KFY - Korn Ferry: DCF Approach Close To An Entry But Volatility Demands Patience

Summary

- Korn Ferry showed phenomenal growth in four revenue segments in FY2022.

- What will happen to the company’s growth if we see a recession in the next 12 months?

- A conservative 10-year DCF analysis considering negative growth for 2023 and 2024 and subsequent recovery points to patience, and the Korn Ferry entry point is close.

Investment Thesis

After forecasting the financial statements of Korn Ferry ( KFY ), assuming conservative revenue growth for the next 10 years, my discounted cash flow ("DCF") analysis and the current market situation tell me to wait before investing in this company. The valuation is very close to an entry point for long-term investors and patience is key here.

The impending recession in the U.S. has everyone up in arms, but so far, we are not seeing anything giving, especially the unemployment number, which keeps ticking down month-over-month, sending signals to the markets that the Fed will continue to be hawkish in their policy. I decided to have a look at what would happen if in the next 12 months, we will finally see the unemployment rate tick up and we would enter a recession. How would recruiting companies like Korn Ferry be affected? Is Korn Ferry resilient to higher unemployment or will the company be drastically affected by less demand for their services? I believe that the company is not going to be affected as much as other recruitment companies because of how diversified they are in their revenue segments.

In this article, I will look into the company's strengths and the historical performance of its four different revenue segments to see if some are more resilient than others to a downturn in the economy. I believe that the company is well-equipped for a downturn, as it is not just a recruiting company at its core and offers a wide variety of consulting services such as leadership development and organizational consulting, which help companies retain top talent.

Based on research and analysis, I have come up with reasonable and conservative growth assumptions for the company. I am conservative with my assumptions, as I want to have a decent margin of safety, and when the conservative estimates still tell me that the company is undervalued, that means it is a good investment in the long run.

Main Revenue Segments and Future Potential

Korn Ferry has four main revenue segments within the consulting and recruiting space. Consulting revenues, Digital revenues, Executive Search, and RPO and Professional. Executive search has been the highest revenue generator for the company for at least 5 years, averaging around 37% of total revenues, with consulting and RPO revenues taking around 25% each and Digital taking the rest.

Executive Search

Let's start with the largest contributor, and the one I believe will be affected the least by a recession. I think that companies will be more cautious in terms of hiring and will prioritize hiring only for critical roles in the company or leadership positions if we do see a recession. This will lead to an increased demand for executive search to find the best talent.

Furthermore, I believe this segment will be more resilient to an economic downturn because companies will hire for long-term strategic goals rather than short-term operational objectives. If a company would like to get back into future growth and increase profits, it will hire someone who is going to turn the ship around and achieve results. Companies may be willing to invest in the recruitment of top talent even during a recession if they believe this is going to improve their position in the long run.

Looking at the numbers in the segment, 2019 to 2021 saw quite disappointing results in terms of growth. From 2019 to 2020 the segment had -5% growth and -13% growth the next year only to come back very strong in FY2022 with a whopping 47% increase. We can see that the pandemic has affected this segment quite a bit, especially when the unemployment rate spiked to 14.7% when everything shut down globally.

Although the numbers tell us that there was much less demand for C-level positions and the revenue has gone down during the tough times, I believe that the pandemic-induced recession is very different from a recession that is supposedly on the horizon. It made sense not to hire any C-level executives then because no one was hired at all pretty much. When the next recession hits, I believe we will see a lot of changes in management in many companies which will keep the demand for these services high.

If we believe that the recession comes within the next year, my growth assumptions for this segment are -10% for 2023 and -8% for 2024, assuming that the recession isn’t very severe and that in 2024 the demand will pick back up and get back to growth in 2025, but not at the levels the company saw in 2022.

RPO and Professional

This segment is quite an interesting one, due to how quickly it grew y-o-y to become the second-highest revenue generator for the company. For the last couple of years, it was earning around $300m and then in FY22 it saw an 87% increase in revenue, beating out Consulting Revenues by a small margin. The massive increase in revenue in this segment was due to more companies adopting recruitment process outsourcing as their main way of acquiring new talent and Korn Ferry has solid expertise in the area. Furthermore, they are acquiring more companies that will synergize well with its current offerings. In FY22 they acquired The Lucas Group and Patina Solutions Group which will enhance the company’s interim expertise and professional search portfolio.

As for the future of this segment, I am positive that it will continue to perform well, as one of the company’s main strategy points is to “Pursue Transformational M&A Opportunities at the Intersection of Talent and Strategy.” With the mentioned groups acquired in FY22, I believe they will continue to seek other firms to enhance their quality portfolio and establish themselves as the main player in C-suite professional search area.

Just like with the Executive Search, I will model slightly negative growth for the next two years (-5%, -5%) just to be safe, even though, the segment has not seen a decline even during 2020 and 2021. I could also see this segment becoming the best-performing segment for the company in the future if the company can acquire more strategic opportunities and even wider adoption of RPO.

Consulting Revenues and Digital Revenues

I decided to pool these two together, as they are quite closely aligned. Both segments performed well during FY22, just like the other segments did. Consulting revenue increased 26% y-o-y and digital had an increase of 21.5%, while 34% of total digital revenues came from the Consulting Segment.

Both of the segments saw declines the year before and bounced back quite considerably. Consulting segment deals with everything around the client's organization, mainly the company itself in terms of enhancing performance, culture, and people to drive growth with four main objectives to achieve organic growth: Organization Strategy, Assessment and Succession, Leadership and Professional Development, and Total Rewards.

Digital is a tech-enabled solution that helps clients to find the best structures, and roles and find the best strategy through data analytics which will help the organizations move forward and grow. As more and more companies adopt technology into their strategies, digital and consulting revenues will see higher growth and I do believe these segments will continue to grow at healthy double-digit numbers year over year, but just to be conservative yet again, I will model negative growth for the next two years.

Overall, I am very optimistic that all the main segments will do great in the future, as the company is quite different from an ordinary recruiting company because it provides services for top management recruitment, data analytics solutions coupled with consulting strategies, which tells me that the company is very well diversified in all the aspects of a corporation, not just talent acquisition.

Financials

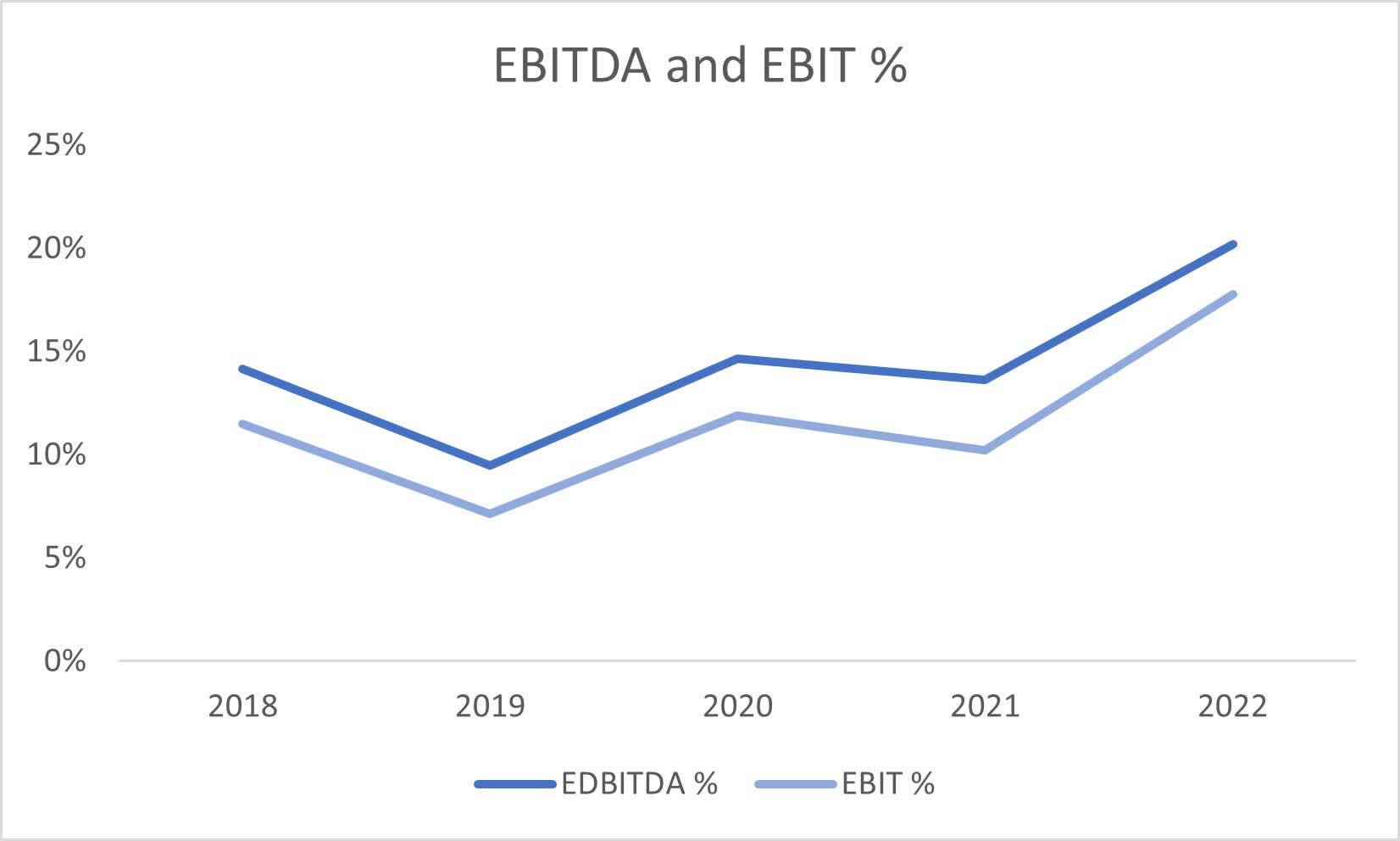

Gross Margins have been around 95% because they have a very low cost of goods sold associated with producing or acquiring products. Their main expenses come through operating expenses, mainly compensation, and benefits. EBIT and EBITDA Margins have been growing steadily and are very healthy. I’d like to see the company continue what they are doing currently, as it does seem to be working. If we do see a recession coming in the next 12 months, I would expect a dip in these two metrics, however, I don’t expect the dips to be very large.

{kind=link}

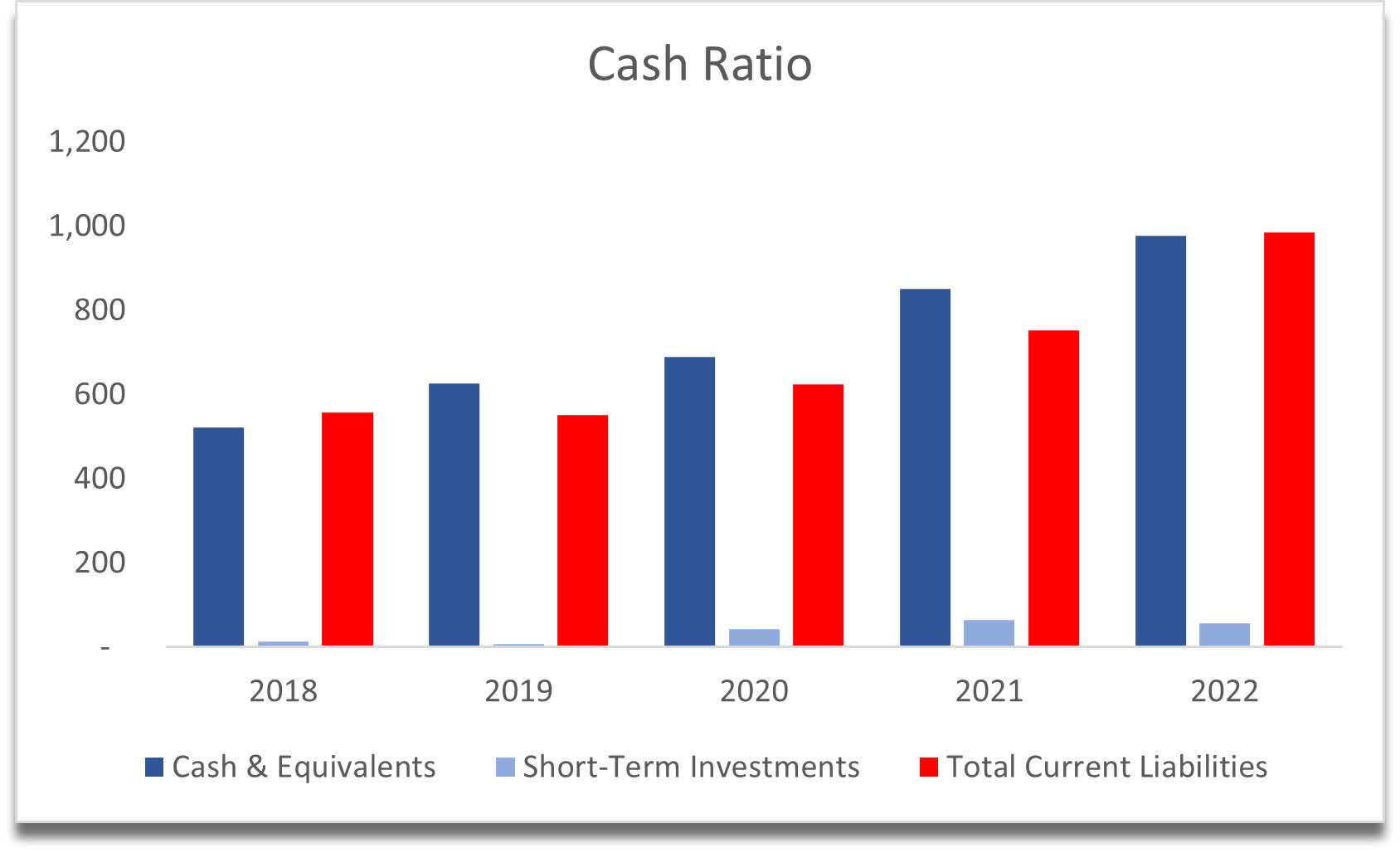

A lot of companies that I look at are not able to cover their short-term obligations with cash on hand and short-term investments. Here, the company is just about able to, which is a good sign. The cash ratio is a much stricter way of looking at the company's liquidity. I do not see any liquidity problems in the future.

{kind=link}

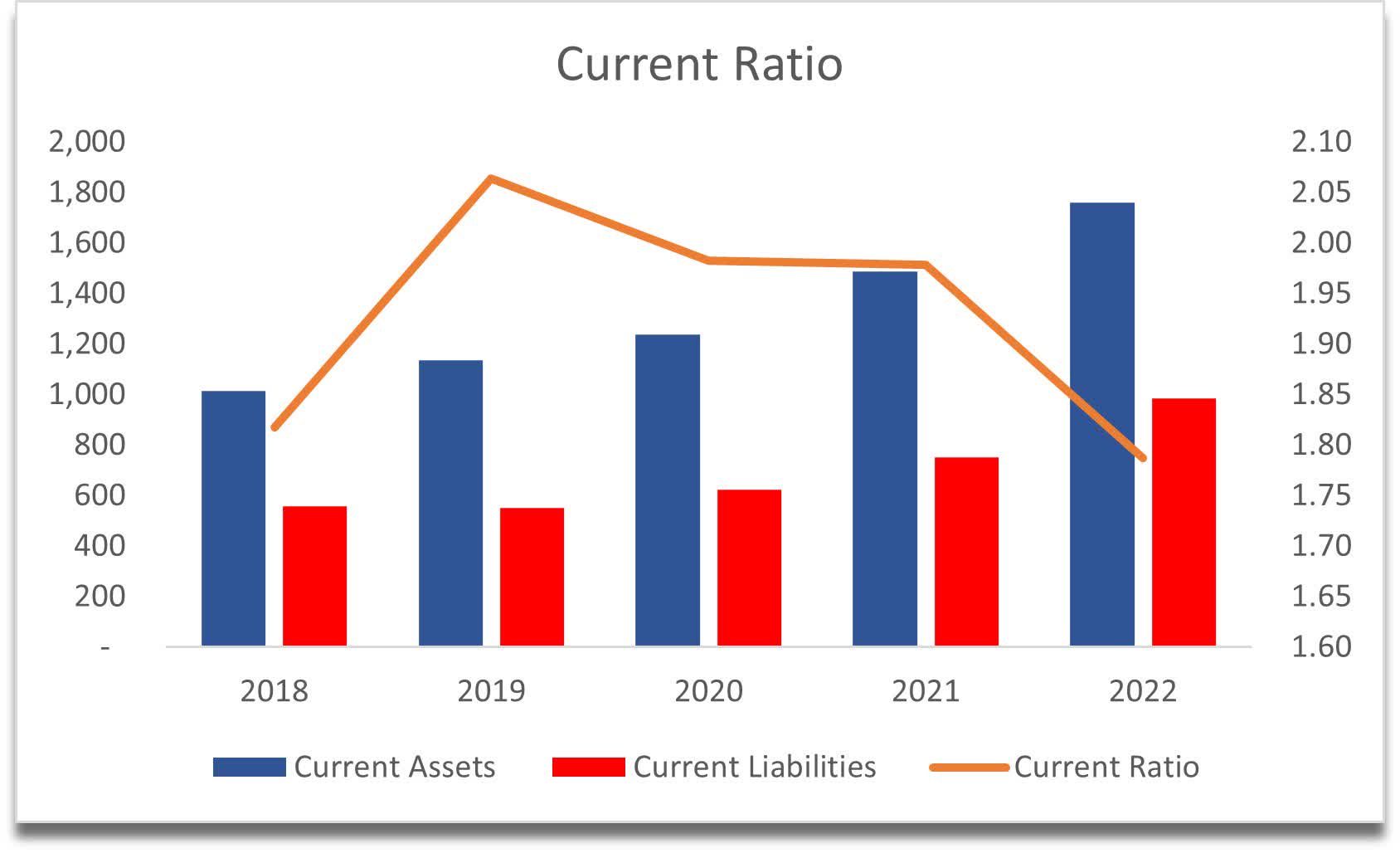

To further cement my view that the company is well-managed and will have no liquidity problems, look at the current ratio. This is hovering around 2 for the last 5 years with a slight dip in FY22, which I believe will be short-lived. In their latest 10-Q report, the ratio is back at around 1.97.

{kind=link}

The debt figure is sufficiently covered by cash on hand, and I am not worried about this, as long as they keep using the debt for strategic purposes, like repurchasing shares and paying dividends. The company has repurchased approximately $220m worth of shares in the last 3 years. 2020 was a good year to repurchase shares, as it was beaten down quite a bit. During this year, they repurchased $92m. During the next 2 fiscal years, the company, looking through some price charts, might have repurchased shares at around $60+ a share, which isn’t very ideal, as I believe it was a bit expensive and they could have spent that money on other endeavors, like acquiring another small company to enhance their portfolio.

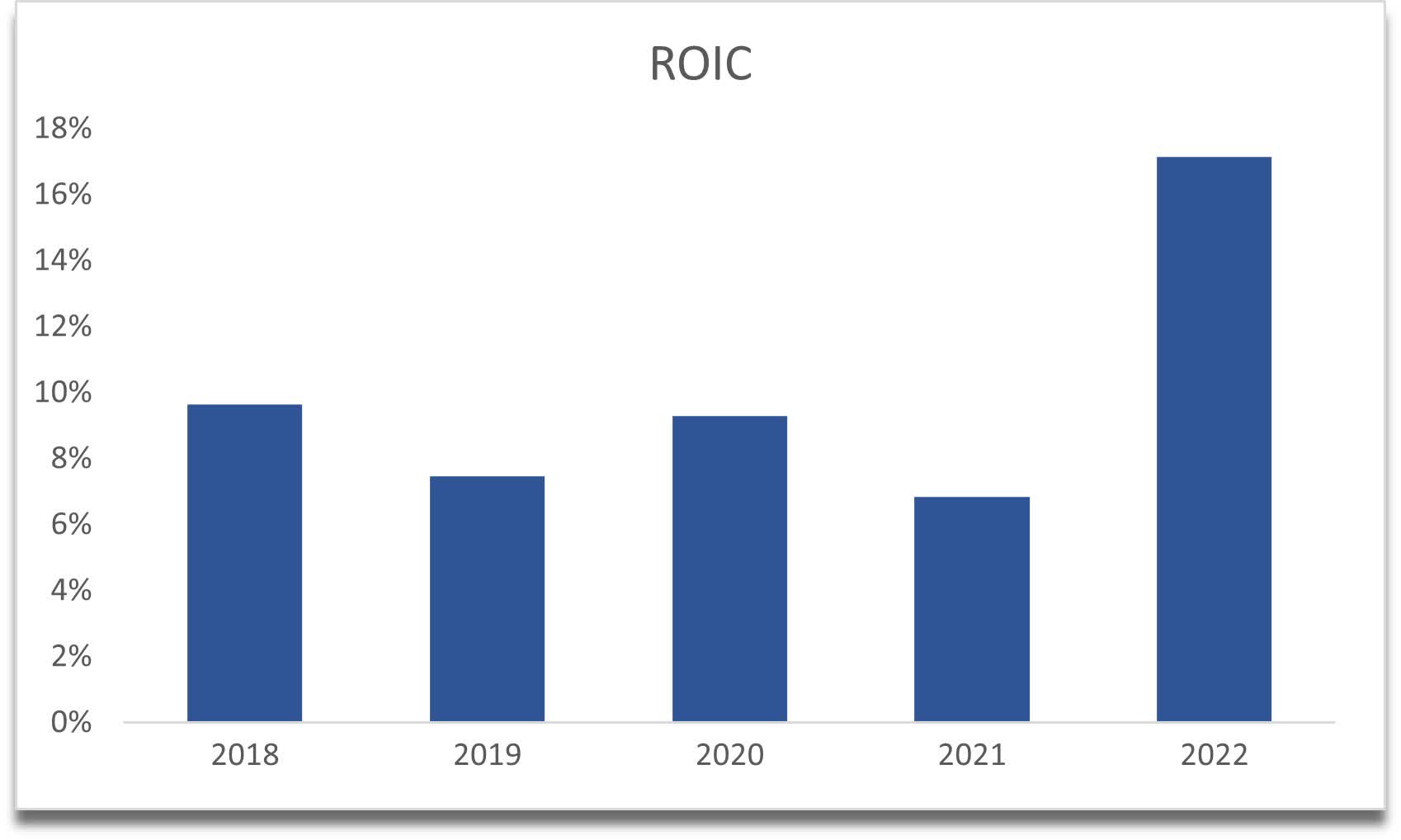

The company has seen a large jump in ROIC, which is a great sign, and I hope that either this continues to be the case or at least hovers at these elevated levels, however, if there is a recession, we will see a dip.

{kind=link}

Overall, Korn Ferry seems to be managed very well, and I do not see any red flags that would deter me from looking further into the company as a potential investment. I do find companies that have great balance sheets and warrant an investment on that alone, however, for a full analysis we need to look at other factors also, such as the price that the balance sheet and growth estimates are worth. That is where my next section comes in, DCF valuation.

Valuation

Now that we have talked about the most important financial metrics and growth assumptions for the four segments, it’s time to put these into the model. As I mentioned, to get a better perspective of how the total revenues grew, I divided them into four main revenue segments. Also, to get the possible price range for the company, I modeled 3 different scenarios, conservative, base, and optimistic.

My model will take on a more conservative approach. The estimates in my opinion have been beaten down a bit more than they should have been, but I stick to these assumptions because I do like to see a good margin of safety in case my calculations are not as accurate. I like to beat up stocks like that to see where the real value is. Sometimes, but not very often, I see companies still being undervalued under these harsh growth assumptions, for example, my Meta Platforms ( META ) and Crocs , Inc. ( CROX ) analyses most recently passed these assumptions.

For all four revenue segments, I have modeled 2023 and 2024 negative growth in revenue, as I assume that we will have a recession over the next 12 -18 months and the demand will fall for their services. Then I modeled double-digit growth for all segments to show an increase in demand for their services and then come back down over the next couple of years to single-digit growth, which gives me around 8.1% average revenue growth on total revenues over 10 years on my base case, 6.1% on the conservative case and 10.1% on the optimistic case.

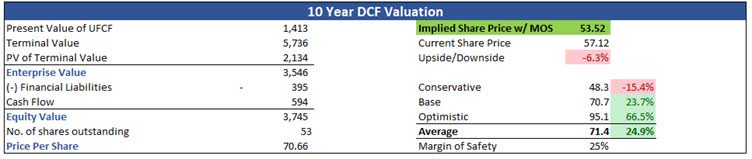

I assume -7% revenue growth in 2023 and -6% in 2024 when all segments aggregate into total revenues. In the last 10 years, Korn Ferry’s revenues have been positive in all but one year in 2021, so I am being much more conservative in my estimates. On top of my conservative numbers, I also like to add a good margin of safety of around 25%. With that being said, the value of the company from a 10-year DCF analysis is 53.52, which is around 6% lower than what the company is currently trading at.

{kind=link}

Closing Remarks

As I mentioned earlier, I believe I am being very pessimistic about the economic outlook and the company's growth prospects, and still, Korn Ferry is very close to being at a good price to invest in the long term. I do believe we will have some more volatility in the markets and the company will see a drop in the share price as all other companies will drop due to lingering uncertainty.

I believe there will be a good Korn Ferry entry point coming up in the next couple of months where investors can start building up a position in this great company, but as of right now, I would suggest holding off and keeping it on your watchlists. Set a price alert a little lower and check technical analysis for a good entry point, although it is not very necessary. Earnings are sometime in March; this will most likely bring volatility and probably an opportunity.

I would also pay attention to the options market to see if the spreads are not too wide and look into selling cash-secured puts at somewhere around $50 per share, collecting a premium while waiting for the right price.

In my opinion, future mergers and acquisitions and more companies adopting RPO services will only strengthen Korn Ferry's position. The company, I would say, is well-diversified in its service offerings and will not suffer very badly when we see a downturn in the economy.

Take this analysis of future growth with a grain of salt, of course, and do extra due diligence to decide if Korn Ferry is a company that is worth investing your money into for the long term. Thank you all for reading!

For further details see:

Korn Ferry: DCF Approach Close To An Entry, But Volatility Demands Patience