KHC - Kraft Heinz: A Compelling Buy For Dividend Investors

2023-10-10 08:05:00 ET

Summary

- Dollar cost averaging is an effective technique for growing wealth and income over time, especially when applied to value stocks with high dividend yields.

- Kraft Heinz presents a strong buying opportunity for income value investors while it's trading near its 52-week low with a 5% yield.

- Its turnaround and brand renovation efforts are underway, and it maintains pricing power while exploring new innovative areas.

Dollar cost averaging (or DCA) is an effective technique for growing wealth and income over time, especially when it's applied to value stocks that pay high dividend yields. Whether investors use disposable income from wages, rental income, or stock dividends, now is one of the best times in 2023 to hunt for dividend bargains.

This brings me to Kraft Heinz (KHC), which I last covered here in early July with a 'Buy' rating, noting its strong sales and margin performance. The stock hasn't been one of my best performers, with the price falling by 9.8% since then, but that's not necessarily a bad thing for long-term value investors who prize the ability to DCA into quality dividend payers on low prices.

As shown below, KHC is now trading just slightly above its 52-week low and in this article, I discuss why it presents a good 'Buy' for income value investors, so let's get started!

{kind=link}

Why KHC?

Kraft Heinz is a $27 billion (in annual sales) company that manufactures some of the most recognizable food names in the industry, and operates in 190 countries with 200 brands. Those familiar with the company may know that KHC has seen its ups and downs in terms of price action in recent years.

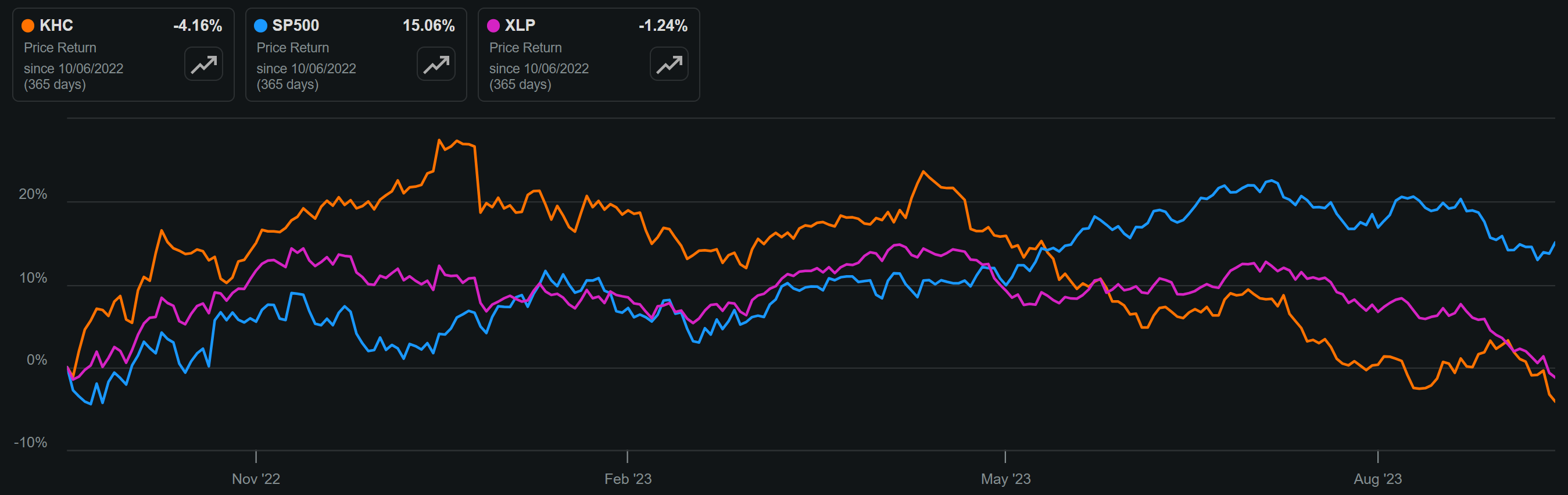

As shown below, KHC has underperformed both that of the S&P 500 ( SPY ) and the SPDR Select Consumer Staples ETF ( XLP ) over the past 12 months, with a 4% decline compared to the 1% decline of the latter.

KHC 1-Year Price Return (Seeking Alpha)

{kind=link}

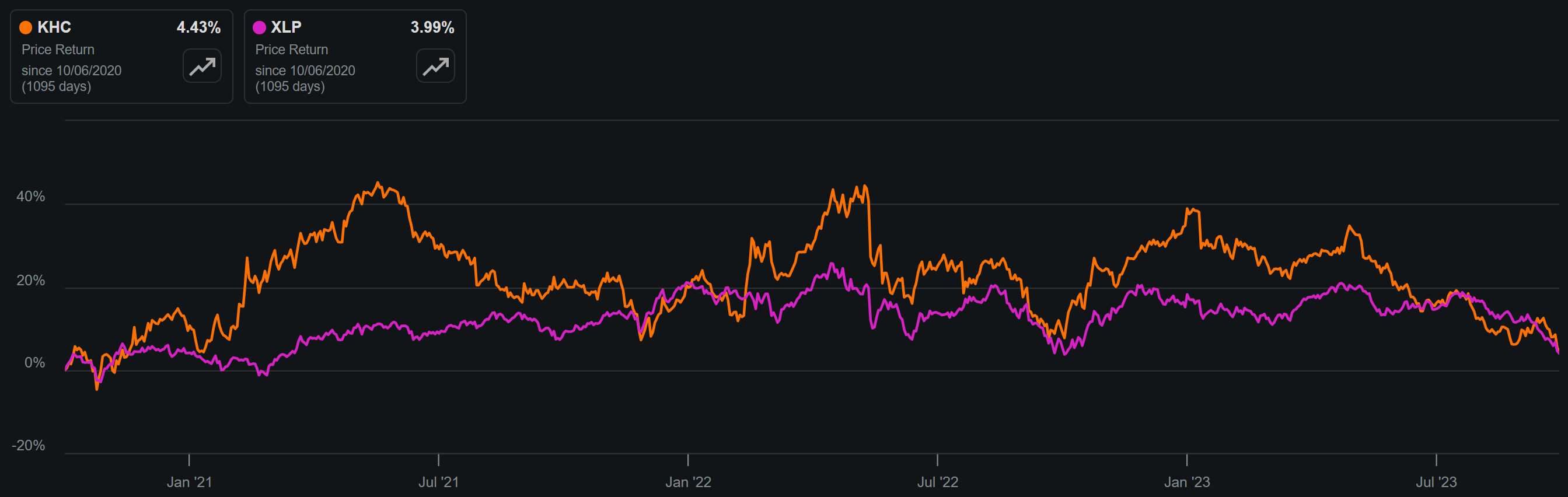

However, when looking at the past 3 year period, KHC's performance hasn't been all that bad compared to XLP, with a 4.4% price return compared to the 4% of XLP.

KHC 3-Year Price Return (Seeking Alpha)

{kind=link}

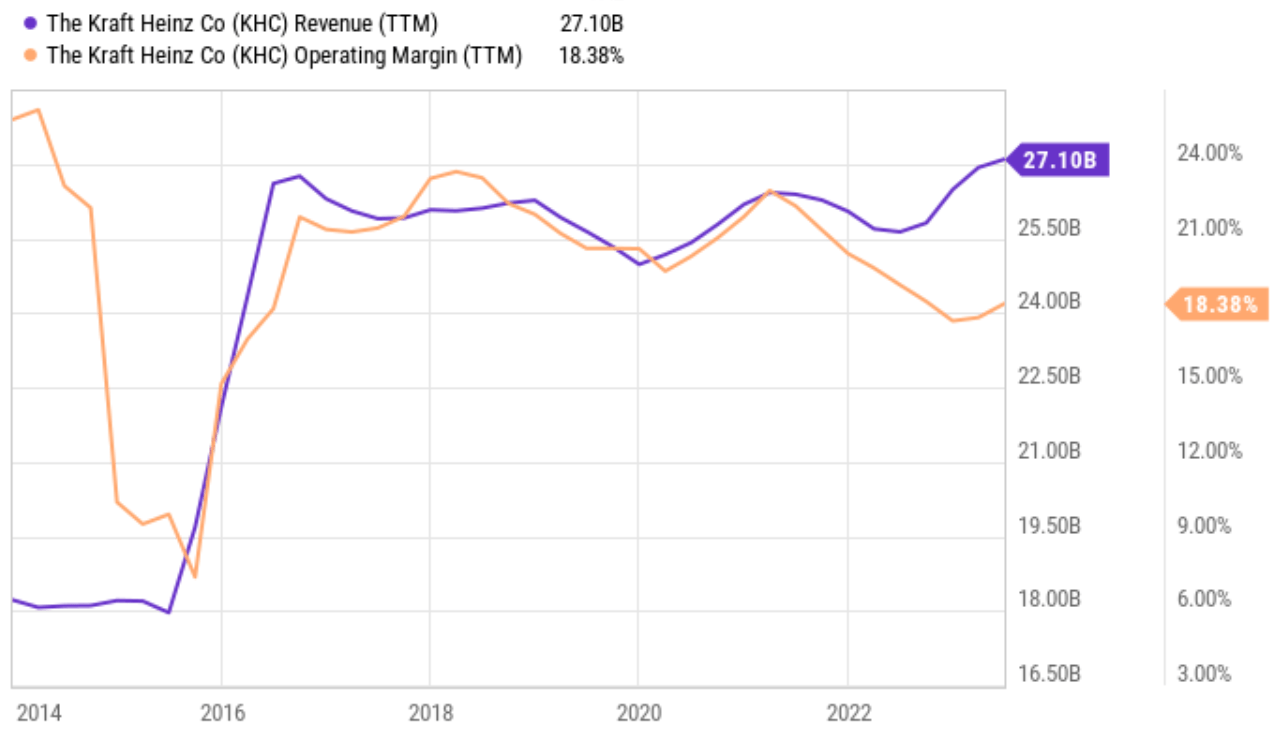

While KHC has seen material share price weakness over the past year, its top and bottom-line performance belies the amount of negativity the market has baked into the stock. This is reflected by KHC's trailing 12 month revenue now sitting at its highest point since 2016. Moreover, it appears that the margin hit from supply chain disruptions and wage inflation is starting to moderate with TTM operating margin showing signs of a recovery, as shown below.

{kind=link}

This is not to say that KHC hasn't seen near-term headwinds, as consumers remain pressured under higher than normal inflation. Plus, concerns around the resumptions of student loan repayments weigh on consumers' ability to purchase "premium" consumer goods compared to cheaper store-branded options. These concerns are reflected by KHC's volume declines in both domestically and internationally, with a combined 7% YoY in product volume in the last reported quarter.

However, KHC carries some degree of pricing power, as it was able to raise prices by 11% YoY during the last reported quarter. This helped to offset volume declines, resulting in organic net sales rising by 4% and supply chain improvements resulted in gross profit improving by 12% YoY.

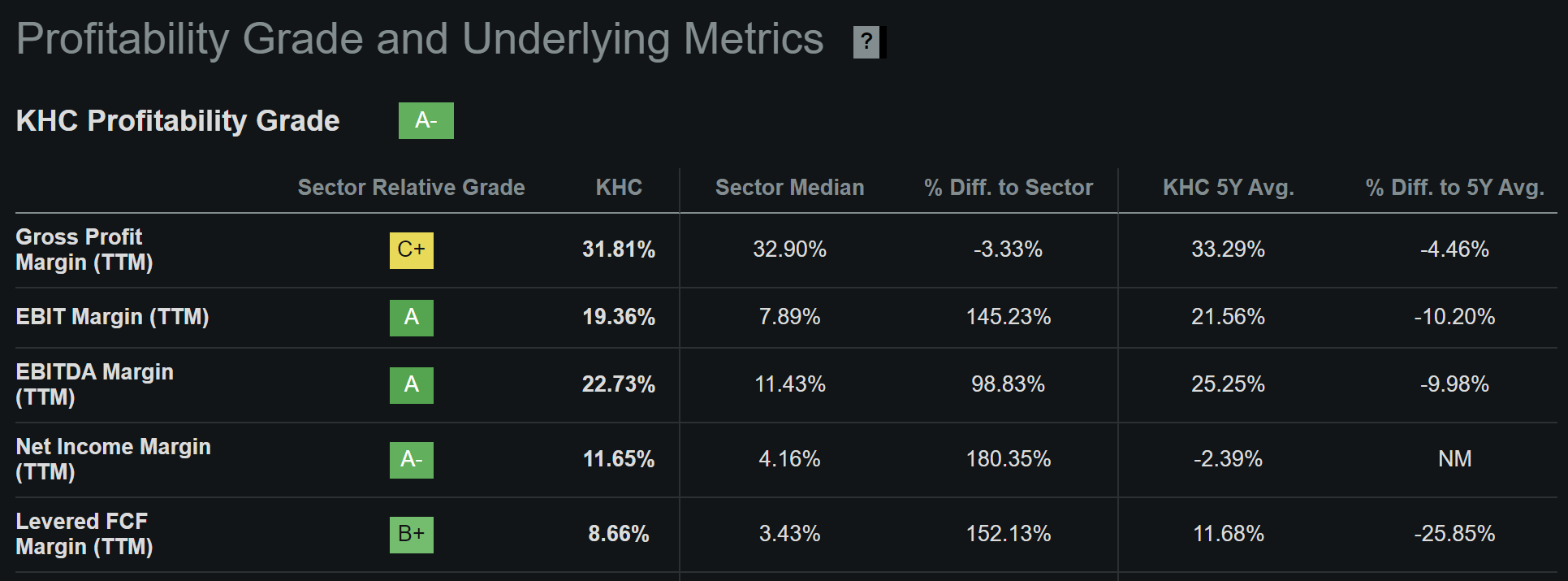

This provides support that management's turnaround strategy is working, with focus on technology, efficiency, and brand renovation that's already been completed across 90% of the portfolio over the past 3 years. This includes $2.5 billion in anticipated cost savings between 2022 and 2027, including $450 million in savings realized last year, up from the original $2 billion estimate. This could help to further strengthen KHC's margin profile, which already earns an 'A-' grade for profitability, with well-above average EBITDA and Net Income margins of 22.7% and 11.7%, respectively, as shown below.

{kind=link}

Risks around KHC's strategy include higher than expected inflation and potential for a hard landing in the economy due to aggressive rate hikes. This could further put a strain on the consumer, as Evercore ISI recently noted that rising price elasticity of demand is likely to remain an overhang for the Food industry.

Nonetheless, KHC sees core strengths as noted during an industry conference last month, and expects the Lunchables and its namesake Ketchup business to improve between now and the end of the year. To maintain its leadership position in key categories, KHC has invested 23% more in marketing and 10% more in R&D on its brands. It's also keeping up with evolving consumer tastes by getting in plant-based foods, as noted during the same conference:

We see joint partnerships being a truly acceleration for us at Kraft Heinz. And we have done that in places like our joint venture with NotCo. It allows us to get into plant-based and leverage our North America brands. There would be opportunity for us to think about partnerships more globally in our company as well as we go forward. But again, things that are true for us that we potentially can accelerate.

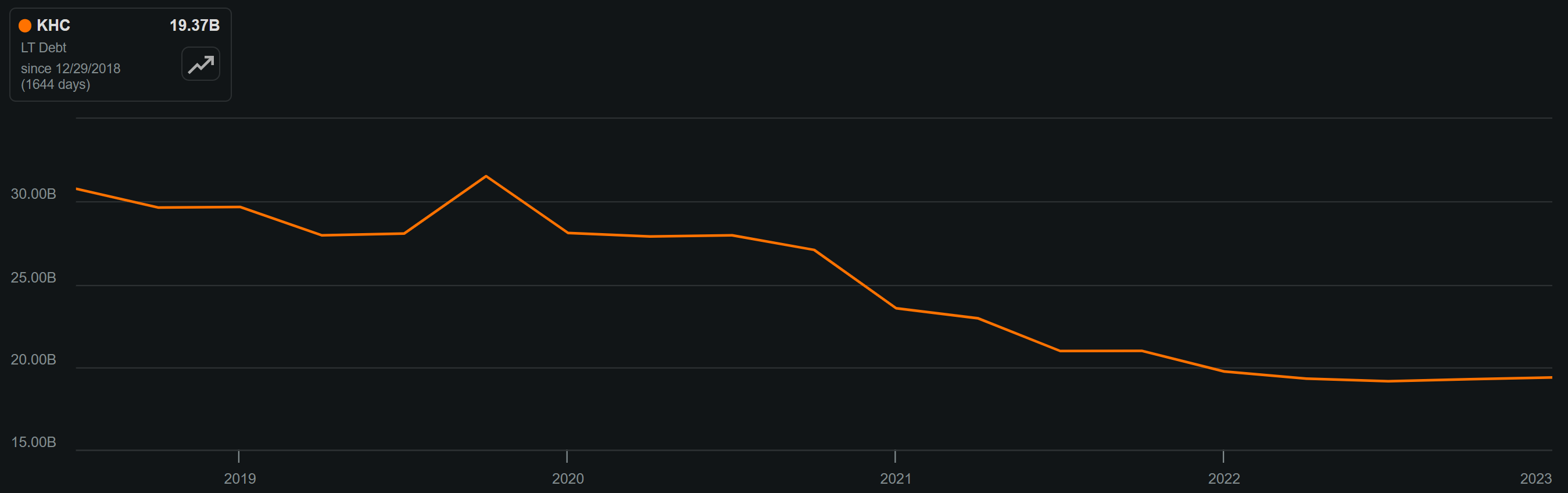

Importantly, KHC has meaningfully deleveraged its balance sheet in recent years. This includes reducing long-term debt by $1.6 billion since the end of 2021, and this is on top of the $7 billion LT debt reduction between 2020 and 2021. KHC carries a BBB investment grade credit rating and while its net debt to EBITDA ratio of 3.1x is slightly high, I would expect for it to continue to trend down below 3x as deleveraging continues. At present, As shown below, this follows a long-term debt reduction trend since 2018.

{kind=link}

Meanwhile, KHC currently yields an appealing 5.0%, which is high for the consumer staples segment outside of tobacco companies. The dividend is well-protected by a 54% payout ratio. While dividend growth has been lacking since the dividend was cut in 2019, I believe deleveraging the balance sheet takes precedence in this higher interest rate environment.

Lastly, KHC appears to solidly be in value range at the current price of $32 with a forward PE of just 11.1, sitting well under its normal PE of 16.5 since 2015. Analysts expect between 2.6% and 10.9% annual EPS growth over the next 3 years.

I come up with a fair value of $40.27 based on the NPV analysis below. This utilizes the $2.90 estimated EPS for this year, a reasonable 5% long-term EPS growth rate, and 2.5% discount rate (slightly higher than the 2% targeted rate by the Federal reserve), equating to a potential 26% upside based on share price appreciation alone.

NPV Analysis (Produced By Author)

{kind=link}

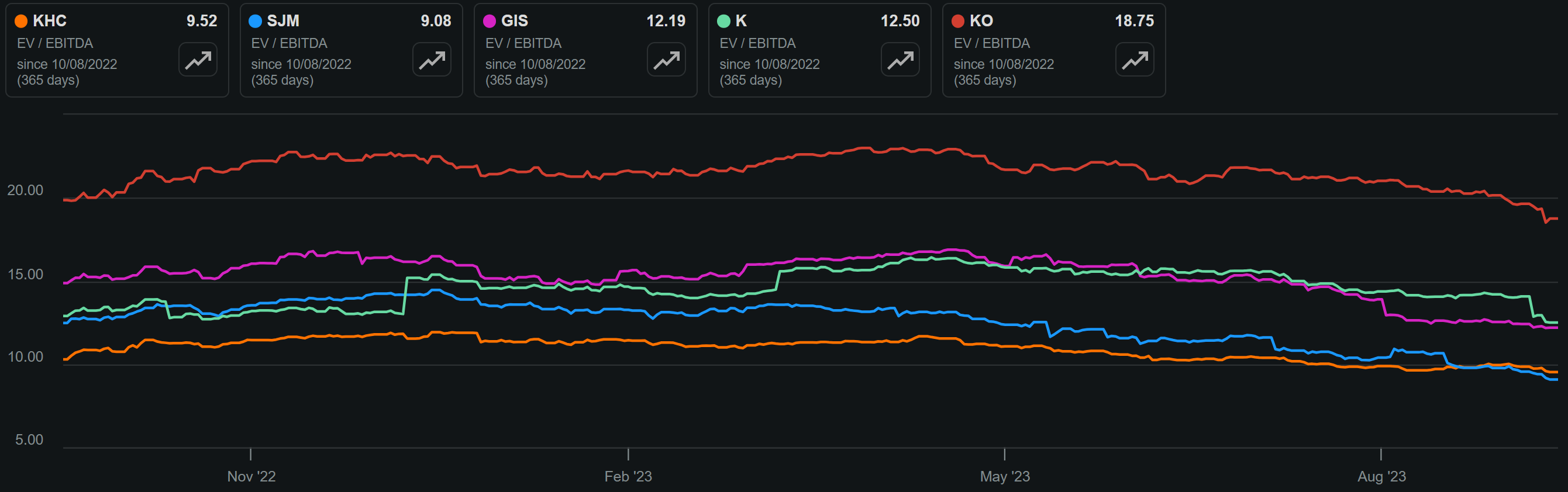

KHC also trades at a substantial discount to its consumer staples peers. With the exception of J.M. Smucker ( SJM ), which is slightly cheaper from an EV/EBITDA perspective, General Mills ( GIS ), Kellanova ( K ), and just for kicks, Coca-Cola ( KO ), all carry significantly higher valuations than KHC's 9.5 EV/EBITDA.

KHC & Peers EV/EBITDA (Seeking Alpha)

{kind=link}

Investor Takeaway

Despite near-term headwinds from inflation and student loan repayments affecting consumer spending, KHC has managed to maintain pricing power while implementing cost-saving measures. Plus, its turnaround efforts, including cost efficiencies and brand renovations are well-underway. With an improving balance sheet and attractive valuation with high yield, along with potential for dividend growth in the future, KHC could make for a compelling investment opportunity in the consumer staples at the current price. Given KHC's undervaluation, I'm upgrading the stock to a 'Strong Buy'.

For further details see:

Kraft Heinz: A Compelling Buy For Dividend Investors