KKPNF - KPN: A 4.5% Yield With A Sub-70% Payout Ratio

2023-05-08 11:30:00 ET

Summary

- KPN is the largest telecommunications company in the Netherlands.

- Although it needs to invest in its product offerings to protect its market share, the underlying free cash flow remains strong.

- The FCF performance is stronger than you'd expect as the cash taxes are lower than the tax expenses due to a large, multi-billion euro loss generated in 2014.

- The company will pay a 15 cent dividend in 2023. This will be covered by a 22 cent per share free cash flow performance.

- KPN has launched a EUR300M share buyback program. This should reduce the share count by more than 2%.

Introduction

KPN ( KKPNF ) ( KKPNY ) is the largest telecom company in the Netherlands. The operating and financial performance has been better than I had expected in the past few years, and the company's cash flows remain strong despite dealing with competition in its domestic markets. As it has been a few years since I last had a look at KPN , I wanted to check up on the company's Q1 2023 results and FY 2022 results to see if it should be one of the few European telecom companies I should have a closer look at. As a one-stop shop, KPN offers mobile and fixed line telecom solutions as well as internet packages to its customers in both the B2B and B2C segment.

{kind=link}

As KPN is a Dutch company, it's perhaps not a surprise it's listing on Euronext Amsterdam is the most liquid listing. The company is trading in Amsterdam with KPN as its ticker symbol and the average daily volume is almost 13 million shares. The current market capitalization is just over EUR13B.

Off to a good start in 2023

About a decade ago, KPN was the subject of a takeover battle as it received an unsolicited offer from Carlos Slim's America Movil ( AMX ). The KPN management and board objected to this EUR 2.40 offer , claiming the offered price was undervaluing the company, but unfortunately, the company's share price has continued to tread water in the past ten years (not unlike suitor America Movil).

{kind=link}

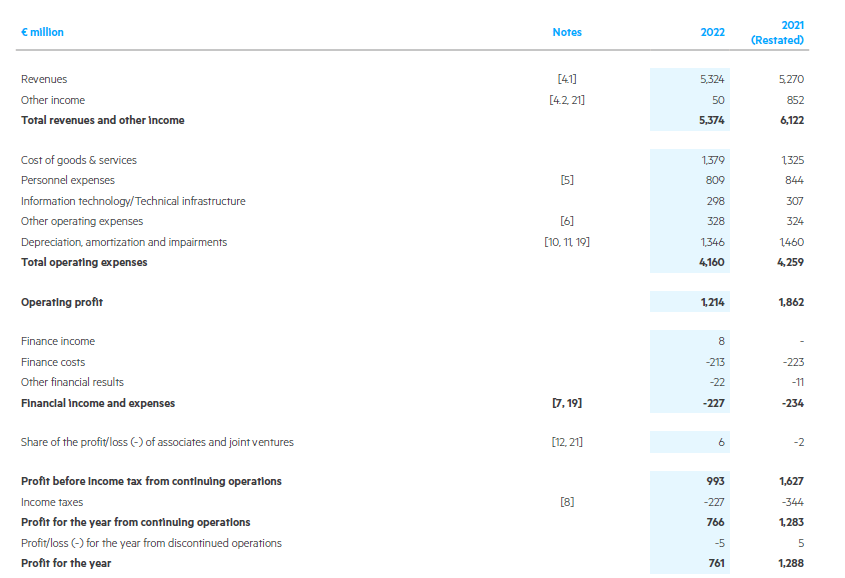

Before discussing the Q1 trading update, I think it's a good idea to look back at FY 2022 to 'set the scene'. The company reported a total revenue of almost EUR 5.4B in FY 2022 which is a decrease of more than 10% compared to FY 2021. That's not alarming considering the FY 2021 performance was boosted by a EUR800M higher 'other income' which was related to the non-recurring sale of Glaspoort, a subsidiary. Excluding the non-recurring items in both years, the revenue would have increased by approximately 1%.

{kind=link}

Fortunately, the operating expenses decreased by approximately 2.5%, and this was almost entirely related to slightly lower personnel expenses and a substantial decrease in the depreciation and amortization expenses after the deconsolidation of Glaspoort BV (which is now reported on as a joint venture). The operating profit was approximately EUR1.21B and if we would deduct the 'other income' from the equation in both 2021 and 2022, the underlying operating profit would have increased by approximately 15% to EUR1.16B.

A very respectable result indeed, and 2022 generally was a good year as the pre-tax income of EUR993M resulted in a net income of EUR766M of which EUR761M was attributable to the shareholders of KPN. And while the EPS came in at 18 cents per share, using the current share count of 4.04B shares outstanding, the EPS would be 19 cents per share.

The main issue I currently have with European telecom companies is the heavy capex bill they are all facing to roll out fiberoptic internet and to continue to invest in 5G. Fortunately, KPN has been able to spend its Euros quite wisely and the free cash flow remained pretty strong in 2022.

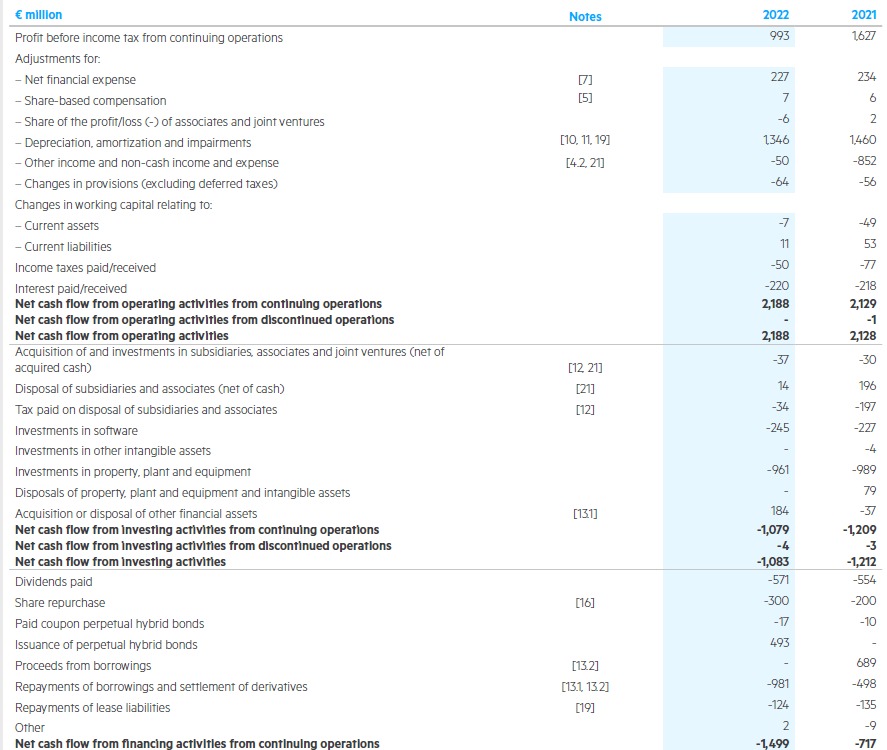

KPN reported an operating cash flow of EUR2.19B, but this included just EUR50M in cash income taxes paid (versus the EUR227M in income taxes incurred as per the income statement). We should also deduct the EUR17M coupon paid on the hybrid bonds (which are considered equity on the balance sheet, so it's only fair to take these payments into consideration as well) and I am deducting the EUR124M in lease payments.

{kind=link}

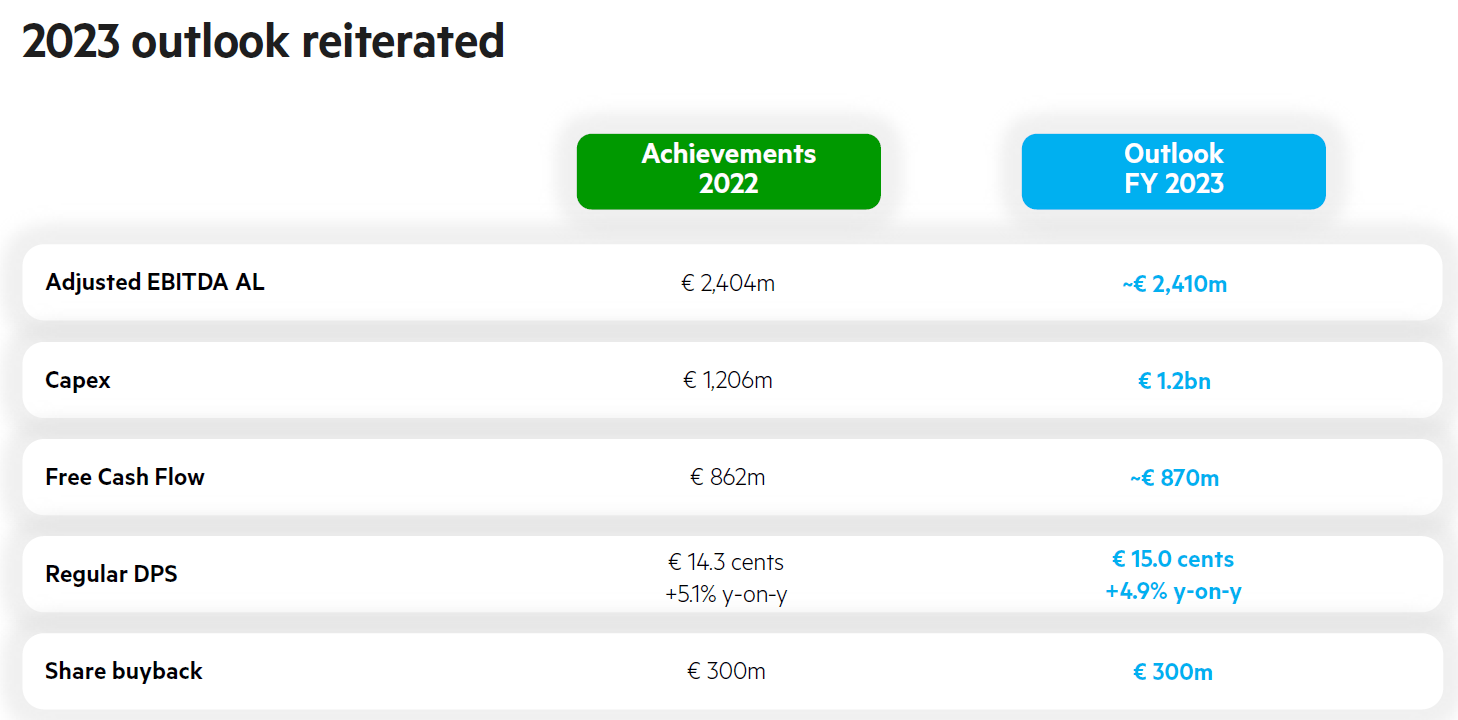

This means that on an adjusted basis, the operating cash flow was EUR2.04B (and approximately EUR1.85B if I would use the actual recorded tax bill). The total capex was EUR1.2B, resulting in a free cash flow result of EUR840M (or EUR665M) depending on whether or not you use the amount of taxes paid or taxes owed. Divided over the current share count of 4.04B shares, this represents a free cash flow result of EUR0.21 per share or 16.5 cents per share. In both cases, the 14.3 cent dividend is well-covered.

KPN also sounded upbeat for 2023. The company expects its EBITDA AL to come in at EUR 2.41B (which is less than 1% higher than in 2022) and is guiding for a free cash flow result of EUR870M after spending about 1.2 billion Euro on capital expenditures. As KPN also announced a new EUR 300M share buyback program , it will likely repurchase 100M shares this year.

If I'd err on the side of being cautious and assume about 75M shares will be repurchased, the year-end share count will decrease to just 3.97B shares and a free cash flow result of EUR870M would then result in a free cash flow of 22 cents per share. KPN is guiding for a full-year dividend of 15 cents per share, which would indicate a payout ratio of just under 70%. The main caveat here is that the FCF guidance likely includes the (lower) amount of taxes paid versus the total amount of taxes owed. That's fair, as KPN is currently using the losses it recorded on the sale of its E-Plus stake in 2014 . The loss realized on that sale has acted as a very effective shield against income taxes since 2014 and will likely continue to shield the company from cash taxes in the foreseeable future.

{kind=link}

Investment thesis

The free cash flow will nose dive as soon as KPN will actually have to pay taxes on its pre-tax income result, but it's not an element to worry about right now. This means the stock is currently trading at a free cash flow yield of 6.7% and the dividend yield of 4.5% is fully covered. Additionally, the EUR300M share buyback program will also add value.

I haven't been too keen on European telecom companies as they are all entering a heavy investment cycle, but KPN has done a good job in managing the investment risks. I currently have no position in KPN, but it could be a valid candidate to reinvest my proceeds from the sale of Telenet (TLGHF) (TLGHY), a Belgian telecom company which is currently the subject of an all-cash buyout offer from majority shareholder Liberty Global (LBTYA) (LBTYB) (LBTYK).

For further details see:

KPN: A 4.5% Yield With A Sub-70% Payout Ratio