KHC - Kraft Heinz: Decent Company However I'm Waiting For Improvements

2023-09-07 19:59:00 ET

Summary

- Kraft Heinz's low P/E ratio is justified due to low revenue potential and unknowns in margins.

- The company's revenue growth is stagnant, with the Taste Elevation segment being the only area of growth.

- Kraft Heinz needs to focus on expanding internationally and improving its financial metrics and competitive advantage.

Investment Thesis

Kraft Heinz ( KHC ) has been going downhill for a while now, plummeting over 40% in the last 5 years, and now trading at a forward P/E of around 11. I wanted to take a look at the company's financial health over the last couple of years and see if this low P/E is justified or if is there a deal to be had. With the management's cost-cutting measures going well, and a predictable yet low revenue growth, I believe that the FW P/E ratio is warranted, and I can see the company growing EPS steadily for many years. The shares are valued fairly; however, I would like to see financials improve more, therefore I assign a hold rating.

Outlook

The company's growth is very easy to predict since it isn't growing much anymore in terms of revenue potential. From FY17 to FY22 the company’s revenues went essentially nowhere and are propped up by the only decent segment which is the Taste Elevation that includes sauces and condiments. This segment still saw low-double-digit growth as of FY22 and Q2 ’23 while the rest of the segments either fell or were essentially flat.

I would like to see the company putting more effort into growing its revenues internationally, as it looks like the North American segment has been fully penetrated and the revenue growth seems to keep up with stabilized inflation of around 2.5%-3%.

The management mentioned that emerging markets make up around 10% of total revenues and are confident that the growth in this segment is going to be in the double-digits as it has been in the past. So, the impact on the total revenue isn’t going to be huge for now, and I don’t expect it to become very big in the near future. Further ventures like the one with NotCo are a step in the right direction, but I don't think these types of plant-based alternatives are going to yield a lot of profit in the long run. It certainly won't hurt, but my biggest concern is how pricy these alternatives are going to be in the future and what kind of margins will be attained.

Another way the company can improve its value is by managing the costs. In the Q1 quarterly transcript , the management was very confident in their cost-cutting measures, which totaled around $400m a year for the last 3 years. The management was so confident in their cost-cutting measures, that they have increased their annual savings target to $500m a year going forward. Cutting off low-yielding margin products and focusing on better-performing ones is a sure way to increase profitability and we will have to wait and see what kind of savings the company will attain.

Financials

The following graphs will be as of FY22 because this will give me a better understanding of how the company has been performing and whether there is a trend. I will include some of the latest figures that I deem necessary for extra color.

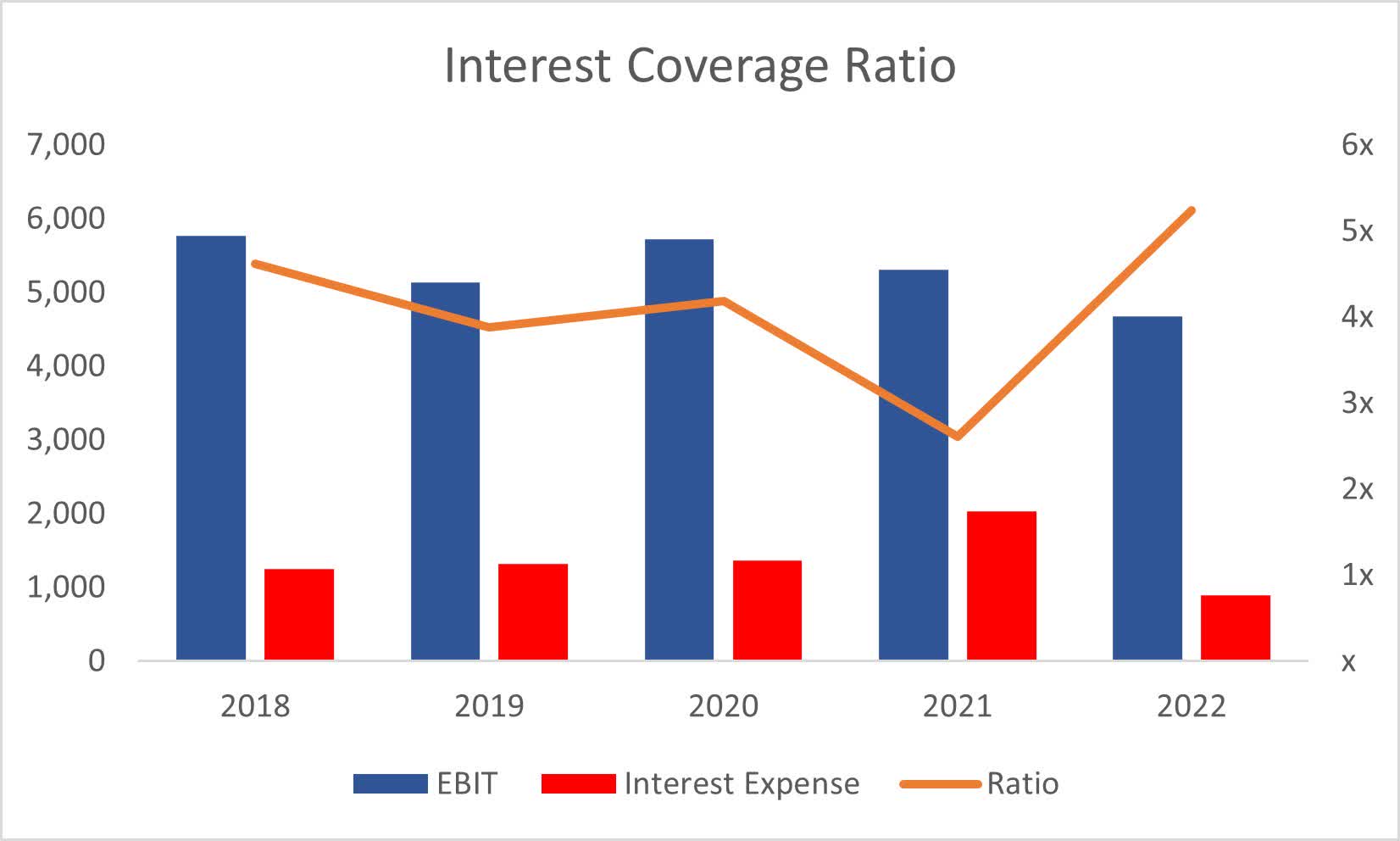

As of Q2 ‘23 , the company had $947m in cash against $19B in long-term debt. That is quite a substantial amount of debt, and many investors would look no further because of the inherent dislike of leverage. I believe that debt is a smart way of improving a company's operations and it is only bad if the debt levels are not managed properly. I believe the debt of KHC is manageable. The interest coverage ratio historically has been around 2x-5x, which means that EBIT has been able to cover annual interest expense on debt around twice to five times over. For reference, 2x is considered a good ratio in general, however, I consider 5x to be the minimum because I like to be more conservative. In my opinion, the company is at no risk of insolvency.

Interest Coverage Ratio (Author)

{kind=link}

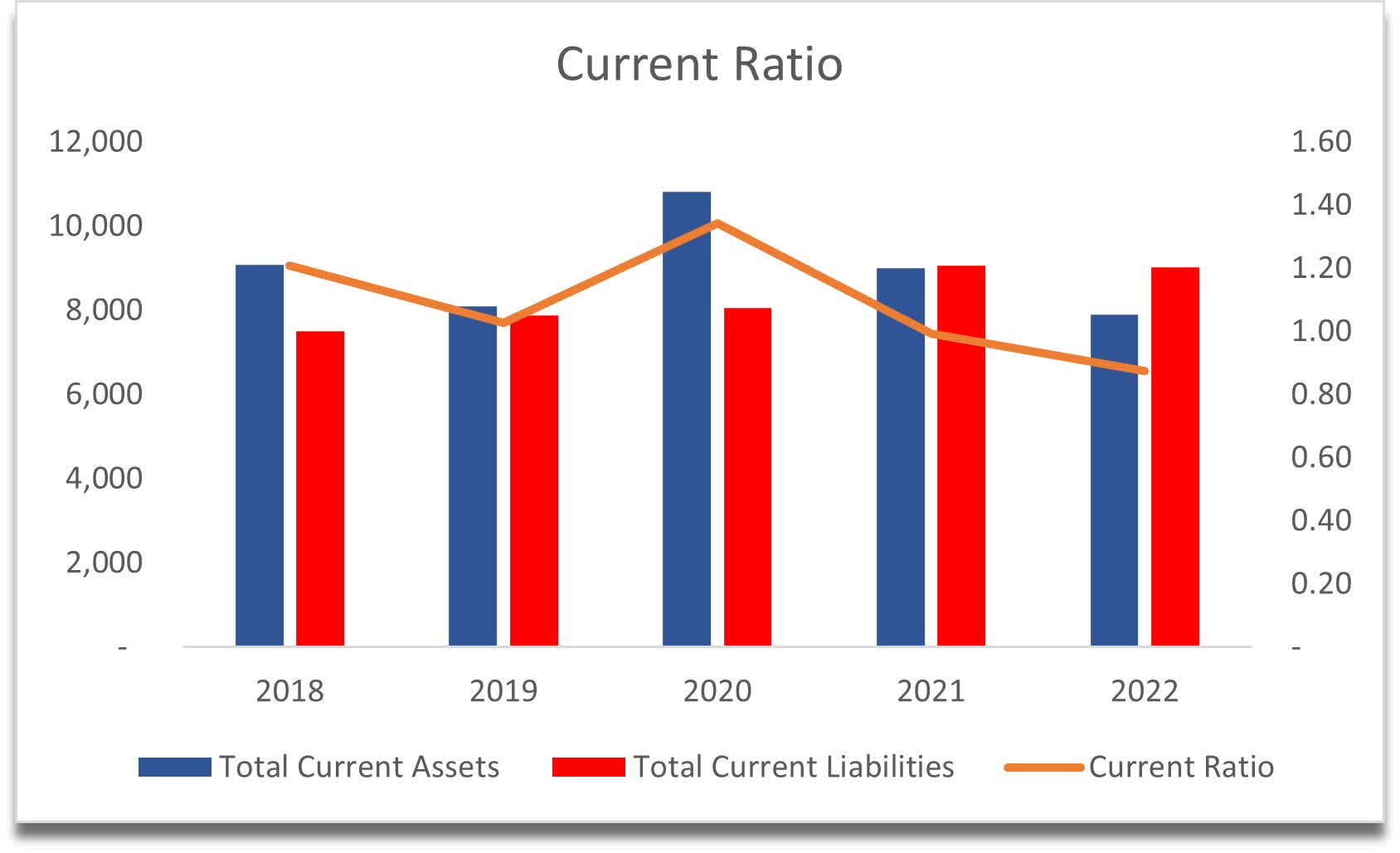

The company’s current ratio has been a little disappointing, however, it seems to be sector-wide as many other competitors do have somewhat lower ratios than what I am looking for, which is around 1.5-2.0. As of Q2 ’23, this has slightly improved from FY22, which is a good sign. The positive I could take from this current ratio is that the company seems to be using its cash and not hoarding it. I like the fact that the management is taking action to continue to expand its operations. I don’t think the company has any liquidity issues.

{kind=link}

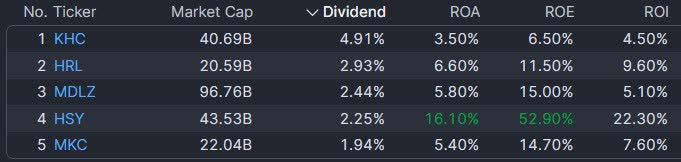

In terms of efficiency and profitability, the company's ROA and ROE, have been on the lower end for my liking, which isn't ideal, to be honest, especially compared to the competition. I took the suggested competitors by Seeking Alpha, so we can see that the ROA and ROE of KHC are the lowest out of all of them, which tells me that the management isn't using the company's assets and shareholder capital very efficiently. Furthermore, the company doesn't seem to have a competitive edge or a strong moat also when looking at the return on investment.

ROA, ROE, ROI, and Dividend Yield ( Finviz)

{kind=link}

The company’s dividend yield is also quite attractive compared to the competition; however, I wouldn’t rely on that. The company has 0 years of dividend growth and has cut it in 2019. The current payout ratio sits at around 62% according to Seeking Alpha, which could mean it may be cut once again if the performance goes down, or the company may have to take on more debt to finance that dividend.

Overall, the financials are on the lower end of the competition, which tells me there is a lot of work ahead for KHC. I will need to assign a higher margin of safety to my valuation model to find what I would be willing to pay for such a company.

Valuation

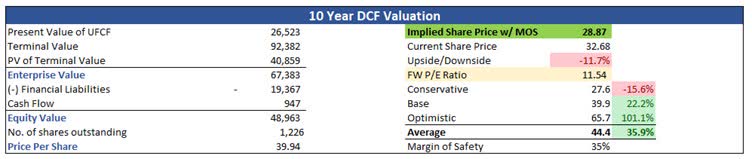

Seeing that the revenues haven't grown much over the last 5 or so years, for my base case scenario, I will grow revenues at around 3% CAGR for the next decade, which basically will keep up with inflation. For my optimistic case, I went with 7% CAGR, taking into account that international markets performed extraordinarily well, while for my conservative case, I went with around 1% CAGR to round out the range of possible outcomes.

In terms of margins, I improved gross margins by around 500bps or 5%, while improving operating margins by around 200bps over the next decade. This will bring net margins from around 9% in FY22 to around 16% by FY32.

I wasn’t a big fan of the company’s financials, so I decided to add a 35% margin of safety to the final intrinsic value calculation as I would like to have more safety cushion to take on the risks of the company. With that said, KHC's intrinsic value is $28.87 a share, implying around 11% downside from the current valuation.

{kind=link}

Closing Comments

For me to start a position in a company that has quite disappointing revenue potential, financial metrics, and lots of unknowns in the cost-cutting measures, I would require a larger margin of safety. I feel like around $29 a share, the company would reflect my risk/reward profile better and I would consider opening a position and seeing how it goes over the next couple of years.

I would like to see the company's competitive advantage go up and its moat improve because it looks like it has none compared to the competition. I would like to see better efforts in expanding in emerging markets in the future as I see there is a lot of potential internationally, I feel that the North American market is as good as it gets, but I would like to be pleasantly surprised there too.

I will assign a “hold” rating for now until I see some good progress in the mentioned metrics.

For further details see:

Kraft Heinz: Decent Company, However, I'm Waiting For Improvements