KHC - Kraft Heinz: 3 Reasons To Buy The Stock

2023-08-03 13:23:29 ET

Summary

- Kraft Heinz is focusing on innovation and growth in high-margin sectors, such as mom & pop stores and hospitality & schools.

- The company has substantially reduced its debt, improving its financial position and interest coverage.

- Kraft Heinz has reported strong earnings growth and has a positive outlook for future sales and profitability.

Introduction

Kraft Heinz ( KHC ) is one of the largest food companies in the United States with sales of more than $26 billion. It offers a wide variety of food and beverage products worldwide.

The stock is also a long-term favorite in Berkshire's portfolio with an equity allocation of nearly 4%. However, the stock price has had a wild ride since the merger in 2012. The share price fell significantly in 2017, which I think was mainly caused by the high level of debt. Both debt and costs were significantly reduced. Now that the company is leaner, it's time for a second look. In my article I present 5 reasons why I think the stock is buy-worthy.

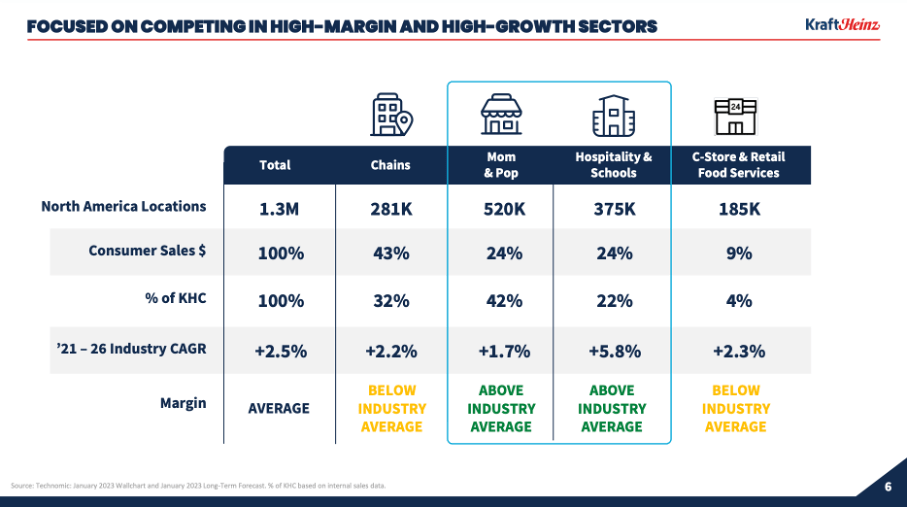

Reason 1: Continued innovation.

Focus On High-Margin and High-Growth sectors. (2023 Analyst Day)

{kind=link}

The qualitative factor of management is important. Kraft Heinz is a company with good management characteristics favored by its continuous pursuit of growth and innovation.

Kraft Heinz does not believe that cutting costs should mean cutting innovation. Kraft Heinz is still innovating strongly by focusing on high-margin, high-growth sectors such as mom & pop stores and hospitality & schools. Kraft Heinz is expected to grow above the industry average in the coming years in these growth sectors.

In addition to focusing on growth sectors, introducing new products should also increase sales, such as the new spicy ketchup flavors and Heinz Hot 57 sauce. Consumers prefer a variety of spicy sauces and flavors. Therefore, Heinz is in a unique position to capitalize on these consumer trends.

Heinz Remix (Kraft Heinz website)

{kind=link}

These sauces are also being introduced in a new ketchup machine called Heinz Remix , where consumers can personalize tomato sauce. Consumers can choose a range of sauces, such as Heinz ketchup, 57 sauce or BBQ sauce, and customize them to their needs with flavors such as jalapeno, smokey chipotle, buffalo and mango. The launch is scheduled for restaurant operators in 2024.

I mentioned in the introduction that debt was significant. Therefore, Kraft Heinz focused on cost and debt reduction, which usually means less innovation. The company's constant focus on innovation is the result of strong management.

Reason 2: Substantial debt reduction.

The stock price crash from 2017 to 2019 opened the eyes of many investors as well as those of management. Investors believed that the level of debt was unacceptably high and that the predicted rate of earnings growth could not be realized. What was the size of the debt and how does it compare to the present debt?

Prior to the stock price crash in 2017 to 2019, Kraft Heinz has a sizable debt load of around $30 billion. With $31 billion in total debt and $1,284 million in interest costs in 2018, the average interest rate was 4.1%. Its interest coverage was therefore 4.5, which is suitable. Companies should have an interest coverage of at least 5 or higher, according to Benjamin Graham (from the book Security Analysis). Low interest rates made the size of the debt unproblematic.

The Fed's continued sharp increases in interest rates from 2016 caused Kraft Heinz's interest expense to rise to $1,394 million by 2020. The total amount of debt decreased to $28.3 billion, and the average interest rate rose to 4.6%.

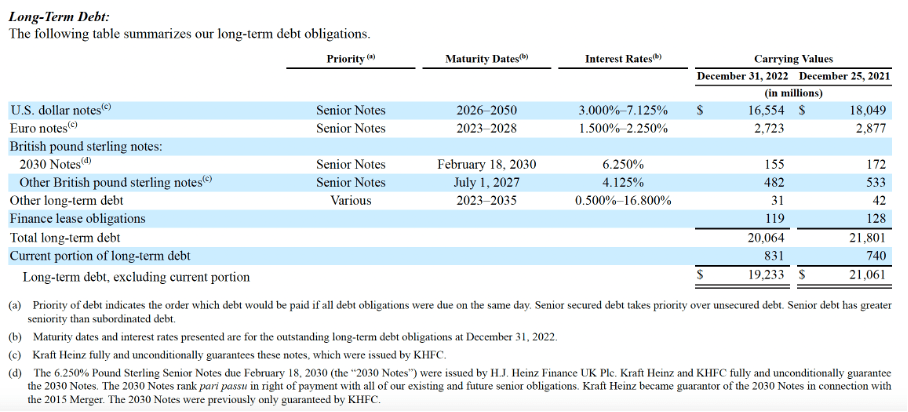

Long-term debt (Kraft Heinz 2022 Annual Report)

{kind=link}

Source: 2022 annual report

The total amount of debt has been decreased to $20.1 billion, and the TTM interest expense has been decreased to $906 million, giving us an average interest rate of 4.5%. Interest coverage improved to 5.2. Fortunately, most of the long-term debt matures after 2026. I think the Fed will cut interest rates by then because of the upcoming recession.

The merger's increased leverage and earnings that fell short of analyst projections led to a sharp decline in the company's share price. Since the debt has been lowered to an acceptable level, Kraft Heinz and its stockholders will benefit substantially. Earnings will increase because of lower interest expenses and lower costs which could lead to increased dividends.

Reason 3: Earnings growth and outlook.

Due to price increases of 11%, Kraft Heinz was able to raise organic revenues by 4% year over year in the second quarter of 2023 despite the substantial fall in sales volumes. However, organic sales growth was slightly behind expectations as analysts projected growth of 4.6%. Geographically, organic sales rose the fastest internationally, at a staggering 13.2% versus 1.3% in the US.

Kraft Heinz reported strong adjusted EBITDA with 6% year-over-year growth to $1.6 billion thanks to price increases and improved operating efficiencies. With this, adjusted earnings per share rose 12.9% to $0.79, which is better than analyst consensus of $0.76.

The future looks bright for Kraft Heinz. For fiscal 2023, Kraft Heinz expects annualized organic sales growth between 4% and 6% and adjusted EBITDA growth of 6% to 8% at constant currency (excluding a lapping 53rd week in 2022). Adjusted earnings per share will be between $2.83 and $2.91 (mid-year growth of 3.2%).

Conclusion

Shares of Kraft Heinz took a big hit several years ago. The company has since sharply reduced its debt in times of rising interest rates. Management is well on its way to increasing profitability by introducing new products, reducing debt and cutting costs. They focus on high-margin, high-growth sectors to differentiate themselves in the market.

With an forward P/E ratio of only 12.4x, Kraft Heinz scores significantly better on stock valuation compared to the industry median with an forward P/E ratio of 18.9x. Despite low single-digit projected sales and earnings growth, Kraft Heinz is favored for its extraordinary 4.5% dividend yield. I think Kraft Heinz is a solid investment because of its improved outlook, streamlined operations and significantly lower debt.

For further details see:

Kraft Heinz: 3 Reasons To Buy The Stock