MKC - Kraft Heinz: A Reluctant Buy For Its Attractive Valuation

2023-06-30 19:05:05 ET

Summary

- The Kraft Heinz Company is a successful, U.S.-based food brand with a broad product portfolio.

- Financial performance has been underwhelming over the past few years, causing Kraft Heinz stock to underperform.

- Recent financial results bring a note of optimism to investors.

- Valuation multiples indicate a sufficient discount for value-oriented investors to consider.

Thesis

The Kraft Heinz Company ( KHC ) is one of the market leaders in the food industry in the United States. The company markets a wide range of popular brands including Kraft, Heinz, Oscar Mayer Philadelphia, Jell-O, and many others. Despite facing strong competition inside the food industry, the company has remained familiar with consumers across the United States while it also attempts to expand its international footing.

Over the past few years, however, KHC has seen its stock price decline (-43% since 2018) due to below-average financial performance.

In this analysis, I attempt a mapping of the U.S. and international food industry, to the degree that it affects KHC, while also examining the company's financials, prospects and valuation.

A Growing, Challenging Food Industry

While Kraft Heinz aims to increase its international presence, the U.S food market is currently, by far, its largest and most significant market.

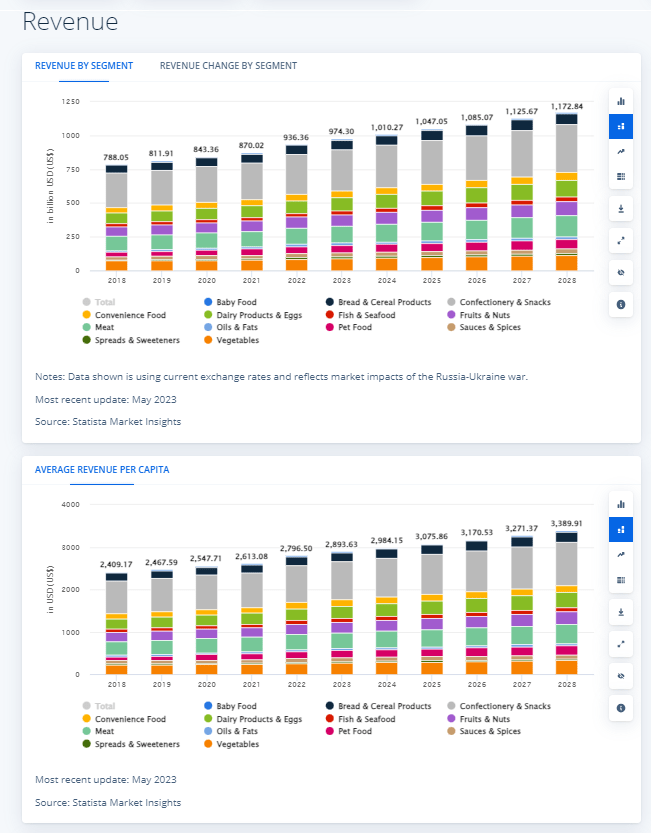

Total revenue in the U.S. food market today is estimated at around $975B, while the food industry is expected to grow at a moderate 3.78% CAGR through 2028. The market's largest segment remains Confectionery & Snacks with a market volume of around $30B in 2023. Average revenue per capita also shows moderate, yet steady increases YoY since 2018 and is also expected to keep growing through 2028.

{kind=link}

Food industry sales are included in those least disrupted by online purchases. In 2023, just 5.2% of total revenue materialized online. Consumers are likely to continue in-person grocery shopping for the foreseeable future and digitalization efforts regarding sales channels should probably be treated as a less pressing priority for manufacturers and distributors.

In global terms, the most revenue in the food industry is generated in China (approximately $1.50B in 2023). The growth in developing markets, especially in the Asia-Pacific region is also more promising and highlights the need for U.S.-based companies, aspiring to grow, to expand their international operations.

A trend that seems to be gaining ground in the food industry concerns the popularity increase of organic food and snack alternatives. Organic foods' market share has increased from 4.9% in 2014 to 7.2% in 2022, and is expected to reach 7.7% in 2027. More traditional brands like KHC are challenged to incorporate more organic solutions into their brand portfolio in order to retain market share.

Sales Characters & Breakdown

Food & Beverage products have naturally inelastic demand and manufacturers tend to pull through rather unscathed during recessionary times in the markets. While some seasonality is inherent to the business, both in the raw materials/production end and the consumer sales end (higher sales during holidays etc.), consumer defensive products tend to have relatively stable and moderate seasonality trends, unlike more discretionary segments of the consumer goods market.

Kraft Heinz offers a diverse product mix that covers many segments of the food industry. This is evident after looking into a segment breakdown of KHC's revenue. Five distinct product categories individually account for over 10% of sales, with Condiments & Sauces leading and Cheese & Dairy products occupying the second place. Both segments are expected to see moderate growth in the mid-term as explained in the previous segment of the analysis

{kind=link}

In terms of geographic positioning, for the fiscal year 2022, approximately 76% of sales came from North America, indicating that the company's international expansion can be a key growth driver for the future, yet also that management has underperformed in this aspiration are so far. The need for accelerated global expansion also derives from the fact that the majority of the company's manufacturing facilities reside overseas. Consequently, it can also be more cost-effective to service foreign markets with larger product volumes from a logistics viewpoint. Provided that the majority of revenue and growth in the food market is currently generated in the Asia-Pacific region, KHC seems to be slow to exploit on a major opportunity.

Revenue Growth Record & Profitability

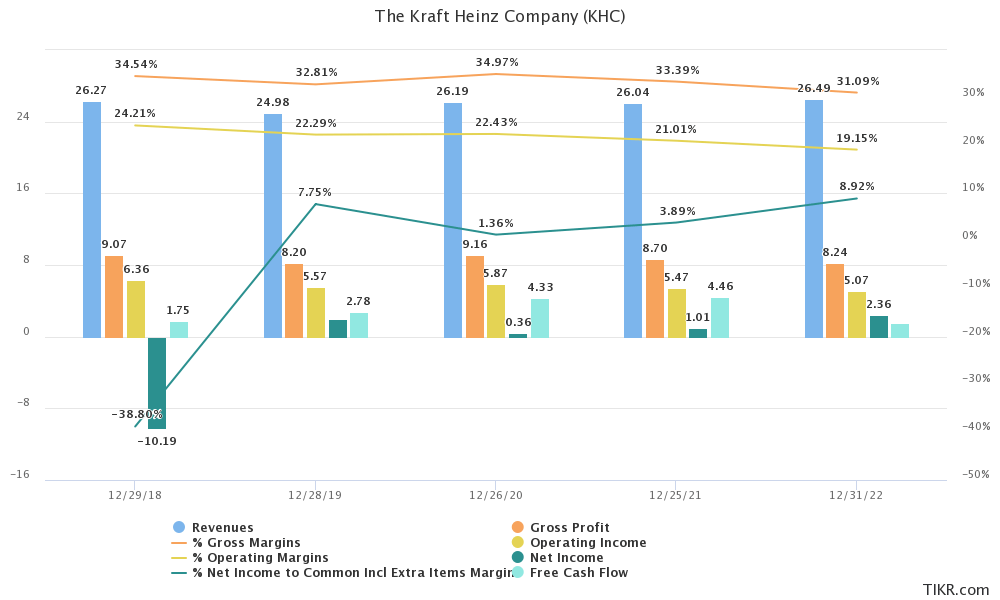

Revenue growth has been at a stalemate over the past 5 years, with sales increasing at a CAGR of just 0.66%. Operating income has actually decreased over the same time period. Both gross and operating margins have remained rather stable at 30-35% and 19-25% respectively, yet recording declines over the past couple of years. Free Cash Flow productivity has seen elevated volatility.

{kind=link}

Recent Uptick in Optimism

For the first quarter of 2023, Kraft Heinz managed to beat on revenue by $100M and EPS by $0.08 (both showing respectable short-term growth), raising analysts' optimism around the company and causing shares to trade higher. Even though volume decreased by 5.3% for the quarter, price increases of 14.7% managed to offset. Solid international growth was a welcomed positive sign for the business

Margins are expected to stabilize going forward, and even improve further, as input cost inflation is beginning to come down and supply chain inefficiencies to slowly fade. In the efficiency-improving topic, the company is also engaging in working capital improvement actions, expecting to increase inventory turnover by leveraging digital solutions, more accurately forecasting demand and cutting costs across the board.

Management has also issued more optimistic guidance regarding the 2023 fiscal year. KHC looks for 4-6% growth in organic sales and EBITDA, while EPS is forecasted to increase by 2-5%.

Financial Performance Metrics

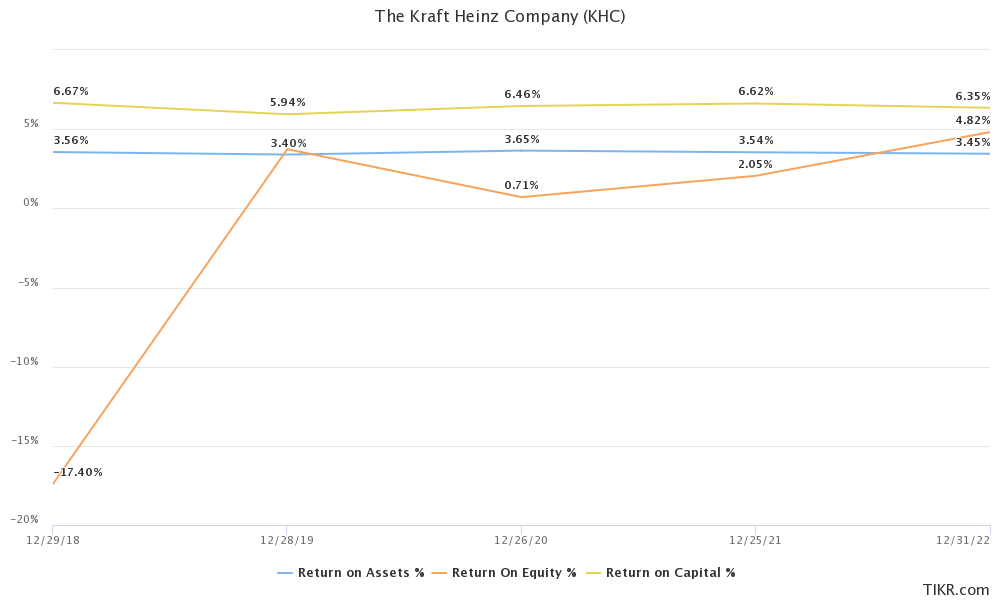

By most financial performance metrics, KHC seems to score below average, compared to peers and industry averages. Return on assets has remained below 4% for the trailing 5 years, indicating a slight inability to effectively utilize resources to generate sales. The same holds true for return on equity. Return on total capital is somewhat higher, hovering around 6-7% since 2018.

The company's net debt is also quite high, at $19.3B (or almost 50% of market capitalization), hurting bottom line profitability and hampering growth opportunities.

{kind=link}

Analysts' Expectations Going Forward

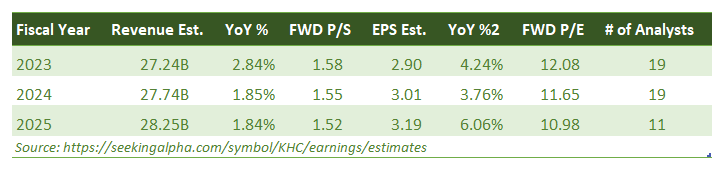

Over the next few years, despite some recent upticks in optimism, analysts expect moderate to slow growth both on the revenue and EPS front. Sales are expected to increase at a 1.5% - 3.0% annualized pace, while EPS are forecasted to grow at a 4.0% - 6.0% annualized rate. For the 2025 fiscal year, analysts foresee $28.25B in sales and $3.19 in EPS. These projected growth figures lie close to the food industry's expected growth, yet lower than the consumer staple's sector growth.

{kind=link}

Valuation

While Kraft Heinz lacks most of its peers in terms of financial performance, the company appears to offer a rather attractive valuation case. KHC trades at a 12.2x forward P/E, a 1.6x forward P/S, and a 10.0x EV/EBITDA multiple. By all three metrics, the company is undervalued compared to three of its most significant competitors: McCormick & Co ( MKC ), General Mills ( GIS ), and PepsiCo ( PEP ). However, it is important to note that KHC has been trading at a discount to these companies for the past few years, and even though the valuation gap has somewhat increased as of recently, it cannot be asserted with certainty that KHC is, in fact, cheaply valued. In my view, nonetheless, these metrics show that some upside potential can be exploited at the current valuation of the stock.

For more valuation-related reference, the average P/E, P/S, and EV/EBITDA multiples across the consumer staples sector currently stand at 20.2x, 1.05x, and 15.3x respectively.

Concerning the valuation outlook of the stock, we should also note that Bank of America has set a $48 share price (compared to the current $35.37), arguing that a valuation multiple expansion is bound to happen as KHC improved performance in Q1 2023. The valuation discount for The Kraft Heinz Company, according to most analysts, does exist and as such it can be exploited by value-focused investors. At this moment in time, I would offer KHC a reluctant buy rating.

Final Thoughts

The Kraft Heinz Company is a popular business that has recorded, over the past few years, moderate financial performance. Even though the current valuation implies that a short-term discount is evidently present for investors to exploit, for investors with a longer-term horizon it is important to consider all the financial and industry-related factors that will benefit or hurt Kraft Heinz's performance in the future.

For further details see:

Kraft Heinz: A Reluctant Buy For Its Attractive Valuation