KHC - Kraft Heinz: Back In Solid Value Territory

2023-07-02 08:30:00 ET

Summary

- Kraft Heinz has demonstrated strong sales and margin performance.

- It has adapted its operating model to improve integration between commercial business units and supply chain.

- The stock offers a good opportunity for value investors looking for a stable income generator.

There are some who can’t stomach volatility, and therefore may not have the right temperament for buying and holding onto equities. For those who can stomach price movements, they can harness the power of volatility to create opportunities.

I continue to believe that it’s a market for stocks rather than the stock market. Despite the S&P 500 ( SPY ) being sharply up so far this year, reliable income generators such as those in the consumer staples sector have materially fallen.

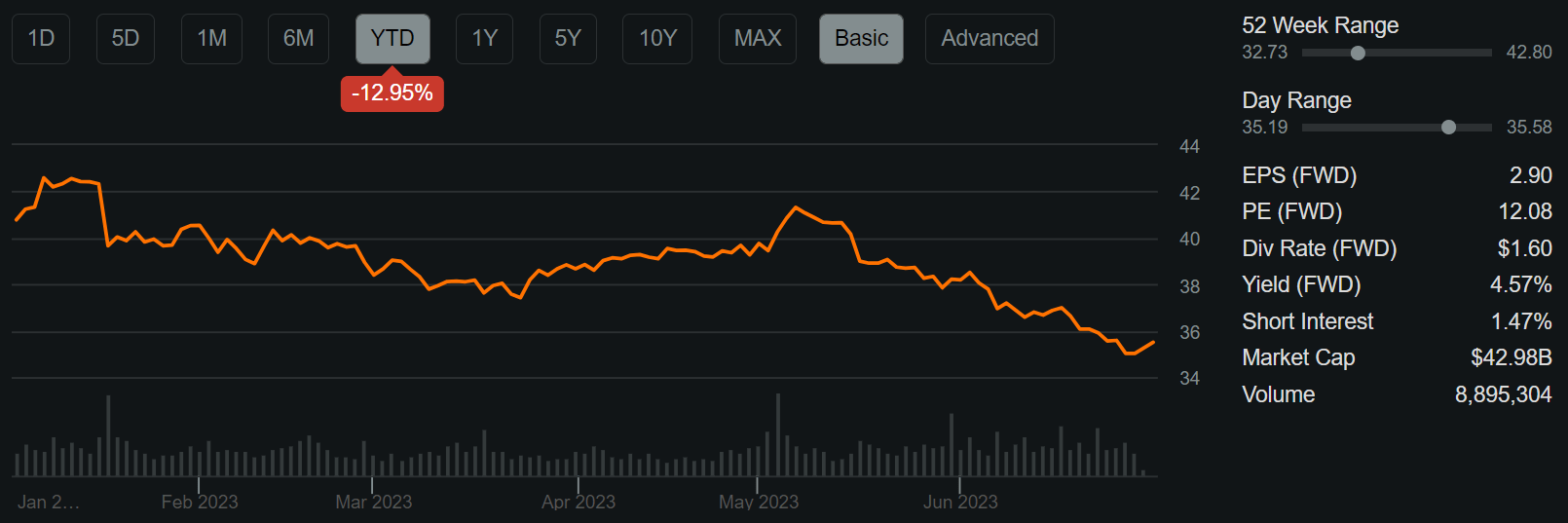

This brings me to Kraft Heinz ( KHC ), which as shown below, has fallen by 13% since the start of the year, putting the price solidly back into value range. I last covered KHC here in March, discussing its progress towards debt reduction and inflation-resistance. In this article, I discuss why KHC is currently a solid value buy at present while market sentiment is working against it.

{kind=link}

Why KHC?

Kraft Heinz is one of the most recognizable names in the food industry, with its namesake brands that span across condiments and packaged foods, along other popular names such as Oscar Mayer and Velveeta. In total, KHC carries over 200 brands, is present in 190 countries, and generated $26 billion in sales last year.

Judging by the share price performance, it would seem as if KHC’s business was doing poorly, but that doesn’t appear to be the case. During Q1, KHC’s net and organic sales grew by 7.3% and 9.4% YoY respectively. Importantly, it’s adjusting well in an inflationary environment with price increase, as reflected by adjusted gross profit margin rising by 126 bps to 32.8%.

Beyond price increases, KHC is also delivering on its promised cost savings of $400 million per year from 2019 levels. After having achieved that over the past 3 years, management is upping the cost savings guidance to $500 million per year, and $2.5 billion in cumulative savings over the next 5 years.

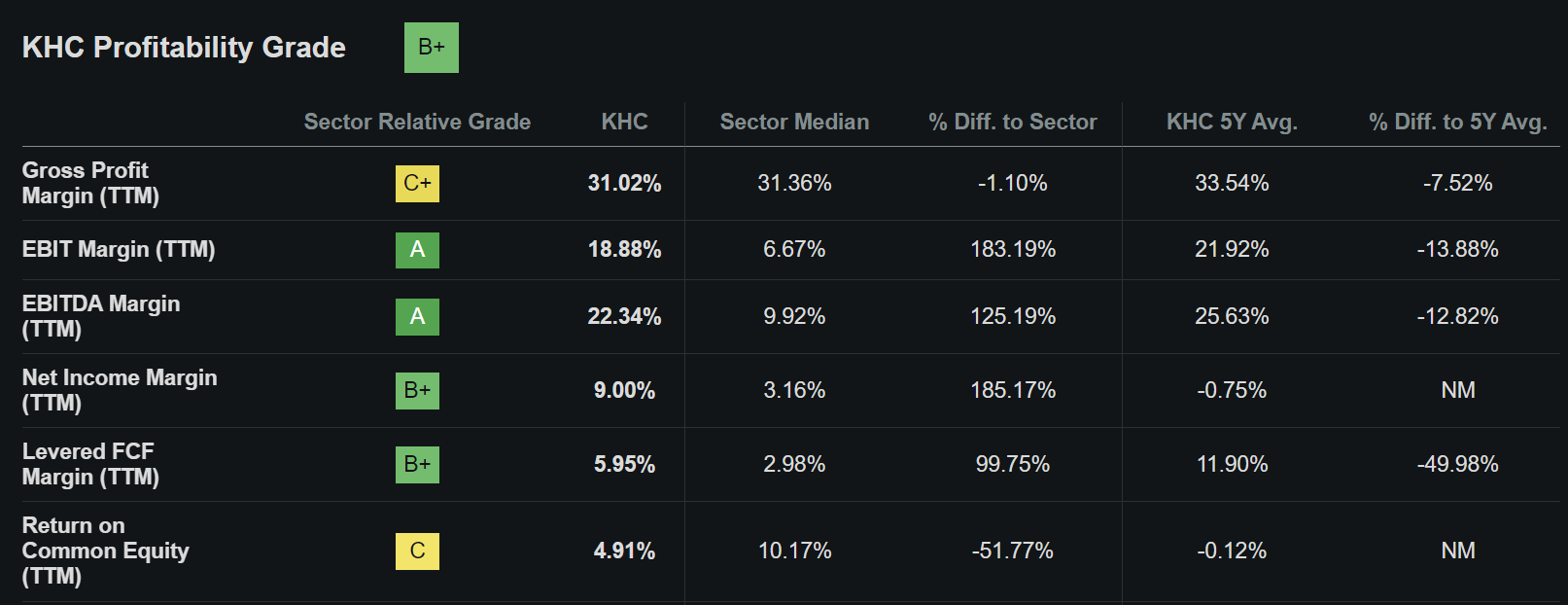

The top-line growth combined with higher profitability contributed to impressive bottom-line adjusted EPS growth of 13.3% YoY. KHC benefits from its wide scale and brand names that enable pricing power. This is reflected by its B+ grade for profitability within the competitive consumer staples sector. As shown below, KHC generates well above average EBITDA and Net Income margins of 22% and 9%, respectively.

{kind=link}

Some of KHC’s success may have to do a dramatic change to the operating model over the past couple of years, in which management broke down siloes between operating units. This was done by changing the incentive structure, in which employees were rewarded for owning the entire P&L rather than just their own component. This is best exemplified by the following management comments during the recent industry conference:

The way that we have managed the company in the past, the commercial people or people in charge of the P&L, they were not really accountable for supply chain performance. As a consequence of that, a lot of energy was wasted inside the company blaming commercial supply chain and the other way around, instead of people working together and really for the better of the company.

We adapted operating model to have very strong integration between commercial and supply chain. For the first time, we have the P&L people also in charge of cash flow, which was not the case up until last year. Even for people to understand holistically the consequences of certain decisions, we are seeing tremendous amount of opportunity getting unlocked, because of that.

Risks to KHC include the recent Supreme Court ruling striking down Biden's proposed cancelation of student loan debt. This could put pressure on consumer discretionary spend and may even result in price disinflation across some spending categories.

While this is a legitimate risk to consider, the pain would be spread across the board, and I would expect for higher end spending like travel and dining out to take more of a hit than consumer staples. In reality, consumers affected by student loan repayments may opt to eat more at home, thereby boosting food stocks like KHC.

Meanwhile, KHC carries a strong BBB credit rating from S&P and has a solid long-term debt to capital ratio of 28%. It's made strong progress towards debt reduction, having paid down long-term debt by more than $8 billion since the end of 2020.

This lends support to KHC's 4.5% dividend yield, which is well-protected by a 56% payout ratio. While dividend growth has been lacking since the dividend was cut in 2019, I would expect for there to be raises down the line, considering that analysts expect around mid-single digit annual EPS growth going forward.

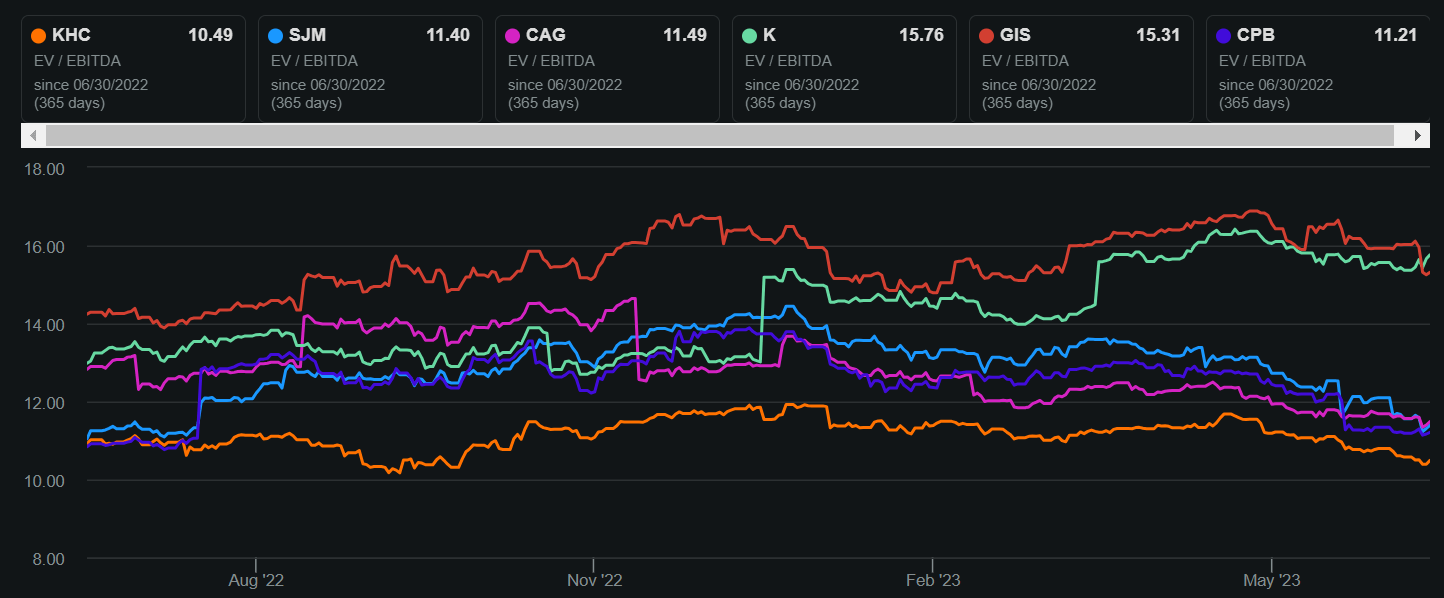

Lastly, KHC appears to be back in bargain territory at the current price of $35.50 with a forward PE of 12.2, sitting well below the 15x to 20x range that consumer staples should trade at over the long run. Doing an apples to apples comparison using EV/EBITDA (since enterprise value includes both equity and debt), KHC trades cheaply compared to its peers. As shown below, its EV/EBITDA of 10.5 sits below that of peers J. M. Smucker ( SJM ), Conagra Brands ( CAG ), Kellogg ( K ), General Mills ( GIS ), and Campbell Soup ( CPB ).

{kind=link}

Investor Takeaway

Kraft Heinz offers a great opportunity to capitalize on market volatility by buying into a strong, well-known brand at an attractive valuation. The company’s debt reduction progress and cost savings initiatives are impressive and should support long-term bottom-line growth.

Moreover, KHC trades cheaply compared to its peers and pays a well-covered dividend that has room for growth. As such, value investors looking for a stable income generator in the consumer staples space ought to consider KHC at the current discounted price.

For further details see:

Kraft Heinz: Back In Solid Value Territory