KFY - Korn Ferry: Mixed Performance Continues To Rangebound The Stock

2023-09-28 11:42:41 ET

Summary

- Korn Ferry's performance has been mixed, with positive and negative indicators balancing each other out.

- The company operates in the recruitment industry and competes with other players like Randstad and ManpowerGroup.

- While there are positive trends emerging in the business, declining demand for permanent placement talent acquisition solutions may limit growth.

Investment Action

Based on my current outlook and analysis of Korn Ferry ( KFY ), I recommend a hold rating. KFY performance so far has been mixed, with both positive and negative indicators, balancing each other out. Until there is a clear direction for where the business is headed in the near term, I expect the stock to remain rangebound.

Basic Information

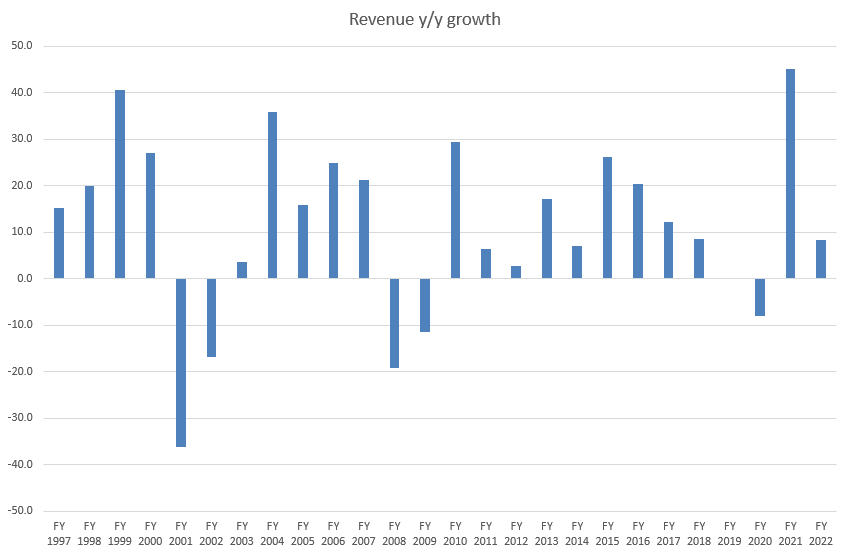

Korn Ferry is in the recruitment industry, where it competes with other players like Randstad, ManpowerGroup, Adecco, etc. You can think of KFY as an outsourced hiring department for a company, whereby businesses will provide job descriptions and requirements while KFY will source candidates. As such, by definition, this is a very cyclical business that sees huge swings in the financials as businesses overhire during the bull cycle (too optimistic) and fire during the downturn, just like what happened over the past 2 years.

{kind=link}

Review

Due to the uncertainty of the current market, I do not think KFY is a good investment at this time. I'll quickly discuss the results of 1Q24. Total fee income was $699.2m, up 0.5% year-over-year (a slowdown from the 1.3% growth seen in 4Q23), with revenue in executive search down 12.1% year-over-year (in constant currency) and RPO down 15.9%. The higher cost of salaries and benefits, as well as the greater proportion of interim staffing revenue with lower margins, led to a decline of 530bps in EBITDA margins to 13.7%. However, EPS of $0.99 were significantly higher than the expected $0.91. Overall, the results were pretty mixed with both positive and negatives.

Let's start with the positive aspects. Undoubtedly, KFY's broad array of income sources enhances its resilience during economic downturns. Presently, the executive and permanent professional search division, known for its challenges in a tight labor market , constitutes approximately 40% of total revenue. The remaining 60% is derived from advisory and interim search services, both of which are displaying favorable trends with year-over-year growth. Notably, the professional search and interim segment expanded by an impressive 43.7%. KFY has recently invested in high-quality interim staffing through acquisitions like Salo and Infinity Consulting Solutions , broadening its market reach and establishing a solid foundation for future expansion. Furthermore, KFY's diversified revenue streams are driving opportunities for cross-selling and capturing greater market share, with the majority of cross-selling activities occurring within Marquee and Regional accounts, collectively contributing to 40% of total revenue.

In regard to new business performance, there are notable improvements across the board. Executive search, which previously declined by 19% in 4Q23, has narrowed its decline to 14% in 1Q24. Consulting new business has shifted from a 4% decline to a 7% growth rate, and the digital sector has moved from a 2% decline to maintaining a stable position. When considered collectively, these trends indicate that KFY is heading in the right direction. Looking ahead, management anticipates consistent growth in consulting, driven by ongoing shifts in the labor market. Particularly, I hold a positive outlook for KFY's digital solutions, as global businesses increasingly recognize the importance of harnessing data for enhanced competitiveness in the years to come.

So I think that's a great opportunity for us. And to continue to use the digital platform as well that we have to drive change within organizations. 1Q24 call

I think we have an enormous opportunity around rewards, compensation, and benefits, both on consulting and digital. The data that we have is just so robust and the opportunity to monetize that data, we have comp data on 30 million people around the world, 30,000 companies. 1Q24 call

On the other hand, KFY has seen a decline in demand for its permanent placement talent acquisition solutions across the world. These solutions include executive search, professional search, and RPO (recruitment process outsourcing). Given that executive search has continued to see significant year-over-year declines in the low double digits during 1Q24, the market is likely to place significant emphasis on this aspect. Moreover, a further 22% drop in 1Q24 follows a 23% drop in 4Q22 for professional search, which is still struggling with significant declines. RPO revenue, which is a leading indicator of future growth and demand stability, has also been falling at a faster rate, up to 16% in 1Q23 from 9% in 4Q22. Notably, RPO new business plummeted by 68% year-over-year to $48 million in 1Q24.

In my honest opinion, KFY stock is probably going to be rangebound for the near term. KFY's performance so far has given both bulls and bears something to chew on. If we look at the KFY stock chart over the past year, the stock has been on a roller coaster ride, bouncing in between the mid-40s and the high 50s. Hence, while there are positive indicators to be encouraged about, I think it is best to sit this one out.

Valuation

Author's work

Being conservative, I am valuing KFY using the market’s (consensus) view, where KFY will continue to see a decline for the rest of FY24, followed by a modest recovery in FY25. Because of the high incremental margin in this business (KFY has a lot of fixed costs—labor), the decline in FY24 will result in a big hit to net margins. On the other hand, the recovery in FY25 should boost earnings growth at a faster rate than revenue, given the increase in margin.

In terms of valuation, I believe the market is pricing the entire industry together, as they are all tied to the macroeconomic health of the country they are mainly operating in. As such, I don’t see a reason for KFY, specifically, to be suddenly trading at a discount. This is especially true when considering that KFY is growing somewhat in line with peers but has higher margins. For the multiple to go up from here, KFY has to show the market that it can grow and recover faster than peers, and I am not confident that it will be able to do so in the near term.

Using these assumptions, the stock is fairly valued at the moment.

{kind=link}

Final thoughts

KFY currently exhibits mixed performance, making a hold rating the most suitable investment action. Positive trends are emerging in the business. However, KFY faces declining demand for permanent placement talent acquisition solutions globally, particularly in executive and professional search, as well as RPO. Given the mixed performance, KFY is likely to remain rangebound in the near term.

For further details see:

Korn Ferry: Mixed Performance Continues To Rangebound The Stock