KHC - Kraft Heinz Stock: Forced To Be Content With A 4% Return

2023-04-27 14:55:33 ET

Summary

- Identifying a profitable investment opportunity is more challenging than identifying an undervalued company.

- Kraft Heinz has been undervalued for a few years now, and for reasons discussed in this analysis, I believe a major change is unlikely this year too.

- There are several promising developments that suggest the company is headed in the right direction.

- I believe investors should look for a key earnings catalyst before doubling down on Kraft Heinz stock at these prices.

Ever since Miguel Patricio took over the helm at The Kraft Heinz Company ( KHC ), I have been bullish on the prospects for the company. As I discussed in my previous article in January, the company has executed the new CEO's vision commendably over the last four years, but unfortunately, its stock price has little to show. Kraft Heinz stock has gone nowhere since the CEO transition, and the $40 mark has proven to be a major barrier. The company is heading in the right direction from a business strategy perspective, but I believe Mr. Market will not reward this positive development for some time to come. The quarterly dividend, which was cut to 40 cents from 63 cents per share in 2019, now yields just over 4%, and I believe investors will have to accept this meager return in this high inflationary environment this year before we see the emergence of a catalyst that could drive the stock price higher.

The Improved Business Strategy

In recent times, "cost-cutting measures" has become a catchphrase that grabs the attention of investors. Companies that implemented cost-saving measures over the last 12 months immediately saw a positive response from Mr. Market, and an increasingly higher number of companies are resorting to cost-cutting measures to drive profitability amid inflationary pressures. Although there is nothing wrong with a company wanting to improve its efficiency by managing its cost structure better, I always approach cost-cutting strategies cautiously as I am wary of investing in companies that prioritize cost reductions over investing for growth. Kraft Heinz's disappointing performance from 2016 (revenue was flat between 2016 and 2022) also stemmed from an overemphasis on cost-cutting.

Today, Kraft Heinz has a better strategy in place, under the guidance of Miguel Patricio. Rather than cutting costs to unsustainably inflate profits, the company is now focused on saving money to boost its marketing and R&D budgets. This is a positive development from a few years ago, when the company shot itself in the foot by slashing its marketing budget, paving the way for competitors to gain market share due to a loss in the company's brand value. Since 2019, Kraft Heinz has incurred $498 million in R&D expenses in comparison to $427 million in the four years leading up to Miguel Patricio's appointment. This increase in R&D expenses is better than it seems because the company had to deal with a global pandemic, supply-chain challenges, and high inflationary pressures amid a business transformation. These investments were partly funded by the cost savings in other divisions. Kraft Heinz had the perfect excuse in the form of macroeconomic challenges had it wanted to curb R&D, but it didn't, which is a clear indication that the company is prioritizing long-term growth over short-term profitability under the new CEO. As a growth-oriented investor, I consider this to be a very positive development.

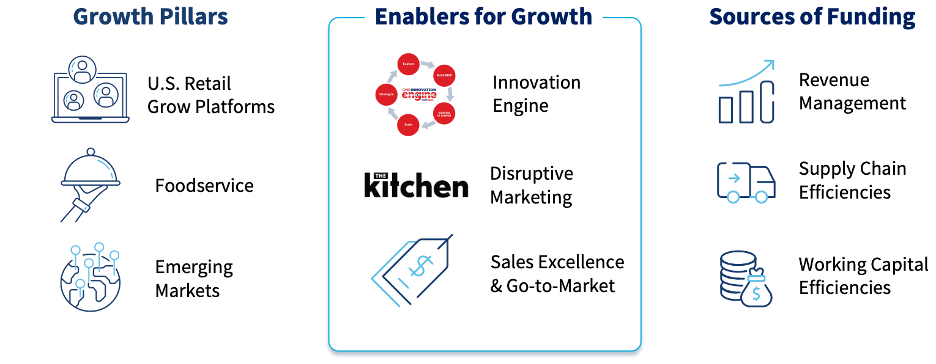

It is also important to note that the increase in R&D expenses over the last four years did not happen by chance. The company, back in 2019, laid out a plan to save costs to internally fund organic growth. At the CAGNY 2023 conference a couple of months ago, Kraft Heinz highlighted this strategy yet again, as illustrated below.

Exhibit 1: Kraft Heinz's growth strategy

{kind=link}

It is easy to come out with an eye-catching business transformation plan but not so much when it comes to executing the plan. Investors who are looking for turnaround opportunities, in my opinion, should pick companies that are led by leaders with a strong track record of executing strategic plans while enacting shareholder-friendly corporate governance policies. The fact that Kraft Heinz has made steady progress since 2019 with an unwavering focus on executing its original transformation plan while managing several macroeconomic headwinds is a testament to the changing corporate culture.

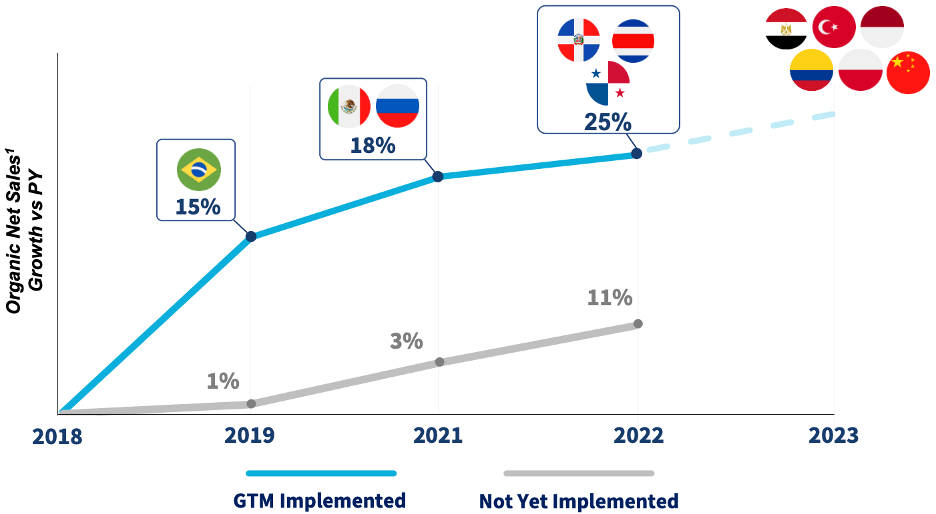

During a business transformation phase, some companies focus more on achieving operational efficiencies in their core markets and less on expanding outside of their core markets to achieve long-term growth. This is a pitfall that needs to be avoided to ensure the long-term sustainability of earnings growth. Kraft Heinz has successfully avoided this pitfall by appointing new executives solely focused on penetrating new markets. For example, the company appointed Cristina Kenz as the Chief International Growth Officer in June 2020 to focus on the massive expansion opportunity in emerging markets. Before joining Kraft Heinz, she served as General Manager (Marketing) at Danone S.A. ( DANOY ) and as Global Marketing Officer at PepsiCo, Inc. ( PEP ). Amid the ongoing business transformation, Kraft Heinz has achieved commendable organic growth in many of its key international markets where its new growth model has been rolled out.

Exhibit 2: Organic net sales growth in emerging markets

{kind=link}

The company plans to implement its new model in 90% of emerging markets by the end of this year, which should pave the way for greater organic growth in the years ahead. More than the organic growth that we saw in the last few years, I am impressed by the company not backing out of growth opportunities during a challenging, transformative time period.

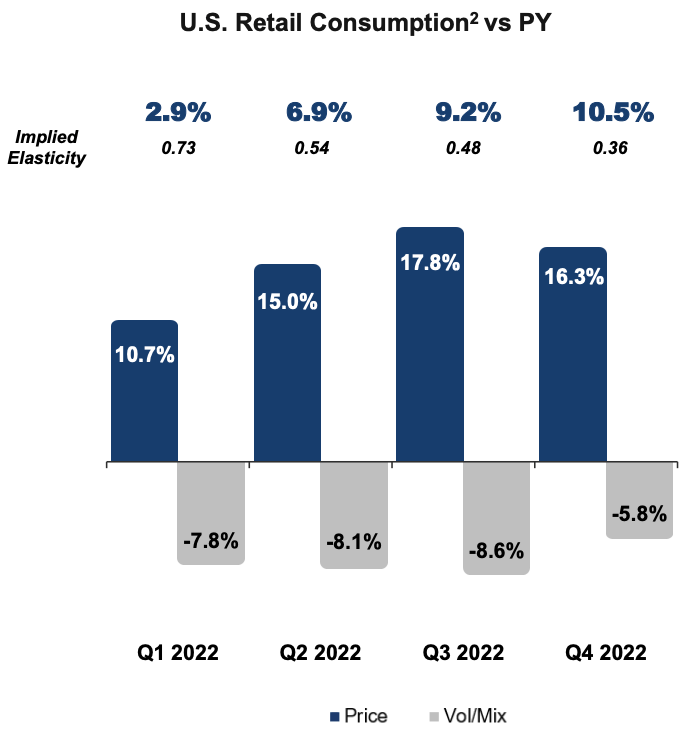

Kraft Heinz was able to pass on some of the cost headwinds to its consumers last year, offsetting some impact from volume declines. This is another encouraging sign which establishes the brand equity of the company. With a refreshed, more focused go-to-market strategy, Kraft Heinz has been able to reverse the damage to its brand value caused by questionable cost-cutting measures in the past.

Exhibit 3: U.S. retail consumption statistics

{kind=link}

Kraft Heinz, with a renewed focus on growth, has done the hard yards to create a platform from which the company launch into the future in the coming years.

A Catalyst Will Take Time To Form

It might be easy to identify an undervalued company, but identifying a profitable investment opportunity is not as easy. Kraft Heinz might have to wait patiently for a rebound in economic growth and a more stable inflationary environment to reap the rewards of the transformative decisions that were taken over the last four years. In 2023, the company expects the adjusted EPS to decline from $2.78 to between $2.67 and $2.75. Some of this negative impact will come from the inclusion of 53rd-week numbers in 2022. The company also expects to take a hit from adverse foreign exchange movements and non-cash post-retirement benefits.

At Leads From Gurus, we look for earnings-based catalysts such as positive earnings revisions and a strong track record of positive earnings surprises. With inflation easing up, supply chain conditions improving, and profit margins trending in the right direction, I believe Kraft Heinz has set itself up to exceed its guidance for earnings this year. This is a positive development, but for the stock price to edge higher from here, a notable increase in the consensus EPS estimate for 2023 will be required. In the last three months, Wall Street analysts have lowered their EPS estimate for 2023 11 times against just four positive revisions. Because we believe there is a strong correlation between long-term stock prices and positive earnings revisions, we believe Kraft Heinz stock will trade sideways in the foreseeable future.

Takeaway

Kraft Heinz continues to be cheaply valued in the market, but in the absence of a key earnings catalyst, the company is likely to remain undervalued through the end of this year. Investors, unfortunately, will have to be content with the 4%-yielding dividend for the time being. The company has set itself up for long-term success, and I believe attractive returns are on the cards for long-term-oriented investors. I remain bullish on the prospects for Kraft Heinz, but I do not plan to add to my long position at these prices as I believe KHC will not beat the market this year.

For further details see:

Kraft Heinz Stock: Forced To Be Content With A 4% Return