KHC - Kraft Heinz: As Price Hikes Fade Focus Will Turn To Volumes

2023-09-07 07:53:21 ET

Summary

- Kraft Heinz has seen growth powered by price hikes, but it has been losing market share.

- The company has seen solid growth in the foodservice industry and emerging markets.

- The dividend currently looks safe.

Back in March , I called Kraft Heinz ( KHC ) a boring, defensive stock - it hasn't exactly lived up to that billing. Since then, the stock has fallen over -13% while the S&P has risen nearly 15%, a pretty stark underperformance. Let's catch up on the ketchup maker.

Company Profile

As a refresher, KHC produces food and beverage products such as condiments, cheese and other dairy products, coffee, meats, sauces, and juices that are sold at grocery stores and other locations. It also serves the foodservice industry, selling its products to places like restaurants and sporting venues. Condiments and sauces is its biggest category, representing approximately 15% of its sales.

The company has six $1 billion revenue brands, including Heinz, Kraft, Philadelphia Cream Cheese, Oscar Mayer, Lunchables, and Velveeta. The company also owns other well-known brands such as Jell-O, Maxwell House, Claussen, Kool-Aid, Capri Sun, Ore-Ida, and Grey Poupon, among others.

Price Vs. Volume

In my original write-up, I noted that price has been the big driver of KHC's sales growth, and this continued to be the case in Q2. For the quarter, the company saw its organic sales rise 4.0%, which is above the company's 2-3% long-term growth target, but which was below analyst expectations of 4.6% growth. Price accounted for 11% of its growth, while volume and mix were -7%.

In North America, organic sales rose 1.3%. Price accounted for 9.4% of the gain, while volume and mix were -8.1%. Internationally, organic sales rose 13.2%, with price increases of 16.5% helping fuel the gains. Volume mix was down -3.3%.

On its Q2 earnings call , CEO Miguel Patricio said:

"Yes, we lost share in the second quarter, but this was a headwind we expected as we priced above the market. Now here's the good news: the pricing is done. And even with elevated price gaps, we aren't losing incremental share to private label. This demonstrates a more resilient portfolio than in the past. Plus, we saw improvements in share each month in the quarter as we executed our action plans discussed in our last earnings call. More about that later. We are, however, losing incremental share to brands who are promoting more than we are. Meanwhile, we are taking a disciplined and surgical approach to protecting our profit dollars in certain categories. With this approach and by continuing to unlock efficiencies across our value chain, we are generating margin gains. With these margin gains, and in line with our strategy to drive further growth, we are investing more in marketing, in R&D and technology."

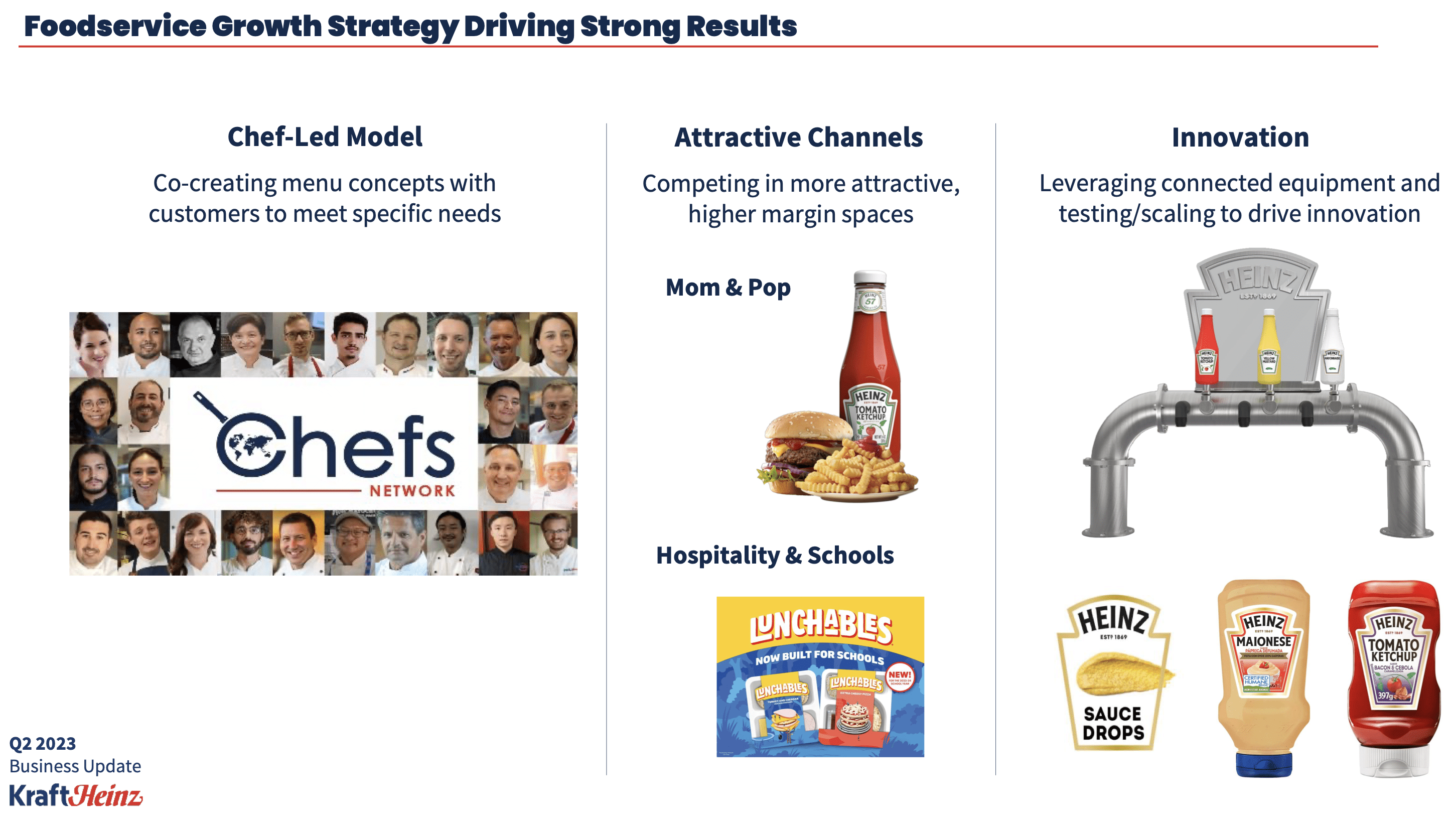

The foodservice industry was another area of growth I discussed back in March, and on that front, the company saw approximately 15% growth in the channel. The company is growing share in this channel, particularly internationally.

The company has introduced new offerings into this channel, such as HEINZ sauce taps, which is a connected technology that has adjustable portion controls, and HEINZ Sauce Drops to test new sauces. This also plays into the innovation opportunity I discussed in my original write-up, and that includes both product innovation as well as tech innovation.

{kind=link}

Emerging markets is another area of focus for KHC, both at retail locations and in the foodservice channel. Emerging markets saw organic sales growth of 11% in the quarter, which slightly trailed overall international growth of 13.2%. The company said a delay in customer replenishment orders and other one-time issues hurt its results by 7%. The company expects emerging market results to resemble its Q1 growth of 23% in the second half.

Overall, KHC grew revenue nearly 3% to $6.72 billion, which just missed the analyst estimates by $80 million. Adjusted EPS rose 13% to 79 cents, topping the 76-cent analyst consensus.

Adjusted EBITDA rose 6% to $1.61 billion. North American EBITDA grew nearly 3% to $1.39 billion, while International adjusted EBITDA climbed 17% to $290 million.

Looking ahead, the company guided for organic net sales growth to be between 4-6%, with the second half more in line with its long-term goal of 2-3% growth. Adjusted EBITDA is expected to grow 4-6%, or 6-8% when accounting for last year having an extra week. Adjusted EPS is projected to be between $2.83-2.91.

On its call, CFO Andre Maciel said:

"Looking to volume, we have seen elasticities revert to more normal levels. And for the remainder of the year, we expect volume declines to moderate. The moderation comes from lapping prior year pricing, the plans Miguel laid out in U.S. Retail, continued market share gains in Foodservice in North America and International zones, and the reacceleration in Emerging Markets from Q2 levels. We expect volume to turn positive in 2024 with future top line growth balanced between volume and price. … We expect the improved momentum from the end of the quarter to carry into the second half of the year. As you can see, we are building a virtuous cycle of growth, enabled by disciplined revenue management, continuing to unlock efficiencies and actively reinvesting back in the business across marketing, R&D and technology to drive future growth."

Later in August, Evercore ISI noted that scanner data showed KHC seeing a -2.9% decline in the prior 4-week period. That compared to overall growth of 2% in the measured U.S. channel. Note that not all sales channels are measured.

After the quarter, the company also announced that CEO Miguel Patricio will be stepping down at the end of the year. He will be replaced by Carlos Abrams-Rivera, who was previously EVP of North America for the company since December 2021. Abrams-Rivera is a long-time industry vet, having served in different roles in the industry since 1998.

While pricing has been strong, volumes have clearly been an issue, with KHC losing market share, particularly in the U.S. Most of the share losses appear to be to other brands that have not taken as much price and are more promotional. This can be a bit of risk, especially with pricing now expected to moderate. If consumers find cheaper alternatives suitable, they may not come back.

As such, the next few quarters will be pretty telling for KHC going forward. The company will have a new CEO to guide them come next year, but the outgoing CEO may have put him in a difficult position with his pricing strategy. That said, I do like the company's initiatives in foodservice and internationally.

Valuation and Dividend

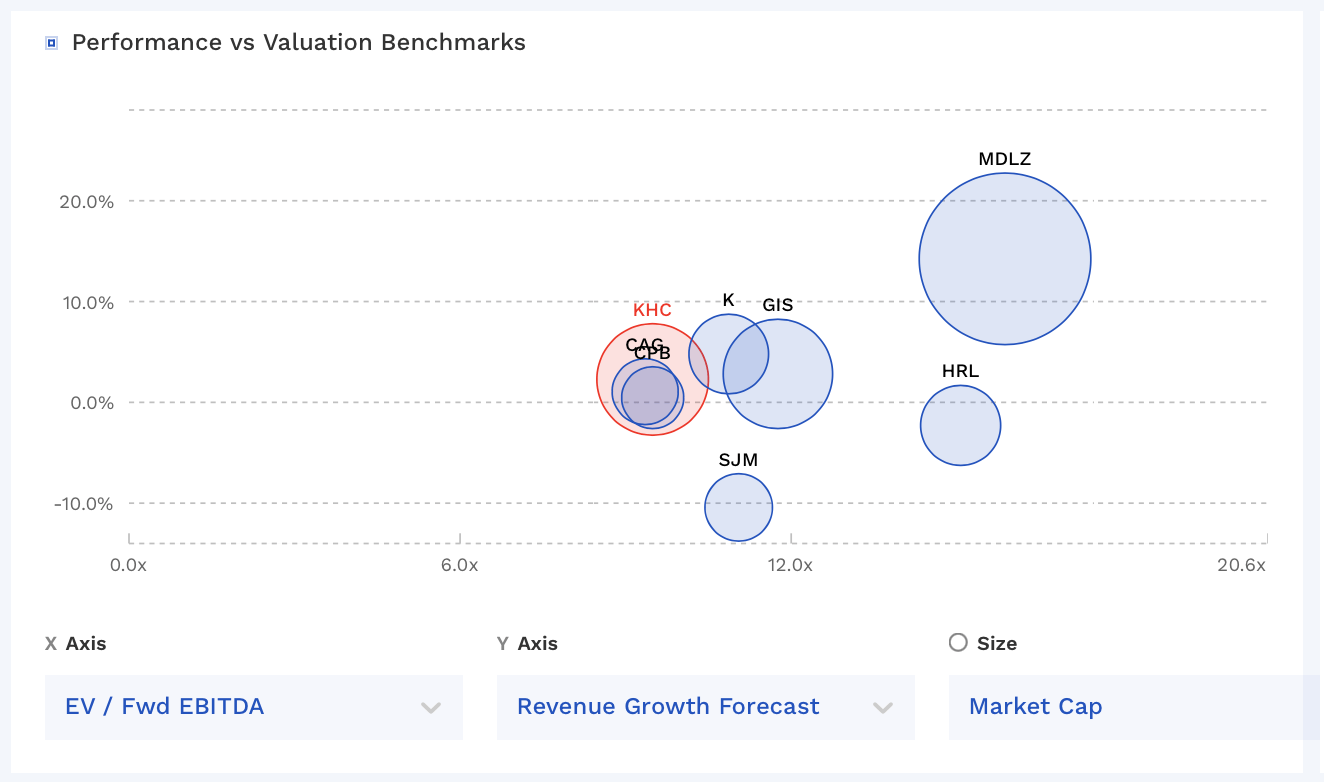

KHC stock currently trades around 9.5x the 2023 consensus EBITDA of $6.24 billion and 9.3x the 2024 consensus of $6.41 billion.

It trades at a forward PE of 11.2x the 2023 consensus of $2.90 and 10.9x the 2024 consensus of $2.99.

It's projected to grow revenue by 2.3% this year and about 1.5% each of the next two years after that.

The company currently pays a quarterly dividend of 40 cents, good for a yield of near 5%. It has paid out the same dividend since 2019, after cutting it from 62.5 cents.

Through the first six months of the year, its payout ratio using net income is 53%. Using free cash flow, it is a much tighter 91%. Its leverage was 3.1x a quarter end.

With its leverage near its 3.0x target, the dividend looks safe.

KFC is among the cheaper food product companies out there, and the company has historically traded between a 10-15x EV/EBITDA multiple.

{kind=link}

Conclusion

KFC is currently cheap, trading below its historical range. However, there are still questions surrounding the medium and long-term impact of its price over volume strategy now that price hikes are expected to moderate and there will be more emphasis on recapturing some volume. In addition, given where interest rates are, low-growth consumer staple companies should trade at lower multiples than when rates were very low.

While I like some of the efforts KHC is making in the foodservice channel and in emerging markets, I still want to see some evidence that the company can win back some customers as it looks to rely less on price hikes. As such, I maintain my "Hold" rating.

For further details see:

Kraft Heinz: As Price Hikes Fade, Focus Will Turn To Volumes