KHC - Kraft Heinz: Holding On For Q4 Earnings Improvement As Stock Price Heats Up

2023-12-13 11:34:21 ET

Summary

- The Kraft Heinz Company is rated Hold today, agreeing with the sentiment from the quant system.

- It has positive tailwinds from equity growth and declining debt, and low price-to-book value.

- The share price is trading above average, earnings growth is not exceptional, and dividend growth over 10 years is not competitive.

- The risk of recession impacting consumer spending has been discussed.

Stock Snapshot

Rounding out my latest articles themed around the holiday spending season including retail, airline travel, and food brands... today's research note covers what I would call a well-known and long-established household brand name in the supermarket aisle, and one that could have a place at the holiday food table this year.

Some quick facts about The Kraft Heinz Company ( KHC ) are that it is the parent company behind such food brands as Velveeta cheese, Jell-O pudding, Heinz ketchup, Capri-Sun juice packs, and many more.

It calls itself one of the largest food and beverage companies in the world, its 2022 net sales topped +$26B, and is involved in 40+ countries worldwide.

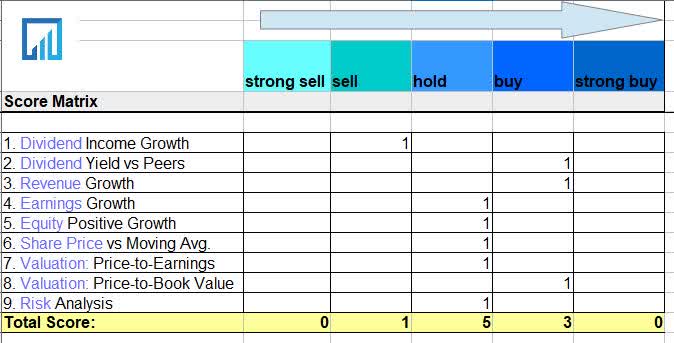

Scoring Matrix

This article uses a 9-point scoring matrix that holistically considers multiple angles of the stock, with an emphasis on cashflow potential for investors and fundamental trends from the key accounting statements publicly available such as the balance sheet and income statements, as well as a future-looking outlook on this stock.

Today's Rating

{kind=link}

Based on the score total in the score matrix above, this stock is getting a rating of hold.

Compare to the consensus rating on Seeking Alpha, I am agreeing with the sentiment from the SA quant system this time:

Kraft Heinz - rating consensus (Seeking Alpha)

Dividend Income Growth

This section uses dividend growth data to explores the 10-year dividend income growth for a hypothetical investor owning 100 shares, to determine whether this stock is a great dividend income opportunity.

{kind=link}

Using the above 10 year dividend growth chart, let's say I bought 100 shares in 2013 when the annual dividend was $2.05 ($205 annual dividend income) and compared with 2022 when annual dividend dropped to $1.60 ($160 annual dividend income), that is nearly a 22% decline in dividend income over this 10 year period (2013 - 2022).

Looking at the history , for 2023 the dividend has not increased yet, so we can assume the annual income would still be the same at $160. As there is no steady growth trend in the last 10 years, it becomes difficult to extrapolate to the next 10 years and how 2032 would look for a dividend investor.

For this reason, I will call this stock a sell in this category, on the basis of proven declining dividend income potential in the last 10 years, and a flat growth this year.

Dividend Yield vs Peers

This section uses dividend yield data to compare the trailing dividend yield vs 3 similar peers in the same sector, to determine if this stock presents the most competitive dividend yield on capital invested.

{kind=link}

In this comparison chart I did above, I am comparing my focus stock of Kraft Heinz with some peers and or related food brand parent companies with significant brand penetration in American supermarkets. These include spice company McCormick ( MKC ), food conglomerate Mondelez International ( MDLZ ), and Hershey ( HSY ).

Of this peer group, Kraft Heinz came out far ahead of the pack with a trailing dividend yield of 4.35% (same as their forward yield), while the others trailed behind in the +2% range.

I would call this stock a buy in this category on the basis of a +4% yield beating several peers, and presenting a buy opportunity for a dividend investor looking to maximize yield on capital invested.

Revenue Growth

This section explores this company's revenue growth trends over the last year, using data from the income statement.

From this data point, we can gather that the revenue in the quarter ending September grew to $6.57B vs $6.50B in Sept 2022, a sluggish 1% YoY growth.

The longer trend between June 2022 and Sept 2023 shows an unsteady trend jumping between growth and decline, and no steady long-term growth trend.

Diving a bit further into company Q3 data to better understand the drivers of these results, we first see that organic net sales grew less than 2% on a YoY basis:

Kraft Heinz - organic net sales (company results)

A positive mention is that their international business saw +5% net sales growth in this period while North America actually struggled to grow.

Kraft Heinz - intl growth (company results)

In addition, its outlook for the entire FY23 remains mildly positive, with "organic net sales growth of 4 to 6 percent versus the prior year, closer to the lower end of the range at approximately 4%."

In this category I will give it a buy on the basis of positive but mediocre top-line revenue growth, combined with the positive full-year outlook. Also, we are approaching the last stretch of holiday shopping season as well as company office parties, family dinners, and such, which means more food spending... and the income statement clearly shows that the quarter ending December is one of the strongest quarters for this company (as shown in years 2022 and 2021).

Earnings Growth

This section explores this company's earnings (net income) growth trends over the last year, using data from the income statement.

This data point shows how the company achieved $262MM in Q3 vs $432MM in Sept 2022, a 39% YoY decline.

Much like with revenue growth, the bottom-line growth has also been lopsided between Sept 2022 and now, not showing a steady growth trend.

According to their Q3 earnings release , drivers of this were "higher non-cash impairment losses in the current year period and higher tax expenses in the current year period."

Net interest expenses appear to have dropped slightly to $216MM vs $221MM in Sept 2022, an improvement but not by a lot.

What appears to have jumped significantly was the total operating expenses which grew to $894MM in Q3 vs $765MM in Sept 2022, a +16.8% YoY increase.

Other factors mentioned as impacting profits were items like inflationary pressure on manufacturing and procurement costs as well as increased commodity costs.

However, also important to note is that the company upgraded its full-year outlook for earnings per share:

Adjusted EPS to be in the range of $2.91 to $2.99, compared to the previous range of $2.83 to $2.91.

In this category I would call this stock a hold , on the basis of earnings declines offset by positive forward outlook on EPS.

Equity Positive Growth

This section explores this company's equity (book value) growth trends over the last year, using data from the balance sheet.

The good news in this category is that the total equity grew to $49.45B in Q3 vs $48.34B in Sept 2022, a +2% YoY growth.

The longer trend is that equity has been generally higher after Dec 2022. Long-term debt decreased only slightly to $19.27B in Q3 vs $19.29B in Sept 2022, while total liabilities as a whole also decreased on a YoY basis.

I will call it a modest buy in this category, on the basis of slight YoY equity growth and declining debt.

Share Price vs Moving Average

This section explores the current share price compared to the 200-day simple moving average , to decide if it currently presents a buy, hold, or sell opportunity.

In the YChart above, the current share price is trending around $37.37, or +4% above the 200-day simple moving average.

I think in terms of this chart a much better buy opportunity presented itself this autumn during that price dip to around $32. However, the current price is still well below the January high, but I don't think quite in sell range yet.

I will call it a hold in this case on the basis that the price has crossed above the long term moving average but not by a lot, and is up from its October lows by about $7/share. At the same time, the company is profitable and has growing equity and a +4% dividend yield but also has very sluggish revenue and earnings growth.

Valuation: Price-to-Earnings

This section uses valuation data to explore the forward P/E ratio and whether it presents an undervalued opportunity.

In this data point we can see that the GAAP-based forward P/E ratio is 14.52, or around 24% below its sector average, and earning a grade of B+ from Seeking Alpha.

In tying back to the share price and earnings discussion, I think what is driving this multiple of 14.5x earnings is the spike in share price combined with weak or declining earnings growth lately.

I think this is an elevated multiple, and I don't think it is justified at 14.5x because earnings growth has not been impressive yet the share price has spiked above its long term moving average. For this reason I will call this stock a hold in this category, until earnings growth catches up to the rise in share price. I am mildly confident they may be able to improve earnings for Q4 which is a busy holiday food shopping quarter, and it appears they have beat all of their last 4 earnings estimates .

Valuation: Price-to-Book Value

This section uses valuation data to explore the forward P/B ratio and whether it presents an undervalued opportunity.

In this data set, we can see that the forward P/B ratio is 0.91, around 68% below the sector average.

In tying back to the equity and share price we discussed, we can see that even though the share price spiked the equity/book value also went up on a YoY basis.

For this reason, I will call it a buy at 0.91x book value, on the basis of improving equity and declining debt liability.

Risk Analysis

This section identifies a key risk to consider about this company and what its probability and impact could be to the business.

Nasdaq mentioned in a Dec. 8th article covering this stock that there were several risks to consider:

Despite the promising outlook, there are also potential risks to consider, such as rising ingredient and labor costs, competition from private labels, and the possibility of an economic downturn that could dampen consumer spending.

I will focus briefly on that last risk of an economic downturn affecting spending. After the shopping spree of the holiday food season subsides, the question is whether the company can count on a sustainable consumer market in the new year or will consumers pull back on things like ketchup and Velveeta cheese.

According to an article in Fortune magazine this week discussing recession potential for 2024:

Consensus growth forecast remains at a sluggish 1.2% (below where they were a year ago) and recession odds are seen at 50%.

Still, other media outlets are giving mixed signals such as today's article by Business Insider's Markets Insider portal:

American consumers are starting to slow down after a ferocious spending spree that lasted through most of 2023. That could set the economy up for a consumer-led slowdown, one strategist told Business Insider, pushing the US to the brink of a recession.

Ultimately though, a recession may present a buying opportunity for investors, Emanuel said, as he believed stocks would benefit from inflation continuing to fall in the back half of the year.

I think it is a safe bet to call this stock a hold when it comes to recession risk since the company being a consumer products company it could face headwinds but at the same time it essentially sells grocery food items which can be considered a critical necessity to American households, in my opinion. In other words, it is not a company selling luxury jeans or stereo headphones, but food.

At the same time, they are not the only game in the supermarket aisle, and have to compete often with store-brand products who may be cheaper, as customers increasingly try to balance their household budgets. There is also the whole trend of organic/healthy/locally sourced food driven by the Whole Foods brand culture I would say, and more health-consciousness about ingredients.

Quick Summary

To summarize, I am neutral on this stock in today's note and the positive tailwind comes from the +4% dividend yield and low price-to-book value, while headwinds are coming from weak earnings and revenue growth, lackluster dividend growth over 10 years, a share price now trading well above its autumn lows, and the risk impact a potential recession could have on this company.

My portfolio strategy in this case if I owned this stock would be to hold on to this one until it potentially goes up a few more bucks per share after Q4 results, assuming Q4 will be a blowout quarter on earnings and it pushes the share price up further, and then sell out of my position since I am not getting much in terms of dividend income.

For further details see:

Kraft Heinz: Holding On For Q4 Earnings Improvement As Stock Price Heats Up