KOP - Koppers Holdings: Signs Of Deterioration In Q3 Earnings

Summary

- KOP is an integrated manufacturer of wood protection chemicals and pressure treated wood products.

- The company operates in cyclical, commoditized and mature industries.

- Although I believe it should be returning capital, the company continues investing heavily, particularly on its less profitable segments.

- With that in mind, I consider KOP should trade based on an average of its earnings across the cycle.

- However, it currently trades significantly above that level.

Koppers Holdings ( KOP ) is a global integrated manufacturer of wood protection chemicals and treated wood products.

In my initiation coverage article on KOP I commented on the company's mature and commoditized industries, its less than desirable capital allocation decisions and the cyclicality of its operations. With the industry then seemingly in the upper portion of the cycle, I recommended avoiding KOP.

Since then the stock has climbed almost 22%. The company's business performance during that period has been normal, not extremely different from what was prevalent a few months ago. For that reason, I still do not consider KOP a valuable opportunity.

Note: Unless otherwise stated, all information has been obtained from KOP's filings with the SEC .

Company overview

For a more detailed review, please visit my initiation coverage article on KOP .

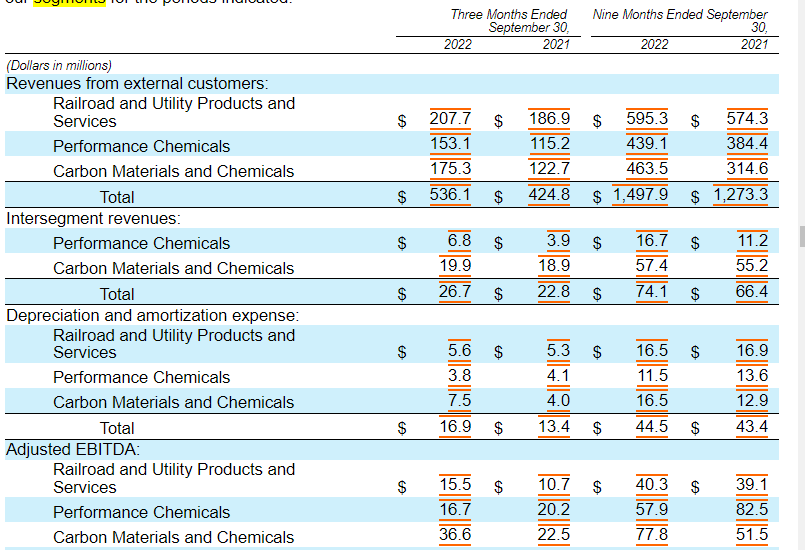

KOP is an integrated wood treatment company. The company manufactures chemicals used to treat wood, made of tar coal (carbon materials and chemicals segment) and copper (performance chemicals segment). KOP also uses these chemicals to pressure treat wood that is then sold to railroads, utilities and for other special uses (railroads and utilities products and services segment). What these segments share in common is that their industries are competitive, either mature or declining, and cyclical.

In the case of the CMC and PC segments, KOP manufactures commodity chemicals that are functionally indistinguishable from the ones manufactured by competitors. In the particular case of CMC, the industry is also in decline as creosote, the main chemical manufactured by the segment, is being slowly abandoned. Part of that decline is absorbed by copper chemicals, manufactured by the PC segment. The RUPS segment is not in decline, as railroads and utilities continue to use wood, but is mature, without much room for growth. The same is true for the PC segment.

All of the segments suffer from cyclicality, CMC ranging from lows of $20 million in operating losses to $60 million in operating profits, RU from $6 to $60 million and PC from $30 to $80 million. These movements come from the latest cycle, spanning the last 6 years.

For a company in a low growth, high competition industry, one would desire a high level of cash return to shareholders, and low level of investment. This has not been the case of KOP, which has consistently spent more in CAPEX than depreciation, has done acquisitions, and has only recently started paying a $0.05 quarterly dividend (yielding less than 1%).

Financially the company was not extremely strong, with a small cash reserve of $45 million against notes for $500 million maturing in 2025 and paying 6% and a credit facility for $800 million ($326 million drawn as of 3Q22) paying SOFR + 1.25%.

For a company like this, showing no growth and returning little cash, I believe the investor should ask for a significant return on the average of the company's earnings across the cycle. These are shown below. Considering a minimum 10% required return, we arrive towards a market cap of between $360 and $420 million. When I wrote the article in July, KOP traded at a market cap close to $480 million and now trades close to $580 million.

Recent developments

Not much has happened in the last two quarters that make me change my understanding of KOP's long-term drivers and my assessment of its value.

At the general level, the company's revenues have increased substantially but operating income has fallen behind, albeit, depending on the quarters compared.

The distribution of revenues and earnings is interesting though. While the PC and RUPS segments have shown trouble growing profits above FY21 levels, with PC falling substantially at the EBITDA level, the CMC segment is showing an important increase in profits and revenues. This has been normal during other periods, when some of KOP's segments move in opposite directions in their industry's cycles.

KOP's 3Q22 10-Q report filed with the SEC

{kind=link}

The problem with this is that as the commentary of the previous section indicated, the CMC segment is the most cyclical and also the least desirable in terms of long-term perspectives. According to the company's management commentary in the 2Q22 and 3Q22 earnings calls, the segment's overperformance is tied to supply constraints around creosote and its input, tar coal, generated by the war in Ukraine. This means we are talking of a purely supply driven peak in prices that is not necessarily sustainable.

In terms of capital allocation, KOP announced a $0.05 quarterly dividend in 2Q22. However, the company continues doing acquisitions (a $15 million acquisition in 4Q22) and purchasing net capital (CAPEX is 50% above depreciation). Most importantly, both acquisitions and CAPEX are concentrated on the lowest margin RUPS segment.

Conclusions

I believe KOP is a low quality business participating in cyclical industries. On top of that, I am not happy with management's capital allocation decisions. As such, I would only consider investing in KOP if it traded offering more than a 10% return on its average earnings (either net income or FCF) across the two portions of the latest cycle.

In this case, the stock has moved in the opposite direction, meaning that KOP is more expensive than before. Fundamentals have not improved to justify these movements. If any, fundamentals may show signs of a reverting cycle in at least some of KOP's markets (PC in particular).

For these reasons, I still believe KOP is not an opportunity, and recommend waiting for further developments, or for the stock to return to cheaper levels before considering investing.

For further details see:

Koppers Holdings: Signs Of Deterioration In Q3 Earnings