KTB - Kontoor Brands Is On Watch Heading Into Earnings

2023-10-31 17:57:15 ET

Summary

- Kontoor Brands, producer of Wrangler and Lee jeans, has experienced lumpy financial performance with declining profits.

- Despite the decline, the stock is cheap on an absolute basis but looks pricey compared to similar firms.

- Analysts expect the upcoming third-quarter results to show an increase in revenue and profits, leading to cautious optimism.

While I have taken an interest in all sorts of companies over the years, I tend to find myself most drawn toward companies that have really simple business models. Single product companies or companies with very few products are some of the most intriguing to me. This is because, if they are attractive, it's because they have a world-class brand and because the business is not that difficult to maintain. One company that fits this description is Kontoor Brands ( KTB ), the producer of fashion brands such as Wrangler and Lee jeans. From a revenue and profit perspective, this year has been rather interesting for the company. Financial performance has been a bit lumpy, with profits coming in particularly low. Even with the decline seen in profitability, shares of the company do look cheap on an absolute basis. But relative to similar firms, the stock is starting to look a bit pricey. But between how shares are priced, the fact that the company is a quality operator, and expectations provided by analysts for the upcoming third quarter release, I have decided to remain cautiously optimistic. In the event that the third quarter comes in worse than anticipated, I do think a downgrade might be in store unless shares fall too far in response to that development. But for now, on the edge of the precipice that is earnings, I've decided to keep the business rated a 'buy'.

A bad fit so far

In early March of this year, I ended up revisiting my bullish thesis regarding Kontoor Brands. From the prior bullish article that I published about the company in November of last year through the time that the most recent article was published, shares of the business had done quite well, jumping 24.1% compared to the 0.2% decline seen by the S&P 500. Despite that nice move higher, I found myself impressed by continued strong growth on both the top and bottom lines. I acknowledged that the easy money had been made up to that point. But I still believed that further upside was on the table. As a result, I ended up keeping the company rated a 'buy', but that has not proven to be all that profitable. Since the publication of that article in March, shares have seen a downside of 8.9% while the S&P 500 has increased 5.1%. Fortunately, I am still up relative to the November 2022 article to the tune of 15.3%. This is more than triple the 4.8% seen by the S&P 500.

{kind=link}

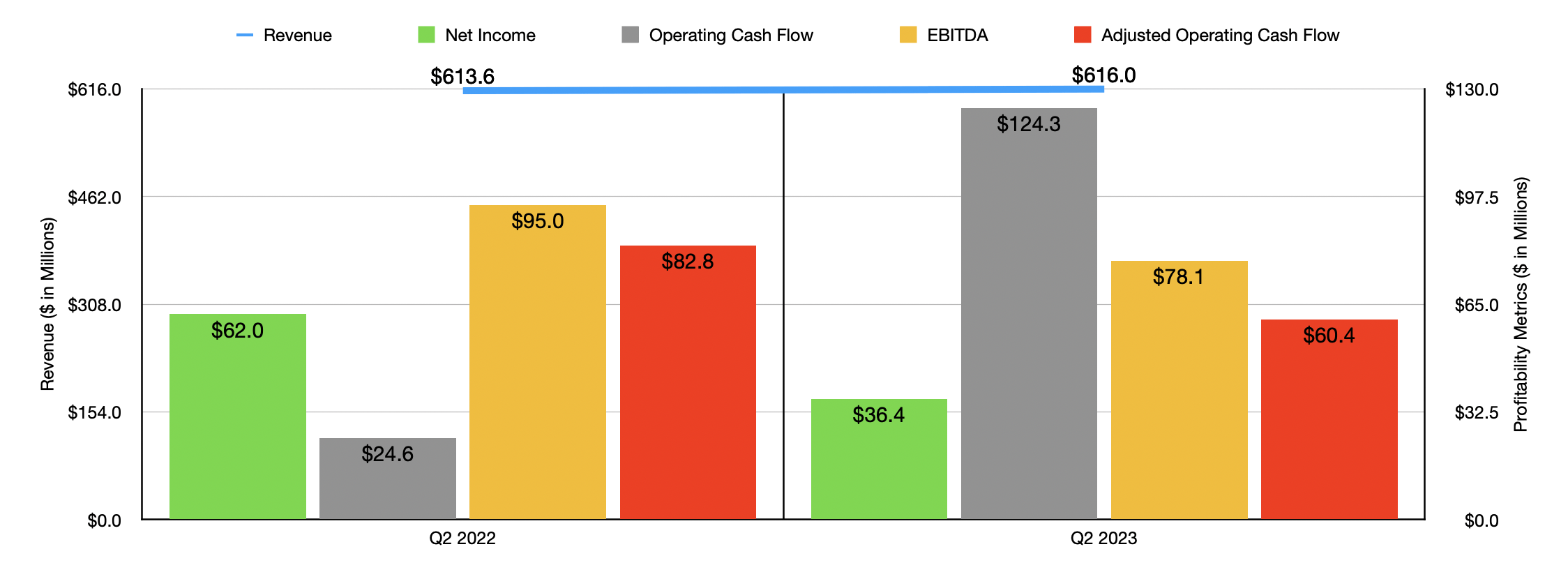

Some of the more recent troubles that Kontoor Brands has faced seemed to involve lumpy financial performance. Take, for instance, the most recent quarter of the 2023 fiscal year. Revenue for the company came in at $616 million. That represents an increase of only 0.4% compared to the $613.6 million reported one year earlier. A small portion of that increase was driven by foreign currency fluctuations. But $1.8 million was attributable to the operations of the company. But this does not mean that revenue was up across the board. In the APAC (Asia/Pacific) regions in which it operates, particularly in China, both wholesale and direct-to-consumer operations posted year-over-year growth. But in the US and EMEA (Europe, Middle East, and Africa) regions, sales declined, with those declines driven by weaker digital wholesale revenue that was only marginally offset by growth in the direct-to-consumer space.

When you break up the data by category, you see something interesting. Revenue for the Wrangler brand came in rather strong at $425.5 million. That's 1.8% above the $417.9 million generated one year earlier. Growth in the US wholesale and direct-to-consumer categories proved to be rather bullish for the company. In the APAC region, licensing activities that the company engaged in pushed sales up a whopping 53%. On the other hand, the Lee brand reported a decline in revenue from $193.1 million to $188 million. What's interesting about this is that where the Wrangler brand performed well, the Lee brand performed poorly and vice versa. In fact, in the Americas, revenue for Lee plummeted 13%. The one exception was the APAC region where revenue also skyrocketed, jumping 78% year over year.

This overall increase in sales for the company should have translated to higher profits as well. But that unfortunately is not what we saw. Net income for the company plummeted from $62 million to $36.4 million. That decline was driven by a combination of factors, including higher inventory costs resulting from inflationary pressures, as well as an unfavorable product mix. Management also pushed through some downtime in incurred costs aimed at streamlining operations further. For the Wrangler brand, the firm's operating margin declined from 18% to 16.7%, while for the Lee brand it dropped from 11.9% to 9.1%. Other profitability metrics largely followed suit. The one exception was operating cash flow which soared from $24.6 million to $124.3 million. But if we adjust for changes in working capital, we get a decline from $82.8 million to $60.4 million. Meanwhile, EBITDA for the business dropped from $95 million to $78.1 million.

{kind=link}

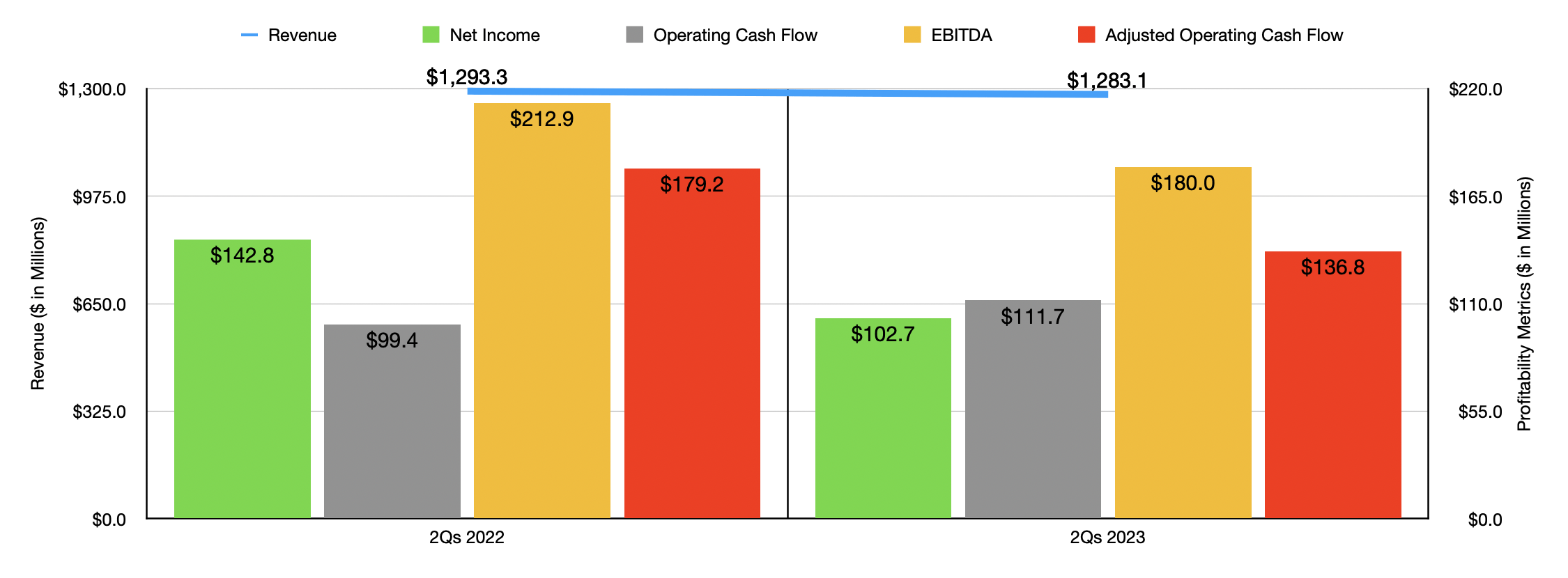

As you can see in the chart above, financial performance for the first half of the year as a whole has also been rather mixed. Revenue actually decreased during this time, while all of the company's profitability metrics, with the exception of operating cash flow, worsened year over year. It's not surprising to see some pain on the bottom line. After all, inflation is at the highest levels that we have seen in over 20 years. And while it would be ideal for a company to be able to push on those inflationary pressures to their customers, only so much of that can be done before there is pushback.

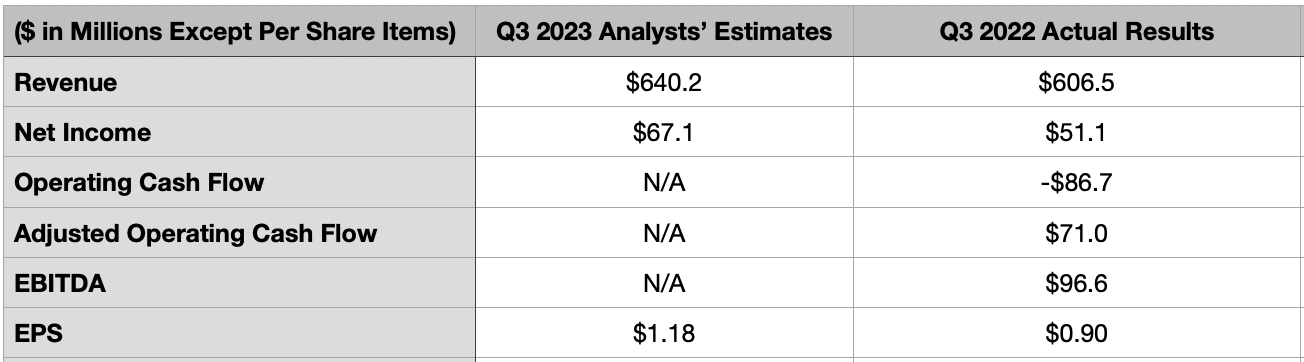

Interestingly, the picture might be about to change. And that change could be for the better. You see, before the market opens on November 2, the management team at Kontoor Brands is expected to announce financial results covering the third quarter of the company's 2023 fiscal year. Analysts are currently forecasting revenue of $640.2 million. If this comes to fruition, it would translate to a 5.6% increase over the $606.5 million generated the same time last year. Even more exciting is the expectation when it comes to the bottom line. The current forecast is for profits per share of $1.18. That would be comfortably above the $0.90 per share reported for the third quarter of 2022. This would result in net profits climbing from $51.1 million to approximately $67.1 million. We don't know what other profitability metrics might come out to be since analysts have not provided any detailed guidance. But for context, you can see, in the table below, what these metrics totaled in the third quarter of last year.

{kind=link}

Fortunately, management has provided guidance when it comes to 2023 in its entirety. They didn't give a specific number, but they did say that revenue should increase at the low-single digit rate. That projected increase is likely why analysts are forecasting growth in the third quarter. That increase is also sensible when you consider US clothing and apparel retail sales so far this year. Revenue for the first nine months of the year came in at $217.6 billion. That's 1.4% higher than what was reported the same time one year earlier. Earnings per share, meanwhile, are expected to be between $4.55 and $4.75. At the midpoint, that would translate to adjusted profits of $264.3 million. Taking the conservative route, I decided to annualize the company's other financial data. Following this approach, I get adjusted operating cash flow of $232.5 million and EBITDA of $340.3 million.

{kind=link}

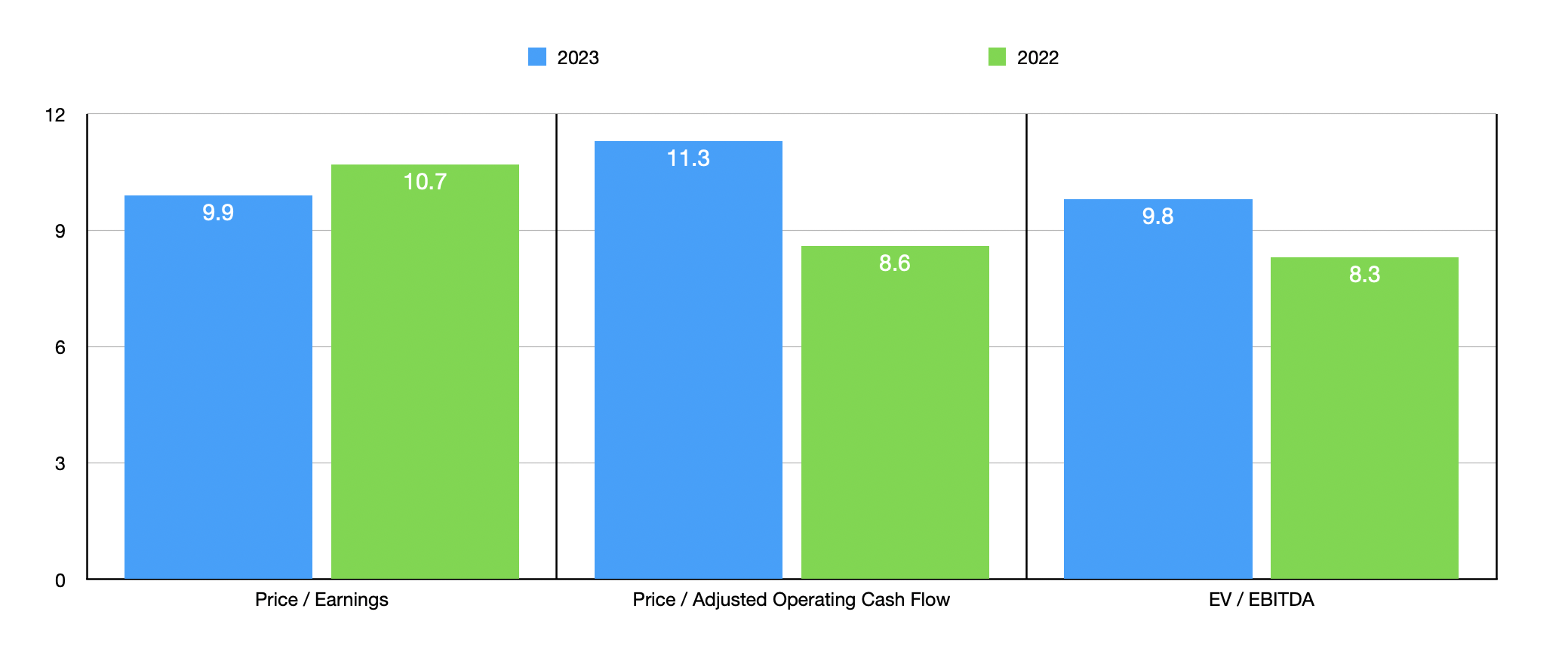

As you can see in the chart above, shares of the company do look cheaper on a forward basis for the price to earnings multiple than if we were to use data from 2022. But they do look more expensive using the other two profitability metrics. On an absolute basis, I wouldn't call shares expensive by any means. But they do look a bit pricey relative to similar enterprises. In the table below you can see what I mean. While on a price to earnings basis two of the five firms I compared it to ended up being cheaper than it, four of the five are cheaper on a price to operating cash flow basis while all five ended up being cheaper when it comes to the EV to EBITDA basis.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Kontoor Brands |

| 9.9 |

| 11.3 |

| 9.8 |

| Canada Goose Holdings ( GOOS ) |

| 30.8 |

| 13.6 |

| 9.2 |

| Capri Holdings Limited ( CPRI ) |

| 14.7 |

| 9.7 |

| 8.9 |

| Oxford Industries ( OXM ) |

| 8.5 |

| 7.3 |

| 5.1 |

| Carter's ( CRI ) |

| 12.3 |

| 6.3 |

| 7.5 |

| G-III Apparel Group ( GIII ) |

| 4.5 |

| 5.5 |

| 6.0 |

Takeaway

From all that I can see, it's clear that the road forward for Kontoor Brands is not as clear as I would have thought. Recent issues with profitability could be difficult to overcome while inflation remains elevated. Having said that, I would argue that the company still looks like a decent prospect at this time. This is especially true if analysts turn out to be accurate regarding the third quarter. On the other hand, should the company report a worsening of results similar to what it did in the second quarter of the year, downgrading it to something neutral like a 'hold' might not be a bad idea. But for the moment, I am keeping it a soft 'buy'.

For further details see:

Kontoor Brands Is On Watch Heading Into Earnings