MKC - Kraft Heinz: Can It Compensate For Poor Sales Growth?

2024-01-16 03:42:59 ET

Summary

- Kraft Heinz's stagnant performance raises questions about its potential while its valuation metrics point to a value investment opportunity.

- International sales are growing while US sales struggle and KHC is focusing on emerging markets for long-term growth.

- Cash flow generation is strong, and favorable margin trends indicate potential profitability gains in the future.

Thesis

Kraft Heinz ( KHC ) is a well-known player in the consumer staples sector and the food industry. Over the recent years, revenue growth has been underwhelming despite other aspects of the business still showing promise. Today, Kraft Heinz also remains a major holding of legendary investor Warren Buffet.

In a previous analysis six months back, I opted for a reluctant buy regarding the stock, concerned about its financial performance, mainly its top-line growth. While that has not drastically changed, the company today shows margin improvement with Q3 results and a willingness to invest more towards growth. As I will show in this analysis, KHC is also focusing on its growing international segment and its attractive valuation remains.

The challenge with Kraft Heinz for the potential investor lies in determining whether the stock's stagnant performance over the recent years indicates a potential laggard in the future or offers a value opportunity worth considering.

Over the past year, Kraft Heinz has seen a steady price decline that has recently been interrupted with the stock ticking upwards. Currently, KHC is trading at a -11% TTM discount, with no gains in stock price returns recorded over the past few years. KHC trades at $37.68 per share ($44.22B market cap) and pays a large 4.25% dividend yield

Brand and Product Variety

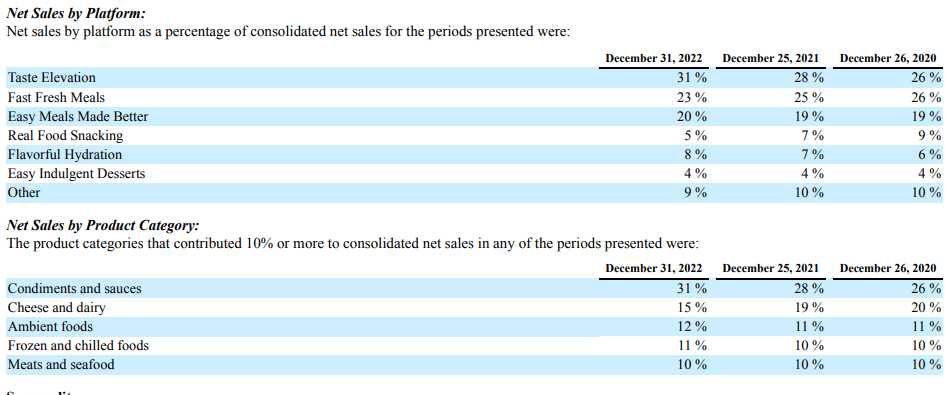

Kraft Heinz is an iconic American food and beverage company that owns an extensive portfolio of brands, including Oscar Mayer, Philadelphia, Heinz, Jell-O, and many others. The diversity of KHC's products is evident in the company's revenue breakdown by platform and product category. The platform leading in Net Sales is Taste Elevation, while the company's popular Condiments and Sauces represent KHC's largest product category.

{kind=link}

International Growth Alleviates Struggles at Home

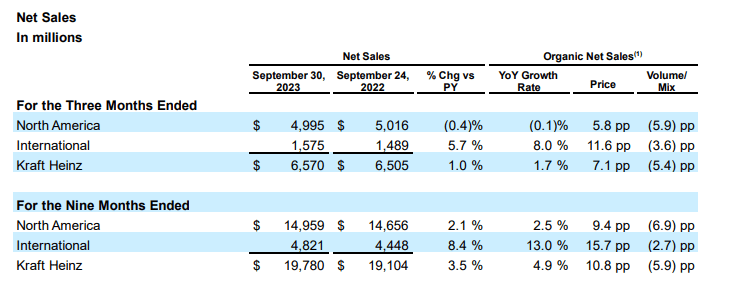

While it is no secret that the company has somewhat struggled with revenue growth over the past years, especially in the United States, international sales seem to be increasing at satisfying rates. In Q3 2023 international sales increased by 5.7% compared to the same quarter last year and 8.4% on a trailing 9-month basis. By focusing more on emerging markets KHC aims to reach its long-term growth goals. Overall, sales increased by a very modest 1.0% in Q3 2023, facing a 0.5% currency translation headwind.

{kind=link}

Other Notable Q3 Items

In order to boost its growth performance, KHC has increased its CAPEX spending by $147M and R&D by 8% YTD in 2023. Kraft Heinz's efforts to gain market share and escape revenue stagnation also include the 25% increase in marketing spending for Q3. The large decrease of 40% in Net Income for Q3 2023 is attributed to accounting reasons, primarily high non-cash impairment losses in the current year period and high tax expenses.

Cash Flow Production

Cash flow generation has significantly increased by 70% (cash from operations), adding to an already strong cash generation performance. KHC has delivered an average of $4.1B in operating cash flow over the past 4 years, widely surpassing net income performance. The amount of free cash flow that the company generates should be able to cover dividend payments to shareholders for the foreseeable future.

Favorable Margin Trends

With inflation cooling down over the past few months, for companies that rely heavily on a wide array of input materials for the production, packaging and delivery of their products, profitability should trend upward in 2024. For KHC this is confirmed in the most recent quarterly results (Q3 2023). The company's gross profit margin improved significantly, by 5.68%, to reach 34%. Adjusted EBITDA also increased by 12.9%. As slow growth comes with the maturity of the business and the defensive nature of the industry, gains in profitability will be key to determining stock performance over the mid-term.

Historic Valuation Multiples

When considering a stock's current valuation attractiveness, it is important to examine the company's own valuation multiples, compared to its own running averages. Counting on mean reversion might not always prove to be a lucrative strategy, but it can still offer some valuable perspective.

From this angle, KHC appears to be trading at a relatively sound valuation at the moment. Kraft Heinz's P/E and P/S ratios stand at 12.5x and 1.7x respectively, both around the company's 3-year averages. The EV/ EBITDA multiple on the other hand stands much lower than its 3-year average, indicating a lower price point for the stock.

Compared to sector average multiples, the stock also appears rather inexpensive. Consumer Staples carry an average 18x P/E, a 1.2x P/S ratio (the only one where the KHC multiple exceeds the sector's), and an EV/EBITDA of 12.4x.

Peer Group Comparison

The consumer staples sector is arguably a very mature one, inhibited by very high-quality companies, especially in the large-cap range. These firms have established massive portfolios of brands and popularity with consumers. They also seem to offer stable slow-growth attributes and strong dividend records. Some of the most notable peers for KHC include PepsiCo ( PEP ), General Mills ( GIS ), Hershey ( HSY ), and McCormick & Company ( MKC ).

As shown in the table below, KHC is the second largest company in the group, behind the giant PepsiCo. It also has a strong net margin of 11.00%, falling behind, however, GIS and HSY. Kraft Heinz pays the largest dividend yield in the group (4.25%), which is mainly a result of the company trading at lower valuation multiples, as the company hasn't managed to deliver growing dividends recently.

On the other hand, KHC's lower valuation metrics come to show that the market does not greatly appreciate the company's lacking growth metrics (0.71% 5-year revenue CAGR and -2.39% 5-year EBIT CAGR). KHC's gross margin is also not that strong despite a very good EBITDA and Net Margin.

SA

Final Thoughts

After all, things are considered, despite KHC lacking competitors in sales and earnings growth, the stock's current valuation multiples are arguably attractive and its overall performance deserving of optimism going forward. Focusing on improving profitability and cash flow productivity investors can expect decent returns from KHC at its current price point. As such, I would currently rate the stock as a buy.

For further details see:

Kraft Heinz: Can It Compensate For Poor Sales Growth?