KOP - Koppers Holdings: Things Are Starting To Improve But Risks Remain High

2023-06-15 03:57:06 ET

Summary

- Koppers Holdings has raised the price of its products, and sales increased as a consequence.

- Margins have also recently improved boosted by these price increases.

- KOP carries significant debt and interest expenses are increasing at worrying levels.

- The dividend is at risk as cash from operations has recently declined.

- Headwinds seem to be temporary by nature, but there are significant risks associated with investing in Koppers Holdings, and potential investors should carefully consider these factors before making a decision.

Investment thesis

Koppers Holdings' ( KOP ) prospects have recently deteriorated due to rising interest expenses as a consequence of increased debt due to recent acquisitions and inflationary pressures and supply chain issues as margins have shrunk from 2021 to 2022. Furthermore, the macroeconomic outlook does not give rise to optimism as recent interest rate hikes seem to be putting the global economy at risk of a relatively deep recession at a time when the company is spending vast amounts of cash investing in growth and reducing workplace accidents.

Even so, profit margins have begun to improve in the first quarter of 2023 thanks to a significant increase in the price of the company's products and good maintenance of volumes, which makes me believe that the current pessimism among investors represents a good opportunity to obtain relatively high capital gains once the current macroeconomic landscape improves. Still, much remains to be done as the management needs to convert part of the company's inventories into actual cash while keeping expenses as low as possible. If we add this to the risk of recession, my advice is to use a cost-averaging strategy as a way to reduce risks as volatility could remain high in the short and medium term.

A brief overview of the company

Koppers Holdings is a global provider of treated wood products, wood preservation chemicals, and carbon compounds for the railroad, specialty chemical, utility, residential lumber, agriculture, aluminum, steel, rubber, and construction industries. The company was founded in 1988 and its market cap currently stands at $700 million, employing over 2,000 workers worldwide.

Koppers Holdings logo (Koppers.com)

The company operates under three main business segments: Railroad and Utility Products and Services, Performance Chemicals, and Carbon Materials and Chemicals. Under the Railroad and Utility Products and Services segment, which provided 40% of the company's net sales in 2022, the company sells treated and untreated wood products, rail joint bars and services to the railroad markets in the United States and Canada, and treated wood products and services to the utility markets in the United States and Australia. Under the Performance Chemicals segment, which provided 29% of the company's net sales in 2022, the company provides copper-based wood preservatives, including micronized copper azole, micronized pigments, alkaline copper quaternary, amine copper azole, dichloro-octyl-isothiazolinone, and chromated copper arsenate mainly for decking, fencing, utility poles, construction lumber and timbers, as well as various agricultural uses. And under the Carbon Materials and Chemicals , which provided 31% of the company's net sales in 2022, the company manufactures creosote, carbon pitch, naphthalene, and phthalic anhydride.

Currently, shares are trading at $33.80, which represents a 34.75% decline from all-time highs of $51.80 on November 9, 2017. This represents a significant decline as investors remain cautious due to recent margin contraction as a consequence of inflationary pressures and supply chain issues amidst a potential recession due to recent interest rate hikes, which I believe represents a good opportunity for those investors with enough patience interested in obtaining capital gains once the current macroeconomic context improves. Still, given that the company is highly cyclical as the share price demonstrates, I strongly advise averaging down due to the current turmoil in the global economy. But even so, the company has grown in recent years thanks to its latest actions, although it will need to deleverage its balance sheet for this growth to reflect in the share price.

Acquisitions and divestitures

The company has historically grown through significant acquisitions. After partially deleveraging the balance sheet by paying down over $200 million of long-term debt in order to digest the acquisition of Osmose carried out in 2014, which costed $494 million, the company entered the North American utility pole market in 2018 with the acquisition of Cox Industries and M.A. Energy Resources for $264 million.

More recently, in September 2020, the company sold Koppers (Jiangsu) Carbon Chemical Company Limited for $107 million. Later, in November 2020, the company bought a city-owned tract of industrial land adjacent to its Rock Hill, South Carolina, facility, in order to expand operations in the area.

Later, in April 2022, the company sold its utility pole treating facility in Sweetwater, Tennessee, in order to reduce underutilized capacity, after divesting its facility in Denver, Colorado in October 2021, and its facility in Follansbee, West Virginia in February 2021.

In November 2022, the company acquired Gross & Janes, the largest independent supplier of untreated railroad crossties in North America with annual revenues of ~$50 million, for $15.5 million. During the same month, it also acquired a 105-acre property in Leesville, Louisiana to expand the peeling and drying capacity used in the Koppers wood treatment process.

And the latest acquisition took place in January 2023, the company completed the acquisition of a 70-acre property in Glendale, Oregon, in order to optimize the Performance Chemicals distribution network and expand wood treating capabilities to the West Coast.

Net sales are taking off boosted by price raises

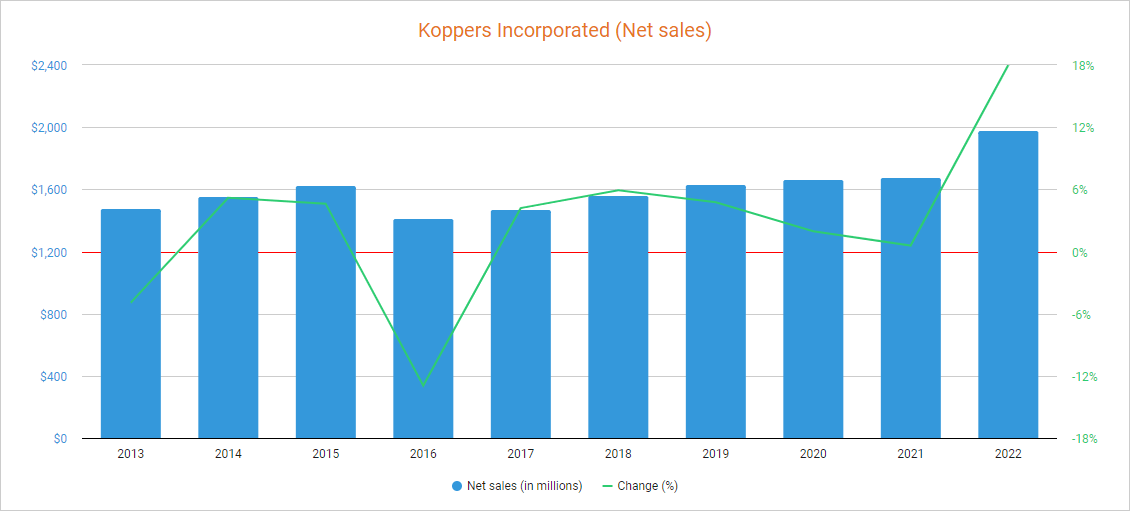

Boosted by acquisitions, the company has historically grown its sales, albeit at a slow pace, but sales seem to have started to pick up since 2022 as net sales increased by 17.99% compared to 2021 to $1.98 billion due to price raises to offset increased production costs due to inflationary pressures.

{kind=link}

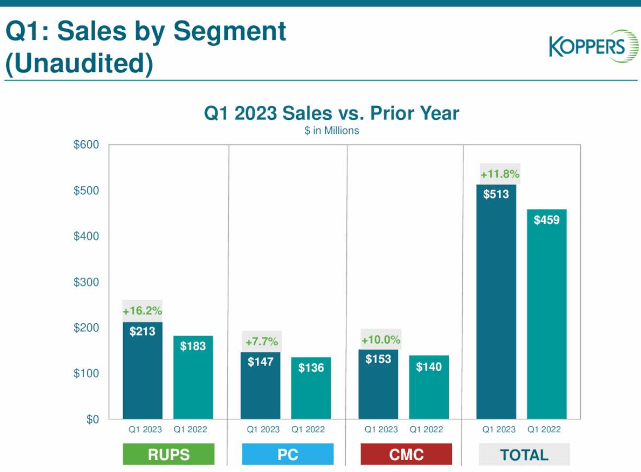

More specifically, net sales increased by 12.71% year over year during the first quarter of 2022, by 13.95% during the second quarter, 26.20% during the third quarter, and by 19.07% during the fourth quarter. The positive trend has continued through the first quarter of 2023 as net sales increased by 11.78% compared to the same quarter of 2022 to $513 million, boosted by price increases.

Koppers Q1 sales growth (Q1 2023 Earnings Call presentation)

{kind=link}

In this regard, the Railroad and Utility Products and Services segment was the business that grew the most in the first quarter of 2023 as it saw its sales grow by 16.2%. The rest of the business areas also saw strong growth as the Performance Chemicals segment reported sales growth of 7.7%, and the Carbon Materials and Chemicals by 10.0%. In February 2020, the company announced its plans to enter the copper naphthenate wood preservative market, and the company recently managed to raise prices while maintaining healthy volumes. Furthermore, sales are expected to increase by 6.57% in 2023, and by a further 1.42% in 2024. But the recent share price decline despite increasing sales has caused a significant decline in the P/S ratio to 0.353, which means that the company generates $2.83 in net sales for each dollar held in shares by investors, annually.

This ratio is 16.55% lower than the average of the past 10 years and represents a 55.03% decline from decade-highs of 0.785, which reflects growing pessimism among investors as net debt significantly increased due to recent acquisitions while margins are showing strong volatility despite recent improvements.

Margins are showing strong signs of stabilization

The company has managed to maintain positive gross profit and EBITDA margins over the years, which has enabled the continuous generation of positive cash from operations. Recently, inflationary pressures and supply chain issues have produced a significant contraction in said margins, and currently, the trailing twelve months' gross profit margin stands at 17.68%, and the EBITDA margin at 10.19% as a consequence. Prior to that, the company was improving its profitability thanks to some restructuring, and margins currently stand at relatively acceptable levels despite headwinds thanks to these efforts.

Furthermore, both gross profit and EBITDA margins showed strong signs of improvement during the first quarter of 2023 as they stood at 20.28% and 12.49%, respectively, and the company achieved a record EBITDA of $62.5 million for the quarter. This is why I consider the state of Kopper's operations to be relatively healthy at this point despite the current complex macroeconomic picture. The problem is that a potential recession as a consequence of the recent interest rate hikes would not only have an impact on sales but also on margins as a consequence of unabsorbed labor produced by declining volumes, and this would be a problem especially for Koppers Holdings as the company's debt is at high levels due to the acquisitions carried out in recent years.

The company needs to deleverage its balance sheet

The company has taken on significant debt as a result of the acquisitions carried out in recent years, and the long-term debt currently stands at $881 million as a consequence. At the same time, the cash and equivalents are very low at $46.40 million.

This means that the company may need to continue borrowing cash to carry out its (temporarily) strong capital expenditures, which are expected to reach $110-$120 million in 2023, and cover its current dividend and share repurchase program, as well as interest expenses of over $50 million as they were $14 million during the first quarter of 2023.

During the earnings call conference of the first quarter of 2023, the management stated that its long-term net leverage ratio target is 2x to 3x, whereas the company reported a leverage ratio of 3.5x during the first quarter of 2023, which means deleveraging the balance sheet is among the plans of the management. In addition, inventories are unusually high at $379.20 million as the company produces inventory at a rate in excess of sales (although much of this increase is attributable to the recent increase in the price of its products).

Considering that interest expenses and capital expenditures will exceed $150 million this year, the company will struggle to cover all of its expenses and generate excess cash as increasing inventories reflect its struggles to sell all of the products it currently manufactures while cash from operations typically sits slightly above $100 million. Therefore, it will be necessary for the company to reduce its production capacity for a fairly sustained period of time in order to convert these inventories into actual cash, with the risk that this could lead to a deterioration in profit margins as a consequence of unabsorbed labor. Still, we must not forget that a big portion of capital expenditures are temporary as the company is aggressively investing in workers' safety and growth.

The dividend is at risk

The company reinstated the quarterly dividend (which was canceled in 2014) during the first quarter of 2022 at $0.05 per share and raised it by 20% to $0.06 in February 2023. Considering the current share price of $33.80, the dividend yield currently stands at just 0.71% as the company pays over ten times more interest expenses than dividends due to its high debt pile.

This means that, in the long term, the current dividend has very high growth potential as the company could increase it as the long-term debt shrinks, but unfortunately, the risks for the short and medium term are too high as a consequence of excessively high interest expenses that are taking the cash payout ratio to unsustainable levels due to the high capex that the company must assume in the coming quarters. In the following table, I have calculated the percentage of cash from operations that the company has dedicated each year to cover its interest expenses, and in 2022 I have added dividend expenses to calculate its sustainability through actual operations.

| Year |

| 2014 |

| 2015 |

| 2016 |

| 2017 |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| Cash from operations (in millions) |

| $35.5 |

| $127.7 |

| $119.5 |

| $101.8 |

| $84.5 |

| $117.8 |

| $127.8 |

| $103.0 |

| $102.3 |

| Interest expenses (in millions) |

| $39.1 |

| $50.7 |

| $50.8 |

| $42.5 |

| $56.3 |

| $62.5 |

| $48.9 |

| $40.5 |

| $44.8 |

| Dividends paid (in millions) |

| $0 |

| $0 |

| $0 |

| $0 |

| $0 |

| $0 |

| $0 |

| $0 |

| $4.2 |

| Cash payout ratio |

| 110.14% |

| 39.70% |

| 42.51% |

| 41.75% |

| 66.63% |

| 53.06% |

| 38.26% |

| 39.32% |

| 49.00% |

As one can see, annual interest expenses of over $40 million are ten times higher than annual dividends of over $4 million, which left a cash payout ratio of 49.00% in 2022 despite such a low dividend yield. Furthermore, interest expenses are expected to surpass the $55 million mark in 2023 as a consequence of recent increases, which puts the current dividend at risk as the company is very capital-intensive. In this regard, a cash payout ratio dancing at around 50% would not be a problem if it were not for the very high capital expenditures that are expected for this year, as well as the high capital expenditures that the company has experienced over the years.

Cash from operations was -$15.3 million during the first quarter of 2023 being a quarter in which the company typically builds working capital for the rest of the year (cash from operations was -$8.0 million during the same quarter of 2022, and -$7.4 million during the same quarter of 2021). Currently, trailing twelve months' cash from operations stands at $95 million, and capital expenditures skyrocketed to $109.5 million, of which 39% is allocated to maintenance, 23% to the company's Zero Harm initiative (whose objective is to significantly reduce the risks to the health of workers), and 38% to growth and productivity (using the first quarter of 2023 as reference) as the company keeps expanding its product portfolio.

With this cash generation capacity, the company will hardly be able to cover dividends of over $4 million, interest expenses of over $55 million, and capital expenditures that are expected to exceed $100 million in 2023, a fact that makes me believe that the dividend is in danger. In the long term, the situation is expected to slightly improve as the recent increase in sales due to inflation, as well as forecasted sales growth, should gradually dilute the company's debt (if it doesn't keep rising, of course), but for the short and medium term, the company will have to tighten its belt by reducing discretionary spending, partially empty inventories by reducing production capacity, and keep capital expenditures as low as possible once ongoing projects conclude. Of course, it is very likely that the pace of share repurchases will slow significantly or even pause in order to meet the company's fixed expenses and investments.

Buybacks could be paused in the immediate future

The company announced a massive share repurchase program of $100 million in August 2021 with no expiration date, and bought back almost $6 million worth of shares during the first quarter of 2023, which means buyback efforts remain in force. With this, management has managed to undo some of the dilution that has taken place in recent years.

But despite this recent decline in the total number of shares outstanding, I believe the pace of share buybacks could slow significantly or even stop completely due to the recent squeeze in profit margins, the recent hike in interest expenses, and the high capital expenditures that the management expects for 2023.

Risks worth mentioning

It is clear that the current picture of Koppers Holdings is quite delicate, and that is why I would like to highlight the risks that I consider to be most important in the short and medium term.

- Profit margins could deteriorate again if inflationary pressures and supply chain issues continue to be part of the macroeconomic landscape for longer, or (especially) if they intensify. This would have a direct impact on cash from operations, which would force the company to continue borrowing.

- The global economy could imminently face a significant recession as a consequence of recent interest rate hikes carried out to combat high inflation rates, which could have a significant impact on the demand for the company's products and, therefore, serious difficulties in converting inventories into cash. Additionally, unabsorbed labor from lower demand could represent a significant headwind if the company fails to reduce production capacity (workforce) in time in a recessionary environment.

- Due to high interest expenses, the company could find it difficult to maintain its dividend if cash from operations suffers a further contraction. In this scenario, the current share repurchase program would also be at risk of being paused or even canceled.

- It is very likely that, in the short and medium term, the company will need to borrow more cash to carry out the investments it has planned for this year, and if it fails to reduce its discretionary expenses, production capacity, and capital expenditures (once ongoing projects finish), it may need to continue borrowing for longer than expected.

Conclusion

It is clear that the situation is not looking very promising for Koppers Holdings in the short and medium term, which is why the share price has fallen 34.75% from all-time highs despite rising sales, which is why the P/S ratio currently stands 55.03% below the peak experienced in 2017. Rising interest expenses at a time of high volatility in profit margins as a result of inflationary pressures and supply chain issues amidst a potential recession due to recent interest rate hikes is keeping investors wary.

Despite this, I view the recent drop in the share price as a good opportunity to get relatively high capital returns once the current landscape improves as margins have improved recently, high capital expenditures are mostly temporary as only 39% of they were allocated for operational maintenance during the first quarter of 2023, and inflationary pressures and supply chain issues are temporary by nature. Furthermore, the company has very high inventories, although it could find it difficult to empty them due to the risk of a recession that could negatively affect demand. It is this risk of a potential recession, as well as global economic instability in general (and the market volatility derived from it), that I believe that averaging down would be a wiser strategy going forward.

For further details see:

Koppers Holdings: Things Are Starting To Improve, But Risks Remain High