KHC - Kraft Heinz: 5% Yield And Up To 40% Undervalued

2023-09-07 04:47:31 ET

Summary

- Rising interest rates and inflation are posing risks of stagflation, impacting even strong stocks like The Kraft Heinz Company.

- KHC is implementing strategic moves, such as entering the school lunch market, to boost organic net sales and profitability.

- With a strong balance sheet and commitment to maintaining dividends, KHC stock is attractively valued and poised for significant upside in the coming years.

Introduction

Interest rates are rising again. Inflation is turning out to be sticky, and the Fed isn't expected to lower rates anytime soon despite weakening economic growth.

Although we aren't there yet, the risks of stagflation are rising.

This is hurting even the strongest stocks on the market. The Kraft Heinz Company ( KHC ) is one of them.

On July 1, I wrote an article titled Kraft Heinz: 4.6% Yield And Undervalued .

Fast forward more than two months, and we're dealing with a 5% yield and a stock that seems to be even more undervalued.

Was I wrong?

If I were a trader, I would have been wrong.

However, as a long-term investor, I continue to believe in buying great companies at great prices - especially because the current macro environment isn't sparing anyone.

For example, even PepsiCo ( PEP ), The Hershey Company ( HSY ), and Procter & Gamble ( PG ) have started to suffer. I consider these three companies to be the gold standard of consumer staples.

The same is happening in other industries, as market participants are increasingly avoiding companies that will likely see limited pricing power going forward.

After almost three years of aggressive price growth, the consumer cannot take much more.

Although I do not expect consumer stocks to take off anytime soon (I'm bullish on energy and believe in sticky inflation), as a long-term investor, I am a big believer in buying high-quality companies at great prices.

The company behind the KHC ticker is one of them!

So, let's get to it!

KHC's Turnaround

This is not a great environment for consumer stocks - especially companies competing with generic brands and other major corporations.

Sticky inflation and slower economic growth are toxic for consumers.

Hence, headlines like the one below are starting to pop up:

{kind=link}

As reported by the Wall Street Journal , this fall, American students can expect to see a selection of Kraft Heinz's popular items, including pasta, hamburgers, and their iconic Lunchables, prepackaged meal kits.

For Kraft Heinz, the decision aligns with its effort to connect with a new generation of consumers and to somewhat reinvent its company.

Over recent years, many shoppers have been gravitating towards smaller, natural, and less processed brands.

However, the COVID-19 pandemic prompted a return to familiar, well-known products, leading Kraft Heinz to adapt its marketing strategy accordingly.

According to the article, Miguel Patricio, CEO of Kraft Heinz, and Carlos Abrams-Rivera, the company's incoming CEO, view schools as a critical channel for expanding their food service division.

They believe this move not only serves schools but also boosts supermarket sales. Kraft Heinz's Lunchables, already a billion-dollar business, seems well-suited to this expansion.

This brings me to the bigger picture. After all, moving into schools is just one of the company's ways to boost volumes in a challenging environment.

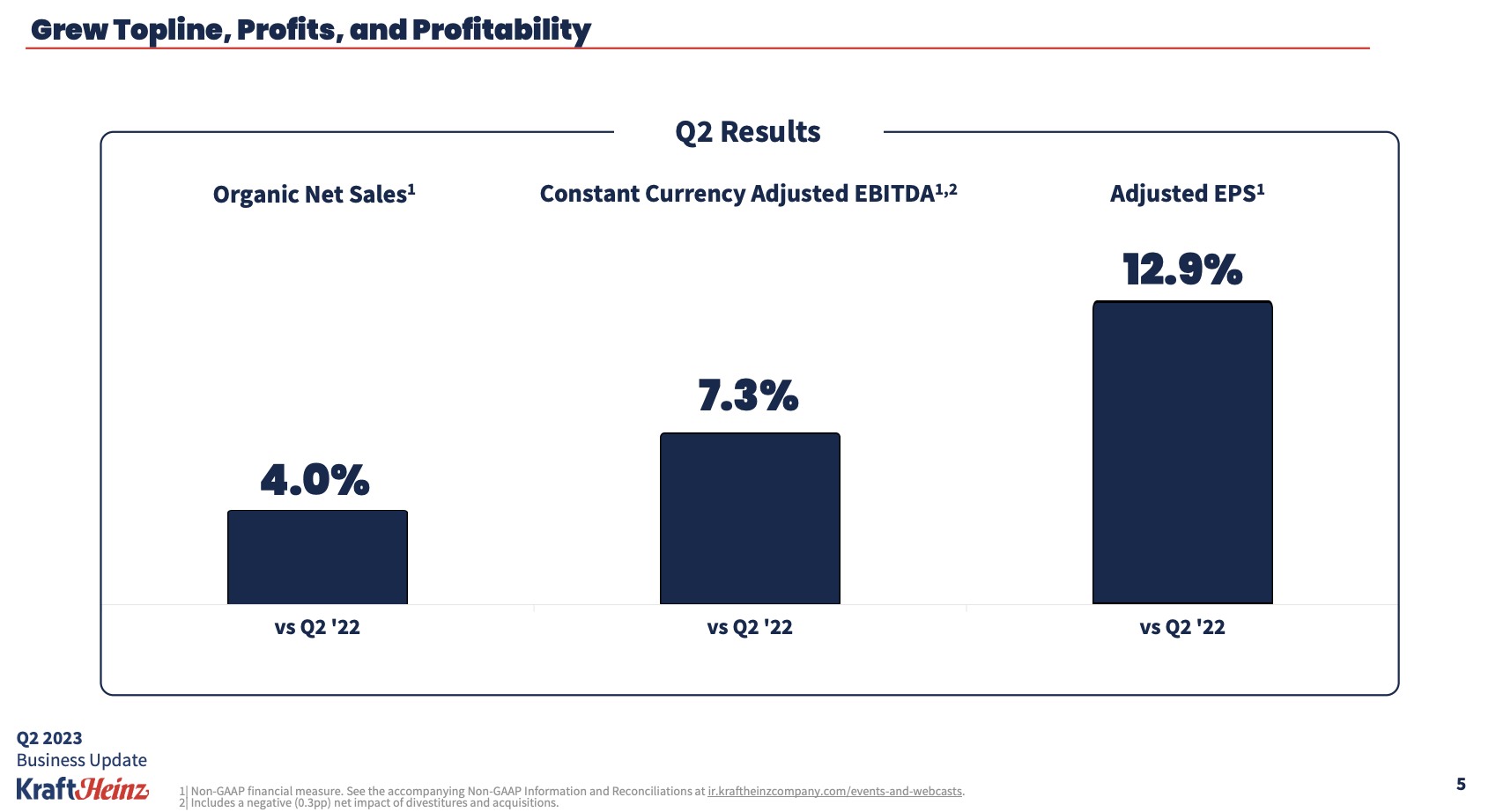

In the second quarter of 2023, the company reported a 4.0% increase in organic net sales globally, primarily driven by its three core pillars.

{kind=link}

In North America, organic net sales grew by 1.3%, thanks to effective price execution.

Meanwhile, International markets saw impressive growth at 13.2%, achieved through strategic pricing adjustments to counter inflation.

Adjusted EBITDA also showed a global increase of 6%, accompanied by an expansion in EBITDA margins across both regions.

The three pillars of growth can be seen below.

- The food service segment grew by roughly 15%, outpacing the industry in North America and internationally. This growth was attributed to strategies like investing in a chef-led model, targeting higher-margin channels, and introducing innovative products like HEINZ sauce taps.

- Emerging Markets witnessed 11% organic net sales growth despite temporary challenges in Brazil. The company expects growth to accelerate in Emerging Markets in the second half of the year.

- In the retail segment, organic net sales grew 1.3%, with a specific focus on GROW platforms like Taste Elevation and Easy Meals, which outperformed and contributed to growth.

{kind=link}

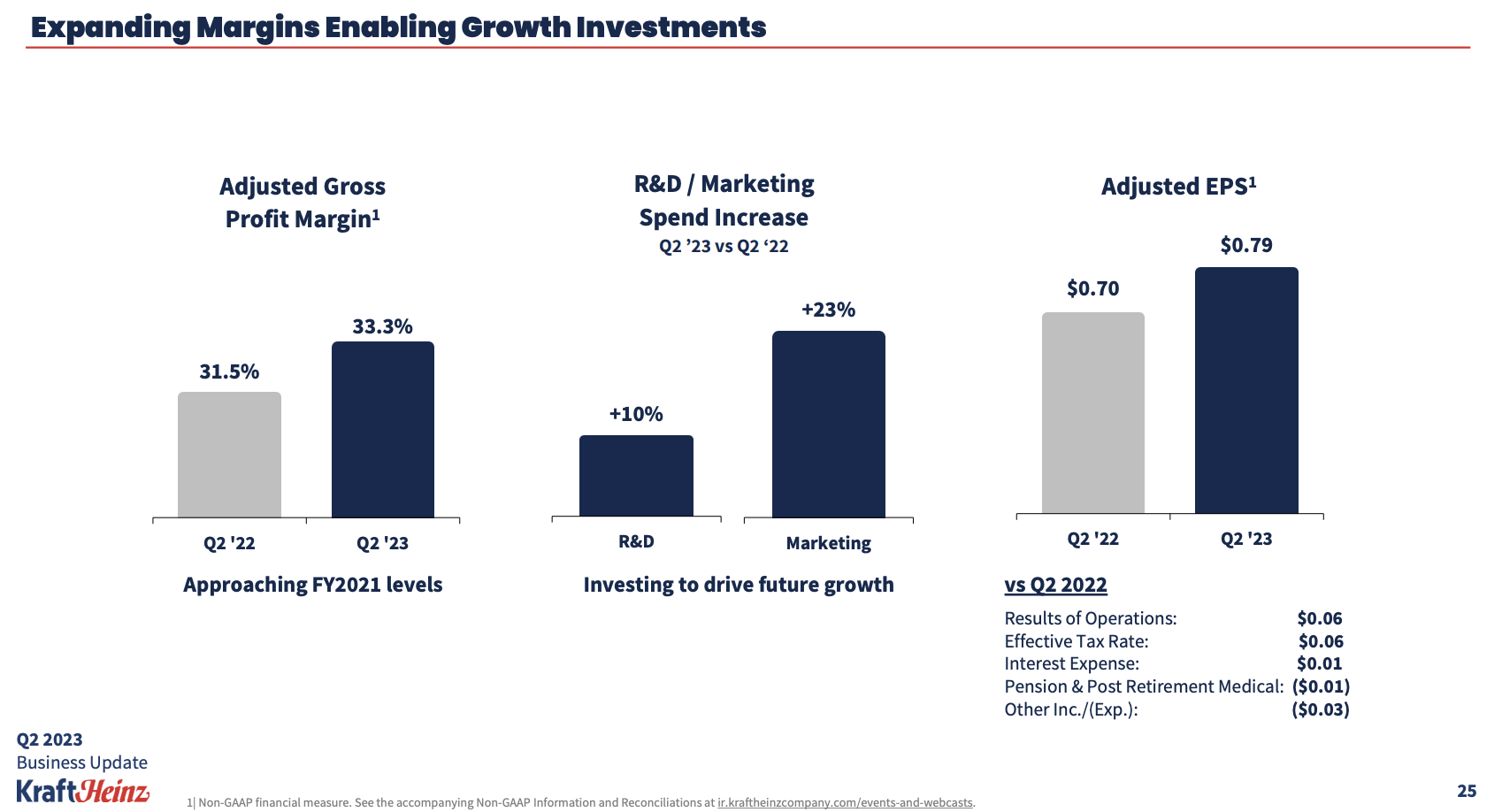

Kraft Heinz attributed its success to pricing strategies and operational efficiencies, resulting in a notable 180 basis point expansion in adjusted gross profit margins compared to the previous year.

This margin improvement allowed the company to invest heavily in marketing, research and development, and technology, with a 10% increase in R&D spending and a 23% boost in marketing investments.

Higher spending has led to product launches, such as NotCheese and plant-based Philly. They are expanding into new grocery store aisles and introducing innovative products globally.

Additionally, the company is investing in technology to accelerate growth and drive efficiencies, including the development of an automated distribution center set to open in 2025.

So far, these initiatives have contributed to a 12.9% growth in adjusted earnings per share, which was primarily driven by strong adjusted EBITDA performance.

{kind=link}

Having said that, the company observed that pricing gaps relative to both private label and branded competitors had expanded in the U.S.

Furthermore, Kraft Heinz maintained a disciplined approach to promotions, with only 29% of the volume sold on promotion compared to the industry average of 35%.

The return on investment for these promotions also improved significantly.

Elasticities in volume reverted to more normal levels, and the company expects volume declines to moderate for the rest of the year, driven by various factors, including market share gains and reacceleration in emerging markets.

In other words, despite an unfavorable environment, KHC is setting itself a bit apart with the outlook of slightly better volumes in the second half. That's not blockbusting news, but it's a great start!

Please note that the company lost some market share in the second quarter (50 basis points) in categories like cold cuts, cream cheese, and kids' single-serve beverages.

However, the aforementioned measures are expected to result in market share gains down the road.

Dividend & Valuation

We – for us to maintain the dividends that we have, which provided a very attractive yield is critical and I think we feel good about our rating now, the level of the grade we had in the past 16 months. - KHC 2Q23 Earnings Call

The quote above is the answer to the following question:

[...] I wanted to ask a follow-up about capital allocation priorities. Paying down debt is I think number three on that list, ahead of portfolio management. You highlighted that leverage is I guess more or less at your target. Does debt pay down thus move down a notch in importance, and I guess what I'm getting at is, is there a scenario in which you might, maybe start to buy back some stock again?

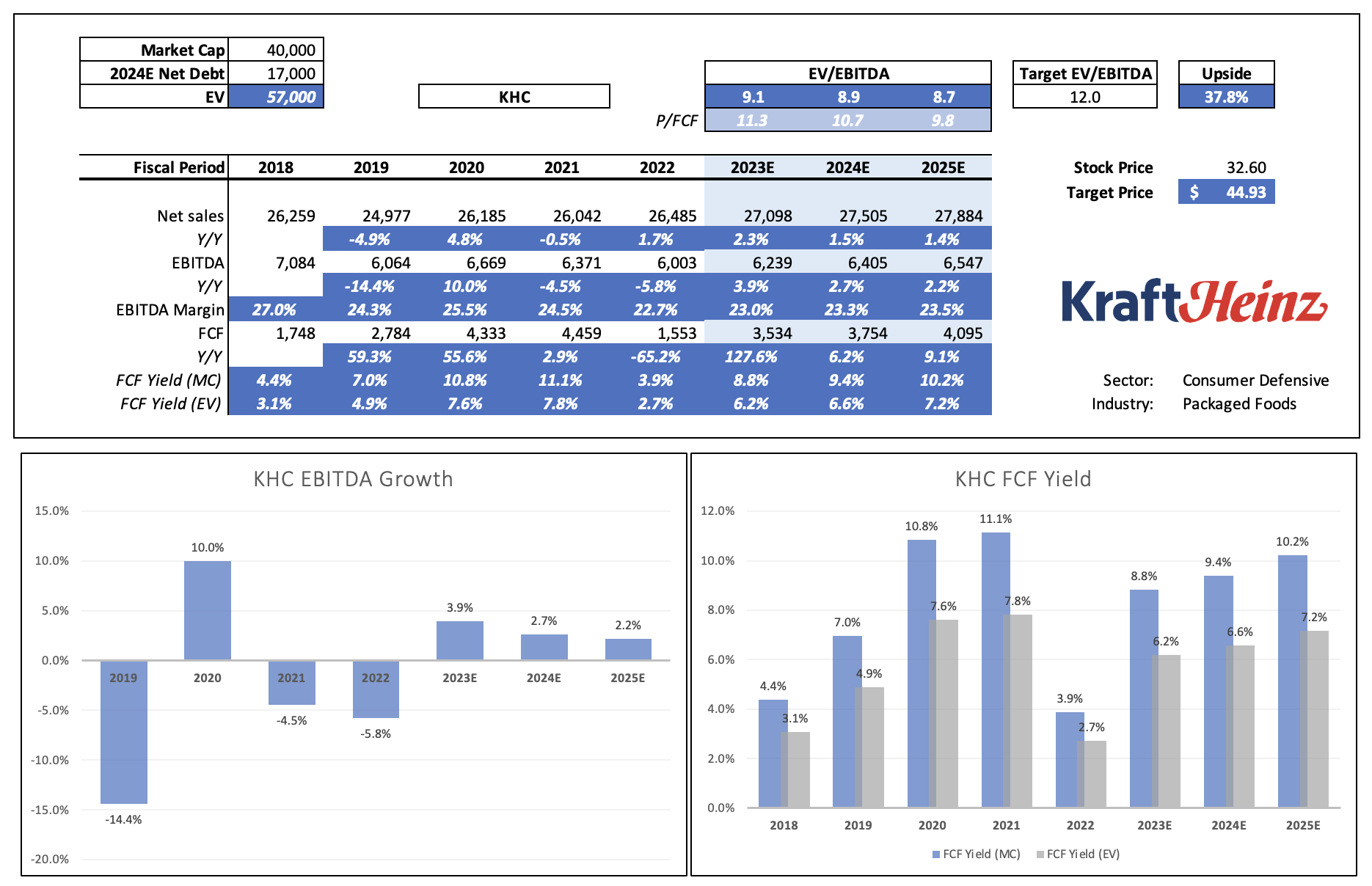

The company's balance sheet is looking increasingly strong. This year, the company is expected to lower its net debt to $18.3 billion, which would indicate a sub-3x leverage ratio.

KHC has a BBB credit rating and a path to a sub-2.4x leverage ratio by 2025.

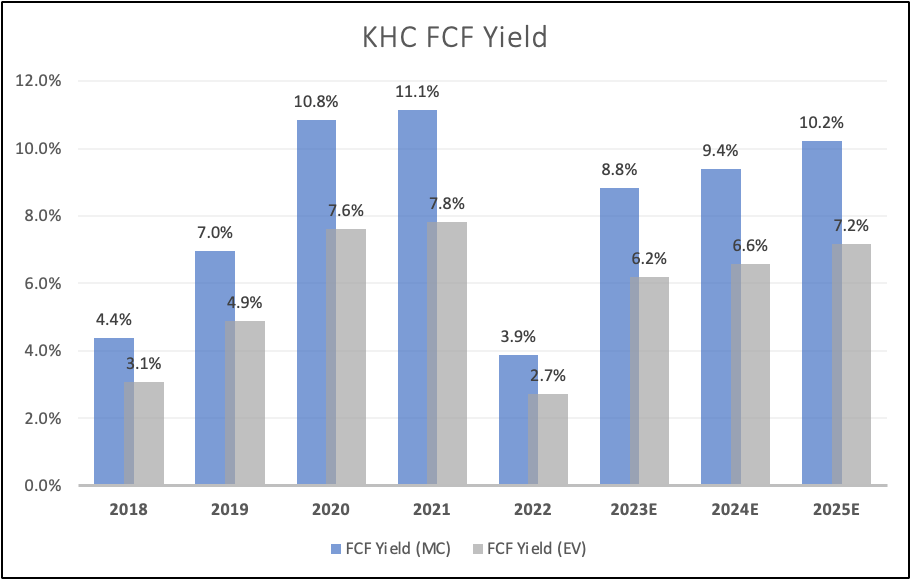

It is no surprise that debt reduction is expected to be quick, as the company is expected to generate a free cash flow yield of 10% in 2025, which not only helps the company to reduce debt and invest in new products and capabilities but also protects its 5% dividend.

Leo Nelissen (Based on analyst expectations)

{kind=link}

On top of that, KHC is attractively valued.

The company is expected to maintain slow (but steady) revenue growth with an improvement in EBITDA margins to 23.5% in 2025.

This could pave the road for high-single-digit EBITDA growth in the next few years.

Given the company's EBITDA growth capabilities and high free cash flow, I stick to what I said in my prior article: KHC deserves a 12x EBITDA multiple.

This would pave the road for roughly 35% to 40% upside over the next two years.

Leo Nelissen (Based on analyst expectations)

{kind=link}

The current consensus price target is $41. My price target is $45. On April 14, the company got a $44 target from Stifel, which gave the stock a Buy rating.

Although I do not believe that KHC - nor any of its peers - will take off anytime soon due to sticky inflation and elevated rates, I believe that KHC offers tremendous long-term value.

I stick to a Buy rating.

The only reason why I do not own KHC is because I prefer consumer staples with lower yields and more growth. That's due to my strategy. If I were an income-focused investor closer to retirement, I would be a KHC shareholder.

Takeaway

In today's challenging economic landscape, marked by rising interest rates and persistent inflation, even the strongest stocks like The Kraft Heinz Company face hurdles. While some might question my earlier assessment of KHC, I remain steadfast in my belief as a long-term investor.

KHC's strategic moves, including entering the school lunch market and focusing on high-margin channels, are paying off with impressive growth in organic net sales and improved profitability. Despite market share setbacks in certain categories, the company's disciplined approach to promotions and promising volume outlook for the second half of the year are encouraging signs.

With a robust balance sheet and a commitment to maintaining dividends, KHC is on a path to financial strength and value creation. It's attractively valued and poised for significant upside in the coming years, offering an appealing long-term investment opportunity.

For further details see:

Kraft Heinz: 5% Yield And Up To 40% Undervalued