KFY - Korn Ferry's Steady Growth And Financial Prudence: A Case For Holding

2023-06-29 11:22:39 ET

Summary

- Korn Ferry, a global organizational consulting firm, has shown consistent revenue growth and strong financial management, particularly in Q4 2023, despite a moderation in new business and a decline in earnings.

- The stock performance has been steady but unimpressive compared to the broader market, and its dividend growth may attract income-focused investors.

- The company grapples with new business slowdown, lower adjusted EBITDA margin, and a 42% YoY decline in diluted EPS. Q1 2024 outlook predicts reduced revenue, stagnant EBITDA, and decreased EPS.

- Korn Ferry faces challenges but shows potential undervaluation, with a P/E ratio of 10.21x, lower than the normal 11.32x and a healthy EPS yield of 9.80%.

- The company's dividend yield of 1.47% offers a steady return for income-focused investors. Given these factors, the article suggests maintaining a holding position on.

Thesis

In this analysis, I delve into Korn Ferry's performance and potential from multiple perspectives, including its financial growth, earnings, performance, risk factors, and valuation. As a dominant player in the global organizational consulting scene, Korn Ferry (KFY) has demonstrated consistent revenue growth and proven financial management, particularly noted in its Q4 2023 results . However, certain challenges lie ahead, marked by a moderation in new business and a decline in earnings. The company's overall stock performance has been steady, but unimpressive compared to the broader market, while its dividend growth may attract income-focused investors. A closer look at the company's valuation hints at potential undervaluation. Despite impending obstacles, I suggest maintaining a holding position on Korn Ferry's stock, given its financial solidity and potential for growth.

Company Overview

Korn Ferry is a prominent player in the global organizational consulting landscape. This LA-based behemoth, established in 1969, delivers an array of consulting services via four key business units: Consulting, Digital, Executive Search, and Recruitment Process Outsourcing (RPO) & Professional Search.

With a focused competency in leadership acquisition, Korn Ferry excels in sourcing talent for board level, chief executive, senior executive, and general management roles across public and private sectors. Their expansive reach isn't limited to corporate entities alone; they cater to middle market, emerging growth companies, government bodies, and non-profit organizations as well.

Bullish Q4 2023 Earnings Takeaways

Korn Ferry delivered a Q4 with global fee revenue climbing 8% YoY to $731 million. This uptick was chiefly driven by a solid contribution from recent acquisitions, including ICS and Salo, which notably boosted interim services fee revenue by $70 million YoY. The company's strong performance in the interim services domain was further reflected in a striking 40% YoY surge in the Professional Search and interim business, leading to a total fee revenue of $152 million, up 50% from the same period last year.

Despite a moderation in new business, it remained robust at $115 million in recruitment process outsourcing (RPO). Furthermore, revenue under contract for RPO reached $777 million, illustrating the continued demand for Korn Ferry's high-quality outsourcing solutions.

The company also marked a healthy increase in digital and consulting segments, up 5% and 3% respectively at constant currency. As for KF Digital, its subscription-based revenue model continues to foster growth, with a 2% YoY rise in global fee revenue to $91 million. The digital subscription and license fee revenue stood at $32 million, making up about 35% of the total fee revenue for the quarter.

Despite the decrease in earnings, the company maintains a strong cash position of $488 million, displaying prudent capital allocation throughout fiscal '23, as evidenced by $490 million of cash deployment. A balanced distribution among share repurchases, dividends, capital expenditures, M&A, and debt service further attests to the firm's well-strategized financial management

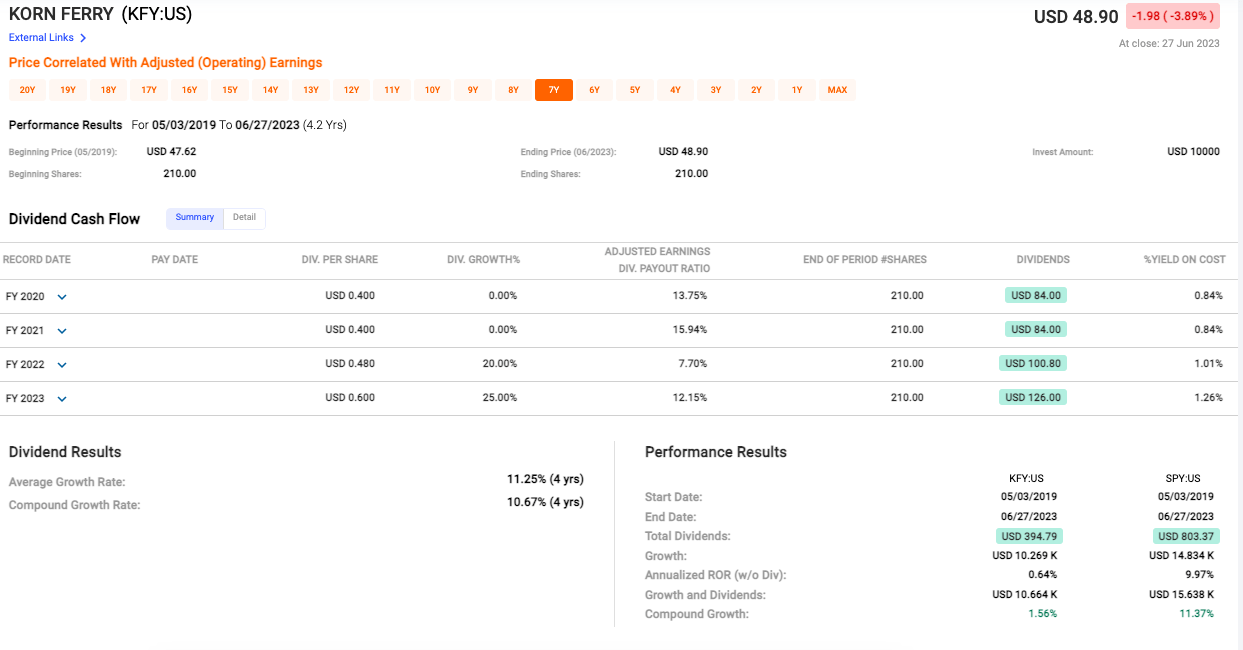

Performance

{kind=link}

Over a 4.2-year period (see data above), the stock had an unimpressive annualized rate of return (ROR) without dividends of 0.64%, indicating sluggish growth in the stock's market value. However, Korn Ferry's dividend payouts have been a brighter aspect of its investment performance representing an average growth rate of 11.25% over the 4-year period. The dividend payout ratio has also fluctuated between 7.7% to 15.94%, indicating a sustainable payout level.

When factoring in dividend payouts, the company's performance appears somewhat stronger, with a compound growth rate of 1.56%. This suggests that while Korn Ferry's stock price growth may have been lackluster, income-focused investors might have found value in its growing dividends.

However, when comparing Korn Ferry's performance to that of the broader market (represented by SPY:US), it appears to have underperformed. The SPY:US provided an annualized ROR of 9.97% (without dividends) and a compound growth of 11.37% over the same period.

Overall, Korn Ferry's performance from 2019 to 2023 indicates a steady, if not particularly robust, stock price growth combined with a consistent increase in dividends, which may appeal to investors seeking consistent income. However, relative to the broader market, the company's returns appear modest.

Risks & Headwinds

On the business development front, Korn Ferry's performance has been somewhat disheartening. With consolidated new business witnessing a 4% dip on a year-on-year (YoY) basis , it's becoming increasingly clear that Korn Ferry's growth trajectory might be hitting a speed bump. An observable slowdown in new business, especially within the executive and professional search domains, is a red flag suggesting that the company may be bracing for slower growth in the immediate future.

Turning our attention towards profitability, Korn Ferry is showing signs of struggle. The company's adjusted EBITDA margin experienced a downward shift, signaling possible operational inefficiencies or cost pressures. Further, the adjusted fully diluted earnings per share experienced a precipitous fall, declining by 42% YoY.

Delving deeper into Korn Ferry's revenue streams, the numbers tell a troubling story. The company's permanent placement fee revenue took a sharp hit, nosediving by 23%. This decline speaks to the challenging market conditions currently facing the firm. It appears as though Korn Ferry's core revenue-generating arm is grappling with headwinds that are significantly affecting its performance.

And as for Korn Ferry's outlook, their guidance for the first quarter of fiscal 2024 is leaning more towards the bearish side. Their projections for the coming quarter show expectations of lower revenue, a stagnant EBITDA margin, and a decreased fully diluted earnings per share. Such a guarded forecast implies that the company anticipates further obstacles on the horizon.

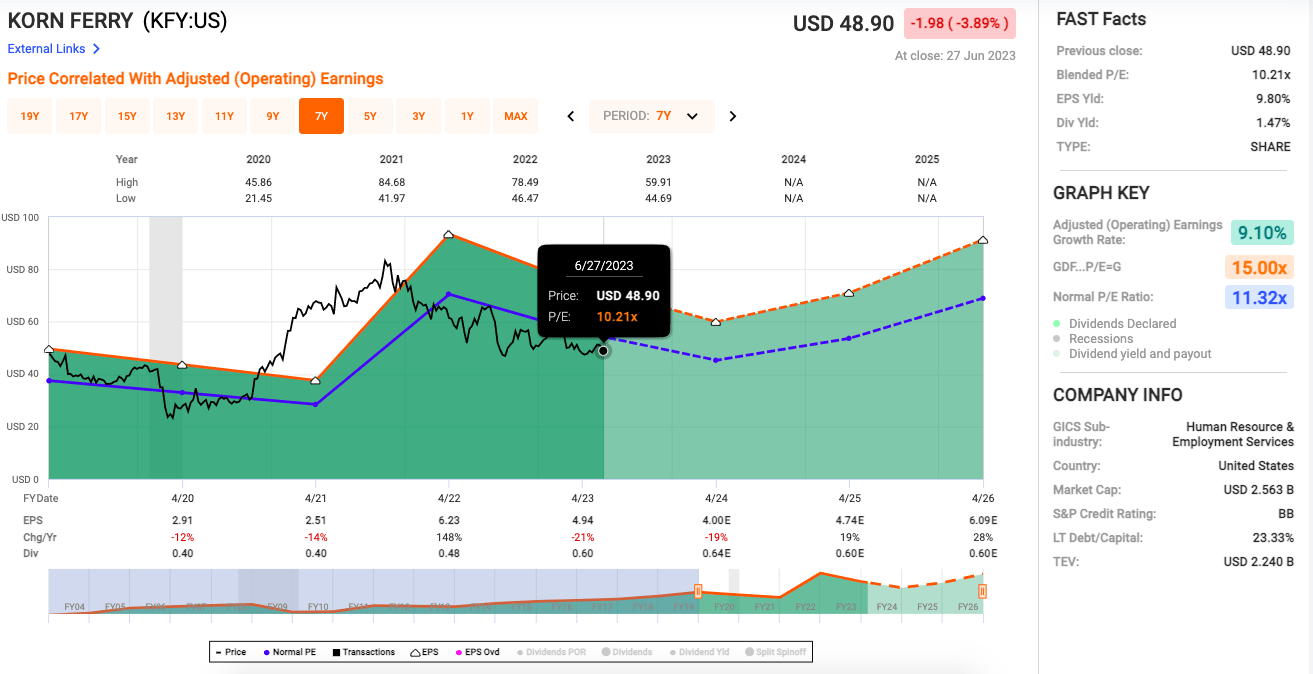

Valuation

{kind=link}

The blended Price-to-Earnings (P/E) ratio stands at 10.21x (see chart above), slightly lower than the normal P/E ratio of 11.32x, potentially suggesting a marginally undervalued status for the firm. The company's earnings per share yield (EPS Yld) is a healthy 9.80%, indicating strong profitability. Concurrently, Korn Ferry has demonstrated a sturdy adjusted (operating) earnings growth rate of 9.10%. Despite the favorable growth rate, the P/E ratio of 10.21x is still below the Gordon's Dividend Discount Model's predicted P/E ratio of 15.00x (GDF...P/E=G), which implies the market may have some more room for further recognition of Korn Ferry's potential. And as for the dividend aspects, Korn Ferry offers a dividend yield of 1.47%, reflecting a modest but steady return for income-focused investors.

Final Takeaway

Given Korn Ferry's consistent revenue growth, particularly with recent acquisitions, robust cash position, and sustained demand for its high-quality outsourcing solutions, it shows promise. Although earnings have declined and new business moderated, the firm demonstrates prudent financial management. Coupled with a healthy P/E ratio suggesting potential undervaluation and a reliable dividend yield for income-focused investors, despite its underperformance compared to the broader market and anticipated challenges, I believe a hold on the stock is warranted.

For further details see:

Korn Ferry's Steady Growth And Financial Prudence: A Case For Holding