KHC - Kraft Heinz: A Buy For Dividend Investors

2023-05-31 13:02:08 ET

Summary

- Kraft Heinz has shown positive financial trends in recent quarters due to management's strategic initiatives, indicating a potential turnaround point.

- The stock offers an attractive dividend yield and substantial upside potential, with a fair stock value estimated at 21% higher than current levels.

- Risks to consider include changing consumer preferences, concentration risk, and vulnerability to input cost volatility.

Investment thesis

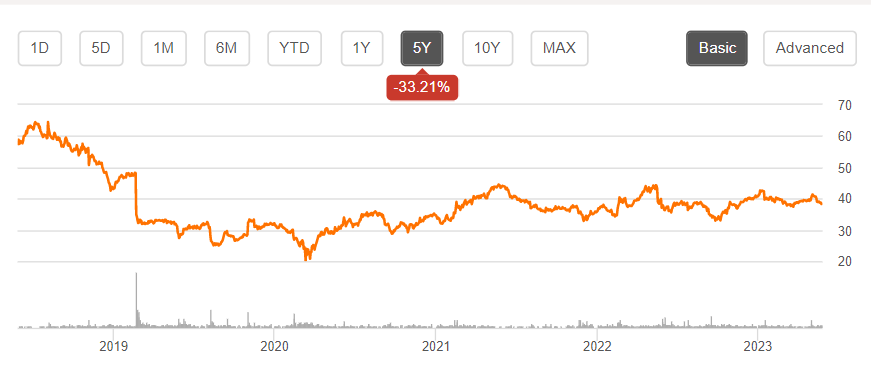

Kraft Heinz ( KHC ) has been struggling to improve its financial performance for many years. Given the stagnating revenue together with shrinking profitability metrics, there is no surprise that the stock has been underperforming over multiple years.

{kind=link}

But, I see very positive trends in the company's financial performance over a few recent quarters, which was thanks to the management's strategic initiatives. The management is focused on improving profitability, though the company currently navigates a challenging macro environment where it is difficult to control costs. Both near and long-term outlooks are positive, with steady topline growth together with EPS expansion. The stock offers an attractive dividend yield together with substantial upside potential. Considering all these favorable factors, I believe the potential benefits outweigh the risks, and the stock is a buy.

Company information

Kraft Heinz is one of the world's largest food and beverage companies, with many well-known brands in its portfolio. The company was formed by merging Kraft Foods and H.J. Heinz in 2015.

{kind=link}

The company disaggregates its revenues by geographic areas, where North America represented about 77% in FY 2022. Sales by product category are presented in the below table.

Compiled by the author based on the company's latest 10-K report

Financials

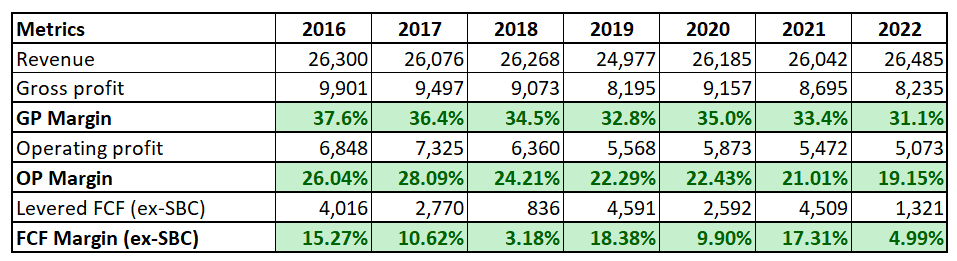

I analyzed the company's financial performance over the last 7 years between FY 2016 and 2022 since the merger occurred in 2015, and the years before the combination would not be representative.

{kind=link}

KHC's revenue stagnated over the past seven years, with margins deteriorating significantly. The company's massive free cash flow [FCF] margin shrank from an impressive 15% to a mere 5%. The company has a substantial amount of debt on its balance sheet, though the interest coverage ratio looks resilient.

Seeking Alpha

I also want to underline that the management has done well in decreasing leverage over the past two years, with net debt moving from $28 billion in 2016 to slightly below $20 billion in 2022. According to the latest quarterly financials , the net debt position continued to demonstrate improvement, which is a good sign for potential investors.

Compiled by the author

In February 2023 , the management outlined its "Transformation Momentum" where long-term financial goals were shared. Apart from expectations of organic net sales to compound at about 3% annually, key profitability metrics are expected to demonstrate sustainable growth within the 4-8% range and free cash flow conversion to 100%. The company has an ambitious goal to reach a gross efficiency target of $2.5 billion.

{kind=link}

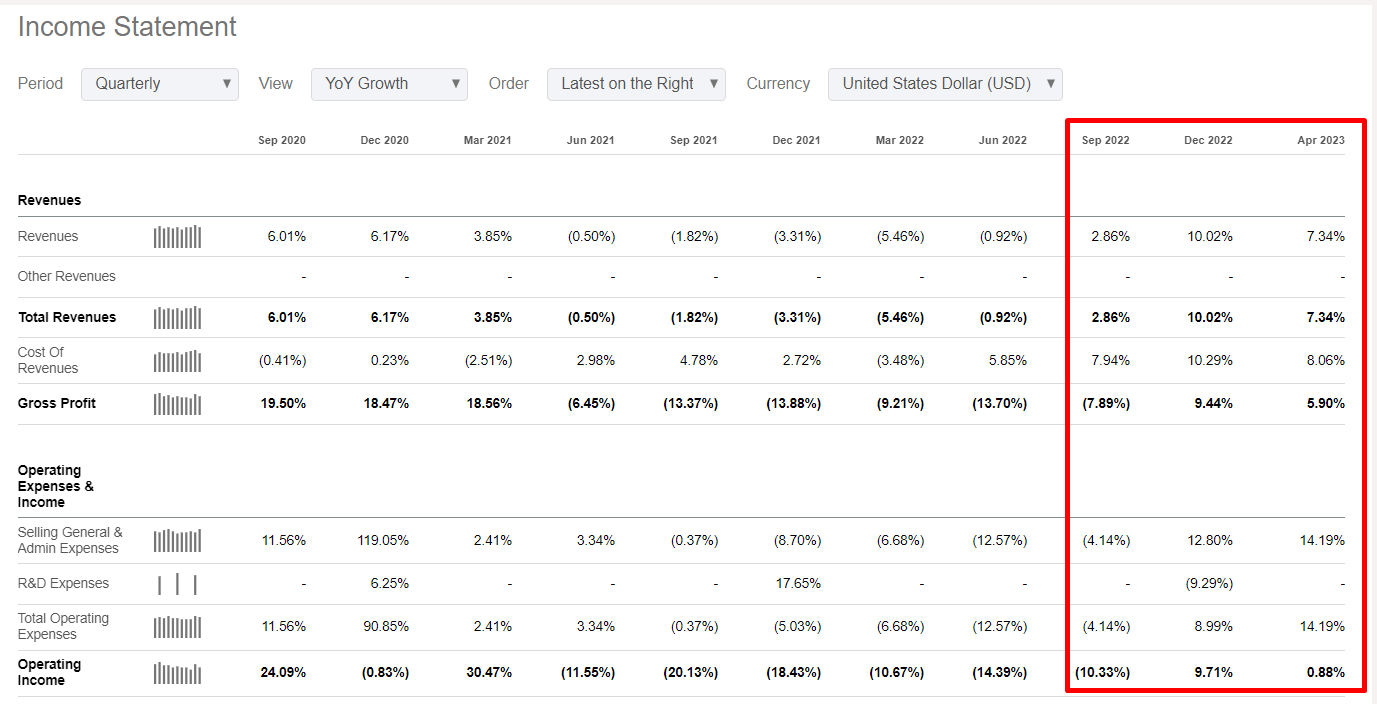

If we look at the last few quarters we can see that the company demonstrated YoY growth in three consecutive quarters which is a good sign, especially in the current challenging environment. Though, the cost of revenues together with operating expenses grew faster than the topline, meaning shrinking profitability metrics. Therefore, there is still plenty of room for management to improve profitability.

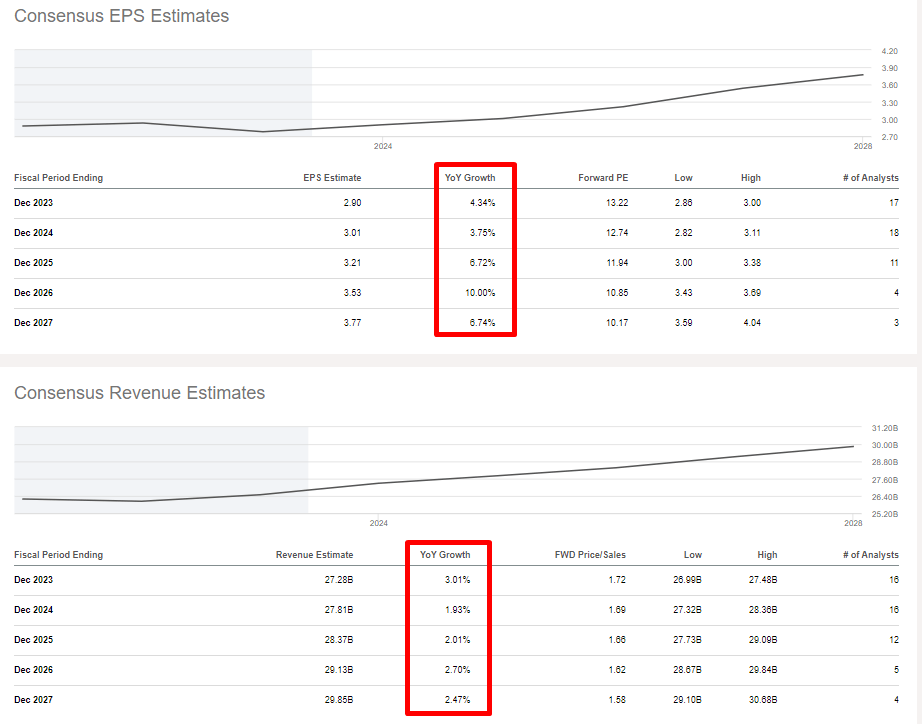

The upcoming quarter's topline is also expected to expand on a YoY basis by about 5%, and EPS to expand 5 cents per share. I think that it is a positive sign, and the management is likely to succeed in its transformation. Long-term consensus estimates are also optimistic about the company's future, with revenue compounding at about 2-3% range and EPS expanding each year.

{kind=link}

Overall, I believe that Kraft Heinz experienced hard times over multiple years, but I see that we are at a turnaround point where recent quarters' financial performance demonstrates signs that management's initiatives are likely to have a positive impact.

Valuation

KHC pays dividends to shareholders, so the dividend discount model [DDM] valuation approach is suitable. I prefer to be conservative when I select underlying assumptions. Therefore, I round up to 6.5% WACC provided by valueinvesting.io. I have consensus estimates for the current dividend, consensus estimates projecting $1.63 per share in FY 2024. The company has struggled to increase dividends over the past years, but as we have seen in the "Financials" section, management is working on improving profitability. So, I use a very modest 3% dividend growth assumption for my valuation analysis.

Author's calculations

The DDM returns me a fair stock value of about $47, or 21% higher than the current stock price levels. The upside potential looks attractive, especially given the 4.2% forward dividend yield.

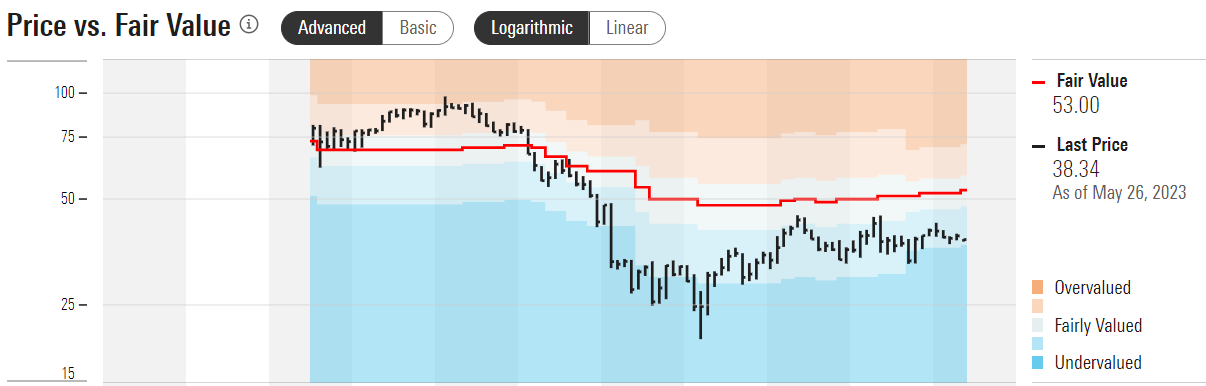

To get more conviction, let me also refer to Morningstar Premium, estimating the stock's fair value at $53 with a medium level of uncertainty. The chart below shows that the stock price has historically traded with a substantial discount to Morningstar's fair value estimation.

{kind=link}

Risks to consider

Investing in Kraft Heinz stock carries risks, mainly due to changing consumer preferences. While Kraft Heinz owns well-known and popular brands worldwide, the concern lies in changing consumer tastes. There is a secular shift where consumers are shifting from packaged foods and increasingly prefer natural and organic meals and condiments. Therefore, I consider relevance risk to be high for KHC.

Another notable risk is the concentration risk. KHC faces a high concentration of sales to its largest customers, with Walmart alone accounting for 21% of total sales in 2022. In addition, the fact that the top five customers in the U.S. account for nearly half of U.S. sales and the top five customers in Canada account for 76% of Canadian sales indicates a significant business concentration. Such a high level of sales concentration increases the company's dependence on its major customers' financial stability and strategic decisions.

Last but not least, the company is vulnerable to the volatility of input costs, especially related to commodities like agricultural products and energy. KHC has almost no power to control commodities prices, so unfavorable movements in raw materials prices can adversely affect the company's profitability. Management has to be proactive in hedging risks related to raw materials volatility.

Bottom line

Overall, I believe that the upside potential and an attractive forward dividend yield outweigh the risks. I like the dynamics of the last three quarters, which indicate a positive trend given the management's strategic initiatives. The stock is a buy for investors who seek a reliable dividend company to add to their portfolios.

For further details see:

Kraft Heinz: A Buy For Dividend Investors