The above should allow management to make good on its 3-5% annual dividend growth goal, but with the current dividend yield of 4.5% below its recent historical average I'd like to see a little higher margin of safety before attaching a Buy rating to these shares. Hold.

Work On Costs, Free Cash Flow Support Growth

KPN offers fixed-line and mobile services to retail and business customers in the Netherlands. It also sells access to its mobile and fixed-line network to third-party operators through its Wholesale division.

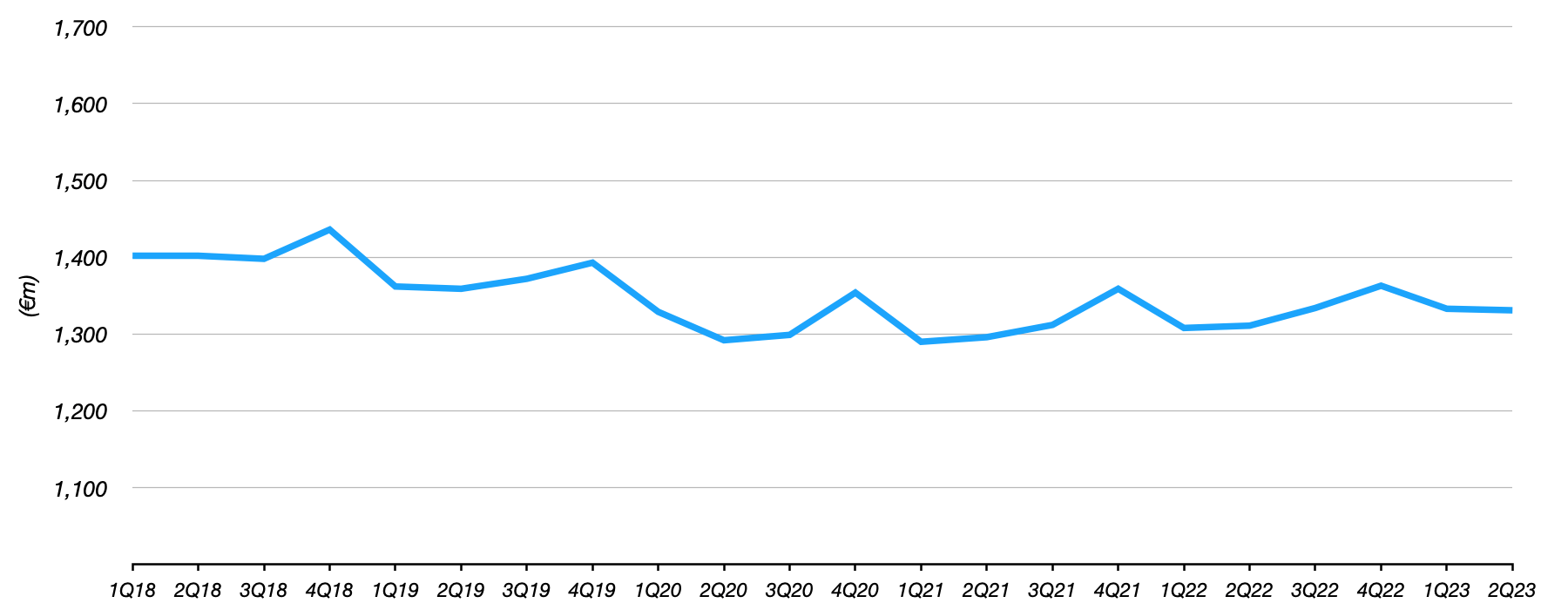

Like many telecom operators in mature markets, KPN has seen recent years marked by fairly stagnant revenue. Its retail customer base has been virtually flat, with average revenue per user ("ARPU") likewise not showing much growth. The Business division has seen better growth in the customer base, but revenue growth has been hampered by the structural decline in traditional fixed voice services which historically generated relatively high ARPU. As a result, group revenue has been down-to-flat over the past several years.

KPN: Quarterly Adjusted Revenue

Data Source: KPN Quarterly Results Supplement

{kind=link}

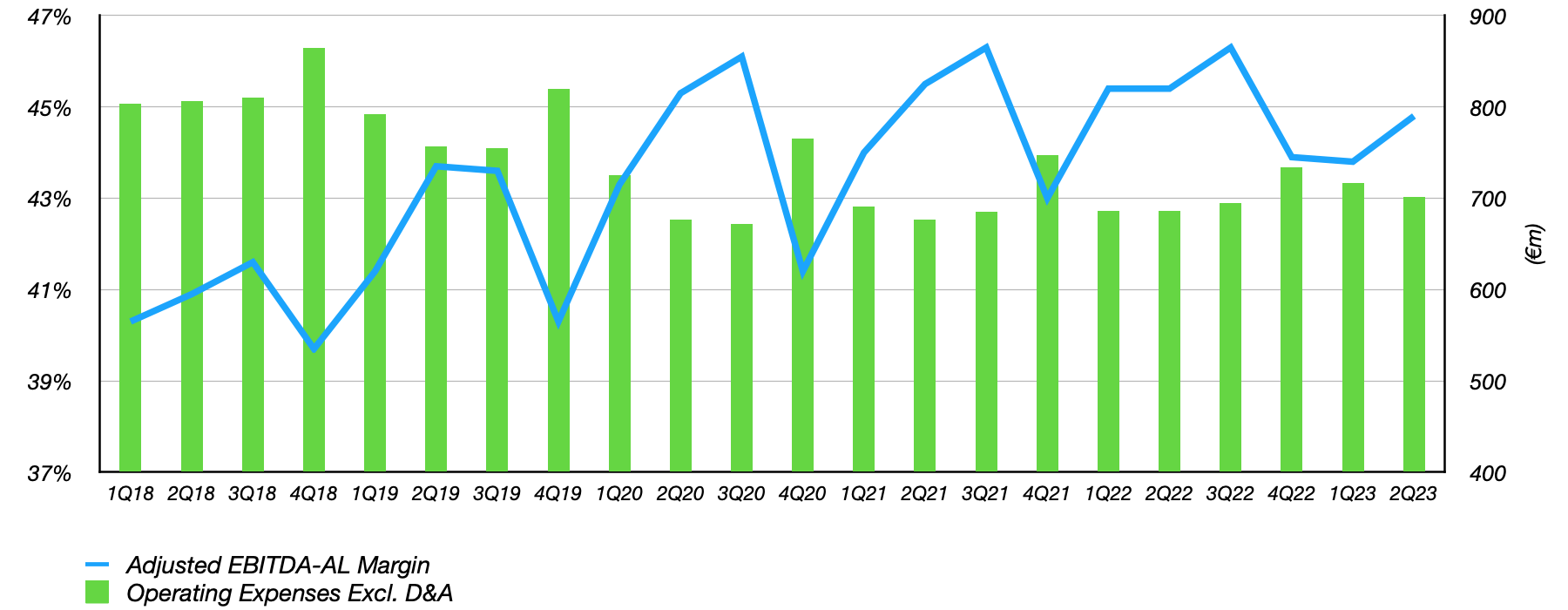

Stagnant revenue has not prevented KPN from growing earnings, as EBITDA margin expansion from operating expense reduction has more than offset this. EBITDA-AL (i.e. after leases) has expanded by over 400bps since 2018, chiefly as a result of declines in personnel expenses.

KPN: Quarterly Operating Expenses & EBITDA-AL Margin

Data Source: KPN Quarterly Results Supplements

{kind=link}

Furthermore, KPN generates relatively healthy levels of free cash flow despite the high CapEx requirements of telecom companies in general. Since 2018 the company has generated €1.2B in surplus free cash flow, which I define as free cash flow after subtracting cash dividends for shareholders. This has allowed the company to spend a cumulative total of approximately €500m on share buybacks over the past couple of years, with the resulting lower share count helping to further support growth in per-share earnings and dividends.

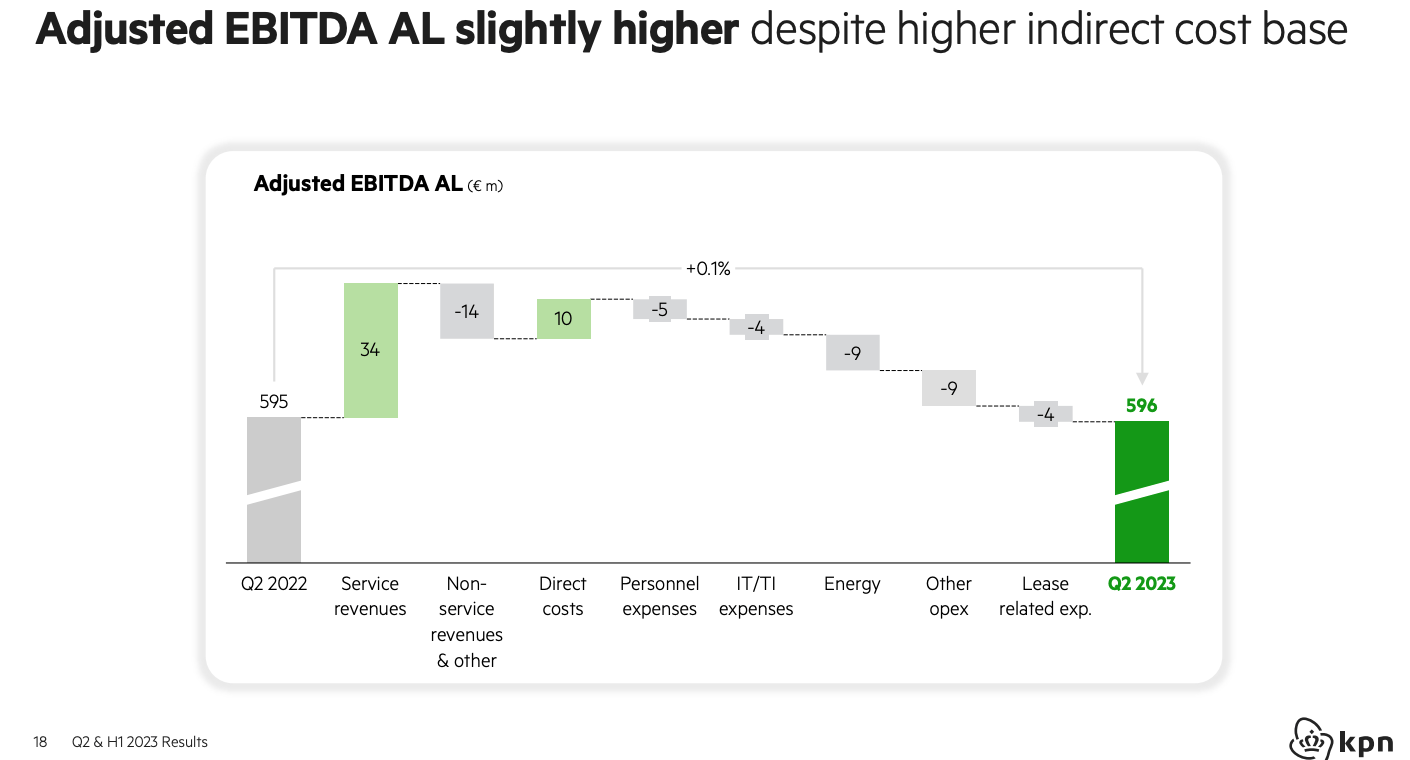

Margins Dip In H1, Should Stabilize In H2

The recent bout of high inflation in the Eurozone has posed a challenge to KPN's growth strategy given the resulting upward pressure on energy and personnel expenses. In the first half of 2023, EBITDA-AL declined slightly year-on-year, chiefly due to higher labor and energy costs leading to a year-on-year rise in operating expenses. Margin declined by over 100bps YoY to 44.3%. Positively, Q2 EBITDA-AL returned to slight growth, albeit not enough to offset the decline in Q1.

Source: KPN Q2 2023 Results Presentation

{kind=link}

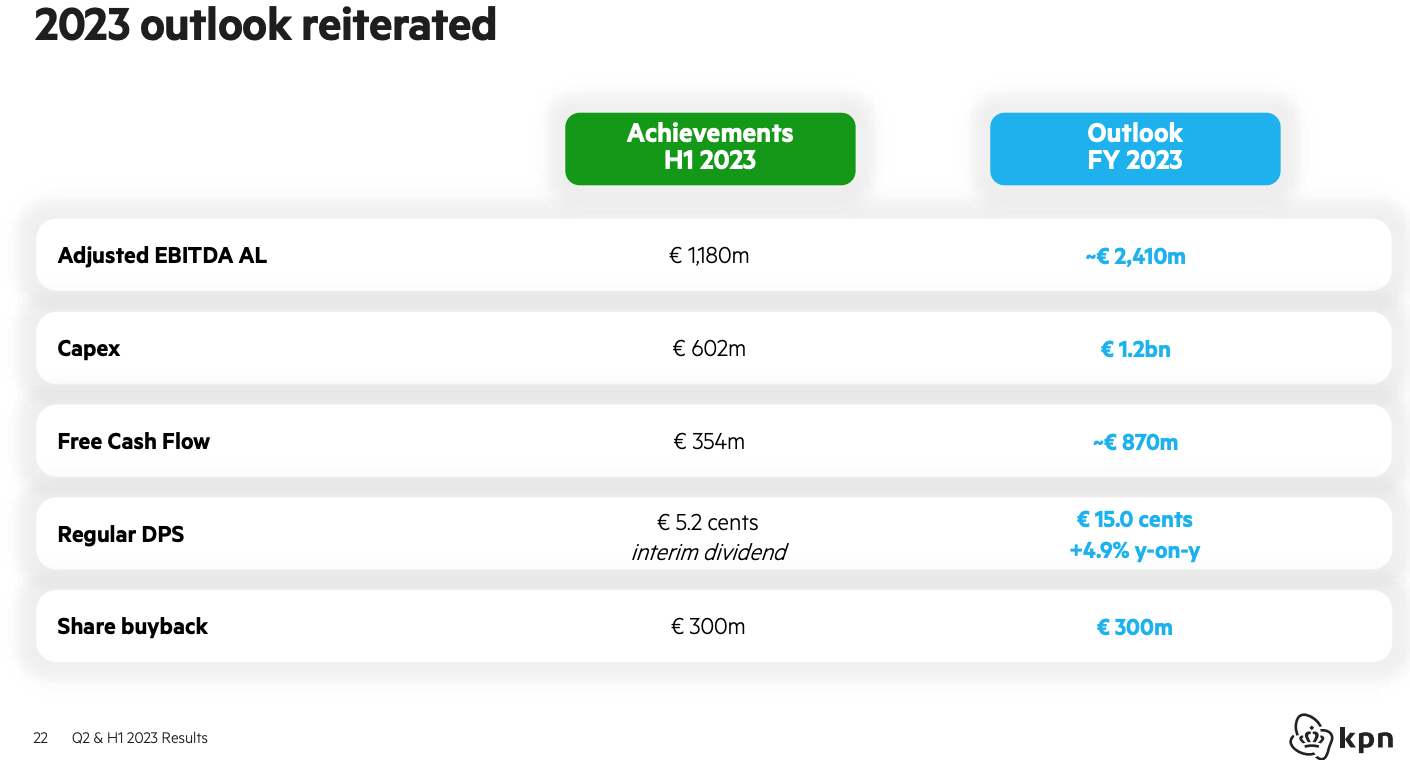

Margins should not deteriorate in the second half of the year, as revenue will get a boost from an inflation-linked 6.4% price increase in the broadband portfolio that took effect from July. KPN has further locked in "most" of its energy procurement for the year, which should further support margins in H2. Management has affirmed previous FY23 guidance of €2.410B in FY23 EBITDA-AL, which would imply slight growth in adjusted EBITDA-AL and an improving YoY margin trend.

{kind=link}

Looking slightly further ahead, management anticipates flat-to-down energy costs in FY23, which alongside moderately higher revenue should lead EBITDA-AL margin back into the 45% area in FY24:

For '24, we bought about 60% at around that price, €150 to €160. The spot market is a bit lower, around €120. So, if you add up, we'll probably get to a flat energy spend next year versus this year possibly a bit lower if the energy market continues to soften, but I'd be -- I don't run ahead of myself.

Chris Figee, KPN Chief Financial Officer, Q2 2023 Earnings Call

Dividend Growth Targets Attainable

Management targets annual growth of 3-5% in the per-share dividend. As per above, in recent years this has been achieved by a combination of OpEx reduction and share buybacks.

These drivers should continue to support growth in the per-share dividend in line with management's goal. On margin expansion, further gains will be harder to come by simply on account of the higher base, as EBITDA-AL margin is already relatively high at 44.8% (Q2 2023) and has expanded by over 400bps in five years. Nevertheless, the company still has drivers to push margin higher. For instance, its rollout of FTTH should naturally support lower levels of OpEx, as customers switching from the old copper network to full fiber will incur savings for KPN:

KPN has successfully started to decommission its copper network in certain areas this year. These areas together cover around 2.4 million connections. Going forward, KPN will be gradually switching off its copper network in areas where fiber is available. Over time this results in significant quality improvements and spend savings related to the closure of technical buildings, reduced service tickets and maintenance costs, and lower energy consumption.

Source - KPN Q2 2023 Results Release

On free cash flow, KPN should benefit once the rollout of FTTH winds down. Capital expenditure as a percentage of a revenue has increased from 19.5% to 24% over the past five years, but with the firm targeting 80% of homes passed by 2025 CapEx requirements should moderate. Even with elevated CapEx free cash flow remains ample, though, with management's 2023 FCF guidance of €870m enough to cover the current dividend with over €250m in surplus.

Shares Look Ballpark Fair Value

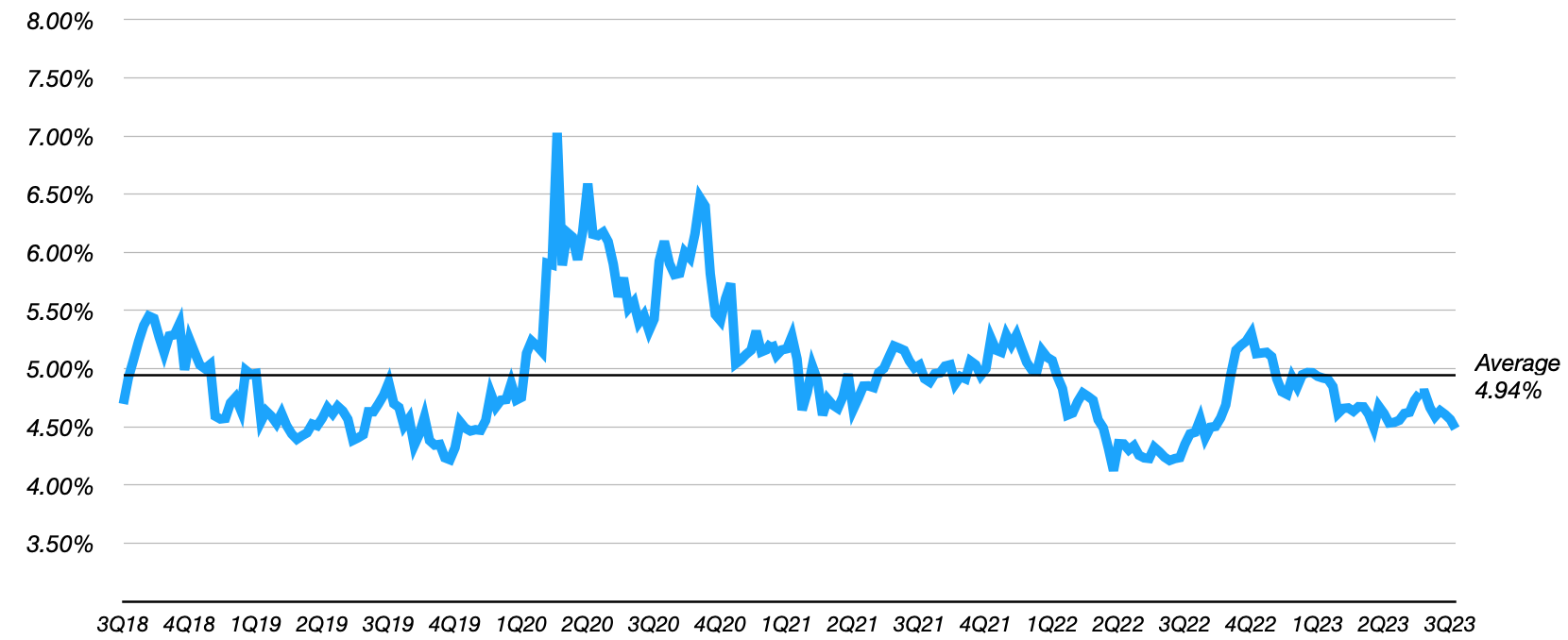

KPN shares trade for €3.29 each in Amsterdam trading at time of writing, putting them on a 4.55% dividend yield based on management's FY23 DPS guidance of €0.15 per share.

KPN: Dividend Yield

Data Source: Yahoo Finance, Author Calculations

{kind=link}

Annual DPS growth edging toward the higher end of management's 3-5% target range would map to the 9% annual returns benchmark I'd typically be looking for, but with the yield toward the lower-end of its historical range I do see the potential for value multiple expansion to eat into that, and so I would be looking for a higher margin of safety before attaching a Buy rating here. Hold.

For further details see:

Koninklijke KPN: Room For More Margin Gains To Support Dividend Growth Plan