KHC - Kraft Heinz: I Believe In Their Deep Value Turnaround Story

2023-07-05 18:07:59 ET

Summary

- Kraft Heinz, the third-largest producer of packaged foods in the US, has seen mixed performance since its 2015 merger, leading to generally pessimistic investor sentiment towards the firm.

- The appointment of a new CEO and a focus on operational excellence could provide a turnaround deep-value opportunity for value-oriented investors.

- Despite challenges such as changing consumer tastes and rising costs, the company's strong brand portfolio and economies of scale provide a narrow economic moat.

- A 29% undervaluation provides a sufficient safety margin to potentially build a position in the firm.

Investment Thesis

The Kraft Heinz Company ( KHC ) is the third-largest producer of packaged foods in the United States. Their global scale combined with a widespread product portfolio provides the firm with a narrow economic moat.

Mixed performance since the 2015 merger of Kraft and Heinz has left investors uncertain about the profitability of the firm with questions about management's competence arising in previous years in my view.

The recent appointment of a new CEO combined with a march towards operational excellence creates a potentially lucrative turnaround deep-value play for value-oriented investors.

Company Background

The Kraft Heinz Company (hereinafter "Kraft Heinz") is a global food and beverage conglomerate that owns and operates a number of iconic brands across a wide range of different product categories.

Brands such as Kraft, Oscar Mayer, Heinz, Philadelphia, Velveeta, Kool-Aid and Jell-O are all trademarked brands sold by Kraft Heinz.

Through a merger that consummated in 2015, Kraft Foods Group and Heinz Holding Corporation came together to become the food giant they are today. Prior to this merger, Heinz used to be owned by Warren Buffett’s Berkshire Hathaway (BRK.B) (BRK.A).

Today, the brand has a huge global presence with products being essentially sold worldwide. This presence is facilitated by their extensive range of brands that are ‘ household names’ in many countries and regions.

Nonetheless, the years following the 2015 merger have been turbulent for the company. Mixed fiscal results combined with some difficult macroeconomic pressures have caused shares to shed a significant 45% of their value since mid-2018.

A change of management in the form of Miguel Patricio stepping-up to the position of CEO has brought along a welcomed change in capital allocation structures which should see KH prioritize long-term profit growth over boosted short-term FCF.

Economic Moat - In-Depth Analysis

KH’s primary drivers of matiness are their extensive range of iconic brands combined with synergies arising from economies of scale advantages.

Kraft Heinz 10-k FY22

KH’s iconic range of brands are the key moatiness drivers for the firm with essentially their entire business resting on the popularity of these banners.

Many individual brands such as Heinz, Kraft and Philadelphia have become synonymous with the products they sell be it sauces, mac and cheese or soft-/cream cheese. This allows KH to charge a premium compared to non-branded products.

Fundamentally, it is critical that KH is able to maintain this level of distinction and reputation for their brands to ensure their pricing power is not eroded. Any erosion in the perception of their brands in the eyes of consumers could lead to declining sales and an inability for KH to charge more for their products compared to their peers.

To maintain the reputation and image of their individual brands, KH must engage in a significant amount of active marketing which targets the consumer demographics their products are aimed at serving.

While some of their brand’s benefit from being established household names, the importance of marketing still cannot be overstated. While Heinz Tomato Ketchup and an off-brand competitor may have slight variances in taste, the real differentiator between such products is how the customers feel about them.

Psychologically , an established and ‘better’ brand image can lead to customers actively experiencing a more enjoyable consumption experience that with a non-brand competing product.

KH relies on this psychology phenomenon to drive sales of their branded products which is why marketing is such a crucial element to their business model. Without a sustained and popular brand image, KH would suffer significantly in the grocery stores as their more expensive products would have no other tangible advantage over cheaper competitors.

Equally, KH is currently dealing with the matter of small-name, niche product brands becoming increasingly popular in the eyes of consumers. This transition in popularity marks a fundamental shift in general consumer sentiment with regards to what qualities are valued most in the purchasing decision making process.

While the well-known image of many of KH’s brands instill confidence and trust in the minds of consumers, the increasingly popular trend for consumers to value artisan products more highly could place KH’s previously robust portfolio in a difficult position.

While the longevity of such trends is difficult to assess, it is undeniable that a shift in consumer orientation away from products owned by “food giants” towards more sustainable or small-scale businesses has been occurring for the last few years. KH must assess how best to deal with this shift if they are to maintain the pricing power their products currently enjoy.

KH has also been trimming their product portfolio to eliminate those brands and businesses that are preventing the firm from achieving margin expansion. In this process, Planters has been sold-off from the company’s portfolio along with Natural Cheese .

Management believes these strategic portfolio adjustments will allow KH to devote more of their resources to the most profitable and strong brands in their portfolio which should ultimately help expand margins and drive further economic growth.

Another source of moatiness for the firm arises from the economies of scale the company enjoys when producing certain ranges of products. The sheer scale of brands such as Heinz allows KH to negotiate harder with suppliers and benefit from numerous operational efficiencies that arise when producing in huge volumes.

KH also has a significant number of business customers in the foodservice industry which further increases total volume production figures for the firm. While foodservice customers generally are more difficult to sell to and often require aggressive pricing contracts to be established, KH is able to utilize these large-scale orders to significant increase their total product output.

Many fixed costs associated with the production of food products can be minimized as a portion of revenue when operating on such a massive scale. This allows KH to enjoy tangible economic competitive advantage that smaller corporate food conglomerates such as McCormick & Company (MKC) or artisanal brands will simply be unable to replicate.

Still, it is important to consider that KH is not the largest player in this industry. Competitors such as Mondelez ( MDLZ ) and Nestle ( NSRGY ) are both two and three times bigger than KH respectively (by current market cap). Therefore, while KH undoubtedly enjoys numerous benefits from the scale of their operations, these advantages may be relatively minor compared to their largest competitors.

Overall, I believe KH harbors a narrow economic moat. It is difficult to assign any real robustness or breadth to their moat due to the lack of tangible differentiation existing in their product portfolio.

Furthermore, while their operational model yields economies of scale benefits that help expand gross margins for the firm, these factors are not unique to the company and are equally present at their closest competitor’s firms.

Financial Situation

The last four years have been a little mixed at KH from a financial performance perspective. Their 4Y average ROA, ROE and ROIC currently rest at 1.25%, 4.23% and 4.10% respectively. While these figures are not particularly outstanding, they do represent a relatively consistent average for the firm since their 2015 merger.

In the same time period, gross, operating and net margins have averaged 32%, 19% and 5% respectively. These margins (particularly operating and net) are quite healthy considering the significant portion of revenues KH must dedicate towards marketing their products.

KH operates their business on an average of 91 days payables which illustrates the relatively tough approach to operations the firm takes with their suppliers.

These core operating performance metrics illustrate that KH is a fundamentally profitable and well operated firm. Some of the variation present in their long-term fiscal history (10Y) is largely due to the nature of the industry.

{kind=link}

Considering KH’s FY22 , a reasonable improvement in operational results was seen compared to FY21. Net sales grew by 1.7% YoY with particular strengths coming from maintained brand popularity resulting in increased product sales along with their Foodservice segment outpacing industry growth expectations.

Organic net sales also increased 9.8% YoY in FY22 which further illustrates the strengths of KH’s brands and brand reputations in the consumer sphere of influence. Of course, this organic net sales figures is a non-GAAP financial measure so its merits should be taken with a pinch of salt just to err on the side of caution.

{kind=link}

Operating income for FY22 grew by 5% YoY totaling $3.63B. This was primarily driven by higher pricing (partly necessitated by the currently inflation affecting economies across the globe) and lower non-cash impairment losses impacting positively on their operations.

Some of these gains were offset by higher supply chain costs particularly in the procurement, logistics and manufacturing costs. Increasing commodity costs were also noted as having a negative impact on net income.

While these factors are nothing new, it is welcomed to see KH dealing with these issues so proficiently. While some companies are seeing net income plummet due to the aforementioned inflationary and interest-rate related issues, KH and their efficient business model seems to be more flexible in adapting to this new macroeconomic environment.

Of course, it is difficult to say how the firm will deal with these factors in the long-run. Nonetheless, current results suggest that KH is well equipped to operate their business even in a more macroeconomically unfavorable environment.

Still, adjusted EBITDA decreased 5.8% YoY to $6.0B in FY22. This was primarily a result of the increased supply chain costs combined with unfavorable FX impacts. While regrettable, I am not too concerned by this decrease as their fundamental operational efficiency was unaffected.

The primary reason that led to adjusted EBITDA falling was the drop in positive impairment losses from $1.6B in FY21 to just $999M in FY22. This was primarily attributed to the sale of Planters and Natural Cheese.

Operating expenses for FY22 actually decreased by $720M YoY which represents a 14% reduction. This is incredibly positive to see especially given the challenges created by the unprecedented macroeconomic conditions currently impacting the globe.

This fundamentally positive performance in FY22 suggests management’s new turnaround initiative is working as intended. The operational efficiency improvements promised seem to be having a positive impact on the profitability of the firm.

{kind=link}

From a geographic perspective, North America remains KH’s largest market representing around 70% of total net sales. However, from a growth perspective KH’s international market segment undeniably has the most potential with 12% YoY growth being unlocked from this expanding business opportunity.

Emerging markets present a unique opportunity for KH as the rapidly growing middle-classes in these regions could become valuable new customers for the firm’s products.

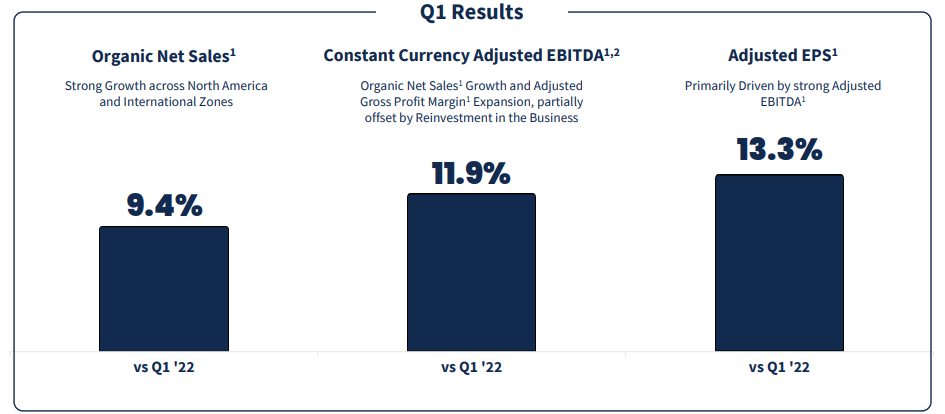

Kraft Heinz FY23 Q1 Presentation

{kind=link}

Similar strengthening performance was observed in Q1 of FY23 with strong organic net sales growth of 9.4% being achieved. Similar growth was seen in their adjusted EBITDA EPS which grew 13.3% YoY along with a constant currency EBITDA expansion of 11.9%.

Gross profit margins have also increased 1.2% YoY thanks to pricing flow-through and unlocked operational efficiencies. These improvements have allowed the company to moderate cost inflation from a business perspective which is great news for shareholders.

This also supports my earlier thesis that KH’s management seems acutely tuned-in to the intricacies involved with managing a difficult macroeconomic environment.

All of KH’s three product categories (foodservice, emerging markets and North American retail) saw healthy YoY growth of 30%, 23% and 8% respectively. These healthy increases in organic net sales once again act as empirical evidence which suggests the firm’s turnaround strategy is working as intended.

Q1 also saw the firm enter net untapped sales channels such as the travel foodservice segment with the firm now supplying airlines with select branded products to be carried aboard regular service flights. A similar expansion of the Lunchables brand into the National School Lunch Program is estimated to represent a $25B market opportunity for the firm.

These strategic expansions into previously disregarded business segments illustrates not only the newfound strategic agility CEO Patricio has brought to the table, but also the universal strength of the firm’s product range.

Many of the firm’s most famous brands cater perfectly to a huge variety of use cases and can be easily adjusted to meet the requirements of different business through small packaging and compositional changes.

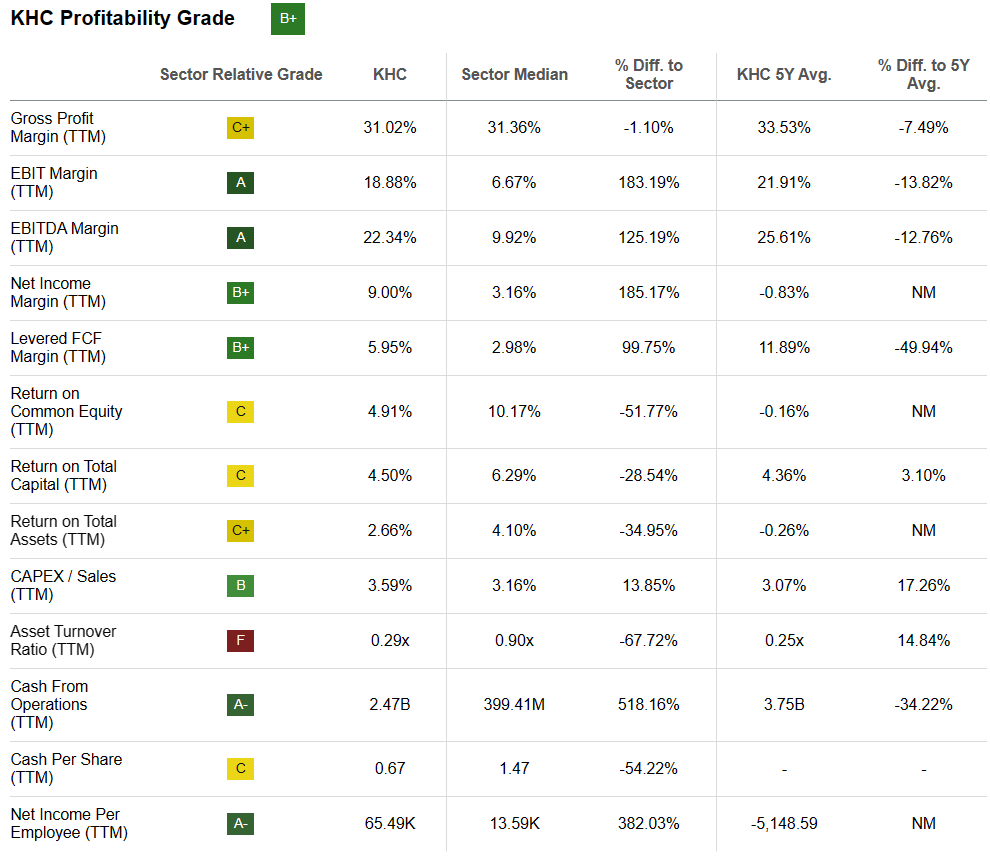

Seeking Alpha | KHC | Profitability

{kind=link}

Seeking Alpha’s Quant assigns KH with a “ B+ ” profitability rating. I believe this is the perfect snapshot and summary of KH’s current profitability.

Considering the firm’s balance sheet, KH looks relatively secure. The firm currently has a small current debt/equity imbalance with total current assets of $8.2B being slightly overshadowed by $8.95B in total current liabilities.

Nonetheless, their total debt/equity ratio is just 0.41 which illustrates that KH faces no fundamental liquidity issues.

{kind=link}

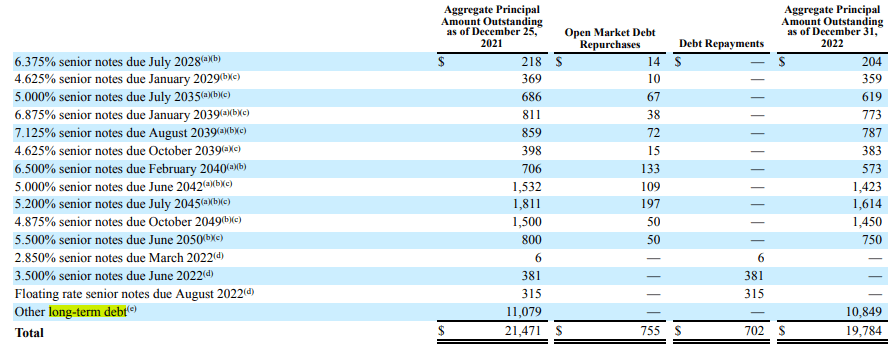

The firm’s material cash requirements for the financing of long-term debt, finance, operating and purchase obligations and leases amounts to $37.2B total.

In 2023 a sizeable $2.4B will be due along with $3.48B and $5.84B between 24-25 and 26-28 respectively. Given the firm’s cash flow from operations for the TTM is just $2.40B, it is very likely KH will have to utilize one of their revolving credit facilities to finance a portion of these debentures.

{kind=link}

Long-term debt is the primary source of cash obligations KH will have to meet. The majority of their debentures are financed with fixed-rate senior notes which protects the company quite well against any huge interest rate expenses.

This should allow FCF to remain reasonably healthy and not be bogged-down by excessive interest expenditure due to rapidly rising variable rates.

KH has obtained a BBB- credit rating from S&P along with a Baa3 rating from Moody’s. Both agencies believe the outlook is stable for KH.

KH has a quick ratio (current assets minus inventory divided by current liabilities) of 0.35x which supports my suspicions that KH will have to delve into more debt facilities in order to finance their short-term cash obligations.

Overall, I believe KH is a recovering firm that is on a solid path to operational excellence. However, their debt burden is relatively significant particularly in the short-term which could ultimately place some downward pressure on earnings and net income.

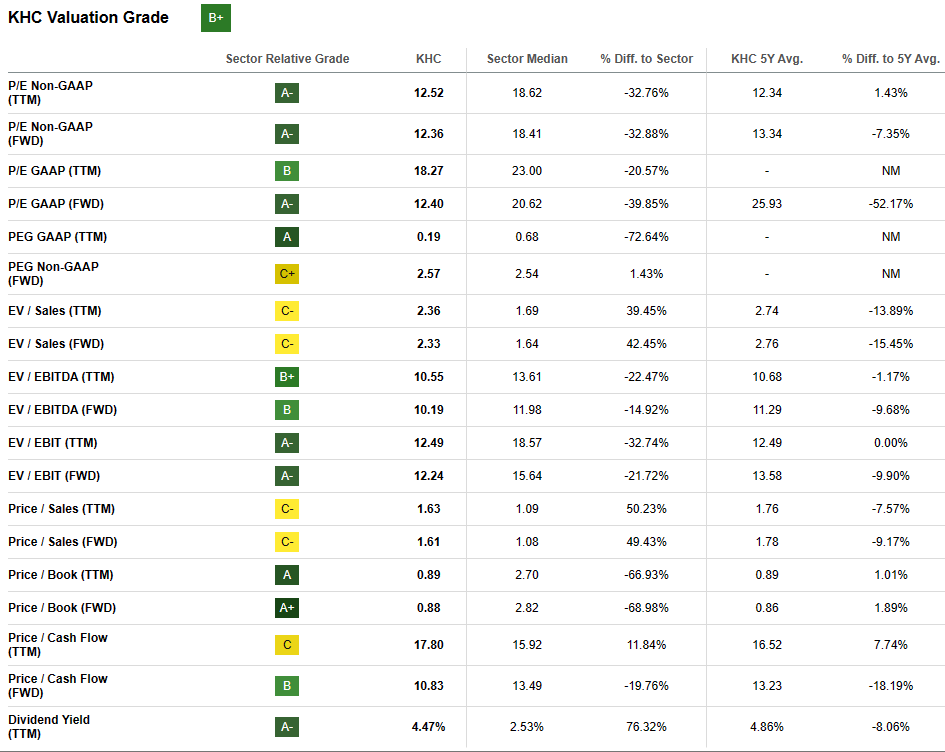

Valuation

Seeking Alpha | KHC | Valuation

{kind=link}

Seeking Alpha’s Quant assigns KH with a “ B+ ” Valuation rating. I believe this is a relatively accurate depiction of the value proposition currently present at KH.

The firm currently trades at a P/E GAAP FWD ratio of 12.40x along with a P/CF TTM of just 17.80x. Their FWD EV/EBITDA of 10.19x is okay especially when considering their EV/Sales TTM and FWD of 2.36x and 2.33x respectively.

These basic valuation metrics suggest KH is perhaps trading at a slight discount relative to their peers.

Seeking Alpha | KHC | Summary Chart

{kind=link}

From an absolute perspective, KH shares are trading pretty close to their historical lows. Shares have mostly flatlined over the past year with current prices of $35.90 last being seen in late 2022.

The Value Corner

By utilizing The Value Corner’s Intrinsic Valuation Calculation, one can better understand what value exists in the company from a more objective perspective.

Using KH’s current share price of $35.91, an estimated 2023 EPS of $2.90, a conservative “r” value of 0.06 (6%) and the current Moody’s Seasoned AAA Corporate Bond Yield ratio of 4.67%, I derive a base-case IV of $56.00. This represents a substantial 36% undervaluation in the firm.

When using a more pessimistic bear case CAGR value for r of 0.05 (5%), KH still appears to be undervalued by around 29% with an intrinsic value of $50.50 per share.

Therefore, I believe KH is soundly trading in deep-value territory and could potentially present a lucrative buy and hold play.

In the short term (3-7 months), I find it very difficult to say exactly what may happen to valuations. While the historic cyclical rises and falls in valuations could suggest an increase in prices is due, excessive uncertainty exists to say this for sure.

The firm’s short-term performance is also exposed to the general sentiment surrounding U.S. and global economic performance as a whole with a recession potentially leading to dropping share prices.

In the long-term (1-3 years), I see a brighter outlook for KH. Their position as one of the three big U.S. packaged foods producers looks set to provide the firm with a substantial economic moat to allow their turnaround strategies to be executed successfully. When combined with an intrinsic undervaluation in shares, I believe the potential for great shareholder returns is real.

Risks Facing KH

KH faces a few key risks associated with their business dynamics. Primarily these arise from changing consumer tastes and preferences hurting their portfolio performance along with excessively rising COGS in a highly inflationary environment.

The threat of consumer preferences changing in relation to packaged food requirements could see KH’s established name brands become less relevant in the eyes of consumers. This would hurt the pricing power KH holds in the markets which would result in falling margins, net sales and net incomes.

Equally, a scandal or one-off surprise event that tarnishes the reputation of one of their brands could lead to a significant reduction in sales figures which ultimately would hurt the company’s profitability.

Unfavorable macroeconomic conditions could also hurt KH’s profitability. Intense inflation or high interest rates could see KH’s margin contract and result in less than desirable fiscal performance. The repeat of a surprise event such as COVID-19 could significantly harm KH due to the large exposure of their revenues to the foodservice industry.

From an ESG perspective, KH faces a social risk which could arise from the aforementioned occurrence of a surprise food-safety event. Compromised public health through the sale of unsuitable food produce would be a serious situation for KH and could result in significant negative consumer sentiment.

Such a scenario could also lead to a serious governance issue which could result in fines or limitations being imposed on the firm.

Equally, KH must remain conscious of the usage of environmental resources throughout their supply chain network. The heavy reliance on carbon-emitting facilities and resources makes it difficult for the firm to achieve net-neutral emissions in the coming years.

Some argue that corporate food producers such as KH should be more responsible for the nutritional contents of their foods and the impact these factors have on the human body. Specific criticism has arisen against the National School Lunch Program inclusion of Lunchables which some argue are not a suitable choice for children’s diets.

While KH has some ESG concerns, I believe it would still be a relatively suitable choice for any ESG conscious investor. Of course, opinions may vary and I implore you to conduct your own ESG suitability research should this be of concern to you.

Summary

KH is a bit of a turnaround story in the making. Their mixed financial results post 2015 merger has left investors uncertain on the abilities of this global food giant. While their product portfolio is strong and operational efficiency is improving, the years of underperformance has tarnished investor sentiment towards the firm.

Nonetheless, an attractive intrinsic valuation presenting an almost 30% undervaluation in shares does make the stock seem quite attractive from this perspective. When combined with improving fundamentals, it does seem like KH has all the right ingredients to create a winning combination that outperforms the markets.

Therefore, I rate KH a “Strong Buy”. The firm’s material undervaluation along with a return to greater margins and profitability suggest market outperformance is on the horizon for KH.

For further details see:

Kraft Heinz: I Believe In Their Deep Value Turnaround Story