KFY - Korn Ferry: Exceptional Value Against Meager Risks

2023-10-11 11:47:43 ET

Summary

- Korn Ferry has exceptional discounted cash flow analysis results, as well as strong profitability and safe, diversified operations. The risks in terms of financial health are unsubstantial.

- An operations analysis underscores the quantitative value opportunity, where I outline geographic and business diversification.

- My overall investment analysis rests on a strong buy sentiment reinforced by peer comparisons and an excellent price.

Introduction

I've found an exceptional value investment for my portfolio balanced by only meager risks. I'm excited by the three-year-plus value opportunity of Korn Ferry ( KFY ). I invested in the company primarily because of its exceptional valuation with strong profitability and growth; I have also noted strong operational advantages including a healthy level of geographic and business diversification. I've weighed these positive points against the mild financial risks related to debt and WACC-to-ROIC, which I believe are prudent to consider. I am convinced the investment is a long-term holding that will see well-above-index returns in the next few years.

Operations

I want to know the intricate details of what it is I'm investing in, so I read annual reports, presentations and earnings call transcripts, amongst other documents that outline operational circumstances. This gives me a detailed breakdown of service and product revenue streams and helps me understand industry potentials and risks. I also look carefully at the geographical revenue streams to gauge any potential macroeconomic factors that could negatively (or positively) impact my investment. In the case of Korn Ferry, there aren't many red flags, and the main issue I have noticed is competitive challenges in a highly saturated industry that could realistically mean lower-than-best returns. I'm betting the value opportunity overruns this, though.

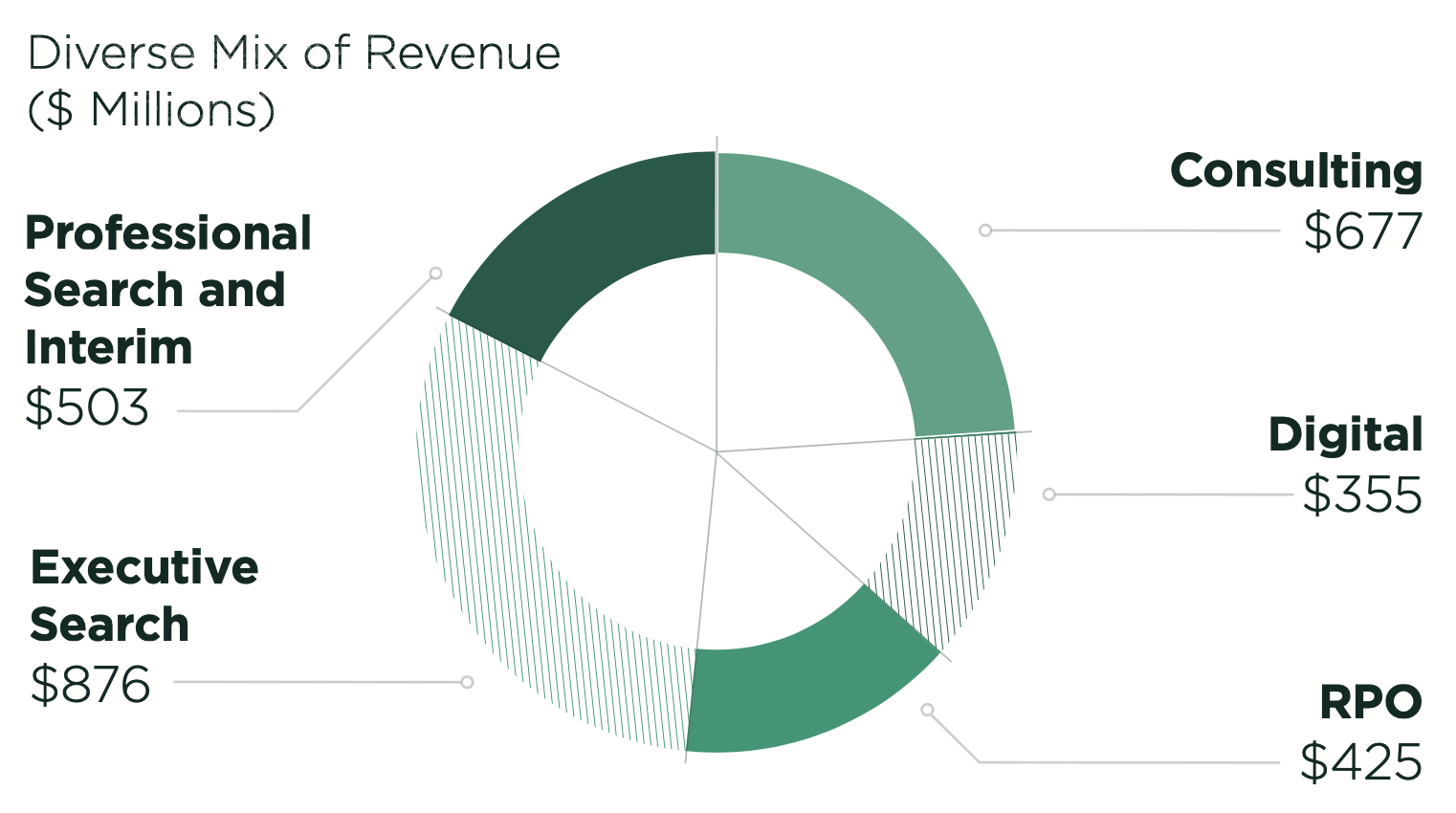

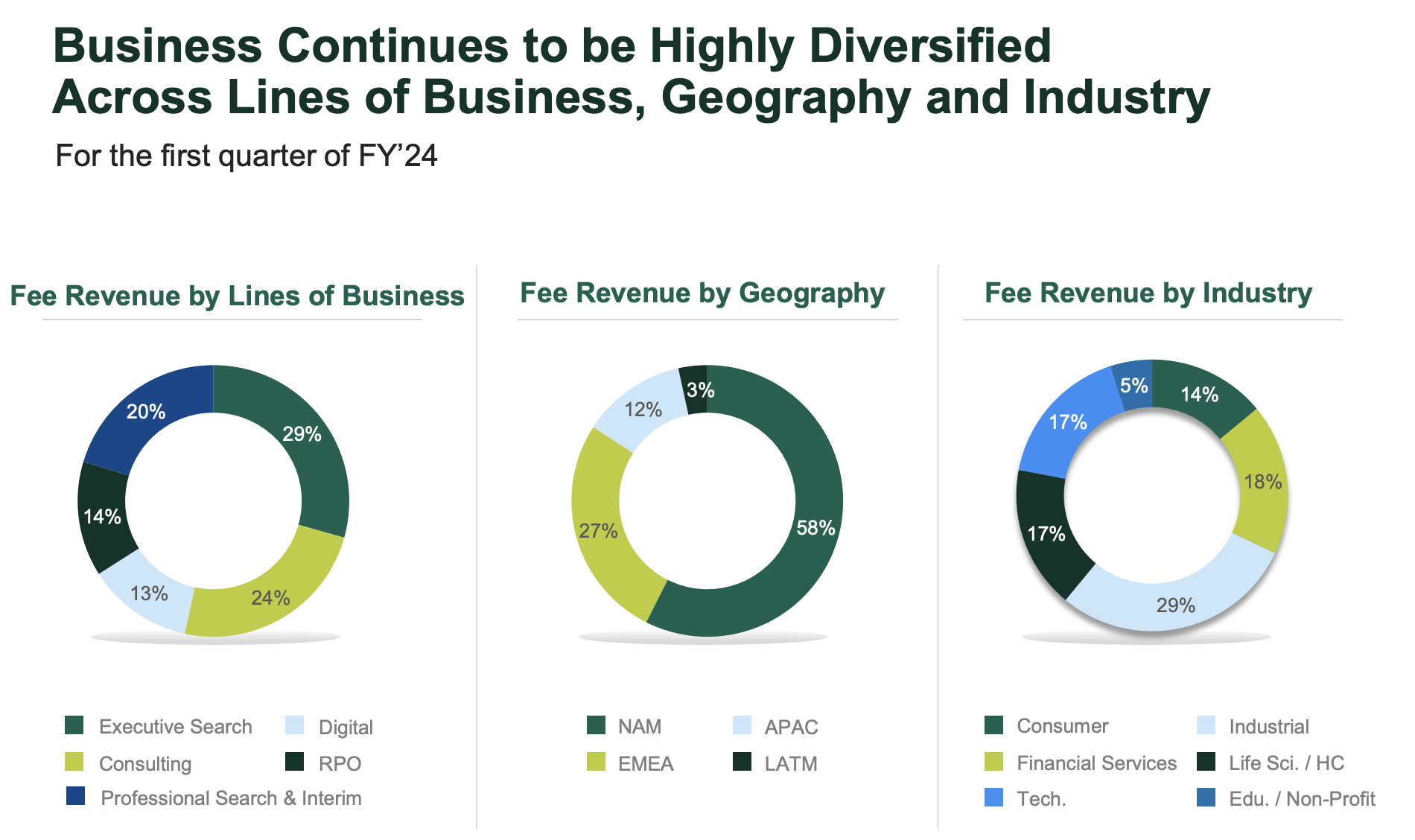

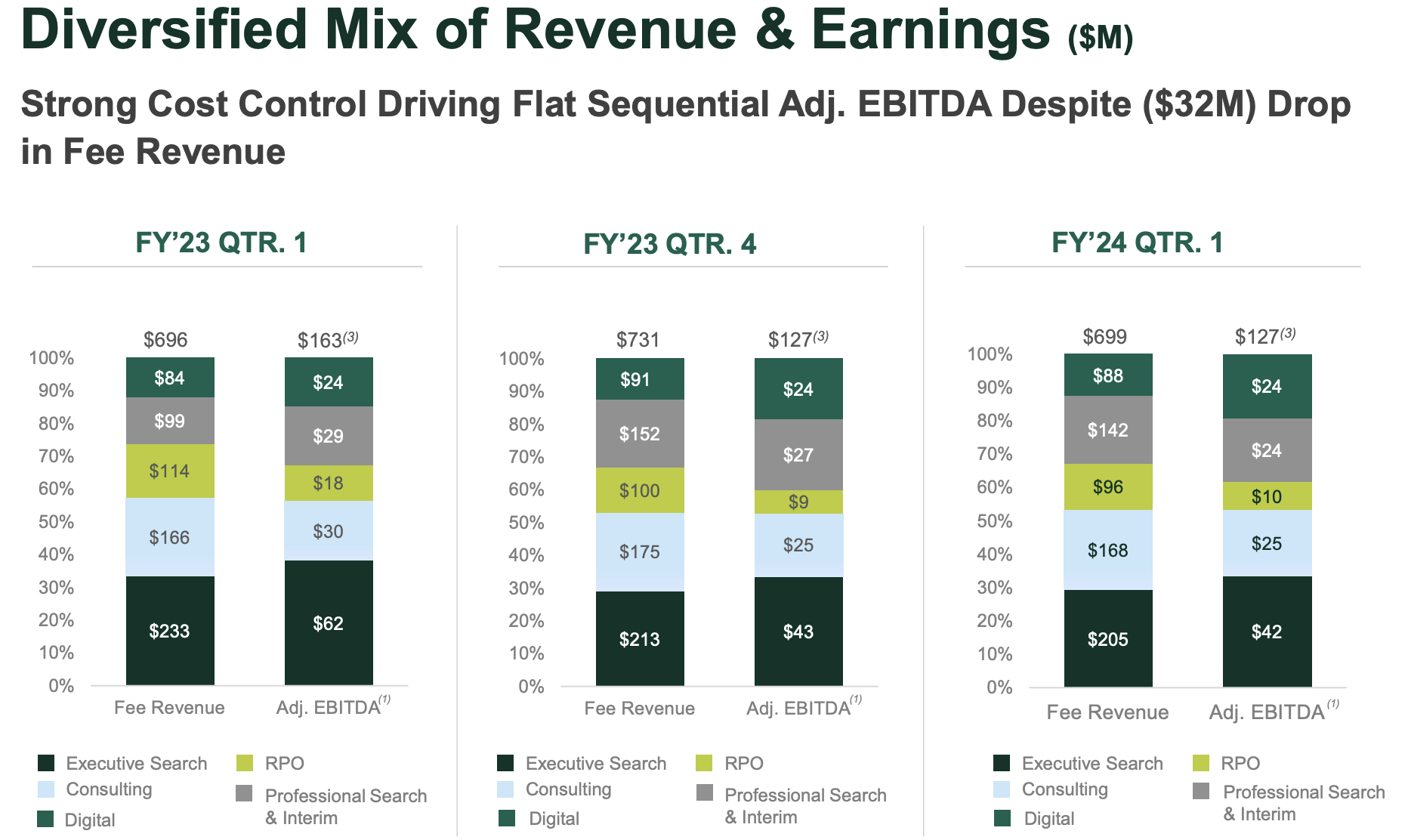

Revenue by Business Segment & Geography

Korn Ferry maintains diversity among its revenue streams in the business services industry, but it is a typical consultant and headhunting firm. I don't see any negatives to the fact that although they are diversified amongst their skill set, they are focused on their niche of expertise. This isn't a multi-industry conglomerate. Perhaps there is some risk associated with the lowered diversification that comes with this, but I simply will not find value at this level with some of the bigger corporations.

{kind=link}

Comparing the breakdown from the Q1 FY'24 earnings presentation is useful. Although the company describes itself as 'highly diversified', and this is true to some degree, I maintain that some caution is reserved especially when we get onto the North American dominance in revenue geographically.

{kind=link}

{kind=link}

61% of business is from North America and Latin America. 58% of that is North American revenue, so we're dealing with a heavily dominant US company. I don't see anything negative about that; I see it as safe.

Europe, the Middle East & Africa make up 27% of revenue, and Asia-Pacific 12%, which could be argued to both provide diversification and exposure to emerging markets, but also volatility risk due to less certain macroeconomic climates and trading conditions.

Key Strength: Conglomeration

Although I do scour the earnings transcripts and annual reports, I am a firm advocate of data speaking for itself. In that sense, I make a conscious effort to understand the business operations and advantages, but I don't let these elements cloud my judgement of current (and past) financial and metric-based business health as evidence of operational effectiveness.

That being said, what I do want to know is what the company is actually and effectively doing on the operational front that is

- causing these fantastic metrics and

- will help continue to cause above-average results in the future.

In 2019 Korn Ferry acquired 28 companies:

The combination brought a world-class portfolio of learning, development, and performance improvement offerings and expertise to Korn Ferry, bolstering the firm's substantial leadership development capabilities. - Korn Ferry

The company also announced a partnership with PGA Tour, which shows promising initiative and further conglomerate-style direction. I feel comfortable investing in diversified and partnered companies with subsidiaries because it creates foundational support to already strong financials and reinforces safety to any capital deployed.

Of the companies acquired by Korn Ferry in 2019, three were Miller Heiman Group , Achieve Forum and Strategy Execution :

Miller Heiman Group specialized in transforming sales performance and customer experience. AchieveForum offered frontline leadership development. Strategy Execution provided organizational and project management training.

The addition of these three companies further expanded Korn Ferry's vast intellectual property and content, leveraging the firm's digital delivery platforms and provided clients direct access to data, insights, and analytics from one of the world's most comprehensive people and organizational databases. - Korn Ferry

2021 then saw the acquisition of Lucas Group , 2022 the acquisition of Patina Solutions and ICS (Infinity Consulting Solutions), and 2023 the acquisition of Salo . These are bold moves and reinforce my thesis that Korn Ferry is becoming more conglomerated as it advances.

Greatest Operational Risk

Competition stood to be the greatest operational risk when I began the analysis of Korn Ferry, with the likes of Accenture ( ACN ) taking the dominant centre-stage position in the industry. For consideration Accenture has a market cap of $209.23bn; Korn Ferry has a market cap of 2.59 billion. That doesn't put Korn Ferry anywhere near second place. Korn Ferry is 83rd on the list of largest professional services companies in the world. Korn Ferry is by no means a monopoly, and on many accounts, it could easily struggle to grow sustainably without strong strategies to acquire market share.

That being said, with an entrenched product and service set, the company is poised for continued growth even amidst potential domination by rival firms. My thesis is hinged on the firm belief, backed up by rigorous quantitative and qualitative evidence, that Korn Ferry is a phenomenal value play, even in the face of less-than-top market reach. For consideration and to touch on the deep dive of fundamental analysis to come in this research article, Korn Ferry has a three-year revenue growth rate better than 78% of companies in the business services industry. It's smaller but more competitive. The fact that it is smaller also opens up an opportunity-the company is less studied, so it hasn't priced in the value advantage as much as it should have yet.

Korn Ferry List of Services (Solutions) (Korn Ferry)

{kind=link}

Valuation

Usually, I will place a valuation discussion at the end of a thesis, but in this instance, it seems prudent to place the topic of valuation at the forefront of my fundamental analysis. The reason for this is that the inherent opportunity here is hinged on value at the current depressed price. If I can convince you of this opportunity, the rest of the metrics have a much clearer and more succinct impression.

I'll perform two discounted cash flow analyses for readers to see why the stock is undervalued right now.

Discounted Cash Flow Analyses

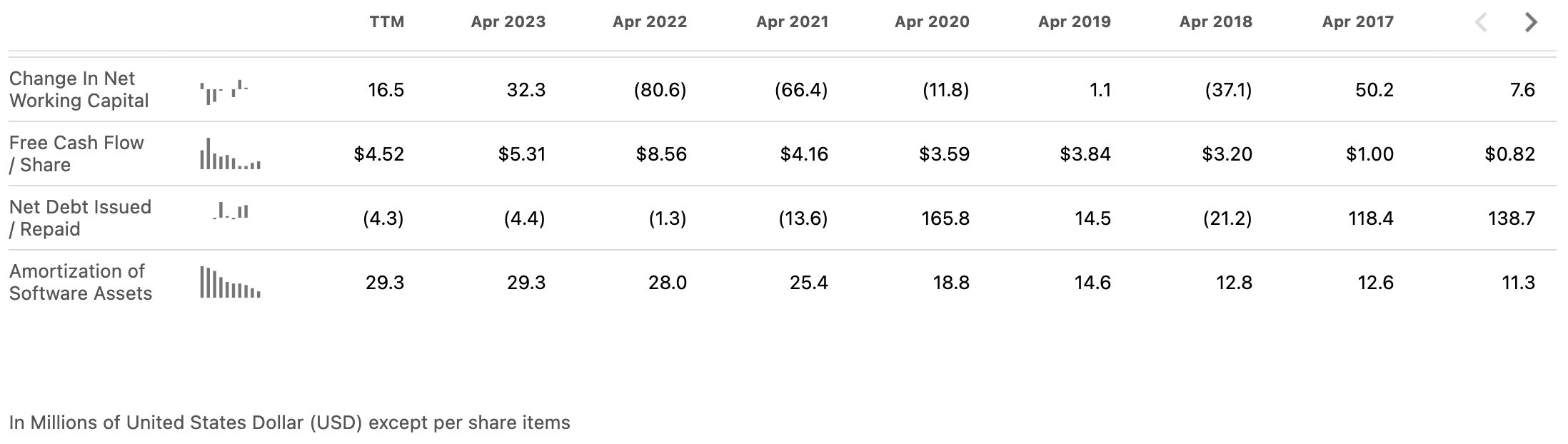

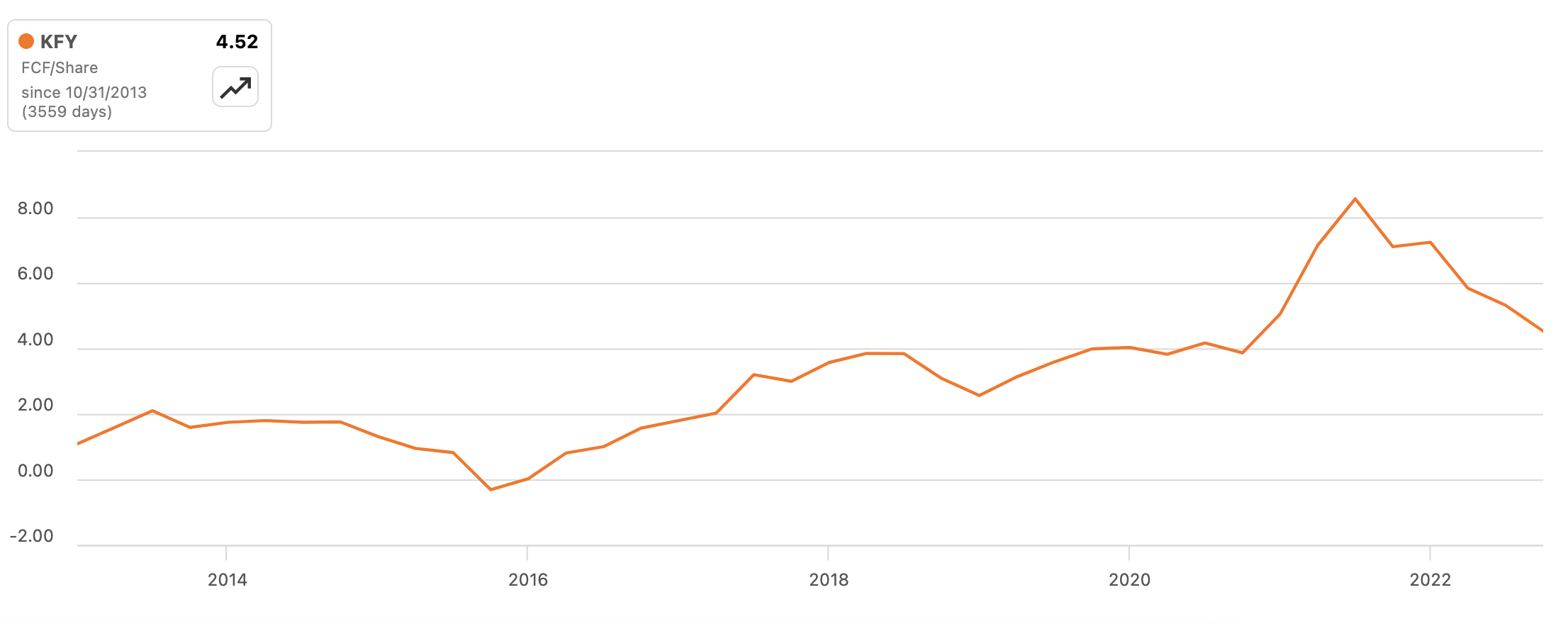

Based on free cash flow per share, since 2013, the growth rate (annualised) has been 20.90%

Seeking Alpha Korn Ferry FCF/Share (Seeking Alpha)

{kind=link}

{kind=link}

Using a 10-year growth stage at a rate of 20% and a 10-year terminal stage at a rate of 4%, with an 11% discount rate, the current fair value is $138.75. With the current share price at $48.12; that's a margin of safety of 65.32%. That is very comfortable and highly to my liking.

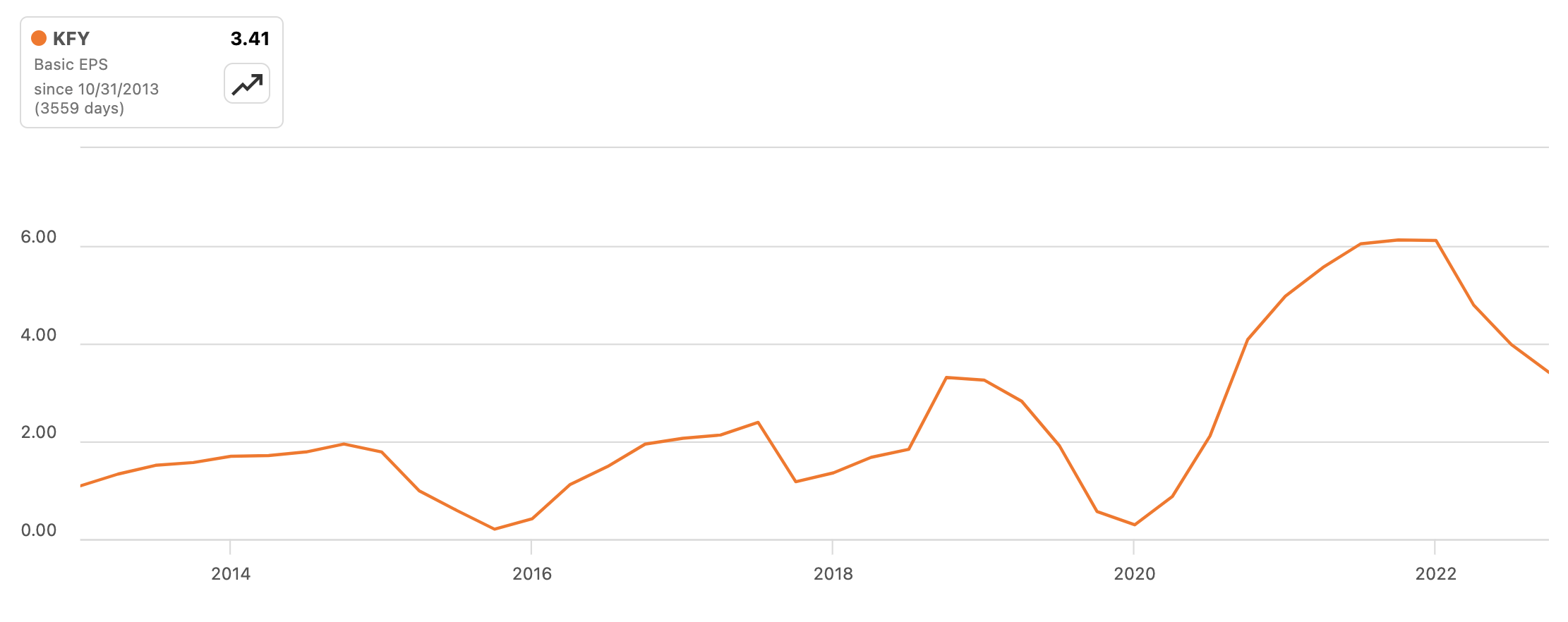

I've also performed a discounted cash flow analysis based on earnings per share without non-recurring items. The 10-year annualised EPS growth rate to date is 17.10%

Korn Ferry Basic EPS (Seeking Alpha)

{kind=link}

Using a 10-year growth stage of 17.10% and a 10-year terminal stage of 4%, with an 11% discount rate, the margin of safety is 44.82%. The fair value based on this calculation is $87.20.

Those are strong findings and are inherent to why Korn Ferry could be a long-term investment that immediately looks great for my portfolio on the valuation front.

However, I've also analysed the P/E GAAP ratio and the P/B ratio to gauge the current price as opposed to peers, which should more strongly support the investment decision on the valuation front.

P/E Comparisons

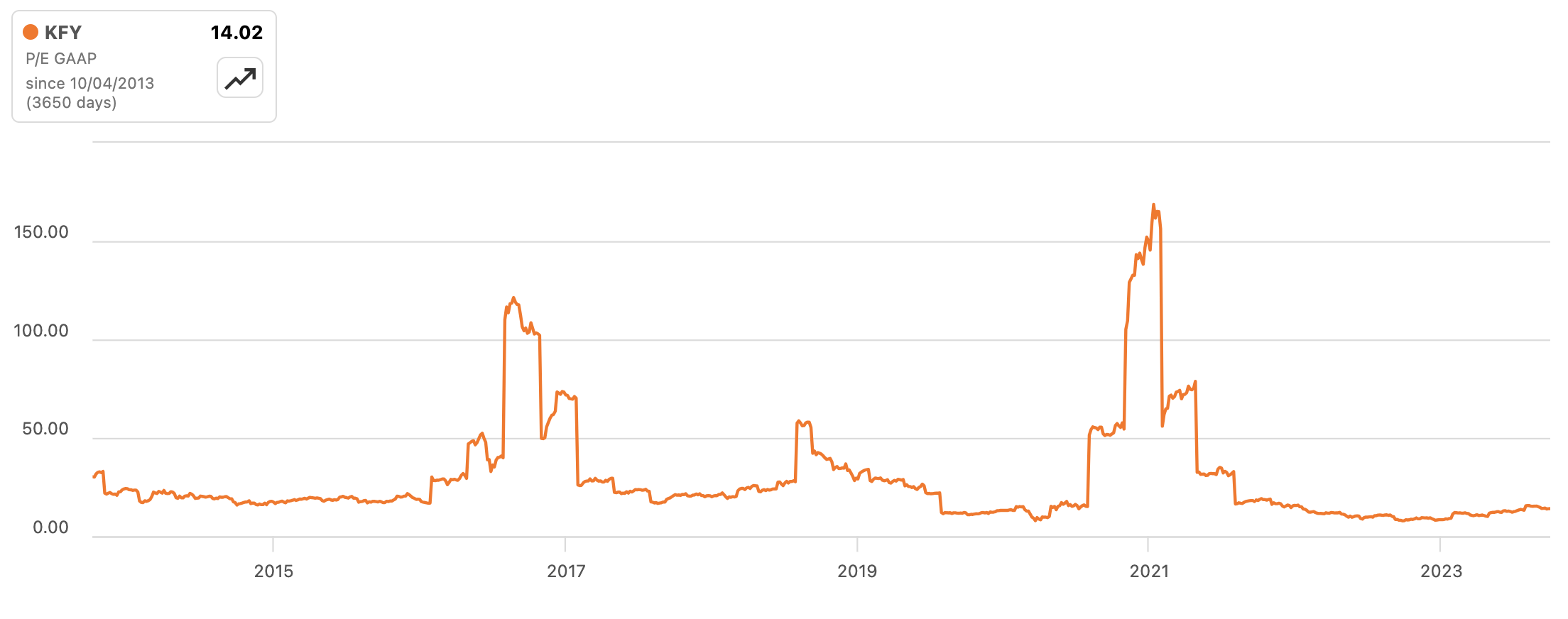

The current P/E ratio is actually near its all-time low.

Korn Ferry P/E GAAP (Seeking Alpha)

{kind=link}

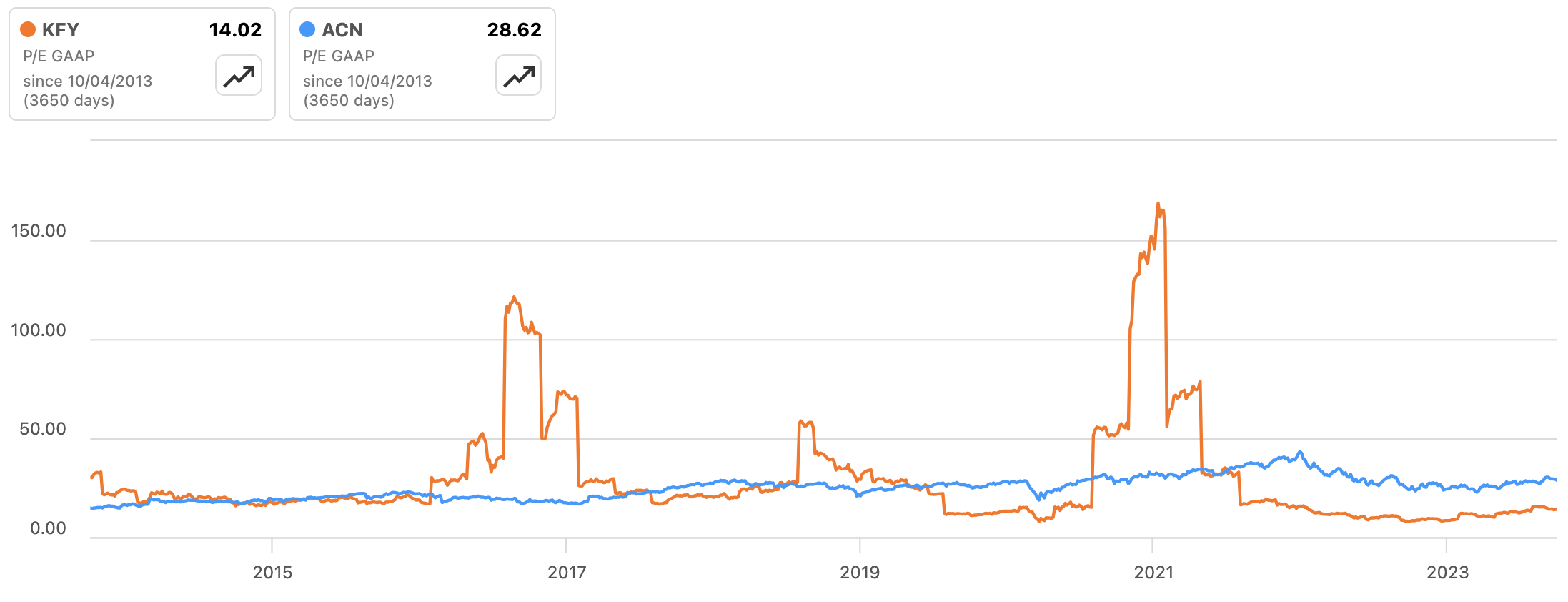

As discussed above, the largest publicly traded professional services company in the world is Accenture. I've compared it to Korn Ferry on the P/E GAAP ratio graphically using SA charting:

Korn Ferry Vs. Accenture P/E (Seeking Alpha)

{kind=link}

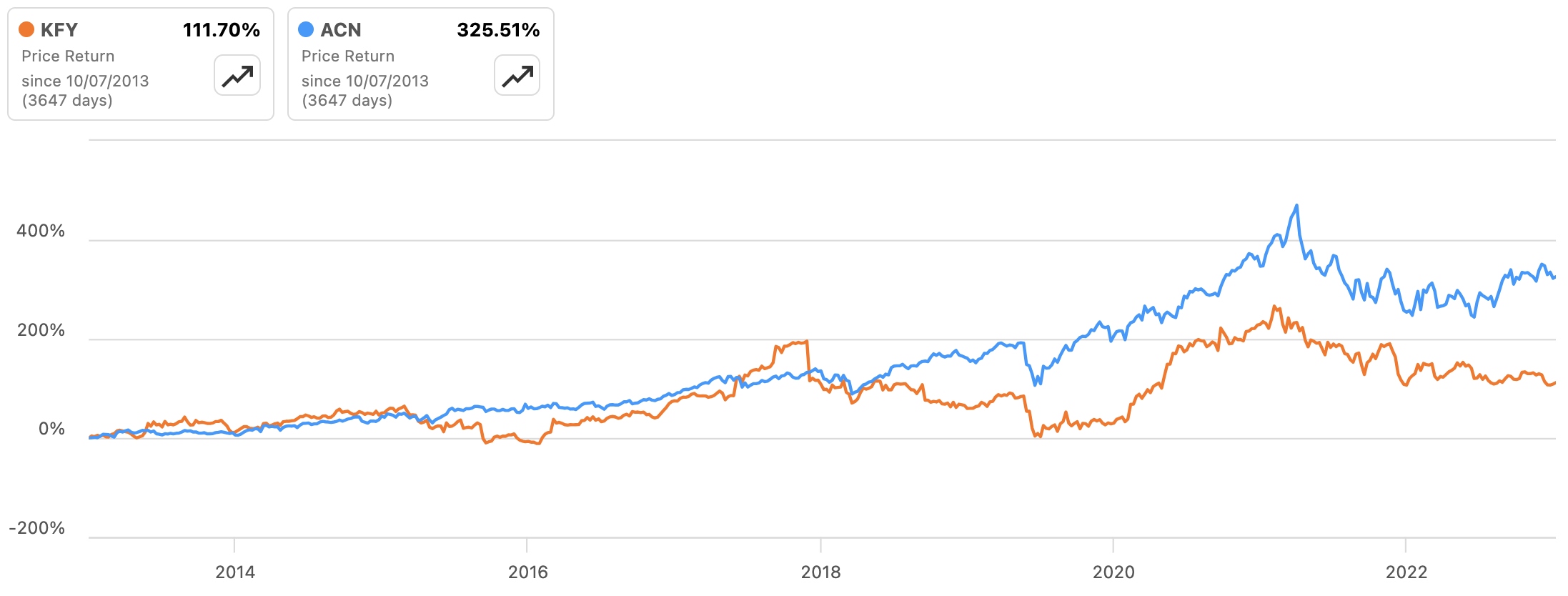

I've also compared Korn Ferry against Accenture on price return:

Korn Ferry Vs. Accenture Price Return (Seeking Alpha)

{kind=link}

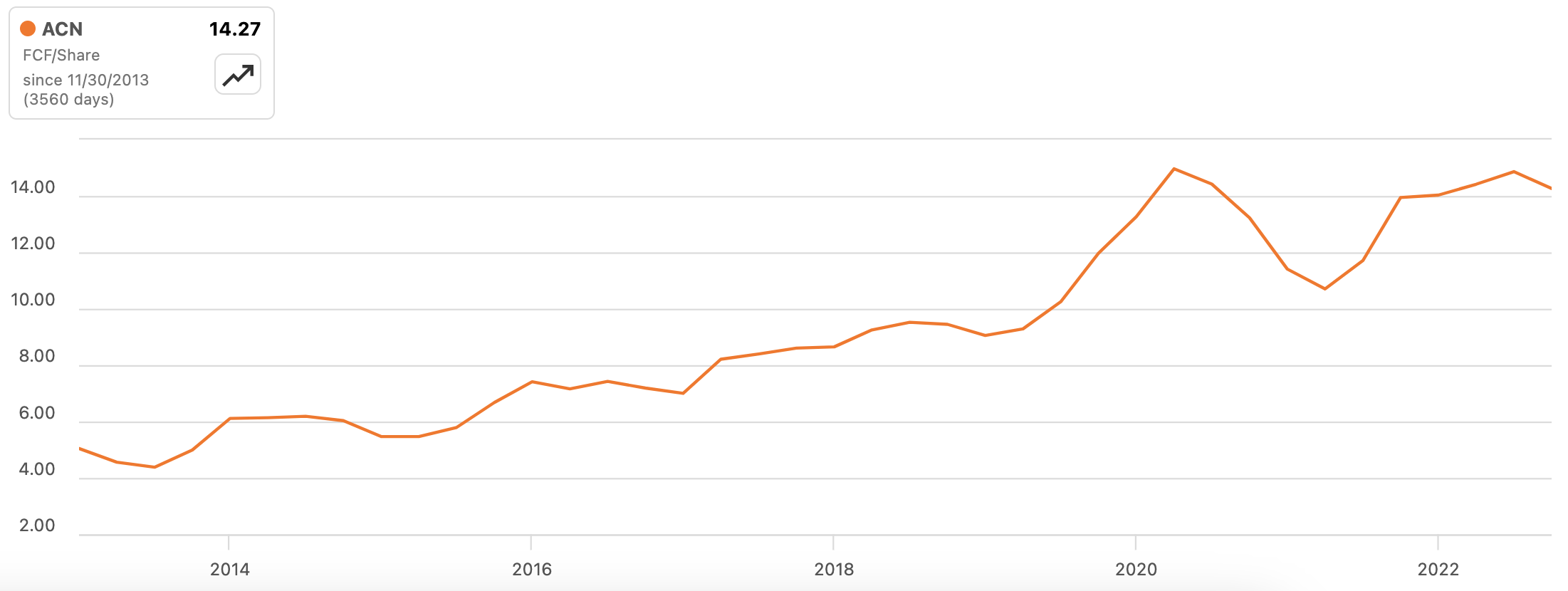

Accenture looks like the stronger competitor, but my main issue with Accenture is the discounted cash flow analysis. Looking at a 10-year annualised free cash flow growth of 14.30%, the margin of safety with a 10-year 14.30% growth stage and a 4% 10-year terminal stage and my standard discount rate of 11%, the fair value is $300.44 and the current value is $309.39. That margin of safety is -2.98% and is generous as the same calculation run on EPS is much worse.

Accenture FCF/Share (Seeking Alpha)

{kind=link}

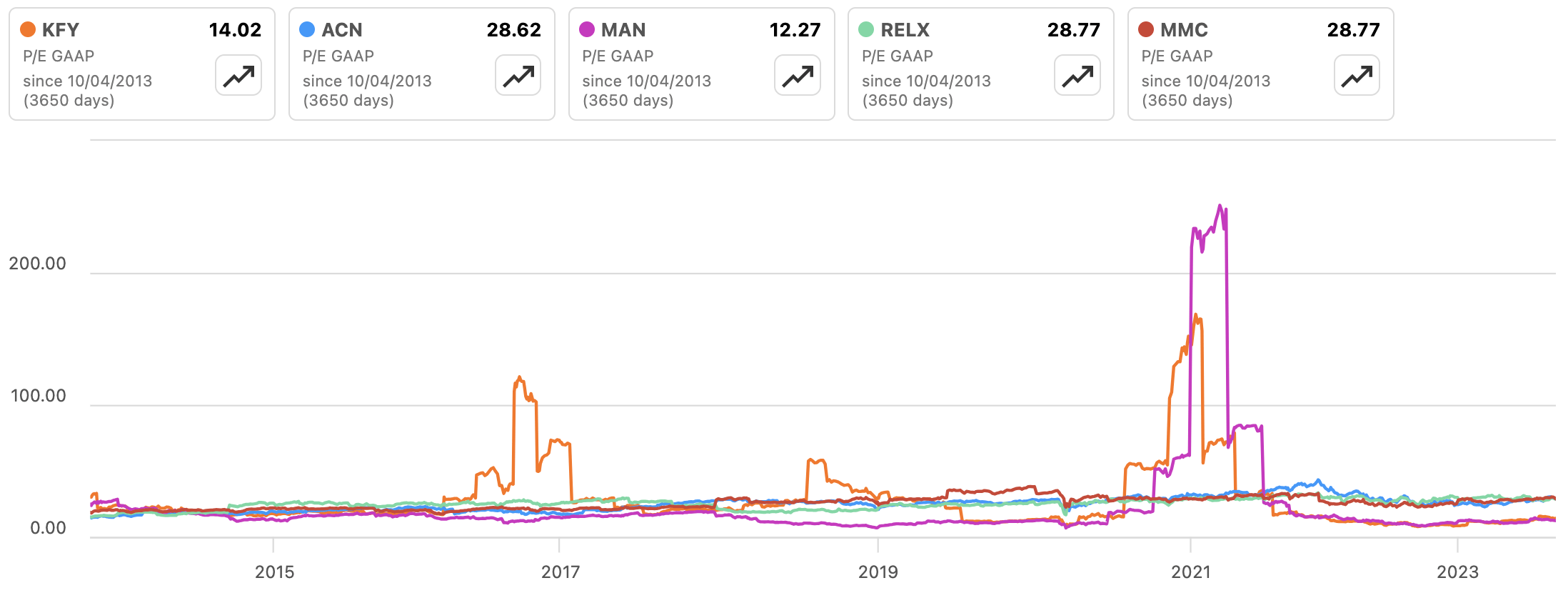

I've compared the P/E GAAP of Korn Ferry against five of its major competitors. I'm looking at high P/E volatility from Korn Ferry, as well as its peer ManpowerGroup.

Korn Ferry P/E GAAP Peer Analysis (Seeking Alpha)

{kind=link}

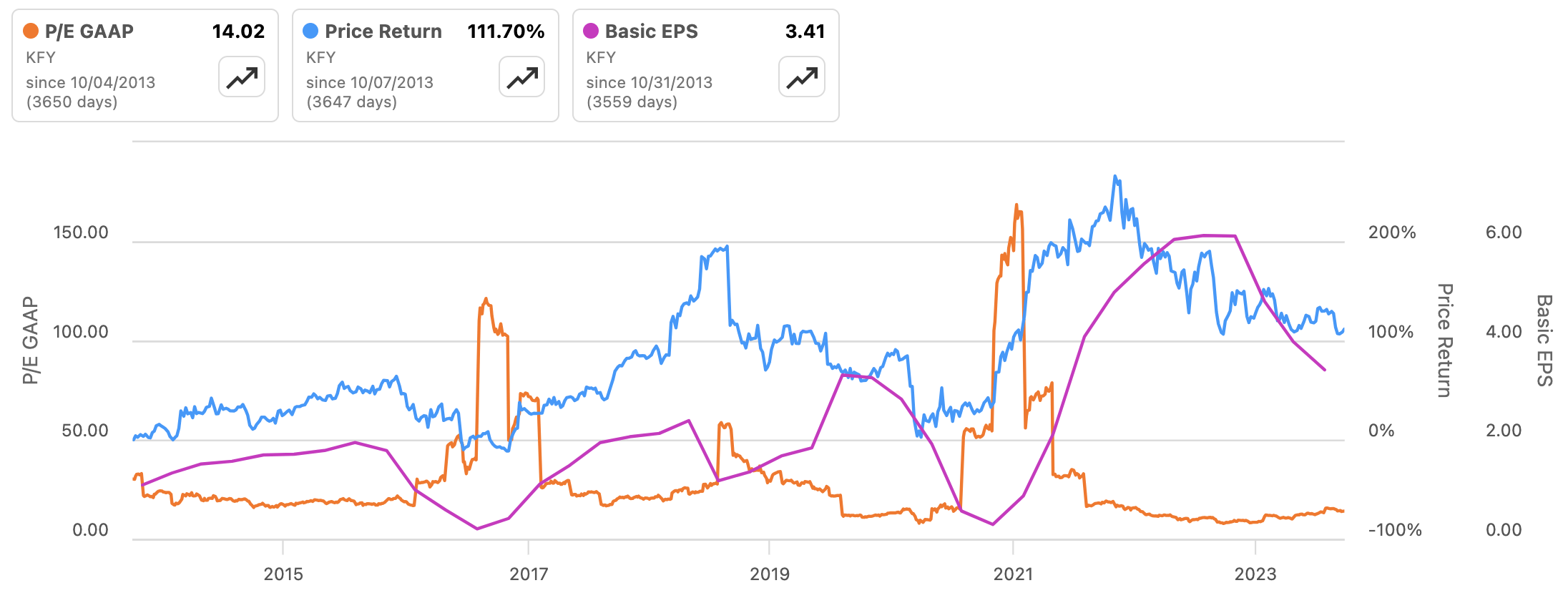

However, I've also compared P/E GAAP to Basic EPS to Price Return to give you a fuller analysis of what causes this P/E volatility visually: earnings dips. The upward trend nonetheless for basic EPS and price return is up. P/E ratio instability, although a red flag in terms of earnings stability, is not a deal breaker by any means. All that means to me is a potentially mildly rocky road to profits, which I'm comfortable weathering as the long-term trend is positive and the current valuation is beyond safe.

Korn Ferry P/E GAAP Vs. Price Return Vs. Basic EPS (Seeking Alpha)

{kind=link}

P/B Comparisons

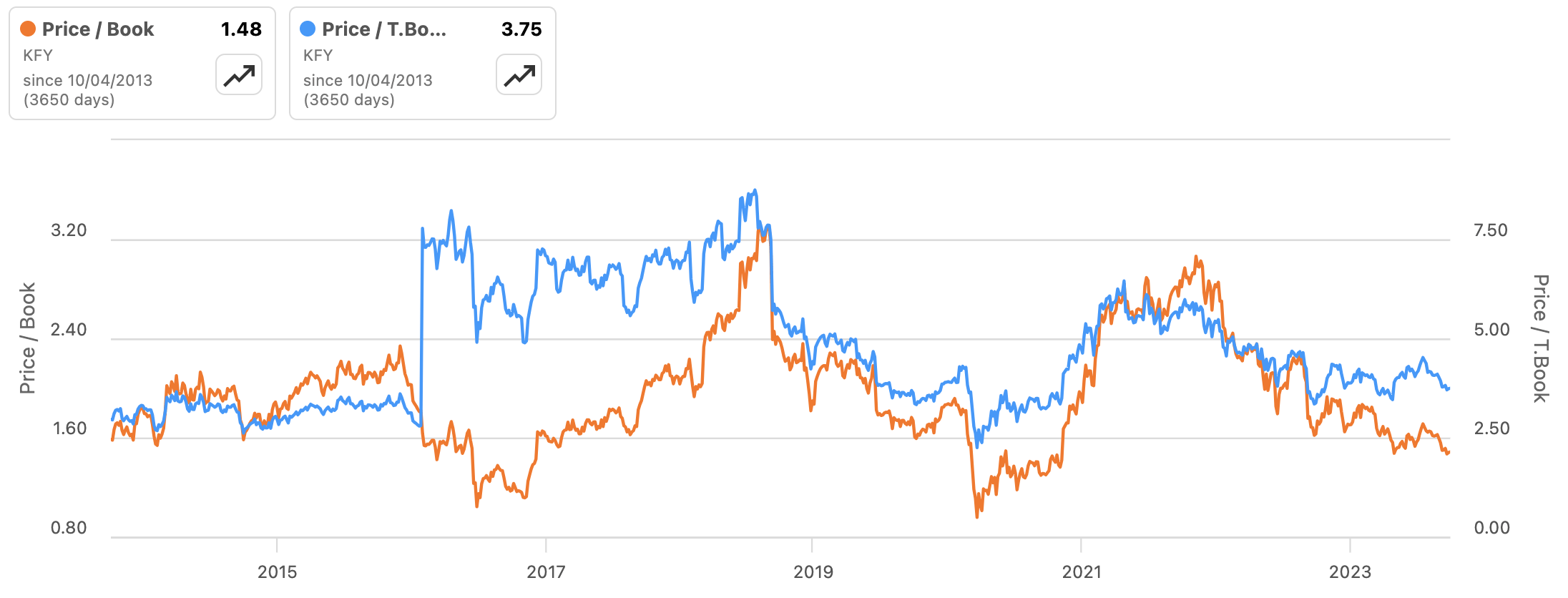

I've analysed both the price to book value and the price to tangible book value and placed them on the same chart.

P/B Vs. P/TB Korn Ferry (Seeking Alpha)

{kind=link}

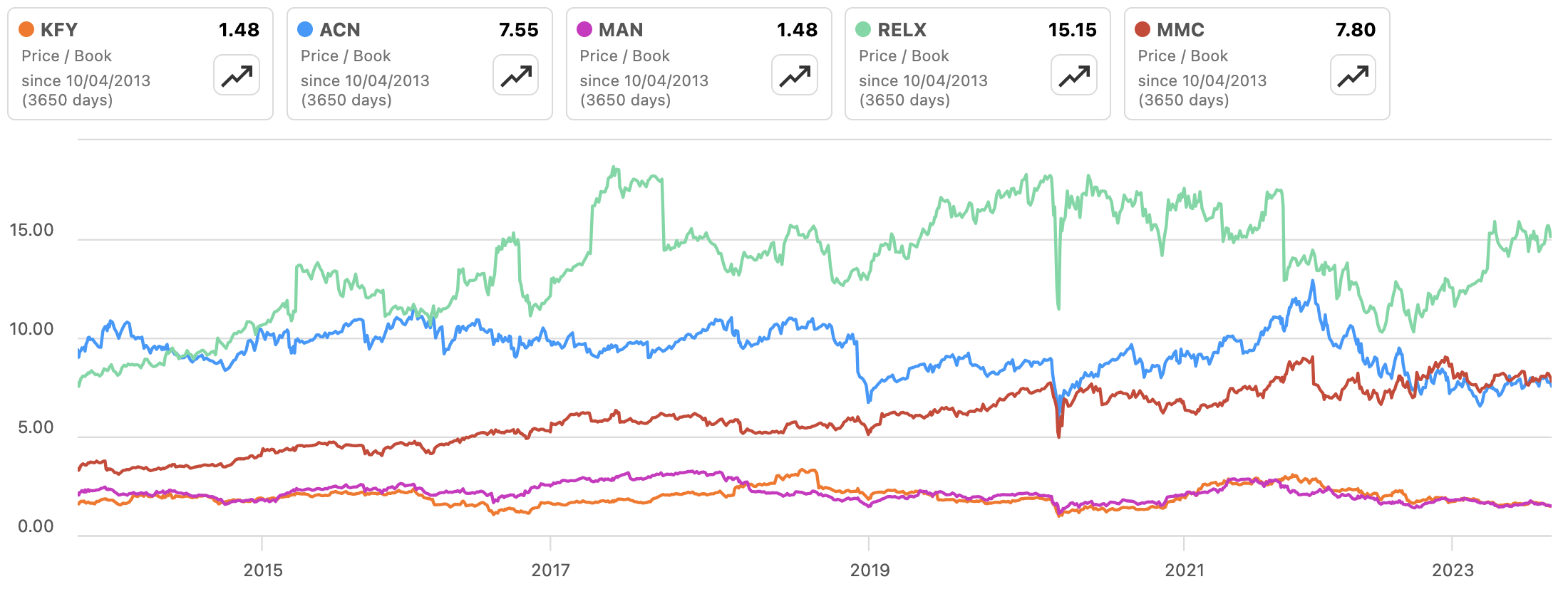

I then compared the P/B readings with peers. For ease of reference, I've used the same five peers as when comparing the P/E GAAP.

Korn Ferry P/B Peer Analysis (Seeking Alpha)

{kind=link}

Korn Ferry is very low on this front. On the P/B measure, it makes an exceptional investment for my portfolio when considering this reading in tandem with the great discounted cash flow analyses. ManpowerGroup ranks in tandem with Korn Ferry on P/B. ACN, as we can see, trades at a much higher valuation.

Final Valuation Thoughts

Overall the valuation is stellar in comparison to peers and the discounted cash flow analyses indicate an obvious investment for my portfolio given the financial metrics I am about to present. I know that the price return might take some time to grow into what I expect and not necessarily on a straight road, but the opportunity remains and I am confident in the real-world business operations strengths to support the depressed price. In my opinion, the investment is an obvious move.

I recently analysed Mitsui on the valuation front, with a deep dive into operational and macroeconomic factors, and Korn Ferry is a much stronger competitor for a value investment at current prices based on my analysis of both companies. Mitsui does have long-term appeal, but it is currently trading at near all-time highs. Korn Ferry on the other hand, actually has much better and more acute financials and operational advantages and is currently trading 41% below its all-time high. Even if I were to realise a 50% gain from Korn Ferry over the next three years and sell at a fair valuation, that's enough for me and ticks my box for seeking alpha.

Profitability

Korn Ferry shows very strong gross margins and net margins vs. industry norms. Return on total capital is also strong relative to peers, but these metrics are average in terms of comparing them to the company's own historical metrics. I've analysed the margins and the ROE and ROTC for the company alongside peers and concluded that the company is ranked well on the profitability front, which further bolsters my confidence in the investment. However, the greatest risks here relate to the lack of profitability growth.

Margin Analyses

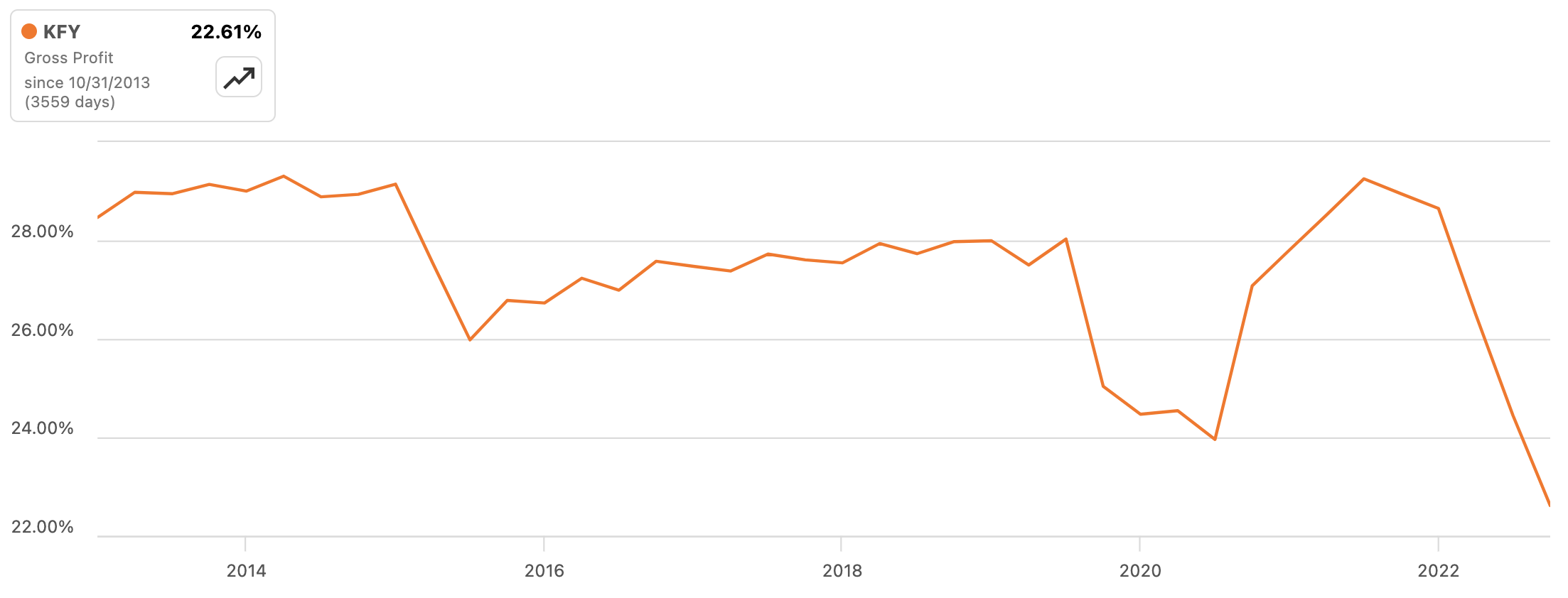

I'm starting with the biggest risk that is apparent to me on the margin analysis front: current gross profit vs. historical gross profit.

Korn Ferry Gross Profit (Seeking Alpha)

{kind=link}

This could be considered a severe warning for me as an investor as it shows there is a major slowdown in profitability and that the element of growth that I like to see as an investor might not be there.

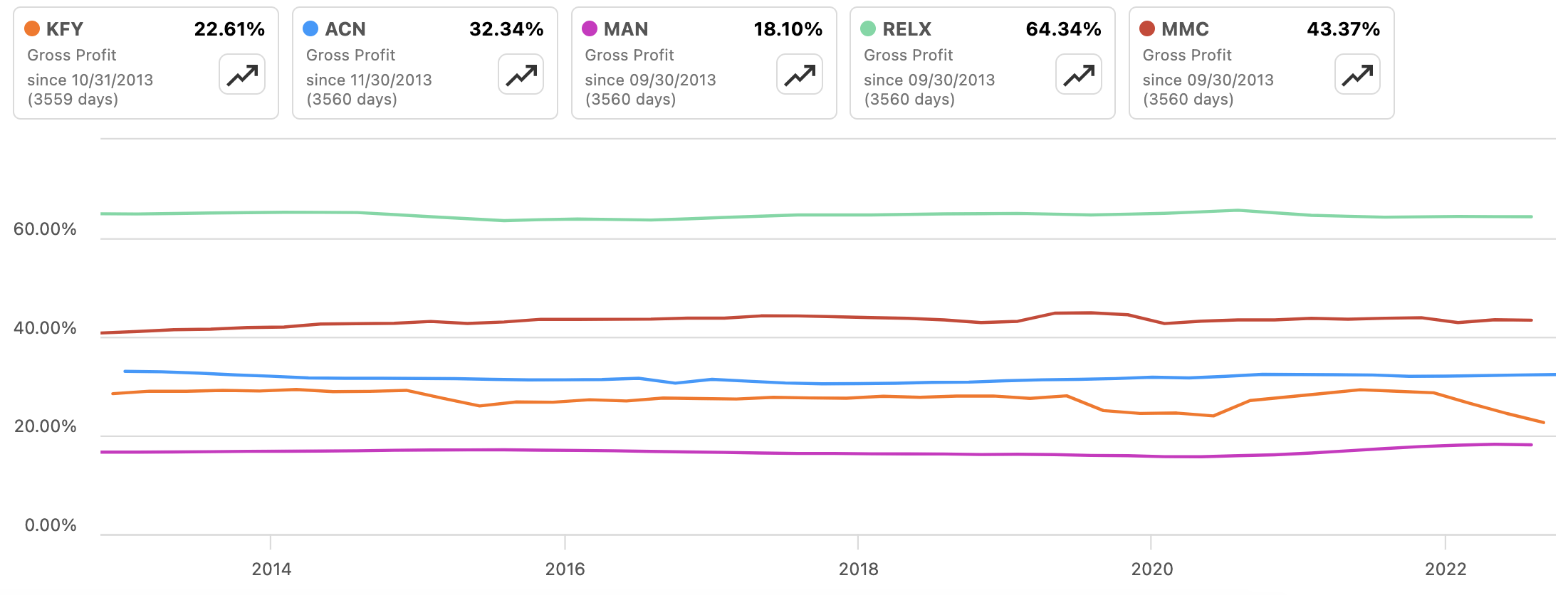

That being said, let's compare it with peers because as is clear by the next graph, the industry norm is stagnant gross profits. Korn Ferry is not too far off Accenture on this front.

Korn Ferry Gross Profit Peer Analysis (Seeking Alpha)

{kind=link}

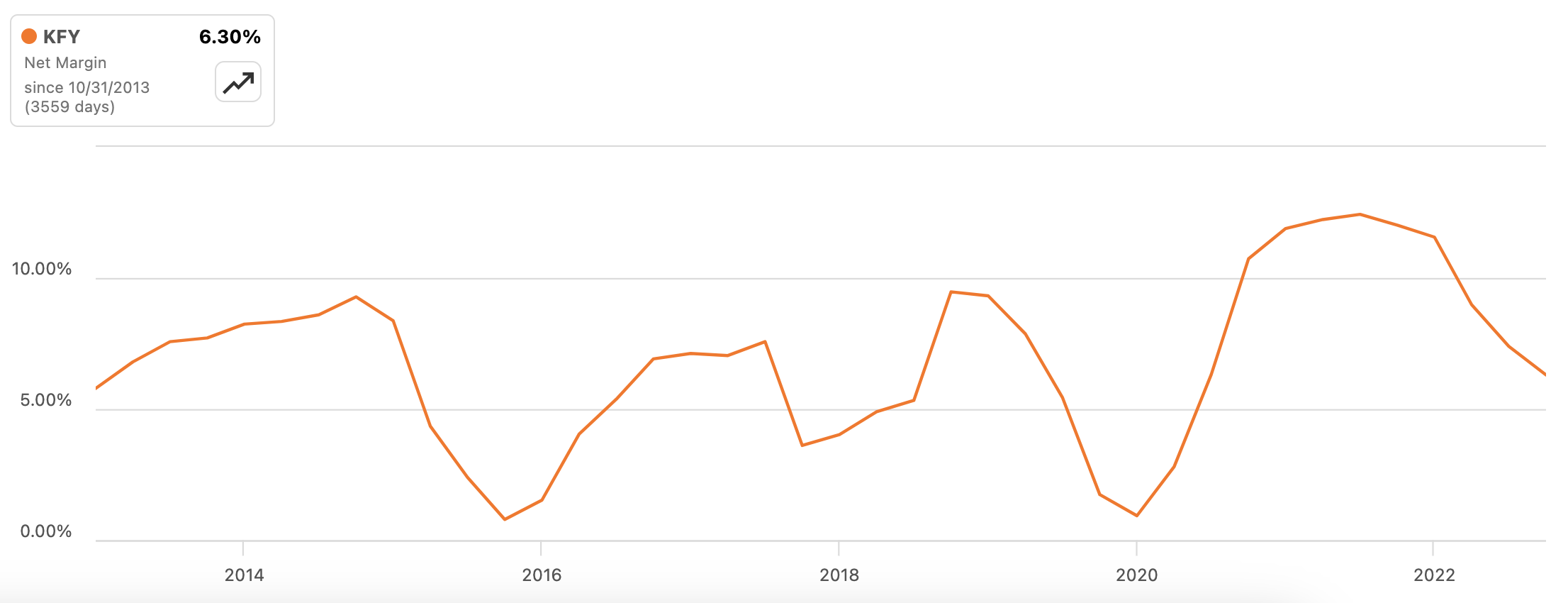

More important to me is the company's net margins:

Korn Ferry Net Margin (Seeking Alpha)

{kind=link}

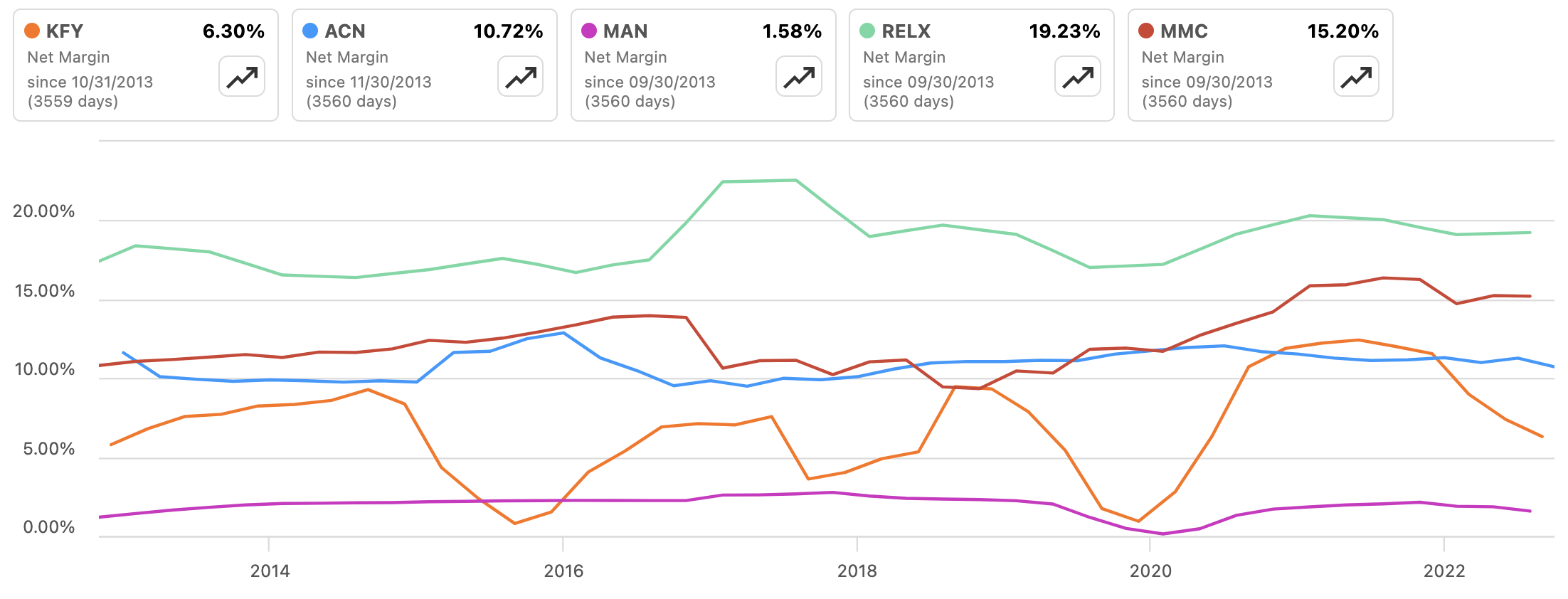

I've compared it to peers and Korn Ferry does show significant volatility on the net margin front and we can also see a low reading when compared to our dataset of five companies. While these are strong peers, when you compare the net margin of Korn Ferry against 1058 companies in the business services industry, it is just above average, performing better than 59.74% of companies. Because the business is very strong on gross margins when compared to all other business services companies (better than 90%), I am hopeful that the company can increase efficiency and amp up its net and operating margins significantly with better resource management.

Korn Ferry Net Margin Peer Analysis (Seeking Alpha)

{kind=link}

Return on Equity & Total Capital

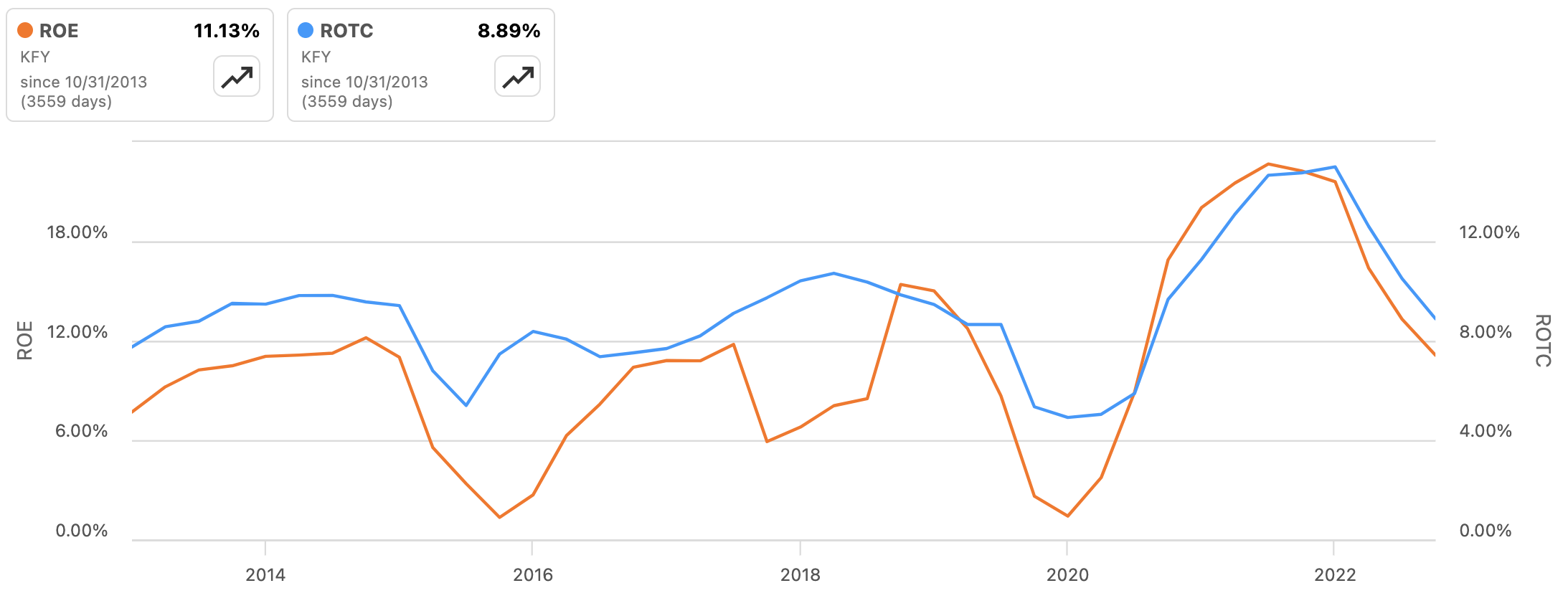

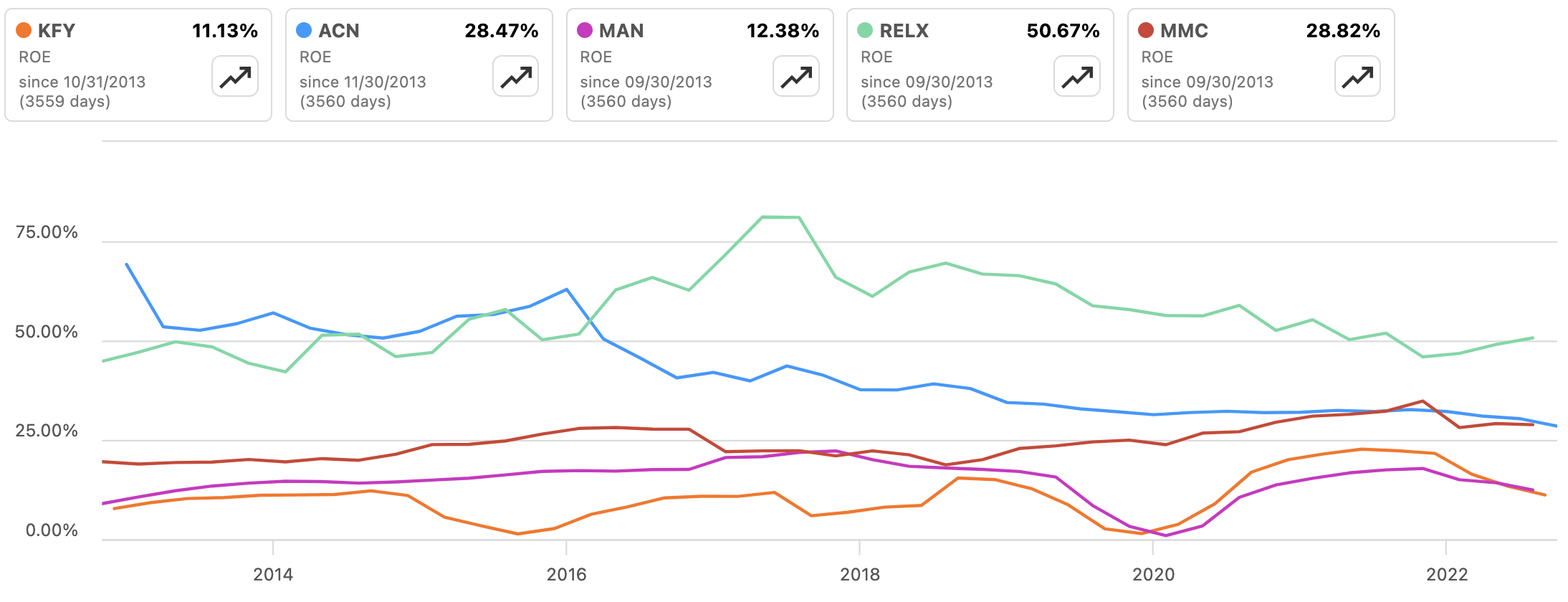

By analysing the return on equity and return on total capital in relation to peers I've gauged further promise on the profitability front.

There is a volatile but upward trend for both ROE and ROTC:

Korn Ferry ROE Vs. ROTC (Seeking Alpha)

{kind=link}

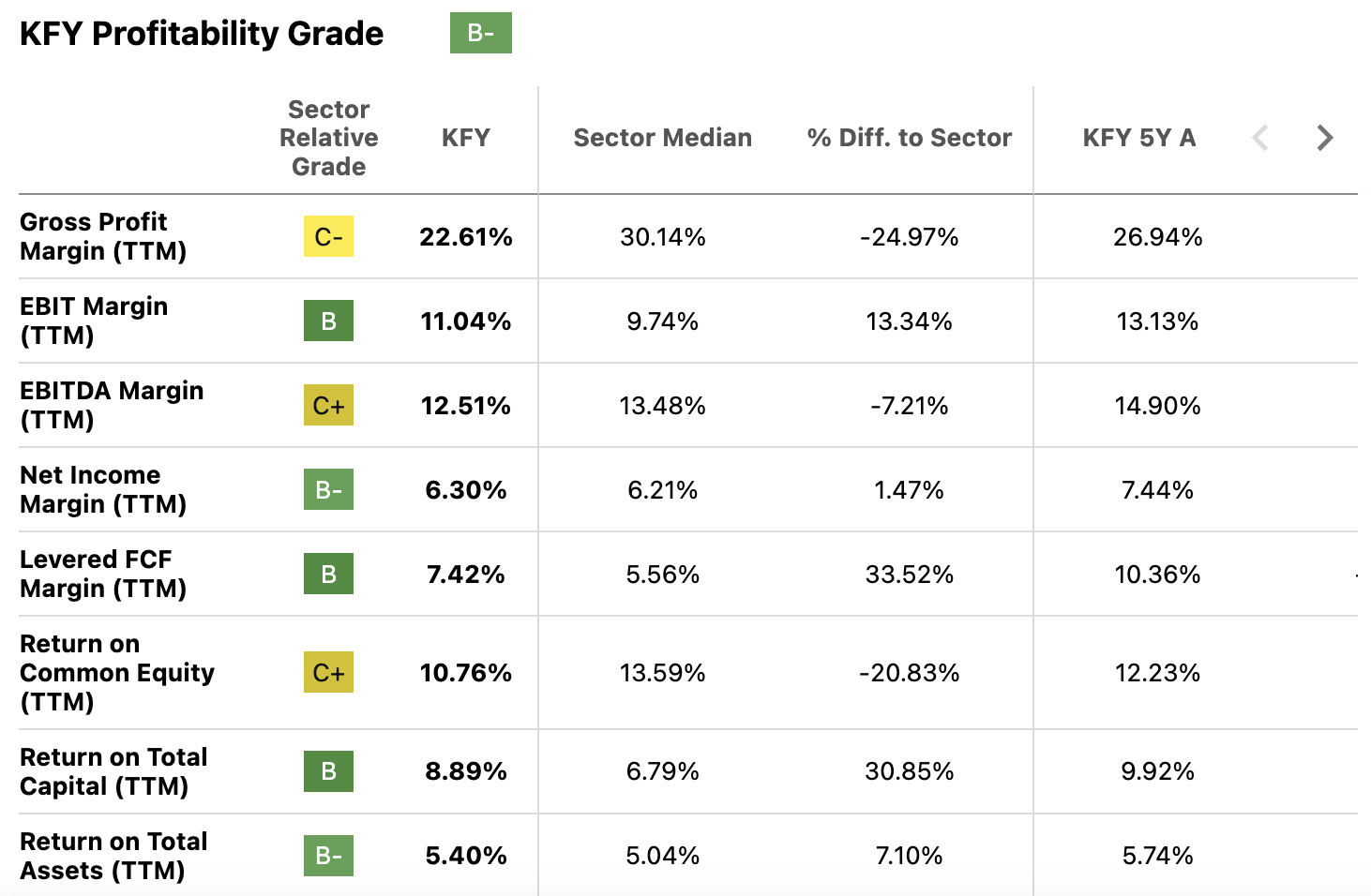

Korn Ferry does have a 30.85% better return on total capital than its peers, but a 20.83% worse return on common equity:

Korn Ferry Profitability Grade (Seeking Alpha)

{kind=link}

Return on equity is low when compared to our dataset of five companies, which is to be expected when we see the standard deviation listed above on the graded C+ return on common equity.

Korn Ferry ROE Peer Analysis (Seeking Alpha)

{kind=link}

Final Thoughts on Profitability

I don't see these profitability results as anything special, but they also aren't anything to worry about and they do indicate profitability health. This investment thesis is hinged on value, and these readings don't detract from the value opportunity at current with Korn Ferry.

I would like to see a better return on common equity and I maintain that this is an issue that can be improved upon with better internal management and stresses on efficiency using both technological and human resources to improve these metrics over the long term. However, I don't expect these factors to play out during my holding period, which as stated, could be as short as when the company returns to fair value. If the company shows radically increased margin and return on equity efficiencies during the course of my investment strategy, it may be shrewd to hold on to the long-term horizon. As yet I have not seen compelling evidence that this is the case.

Financial Health

My analysis shows the biggest risks in a Korn Ferry investment are the cash-to-debt ratio and WACC-to-ROIC ratio. I'll also touch on interest coverage. It is to be noted that these are not major red flags and the company at current does not show any investment deterrent warnings to me.

That being said, I have done a careful analysis of these points to create a compelling synthesis of data on Korn Ferry's financials to gauge what might hold the company back from being a standout investment at this stage. I do expect if I buy Korn Ferry right now it will outpace the index over the next few years. However, on the 10-year horizon, I am not so sure it can; largely because of the financial concerns alongside slowed and stagnant growth.

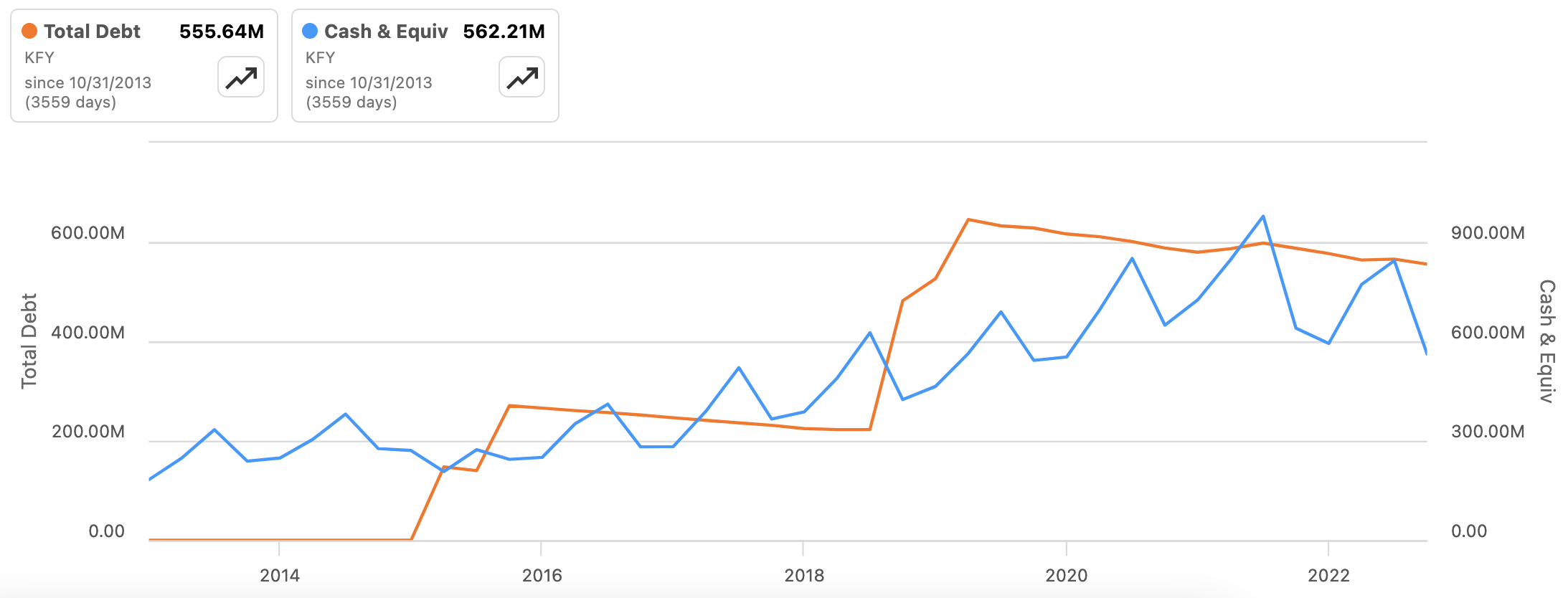

Cash-to-Debt Risk

I've analysed total debt vs. cash and equivalents and you can see there is a notably strong proportion of debt compared to cash.

Korn Ferry Total Debt Vs. Cash & Equivalents (Seeking Alpha)

{kind=link}

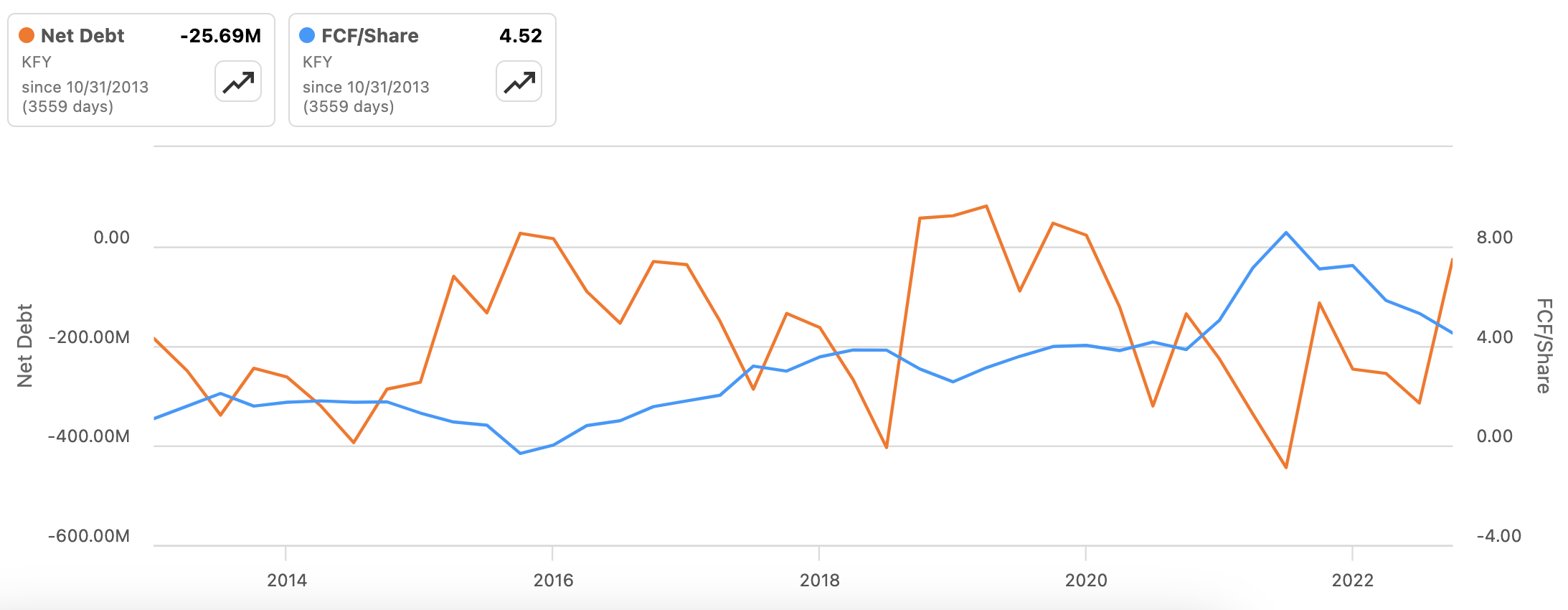

Net debt vs. free cash flow per share is also interesting and the negative net debt does show strong abilities for the company to pay off its debt obligations with sufficient ease most of the time. However, you can see that there are instances, including right now, where the net debt level is almost positive, indicating a tendency to near overextension of debt obligations that does slightly concern me.

Korn Ferry Net Debt Vs. Free Cash Flow Per Share (Seeking Alpha)

{kind=link}

I do believe that the debt level could be further reduced. The weighted cost of raising capital seems high at the moment when compared to the return on invested capital, too, which is what I'll analyse next.

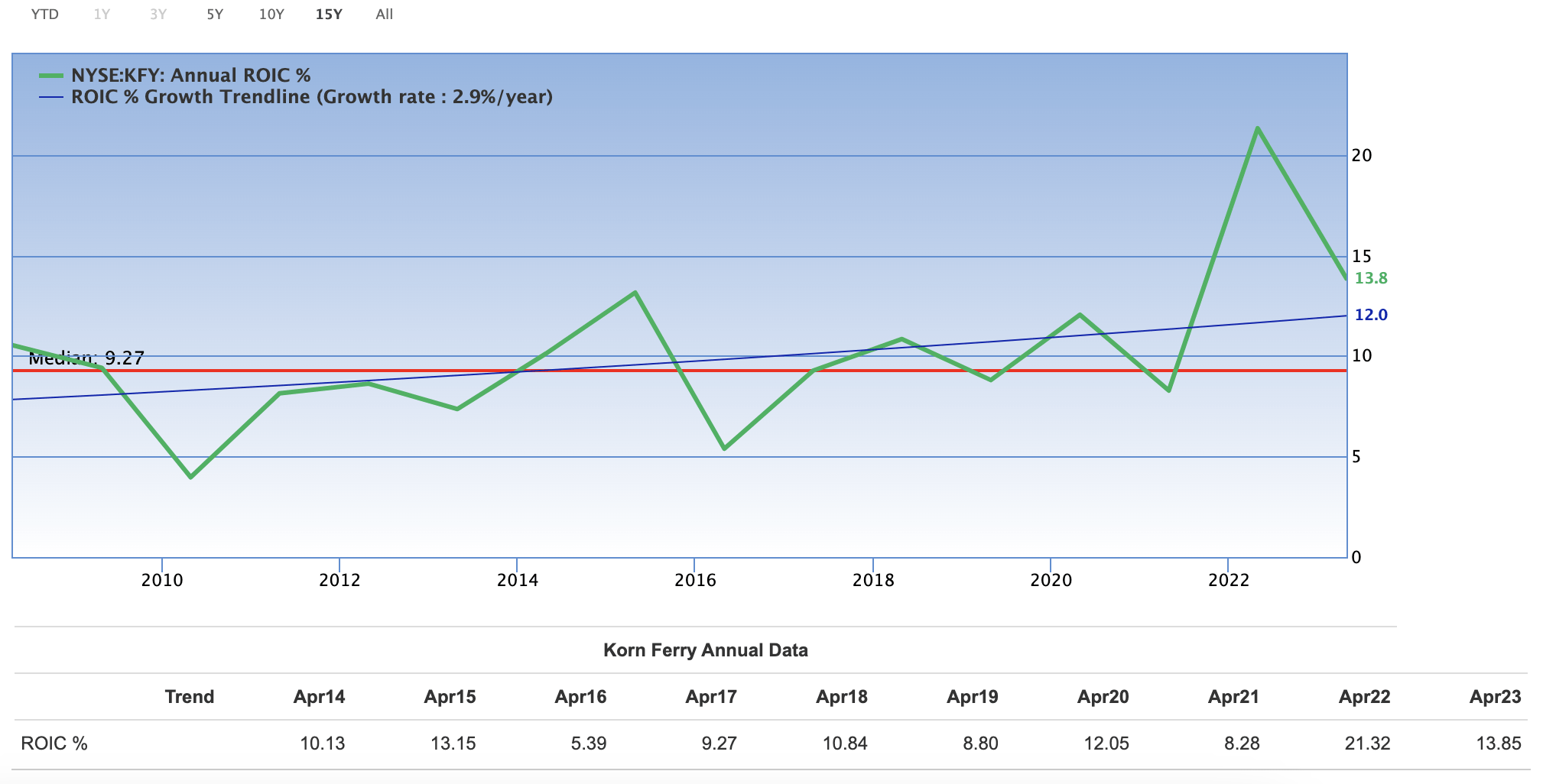

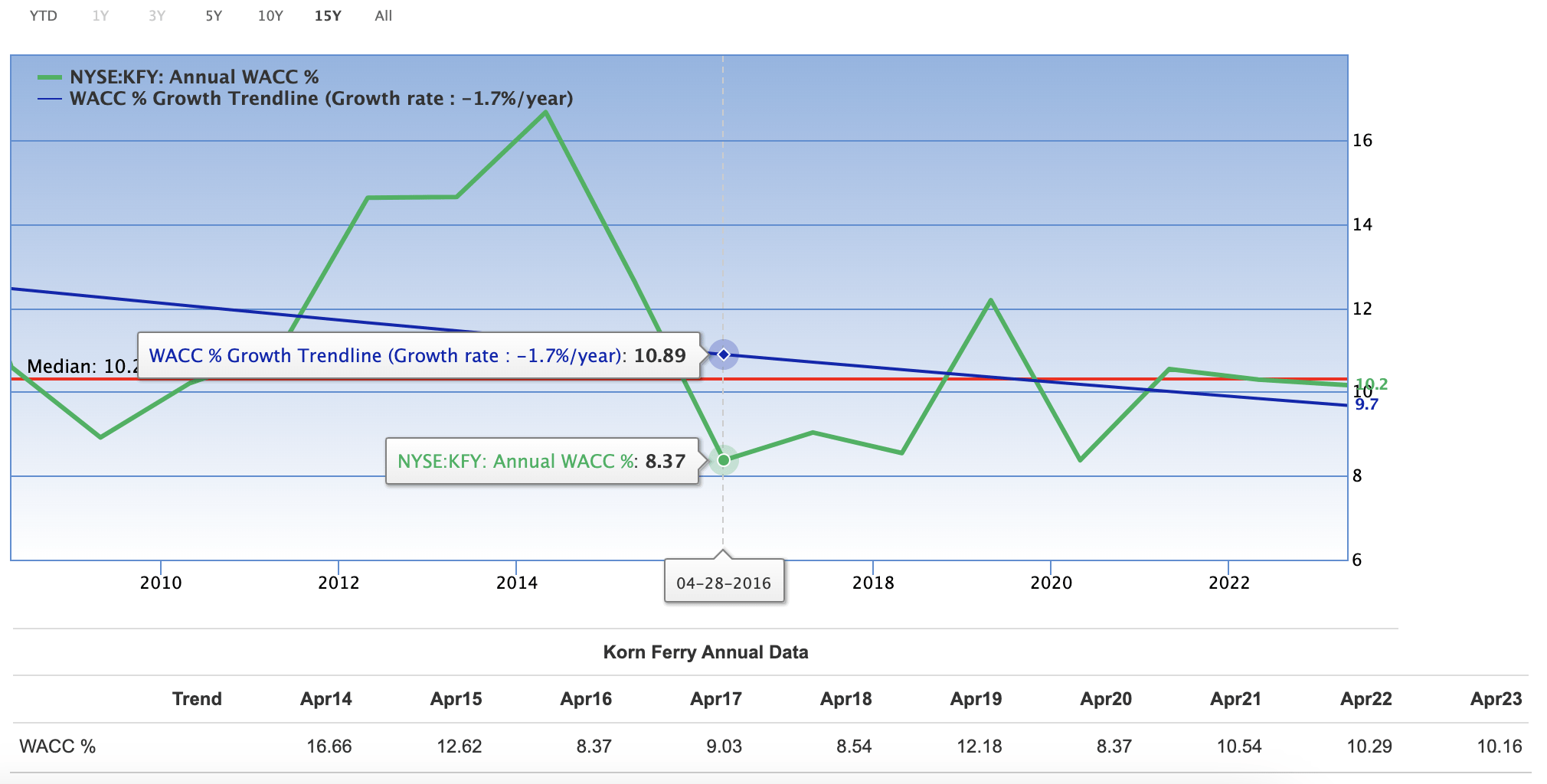

WACC-to-ROIC Risk

I couldn't find comprehensive data on Seeking Alpha for WACC vs. ROIC, so for readers, I sourced the information from elsewhere. I believe this data is an integral part of making an investment decision in the company, especially considering financial health seems to be the company's weakest component.

The weighted average cost of capital employed is 11.57% as of the time of this writing, and the return on invested capital is 11.13%. I'm not impressed by those numbers as they show that Korn Ferry is currently earning a return insufficient to cover the cost of capital.

That being said, from analysing the WACC % vs. the ROIC % it is evident that the company is growing its return on investments and lessening the cost of capital. That's good news and supports my thesis that the company has strong future value potential. I'll be watching carefully to see if Korn Ferry continues to make improvements on this front.

Korn Ferry ROIC % Growth (GuruFocus) Korn Ferry WACC % Decline (GuruFocus)

{kind=link}

{kind=link}

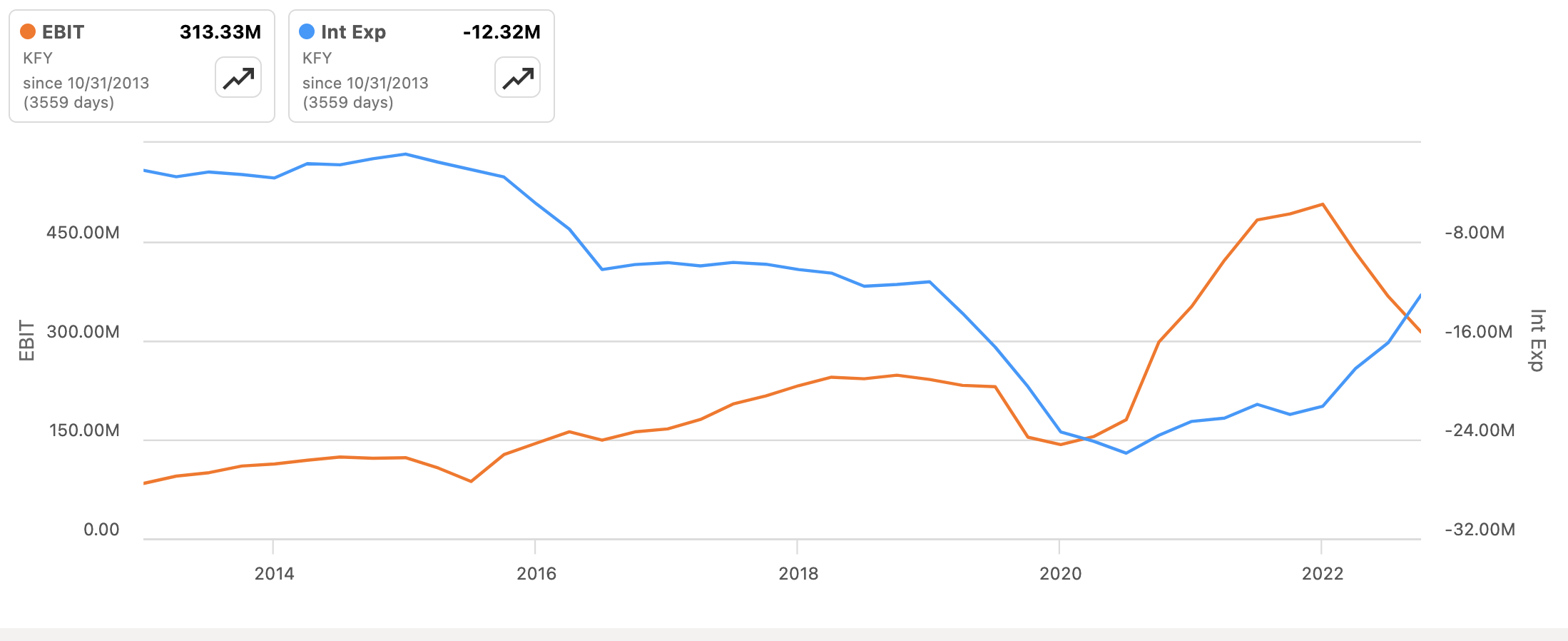

Interest Coverage

I've analysed the company's EBIT against its interest expense and have found the ratio to be quite favourable, but nothing special. It's about average when compared historically and to industry peers.

Korn Ferry EBIT Vs. Interest Expense (Seeking Alpha)

{kind=link}

The current interest coverage for the company is 13.24.

I've noted that the interest coverage is nothing to worry about, a moot point, but good to know in terms of assessing the company's appropriate financial health for investment.

Conclusion

This is an exceptional investment for my portfolio. I bought Korn Ferry stock because I see it as a three-year value play at worst and a 10-year value and growth turnaround story at best.

Highlights

Operations are safe and stress-free generally, with a heavy US component and significant diversification to weather macroeconomic and industry pitfalls. I like the forward-focused conglomerate nature and further acquisitions the company is making to continually diversify and capture market share.

I'm pleased by the great valuation from a discounted cash flow standpoint, with a margin of safety of 65.32% for FCF-based analysis and 44.82% for EPS-based analysis. The low current P/E of 14.02 and P/B of 1.48 are strong indicators of a good price.

Net margins of 6.3% are average for the industry, but gross margins of 22.61% are strong compared to peers in business services generally.

The ROE of 11.13% against peers seems low from my dataset of five companies, but to balance the ROTC is strong in general for the industry.

My biggest concern is the level of debt and the way debt is added and tolerated by the company. I am sure management can stress efficiency and make this better over the long term.

The WACC-to-ROIC is currently poor but is improving with ROIC increasing and WACC declining over time. This is a positive indicator of potentially increased future value.

Verdict

I'm a new shareholder, and I've allocated 5% of my portfolio with approximately a continuous three-year review of Korn Ferry, or selling when the shares reach fair value within that time frame.

Editor's Note : This article was submitted as part of Seeking Alpha's Best Value Idea investment competition , which runs through October 25. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Korn Ferry: Exceptional Value Against Meager Risks