TNET - Korn Ferry: A Little More Upside Is On The Table

Summary

- Korn Ferry has done really well as of late, though there are signs of weakening ahead, with management even taking bold steps now to mitigate any future pain.

- This makes valuing the enterprise a challenge, and investors would be wise to assume that profits and cash flows will eventually weaken.

- Even so, shares are attractively priced compared to similar firms, and it looks as though some additional upside exists.

Sometimes, it can take a great deal of time to generate returns that, in the aggregate, outperform the broader market. Other times, however, such outperformance can occur rather quickly. An example of the latter taking place can be seen by looking at Korn Ferry ( KFY ), an enterprise that provides, amongst other things, consulting services, human resources activities, and data analytics. In recent months, shares have risen nicely, driven by robust topline results and mixed but generally positive cash flow data. In the near term, it does look as though the picture might change, however. Management is even taking steps early on with the hope of mitigating any pain caused by deteriorating market conditions. This on its own may cause some investors to be wary of the company. But given its overall fundamental health, I do believe that some additional upside is on the table. As such, I've decided to keep the 'buy' rating I assigned the stock previously, with the caveat that the easy money has almost certainly been made.

Good times won't continue

In late September 2022, I wrote an article discussing the investment worthiness of Korn Ferry. In that article, I talked about how the company's shares had experienced a bit of downside over the prior few months, even at a time when fundamental strength was undeniably impressive. Investors were assigning a great deal of probability to the downside in the stock because of changing market conditions. I acknowledged that this made sense at the time, but even with a scenario where fundamental performance did worsen, I had a hard time believing that shares would be overvalued. All of this led me to keep the 'buy' rating I had on the stock, a rating that reflected my belief that shares should outperform the broader market for the foreseeable future. Since then, that's exactly what happened. While the S&P 500 is up 12.3%, shares of Korn Ferry have generated a return for investors of 20.3%.

{kind=link}

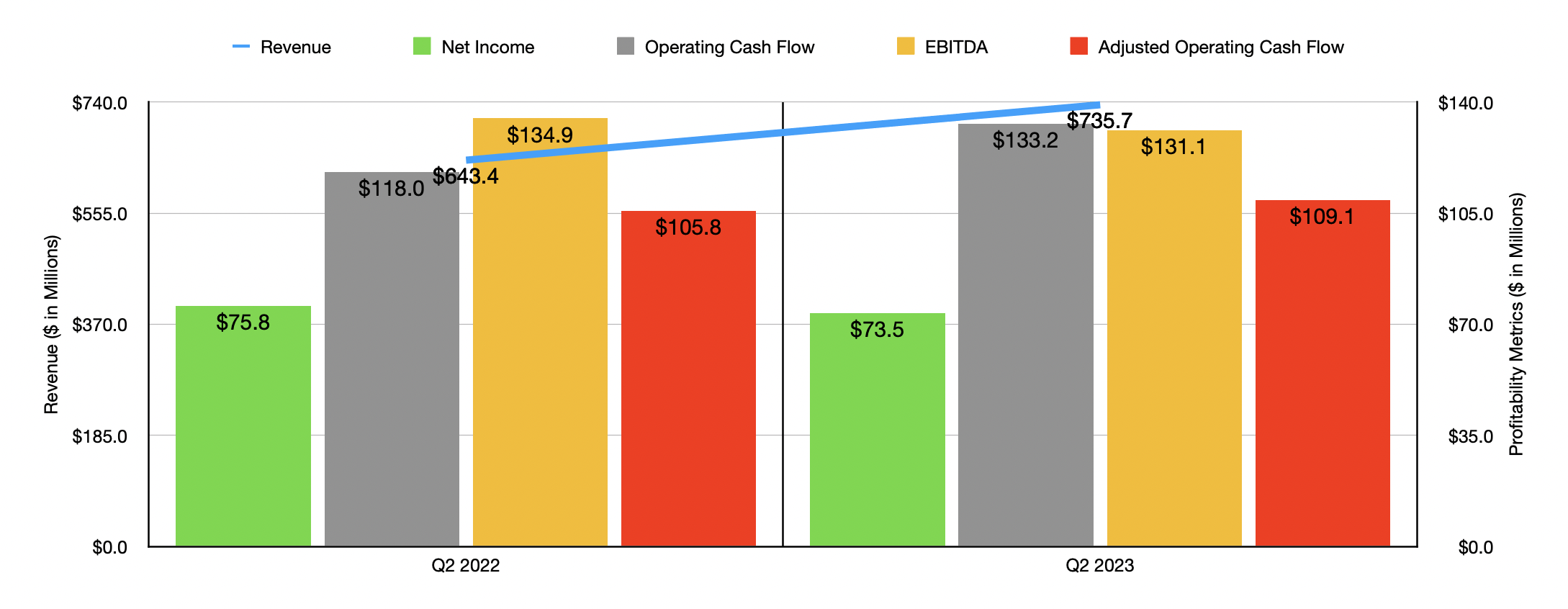

When I last wrote about the company, we only had data covering through the first quarter of its 2023 fiscal year. Fast-forward to today, and that data now extends through the second quarter . During that time, sales came in at $735.7 million. That's 14.3% higher than the $643.4 million generated one year earlier. The greatest revenue rise came from its Professional Search & Interim operations, with revenue spiking from $54.6 million to $134.7 million. This increase, management said, was due largely to businesses that the company acquired. Interim fee revenue associated with acquired companies added $55.3 million to the company's topline, while permanent placement fee revenue of those same companies contributed $24.9 million. RPO revenue, meanwhile, shot up from $95.9 million to $107.3 million. This, management said, was thanks to the wider adoption of RPO services in the market in combination with the company's differentiated solutions. What's really impressive is that sales growth would have been higher here had it not been for $6.1 million in impact associated with foreign currency fluctuations.

Just because sales increased, does not mean that everything for the company was great. Yes, we did also see both Consulting and Digital revenues rise year over year. However, total revenue associated with Executive Search managed to fall by 7.3%, dropping from $235.5 million to $218.4 million. Based on the data provided, this weakness was visible in both North America and the Asia Pacific region, with the latter being hit not only by a 13% decrease in the number of engagements billed but also to the tune of $2.4 million from foreign currency fluctuations. A 14% decrease in the number of engagements billed, partially offset by a 5% rise in the weighted average fee billed per engagement, was present in the North American market.

On the bottom line, the picture was somewhat mixed. Net income dipped from $75.8 million down to $73.5 million. On the other hand, operating cash flow improved, rising from $118 million to $133.2 million. On an adjusted basis where we ignore changes in working capital, the increase would have been more modest from $105.8 million to $109.1 million. But even during this time, EBITDA for the company fell slightly from $134.9 million to $131.1 million. Affecting the bottom line for the company was a roughly 8% increase in total compensation and benefits expenses. Given the tight labor market, this is no surprise. Other costs were also higher year over year, such as general and administrative expenses.

{kind=link}

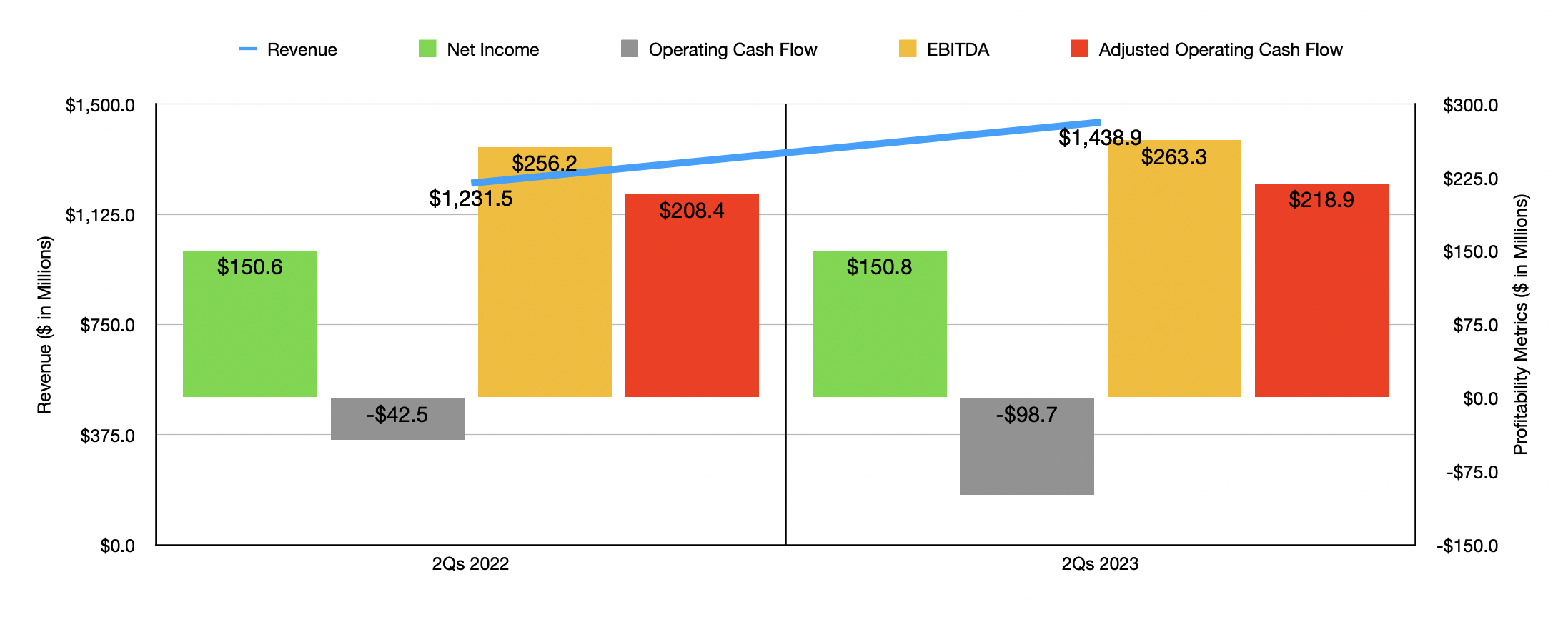

When it comes to the first half of 2023 as a whole, the picture for the company was still mixed. Revenue, for instance, was quite strong, having risen from $1.23 billion during the first half of 2022 to $1.44 billion in the first half of 2023. Net income inched up from $150.6 million to $150.8 million. At the same time, however, operating cash flow worsened from negative $42.5 million to negative $98.7 million. On an adjusted basis, on the other hand, the metric actually rose from $208.4 million to $218.9 million, while EBITDA expanded from $256.2 million to $263.3 million.

Although the picture for the first half of 2023 looked upbeat, management did have some warnings for shareholders. Due to broader economic concerns, the company decided to initiate a plan aimed at reducing run rate expenses by between $45 million and $55 million. They don't expect to see any material improvement on the bottom line until at least the final quarter of 2023. The company also forecasted some financial results for the third quarter that's coming up. Fee revenue should be between $660 million and $690 million. At the midpoint, that would translate to a decrease compared to the $680.7 million reported one year earlier. At the midpoint, the company anticipates EBITDA of roughly $98.5 million, while earnings per share should be between $0.88 and $1. To put this in perspective, EBITDA in the third quarter of the 2022 fiscal year came in at $138.3 million, while earnings per share totaled $1.59. It's also worth noting at this point that, for the third quarter, analysts anticipate revenue of just under $667 million, while earnings per share should be $0.77 and adjusted earnings per share should total $0.91.

{kind=link}

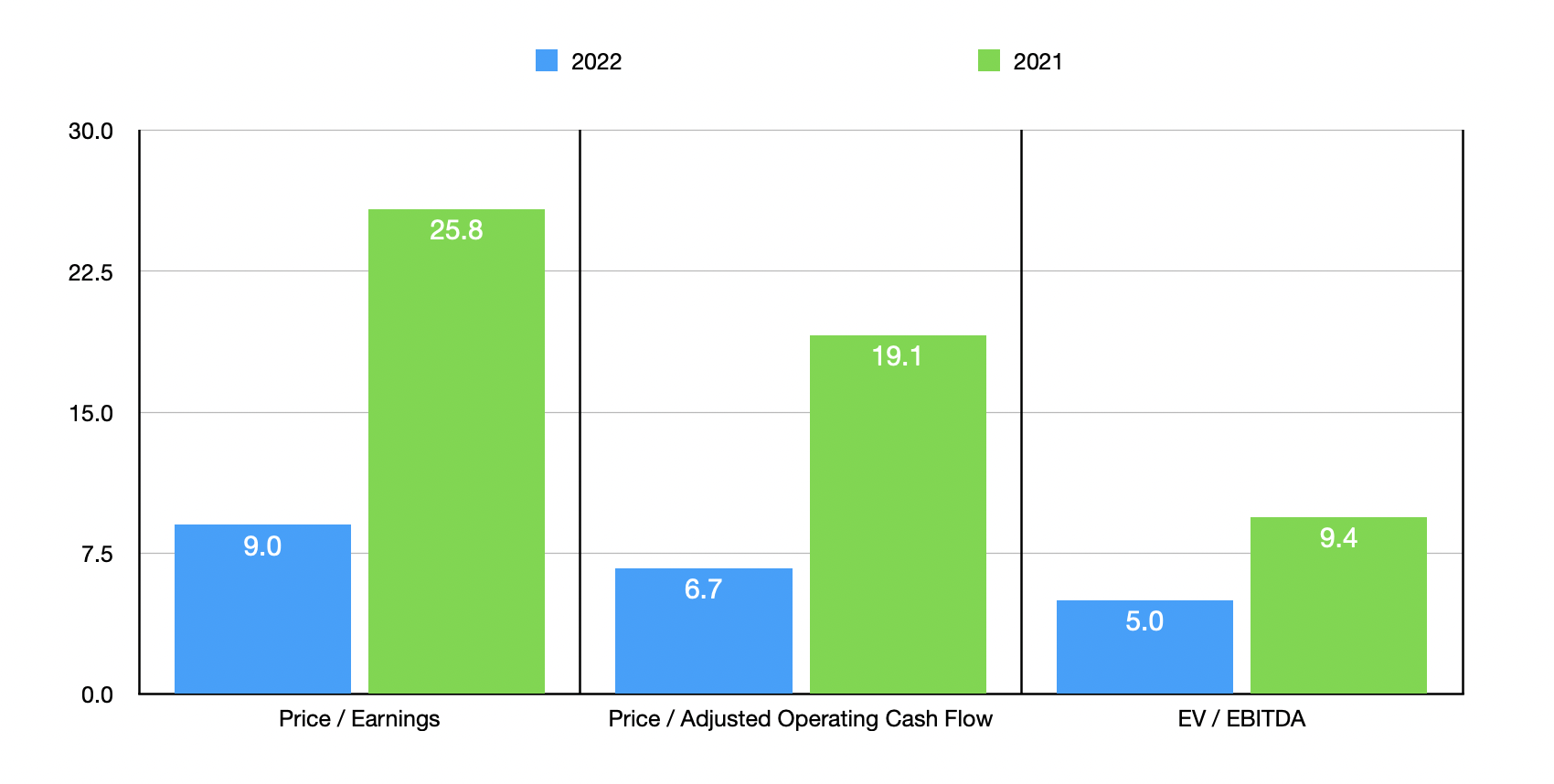

Normally, I like to project out what the financial picture for a company might look like for the rest of its current fiscal year. But given the concerns expressed by management and their cost-cutting initiatives, I believe a better option is to just look at historical financial data and value the company that way. Using data from the 2022 fiscal year, shares of the business are trading at pretty low levels. On a price-to-earnings basis, the multiple should be around 9.0. Using the price to adjusted operating cash flow approach, the multiple is even lower at 6.7, while the EV to EBITDA approach gives me a reading of 5.0. Now, in the event that financial performance was to revert back to what the company experienced in 2021, shares would look a bit pricier. In this case, these multiples would be 25.8, 19.1, and 9.4, respectively. As part of my analysis, I also compared Korn Ferry to five similar firms. On a price-to-earnings basis, these companies ranged from a low of 12.5 to a high of 25.8. Using the price to operating cash flow approach, the range would be from 11.0 to 16.6. And when it comes to the EV to EBITDA approach, it would be from 7.0 to 13.7. In all three scenarios, Korn Ferry was the cheapest of the group.

| Company |

| Price/Earnings |

| Price/Operating Cash Flow |

| EV/EBITDA |

| Korn Ferry |

| 9.0 |

| 6.7 |

| 5.0 |

| Insperity ( NSP ) |

| 25.8 |

| 13.2 |

| 13.7 |

| ManpowerGroup ( MAN ) |

| 12.5 |

| 11.0 |

| 7.0 |

| Kforce ( KFRC ) |

| 16.7 |

| 12.5 |

| 10.5 |

| TriNet ( TNET ) |

| 13.7 |

| 16.6 |

| 7.5 |

| Robert Half International ( RHI ) |

| 13.9 |

| 13.4 |

| 8.2 |

Takeaway

At this time, it looks as though the fundamental condition of Korn Ferry is set to worsen in the near term. This comes after a couple of mixed but solid quarters. In the event that the business reverts back to the levels of profitability seen in 2021, I would make the case that the business is closer to being fairly valued than undervalued. But it does have a couple of other great things going for it. For starters, the cost-cutting initiatives, if successful, will help to alleviate any pain the business experiences. Second, it does have cash in excess of debt that totals $257.3 million. That gives it a great deal of flexibility for difficult times. And finally, at present at least, shares are cheap relative to similar firms. This establishes it as a favorable risk-to-reward prospect in its space. All of this combined makes me feel comfortable keeping the company rated a 'buy', but with the acknowledgment that an upside from here will be a lot harder than what it was previously.

For further details see:

Korn Ferry: A Little More Upside Is On The Table