KFY - Korn Ferry: Tech-Enabled Talent Expert Trading At A Discount

2023-11-13 19:46:11 ET

Summary

- Korn Ferry’s revenue and EBITDA have grown at a respectable 12% during the last decade, as industry tailwinds and internal development have propelled the company forward.

- We believe the evolution of its service offering, particularly the creation of digital solutions, has future-proofed its business model. Critically, this will reduce the cyclical impact of recruitment.

- Underpinning this is a globally recognized brand and a track record of M&A. Management is incredibly competent and clearly forward-looking.

- Korn Ferry performs well relative to its wider industry, with respectable growth and margins. Although growth is likely to slow, we believe the recent years are more outliers.

- KFY is trading at a discount to its peers and historical average, despite being well positioned. Its FCF yield is sufficient to offset the near-term risk associated with demand.

Investment thesis

Our current investment thesis is:

- KFY is a highly attractive business, primarily due to its broad suite of services. Its revenue profile is highly diversified and to a reasonable extent, allows the business a competitive advantage. Current trading is the perfect illustration of this. While there is clearly a bear market, growth has remained above 0% and margins are in line with the historical average.

- We believe the current management team is strong and their willingness to push heavily into an area of growth, while not necessarily being experts (Digital) is commendable, and the financial results are clear to see. We expect this to become a sequentially more important part of the business in the lead-up to the end of the decade, contributing to a smoother revenue profile.

- Irrespective of this, investors receive a market-leading talent business that operates with strong financial metrics. This is a company trading at a large discount to key benchmarks and has an NTM FCF yield of 9.4%.

Company description

Korn Ferry ( KFY ) is a global organizational consulting firm headquartered in Los Angeles, California. Founded in 1969, the company specializes in talent management solutions, including executive search, leadership development, and organizational consulting. With a presence in more than 100 countries, Korn Ferry serves clients across various industries, helping them identify, attract, develop, and retain top talent.

Share price

KFY’s share price performance has been respectable, with a broad upward trajectory alongside periods of volatility. This has been driven by strong financial performance, with volatility associated with evolving financial metrics as investors seek to forecast the company’s financial performance forward.

Financial analysis

Korn Ferry financials (Capital IQ)

{kind=link}

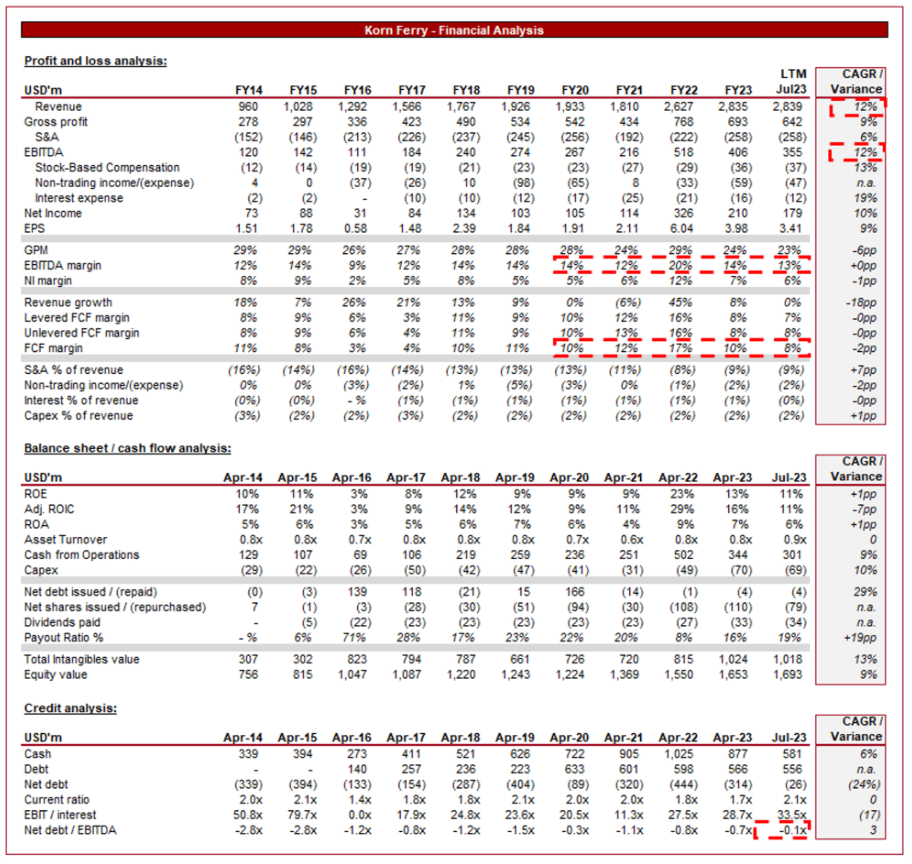

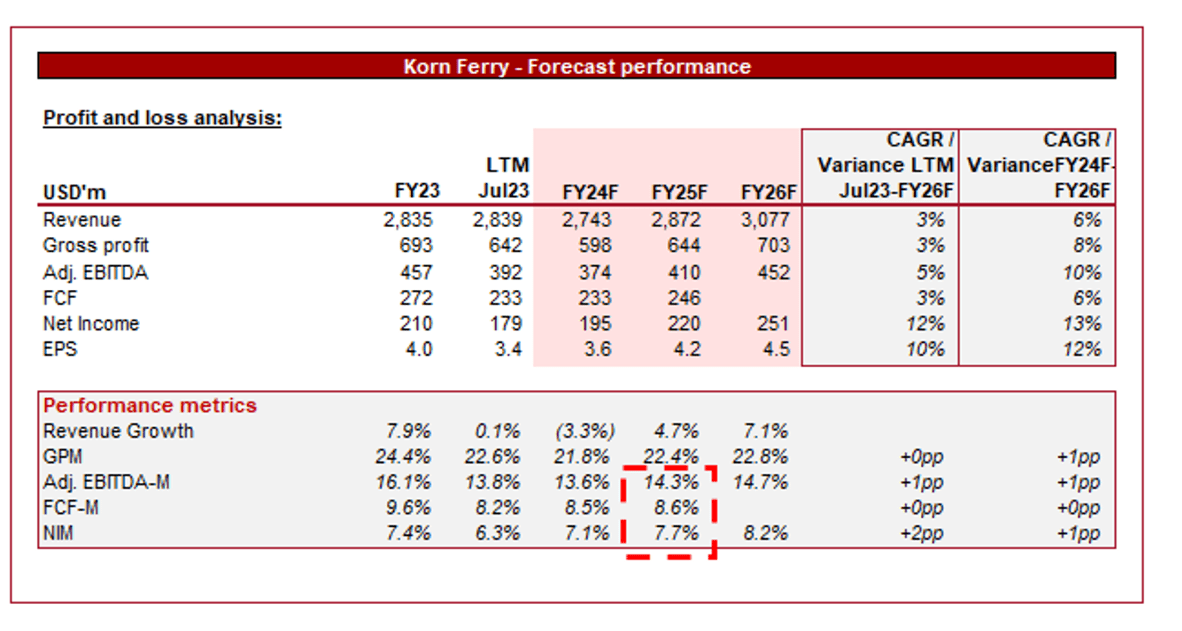

Presented above are KFY's financial results.

Revenue & Commercial Factors

KFY’s revenue has grown at a healthy CAGR of 12% during the last decade, with consistently strong gains year-on-year. There was a clear acceleration in the post-pandemic period, which has now rapidly slowed. EBITDA growth has matched revenue on an average basis, although has fluctuated based on demand.

Business Model

Korn Ferry is renowned for its executive search services. This involves identifying and recruiting senior-level executives, including CEOs, CFOs, and other C-suite professionals, for client organizations. Given the senior leadership focus, the business faces reduced competition and higher compensation, allowing for a more tailored, specialized service. This is one of the primary reasons for Executive Search segment having higher margins relative to the wider talent acquisition industry on average.

This said, the firm does assist clients in recruiting talent at various levels within their organizations, not just executives. Where this is the case, the focus is on high-skilled roles such as managerial, technical, and specialized.

Additionally, KFY offers leadership development programs and services to help organizations groom their existing talent into future leaders. This includes coaching, assessments, and leadership training. Furthermore, it provides assessments and evaluations to help clients understand their talent's capabilities, strengths, and areas for improvement. This has allowed the business to develop its revenue-earning potential by utilizing its brand, contributing to more recurring, less volatile revenue.

KFY has embraced technology by offering digital tools and platforms for talent assessment, data analytics, and talent management (Segment is referred to as “Digital”. This is an area of expansion for the business, with an aggressive innovative strategy, that has resulted in the creation of platforms such as “Korn Ferry Sell”, which is partnered with Salesforce ( CRM ) and Microsoft (MSFT). Management is not embracing technology to “tick a box” but instead actually innovating to transition its business model to include genuine subscription/licensing revenue.

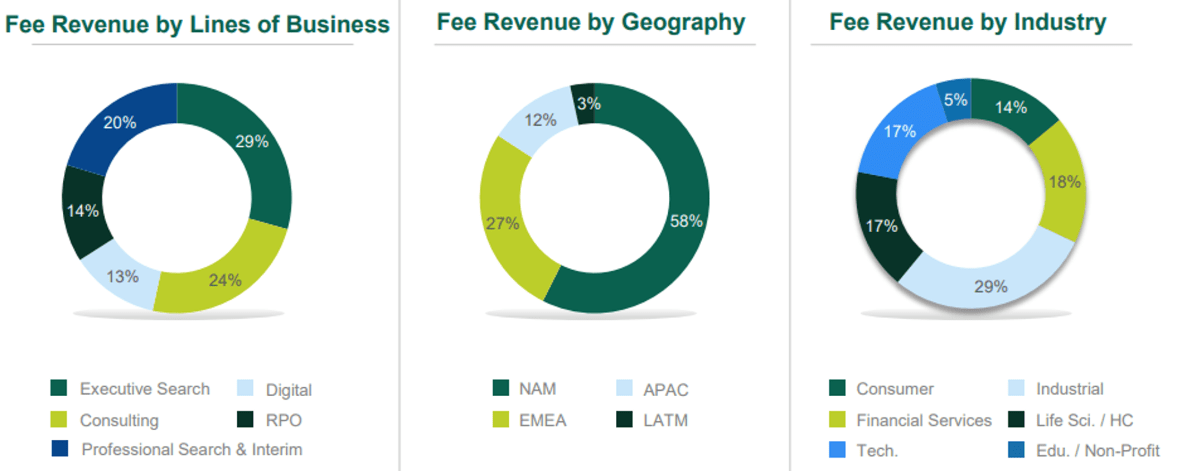

The following is a breakdown of the company’s revenue by key segments. As the initial pie chart shows, revenue is broadly diversified, although it should be noted that several segments are highly correlated to recruitment activities, and so is misleading. Further, KFY is heavily exposed to the US market, which economically has shown itself to be the strongest in the West, and so we are not concerned by this. We are also positive about its exposure growth regions, such as APAC and LatAm. Finally, KFY is well diversified by industry, again reducing any concerns around specific segment cyclicality.

Despite the diversification, it is worth highlighting that this is a highly cyclical business. Without spelling out the obvious, during an economic upswing, recruitment activity will increase, particularly in the higher paying jobs. Equally, during a downturn, there will be a reduction in spending as businesses make redundancies and attempt to minimize costs. KFY is attempting to diversify from this but it remains a key risk to the company.

{kind=link}

KFY has utilized M&A to expand its current market presence, as well as gaining exposure to new segments/industries. Most recently the company has acquired Salo and ICS, further enhancing its current portfolio. This is a strategy we prefer to see given the maturity of the industry, allowing for support to revenue over time.

Talent Industry

The talent industry is highly competitive, owing to the low barriers to entry and its human-capital nature. Businesses such as KFY have been able to differentiate themselves through the development of a brand, a track record, and the network effect with having good talent and clients who are regularly recruiting.

We believe the following industry trends have the potential to drive improved growth:

- Rising Demand for Leadership Development - With technological development and other related factors, there has been a clear increase in the complexity of running a business. This theoretically will contribute to the demand for leadership development programs.

- Growth - The Talent industry is inherently a call option on global growth. With economic expansion and global investment in the development of humanity, the demand for talent will only increase. KFY is well positioned given its truly global business model, with M&A providing the optionality to increase its exposure to particular markets if desired.

- Talent Shortages - In certain industries and regions, particularly STEMs across the West, there are talent shortages, making the need for specialized recruitment services more critical. This is beneficial in numerous ways. Firstly, the demand for specialists will remain strong, with less volatility. Secondly, businesses will rely more heavily on talent management and acquisition, contributing again to greater demand across services.

- Data and Technology - Technology is propelling value across a number of industries, contributing to margin improvement and an uptick in growth rate. The talent industry is ripe for exploitation, similar to how KFY is already doing. We expect continued investment in IP and digital capabilities, contributing to a superior financial profile. The positive with KFY is that it seems Management has identified this as an investment imperative and is showing strong early signs.

Margins

{kind=link}

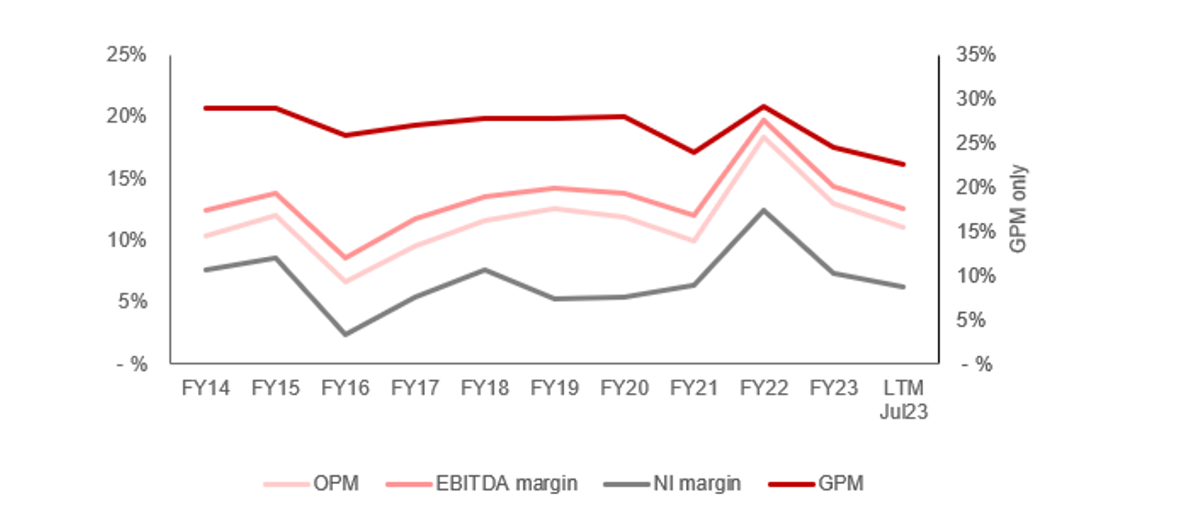

KFY’s margins have been broadly flat, with a gradual upward movement that has usually reverted to the mean. This consistency is credited to the diversified revenue profile of the business, allowing for reduced volatility associated with the cyclical side of the company (recruitment). We do believe there is scope for improvement with growth in it Digital segment, although strong growth in other segments will offset this (which is not necessarily a bad thing).

Quarterly results

KFY’s revenue growth has slowed in recent quarters, although remains positive. In its last 4 quarters, the company posted top-line growth of +13.8%, +0.0%, +1.3%, and +0.5%. It is clear that the slowdown has accelerated in the last 3 quarters, with limited visibility as to whether this will improve. Management remains cautious, as do we, given the limited macro improvement. Our wider view is that economic improvement in 2024 should contribute to an upward swing. Although growth has been kept positive, it has come at the cost of margins, with EBITDA-M falling in the LTM period to 13% and the last quarter being 10.7%.

The key takeaways from KFY’s most recent quarter are:

- Consulting (24% of revenue) - Revenue growth of 1%, driven by a strong performance across many of its sub-categories, although heavily weighted down by Leadership Development. This likely reflects a reduction in corporate spending in the face of inflationary conditions.

- Digital (13%) - Revenue growth of 5%, with subscription and licensing revenue (34% of the 13%) developing extremely well. This segment is receiving a lot of Management focus and is reflected in its trajectory.

- Executive Search (29%) - This segment has suffered heavily from the wider macro environment, with every region down. This is the segment that is weighing substantially on the company, contributing to the broader flat revenue.

- Professional Search & Interim (20%) - Growth driven by acquisitions and higher Interim services, with a positive movement in average billing rate.

- Recruitment Process Outsourcing (14%) - Fee revenue is down, primarily due to a reduction in hiring volume in line with Executive Search.

Overall, it has been an underwhelming quarter for the company, primarily due to the heavy weighting toward Executive Search. The positives are clearly the diversification away from this segment, which has the potential to create a less volatile, upward revenue profile.

Balance sheet & Cash Flows

KFY’s balance sheet is fairly uneventful, with margins translating well to FCF, allowing the business to minimize debt usage. This excess cash has been reinvested within KFY, alongside distributed to shareholders. Dividends have grown mildly but excess cash allocation has gone to buybacks. Management does have a preference to hold a healthy cash balance, which is defensive in nature (and allows for M&A optionality) but with greater scale should mean higher distributions.

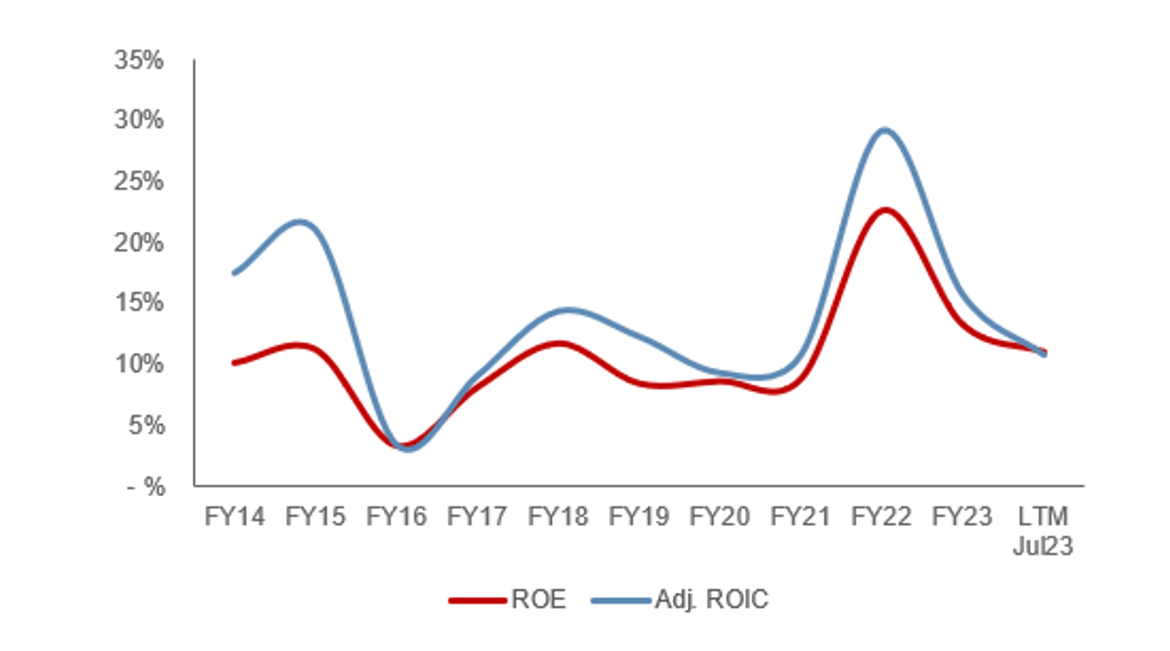

Looking at its returns in an alternative fashion, KFY’s ROE has broadly improved over the historical period, implying accretive reinvestments for the benefit of shareholders. There has been some volatility, but this has always been in an upward direction.

{kind=link}

Outlook

{kind=link}

Presented above is Wall Street's consensus view on the coming 5 years.

Analysts are forecasting a slowdown in the company’s growth rate, with a CAGR of 3% into FY27F. In conjunction with this, margins are expected to incrementally improve, although are not expected to exceed the FY23 level achieved.

We consider these assumptions reasonable. Given the heavy cyclicality of KFY, projecting forward is always difficult. However, given the strong upswing from “abnormal” circumstances, we expect a period of normalization where growth levels off. The question is whether Digital will have a material-enhancing effect in the near term, which we suspect is possible but requires a longer time frame to offset the trends from Executive Search.

As for margins, we are less glaringly positive. The company has faced cyclicality in revenue which directly translates to margin movements. With growth slowing, we would expect margin improvement to be minimal.

Industry analysis

Human Resource and Employment Services Stocks (Seeking Alpha)

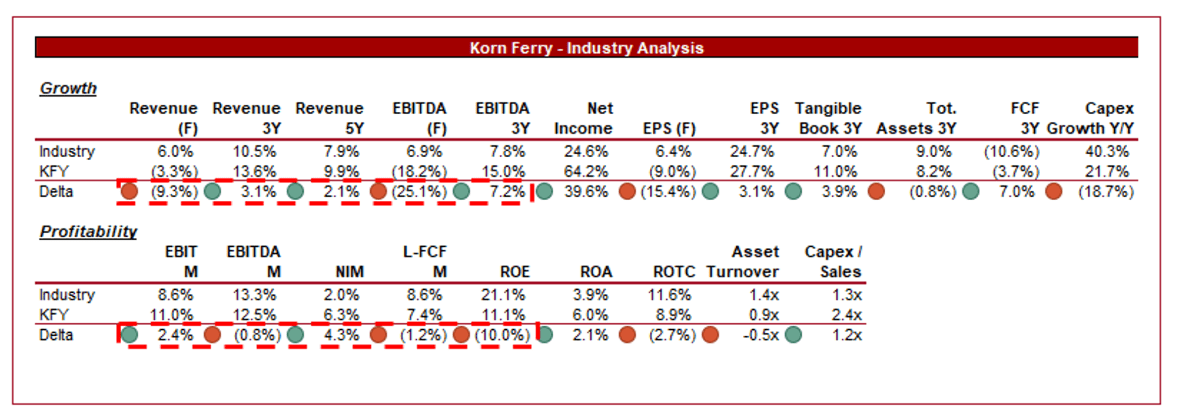

{kind=link}

Presented above is a comparison of KFY's growth and profitability to the average of its industry, as defined by Seeking Alpha (26 companies).

KFY performs modestly relative to its peers, without standing out. The company’s revenue and profitability growth has slightly exceeded the average across both a 3Y and 5Y period, while its forward estimates underwhelming. The outperformance is a reflection of the talent segment’s upswing relative to the wider HR/Employment segment.

From a margin perspective, KFY also performs well. Its margins are broadly in line with the industry as a whole, with NIM higher and EBITDA-M/FCF-M lower. We consider this a strong performance given its exposure to the Talent segment, which usually has lower margins. This is owing to its consulting focus.

Valuation

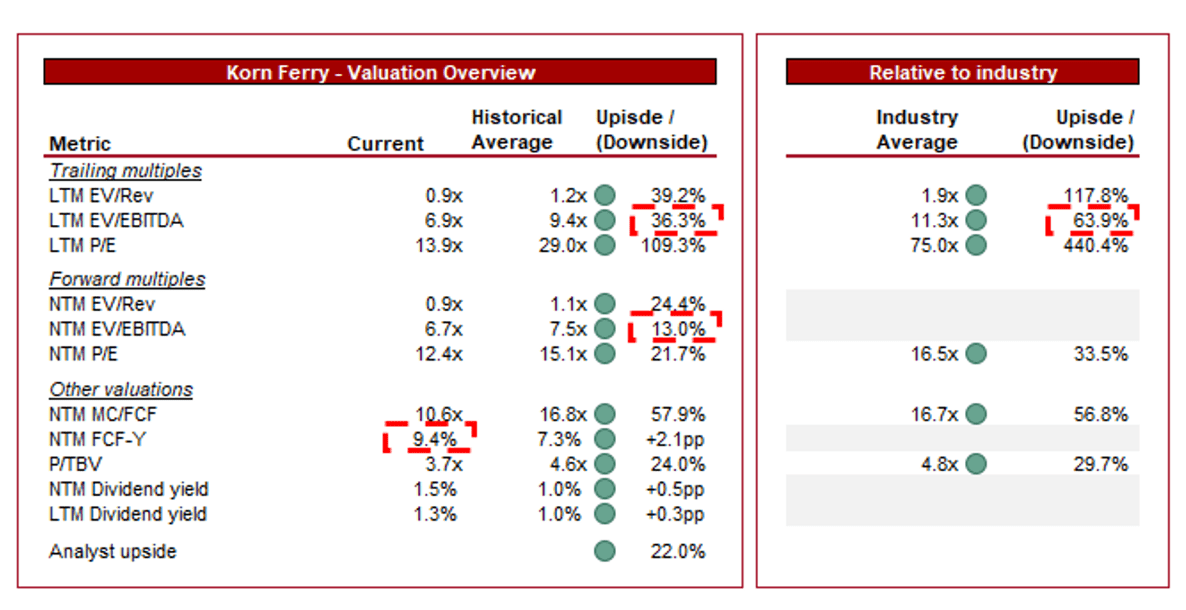

{kind=link}

KFY is currently trading at 7x LTM EBITDA and 7x NTM EBITDA. This is a discount to its historical average.

A discount to the company’s historical average appears reasonable from a conservative view, primarily due to the increased risks associated with a lower-than-average growth rate. This said, the company has greater scope, margin stability in line with its historical average, and commercial development. We could easily accept an argument to suggest parity or even a small premium. This discount appears to reflect investor sentiment around the industry as a whole currently.

Further, the company is trading at a substantial discount to its peer group, with a 64% discount on an LTM EBITDA basis and a 34% discount on a NTM P/E basis. We consider this difficult to justify, primarily due to its comparable financial performance and the broader quality of the Consulting/Digital industry. As the peer group includes exposure to technology and other higher growth opportunities (while being less cyclically linked), we do still concur that a discount is reasonable.

Based on both considerations, we believe there is a sizeable upside with KFY at its current price. Importantly, The company’s FCF yield and broader business development have been positive while its valuation has ticked down, representing greater value for shareholders.

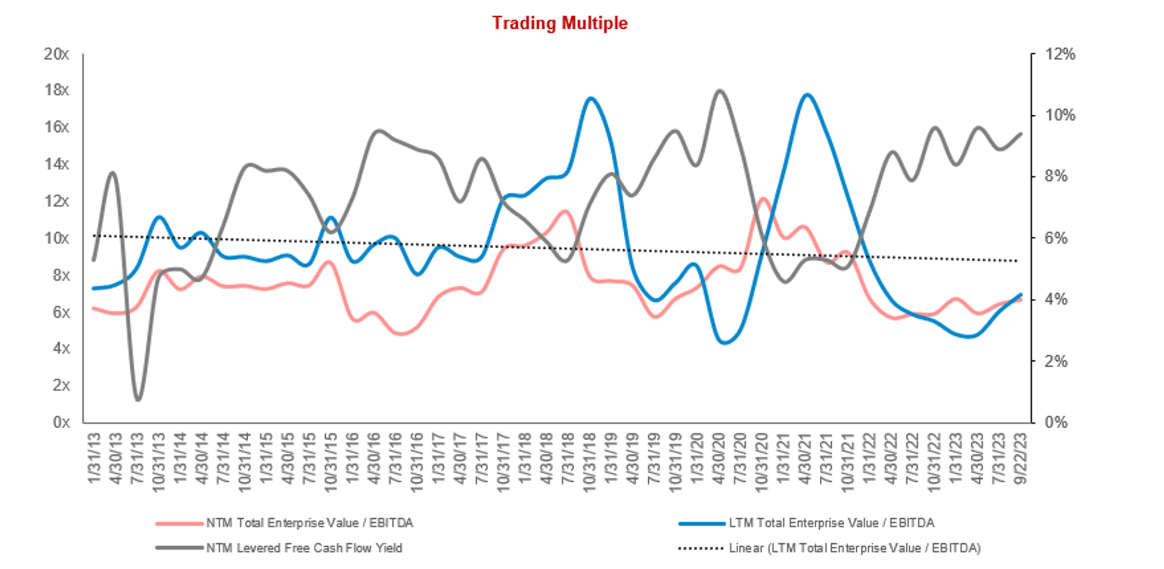

Valuation evolution (Capital IQ)

{kind=link}

Final thoughts

KFY is a strong proposition within the Talent industry. The company has achieved good growth and attractive margins, owing to its strong brand, the delivery of quality service, and the expansion of its solutions. Although it is difficult to develop a wide moat within this industry, its focus on the high-end segment and expansion of solutions to deepen its ties to clients has given it a preferential position within the industry.

With a strong management team and a respectable performance relative to its peers, we consider the business an attractive investment proposition. Underpinning this is a growing FCF yield and a wide delta to its current valuation.

For further details see:

Korn Ferry: Tech-Enabled Talent Expert, Trading At A Discount