KOP - Koppers Holdings: Diversification Resulting In Margin Expansion

2023-09-25 05:04:58 ET

Summary

- Koppers has recently surged in price due to strong earnings, resulting in greater cash flows than expected.

- The firm has outperformed the S&P 500 over the last 3 years and is still highly regarded by analysts.

- Koppers' balance sheet is slightly more leveraged than I would have liked but still stable.

- The firm's diversification strategy will stabilize cash flows and reduce regulatory scrutiny.

- Assuming my DCF figures, Koppers is currently undervalued even after a risk premium, resulting in a buy rating.

Koppers Holdings (KOP) has recently experienced a share price surge over the past year due to strong earnings and guidance. Despite the price movement, I believe Koppers is still a buy due to its solid future performance, more stable cash flows through its diversification strategy, and undervaluation assuming my DCF figures.

Business Overview

Koppers Holdings Inc. serves the US, Australasia, Europe, and other foreign markets as a supplier of treated wood products, wood preservation chemicals, and carbon compounds. Performance Chemicals, Carbon Materials and Chemicals, and Railroad and Utility Products and Services make up the company's three main business segments.

Koppers purchases and treats crossties, switch ties, and various kinds of lumber used in railroad infrastructure, including bridges and crossings, as part of the RUPS segment. Additionally, they provide pilings, transmission and distribution poles for utilities and rail joint bars to attach tracks for railways. Additionally, this division provides railroad services such as engineering, design, maintenance, and inspection for railroad bridges.

For a variety of uses, including decking, fencing, utility poles, and construction lumber, the PC segment is in charge of developing, producing, and selling copper-based wood preservatives. Additionally, they offer chemicals that are fire-resistant and are employed in pressure treatment for commercial buildings.

The CMC business, produces a variety of commodities, including creosote, carbon pitch, naphthalene, and phthalic anhydride, for use in a variety of industries, including railroads, specialized chemicals, utilities, residential lumber, agricultural, aluminum, steel, rubber, and construction.

Koppers

Financials

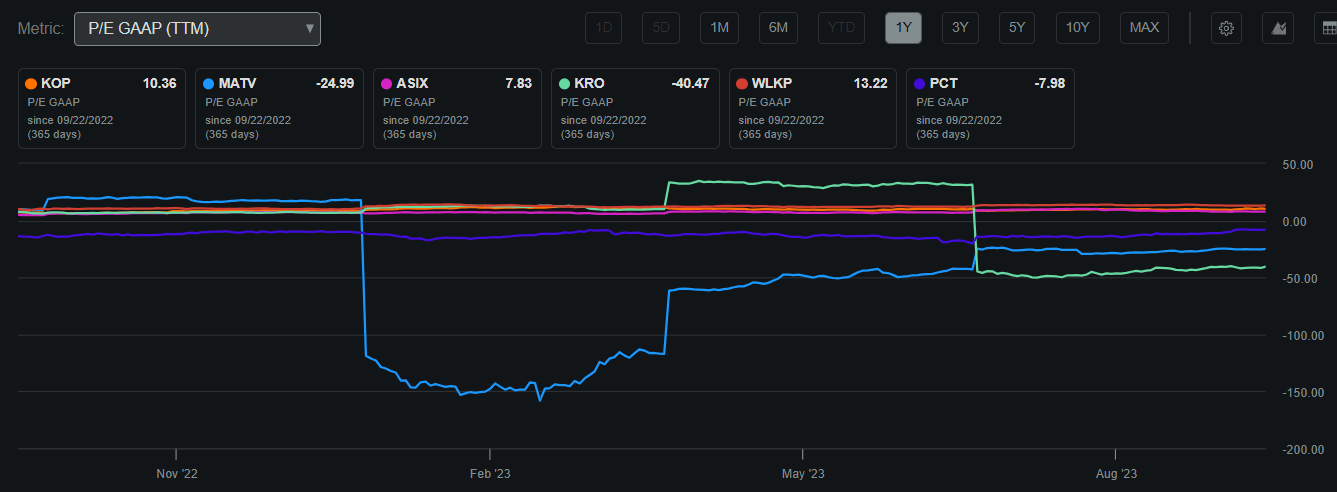

Koppers Holdings is currently valued at around $864.11 million in the market, with a fair Return on Invested Capital of 7%. The stock is presently priced at $40.45 per share, slightly below its 52-week high of $41.91. Koppers also holds a P/E GAAP of 10.36, which is below most of its peers demonstrating that the firm is undervalued on a relative basis.

{kind=link}

Koppers also pays a dividend of 0.57% representing a payout ratio of 5.64%. This indicates that Koppers is committed to providing shareholder values in multiple ways while also keeping the payout extremely conservative to hedge against macro or cyclical headwinds. I believe that as the firm's cash flows become more diversified and its ROIC declines due to its large size, Koppers will begin to increase its dividend, thus improving the income aspect of this equity.

{kind=link}

Earnings

Koppers recently reported strong Q2 2023 earnings by beating on the top and bottom lines. With EPS surpassing expectations by $0.16 at $1.26 and revenues beating estimates by $46.2 million at $577.2 million representing a 14.87% YoY growth, the firm is demonstrating outperformance amid macro headwinds. In regards to guidance, Koppers also recently raised its profit outlook demonstrating operational strength even several weeks after its last report. With earnings estimates displaying rather steady growth, Koppers is in a position to outperform with high cash flow thus creating more value for shareholders.

Earnings Estimates (Seeking Alpha)

Performance Compared to the Broader Market

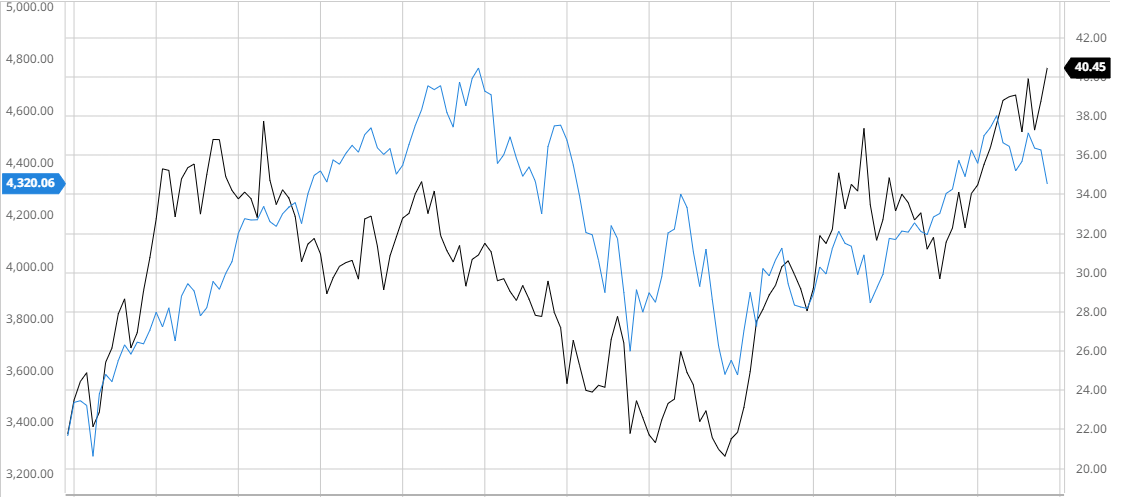

Over the last 3 years, Koppers has outperformed the S&P 500 when adjusting for dividends. This demonstrates the firm's effective use of FCF in order to capitalize on cyclical uptrends and create a more defensive firm for downturns.

Koppers Compared to the S&P 500 3Y (Created by author using Bar Charts)

{kind=link}

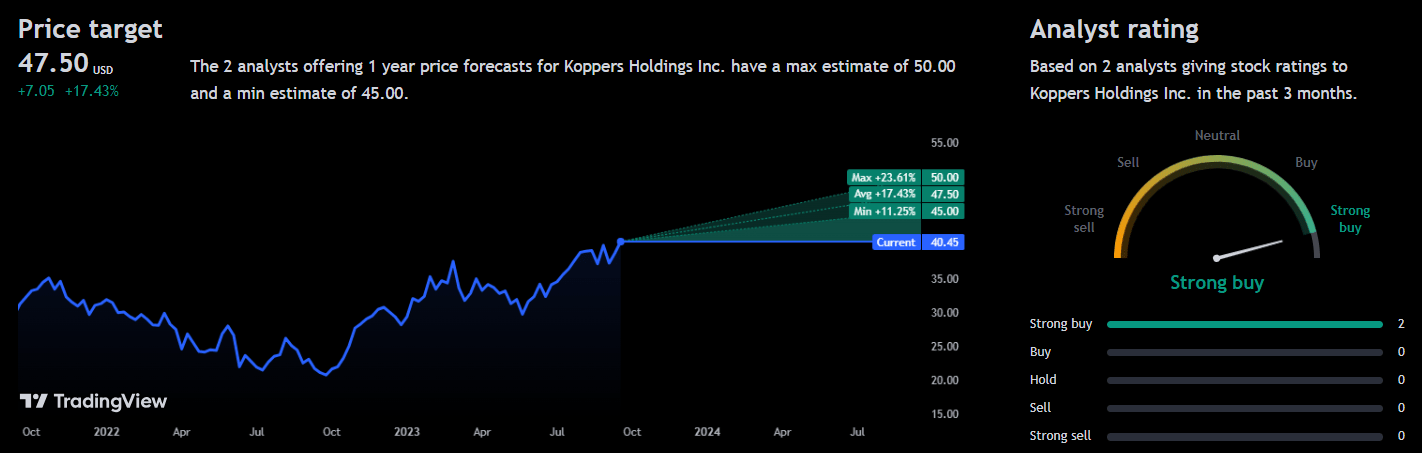

Analyst Consensus

Analysts within the past 3 months currently rate Koppers as a "strong buy" with an average 1Y price target of $47.50 demonstrating a potential 17.43% upside. This confidence in Koppers by analysts truly recognizes the firms solid capabilities along with financials.

{kind=link}

Balance Sheet

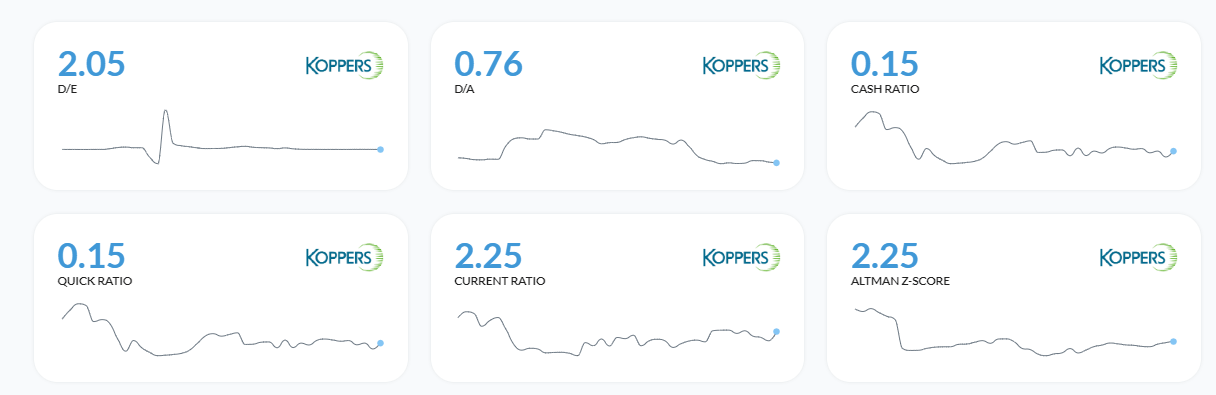

Looking at Koppers' balance sheet, I believe that the firm is slightly more leveraged than I would like. With debt increasing amid high rates and interest coverage of 3.58 during an uptrend in income, Koppers must focus on debt repayment in order to improve cash flow and optimize its leveraging strategy. But, with a current ratio of 2.25 and an Altman-Z-Score of 2.25, Koppers is positioned to remain solvent in the short-medium term demonstrating it still holds some leverage in case of cash flow struggles.

{kind=link}

{kind=link}

{kind=link}

Valuation

Before finding a fair value for Koppers, I decided it would be beneficial to use an accurate discount rate via Cost of Equity and WACC. First off, assuming a risk-free rate of return of 4.44% which represents the 10-year treasury yield , I was able to calculate a Cost of Equity of 8.66% which represents the return demanded to hold Koppers' equity.

Cost of Equity (Created by author using Alpha Spread)

Assuming my previous calculation and Koppers' cost of debt, I was able to find the firm's WACC to be 6.36%.

WACC Calculation (Created by author using Alpha Spread)

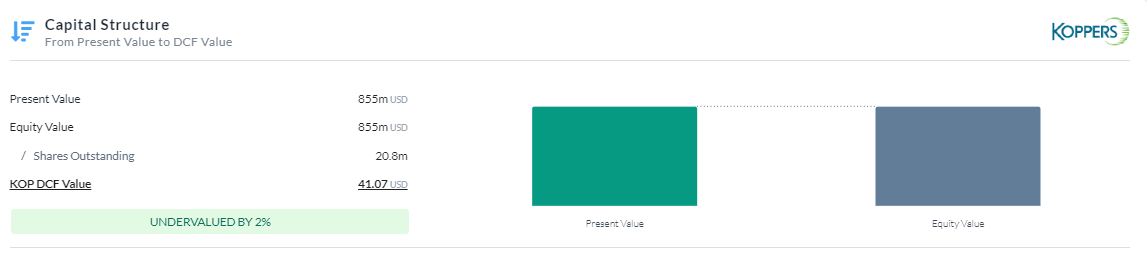

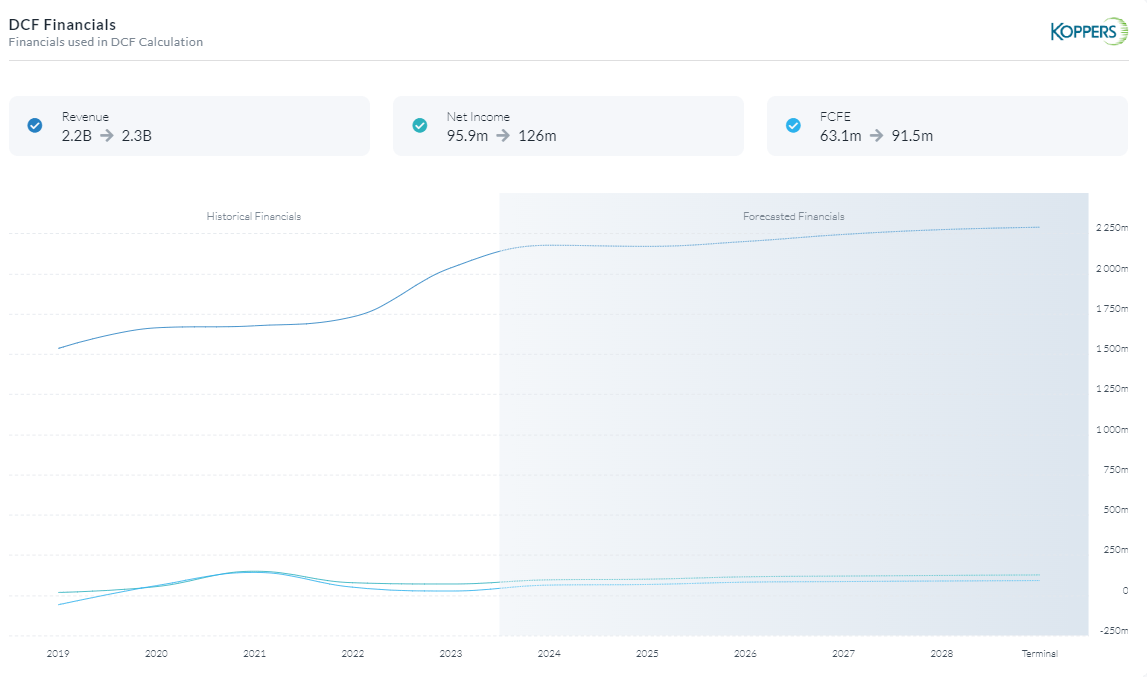

Now that I have calculated an appropriate discount rate, I decided to add a risk premium of 1.34% to account for macro headwinds, the firm's rather leveraged balance sheet, and cyclical downturns. Using a 5Y Equity Model DCF via FCFE, Koppers is currently valued at $41.07 meaning the firm is undervalued by 2%. Regarding my assumptions, my revenue and margin estimations are in line with the average analyst's expectations.

5Y Equity Model DCF Using FCFE (Created by author using Alpha Spread)

{kind=link}

{kind=link}

{kind=link}

Diversification Resulting in Margin Expansion

To improve its position in the market and profitability, Koppers Holdings has followed a diversification and innovation strategy. One of their significant product portfolio diversification tactics includes adding more environmentally friendly and sustainable options to their typical coal tar-based products. They started making chemicals, carbon compounds, and treated wood products for a wider range of businesses.

Koppers, for example, created ways to transform wood into highly valuable carbon compounds used in the manufacture of aluminum and lithium-ion batteries. This action took advantage of the rising demand for environmentally friendly products, particularly in the industries of renewable energy and electric vehicles. In addition to increasing their market reach, this diversification helped them establish themselves as a more inventive and sustainable participant in the market.

In terms of innovation, Koppers made investments in R&D to enhance current procedures and produce more effective, long-lasting, and affordable solutions. By embracing innovation, they were able to adapt to a changing market, changing consumer tastes, and shifting regulatory constraints. For example, they created cutting-edge wood preservation technologies to increase the robustness and security of wood goods used in infrastructure and buildings. These developments were made in an effort to satisfy the rising demand for building supplies.

I believe that Koppers' commitment to remaining ahead of the innovation curve while also diversifying product offerings will result in greater market share and a more competitive position without the alteration of prices. This, along with reduced regulatory risks will stabilize cash flows and leave more FCF to expand its core operations and potentially enter more high-growth, profitable segments of the chemicals industry. In a time of high FCF and an uprise in share price, the increased cost of debt may not deter Koppers' strategy for expansion.

Risks

Raw Material Costs and Supply: Production costs and overall profitability can be affected by changes in the price and availability of raw materials, particularly wood, chemicals, and carbon-based compounds.

Regulatory Compliance: Koppers is a provider of chemicals for wood preservation and is subject to a number of laws governing the environment, public health, and workplace safety. Legal responsibilities, fines, or production interruptions may come from changes in regulations or from inadequate compliance.

Conclusion

To summarize, I believe Koppers is still a buy even after the share price surge due to its solid future performance, more stable cash flows through its diversification strategy, and undervaluation assuming my DCF figures.

For further details see:

Koppers Holdings: Diversification Resulting In Margin Expansion