KHC - Kraft Heinz: Stock Set To Hit Low P/E Screeners With Improved GAAP Numbers

2024-01-03 13:58:02 ET

Summary

- Kraft Heinz is working to reduce debt and improve margins after accounting errors and a large impairment caused a drop in stock value.

- GAAP profitability is improving, with a current GAAP P/E ratio below the market average.

- Warren Buffett's Berkshire Hathaway seems confident in Kraft Heinz, holding the highest ownership percentage and waiting for the turnaround.

- With funds/institutions rebalancing from the Fab 7 to value, many low P/E, and high dividend payers could be popular targets.

- If inflation recedes, you could see a lot of earnings beats and nice dividend increases in the consumer staples sector.

GAAP is back

As we roll into 2024, this is a continuation of the series of articles that I have been writing on The Kraft Heinz Company ( KHC ) which can be found here and here . The company is still a buy. The main items that have changed since my last article are the better GAAP profitability numbers and the turn from cost cutting to organic spending.

Since Berkshire Hathaway Inc. ( BRK.B ) and 3G Capital merged the two companies into one, creating a lot of debt on the newly merged company, the goal has always been to reduce debt and then improve margins. in 2018, accounting errors related to assets resulted in a large impairment. The stock dropped on the order of 60% give or take and here we still sit today. I followed Warren Buffett into this one and have been accumulating. My stubbornness may be ready to pay off.

In this article, I intend to take a deeper look at the debt paydown and turnaround situation. The company is now through most of its write-offs and GAAP profitability is apparent and improving. I believe that most funds and institutions don't look under the hood, they allocate funds based on GAAP screeners and algorithms to see what presents the best opportunities to cash in on the "2 and 20 model" annually [not quite as lucrative anymore, but I'm just emphasizing a point].

If we look at the GAAP and non-GAAP metrics, in addition to the first chart showing a steady 11 X EBITDA/EV multiple, the earnings never went anywhere, they were just hidden beneath the surface. In all honesty, the impairments allowed Kraft Heinz to avoid a lot of income taxes in the interim while the company reduced long-term debt from nearly $30 Billion in 2016 to just under $20 Billion currently.

Was the impairment truly a necessary step? Either way, it certainly assisted in debt reduction:

{kind=link}

The staggering $15.4 billion impairment charge, made up of a $7.1 billion goodwill impairment in US Refrigerated and Canada Retail unit and $8.3 billion related to Kraft and Oscar Mayer intangible assets impairment, drove the company to report a $12.6 billion loss after taxes.

The Kraft Heinz impairment charge was the seventh largest since 2009.

Now that we have a stock in the GAAP earnings range that is below the market average, it's sure to hit multiple screeners of funds and institutions that have a charter that the fund is to hold certain stocks based on certain GAAP earnings multiples. If this comes true, coupled with what could be a highly deflationary year for packaged foods producers, then this investment may finally pay off.

Warren Buffett still hasn't sold a share

{kind=link}

| STOCK |

| OWNERSHIP PERCENTAGE |

| (AAPL ) |

| 5.61% |

| (BAC ) |

| 12.81% |

| (AXP ) |

| 20.02% |

| (KO ) |

| 9.23% |

| ( CVX ) |

| 5.66% |

| (OXY ) |

| 24.34% |

| (KHC ) |

| 26.58% |

Looking at Berkshire Hathaway's top 7 holdings, Kraft Heinz is the company's highest ownership percentage, even exceeding Occidental Petroleum which the company continues to add to regularly. Since the merger of Kraft and Heinz, Berkshire Hathaway has not sold a share, waiting patiently for the turnaround despite the price cratering.

Gregory Abel, the chairman of Berkshire Hathaway sits on the board, giving Berkshire ample influence over the company's operations. I believe this is a company that Berkshire Hathaway has a lot of confidence in regarding the turnaround. They are showing conviction with the steady holding as evidenced in their 13 F filings.

Percent off high

This has been one of my biggest laggards, yet the largest position over the last 5 years, just collecting the dividend and adding along the way. There are not many packaged food, consumer staple stocks thrashed this hard in the market. This is also one of the cheapest on a price-to-book basis. Will this be the year the stock finally breaks out? Indicators are looking positive with the reduction of long-term debt by a third over the past 5 years. Buybacks will finally begin. Unfreezing the dividend payment would be a really big catalyst.

Is 2024 the year of deflation?

The Fed has finally signaled a rate top and possible rate cuts coming as early as March 2024. As many commodities are purchased with futures contracts, the effect of deflation will lag in the cost of goods sold portion of a heavy commodity user income statement until the current contracts are worked through. Anticipating that the cost of goods will drop later this year for many packaged foods producers is a popular outlook in 2024.

Buybacks equal stabilization

Without a stable balance sheet and more predictable future cash flows, CEO Miguel Patricio would not have approved a buyback plan in my opinion.

PITTSBURGH & CHICAGO--[BUSINESS WIRE]--Nov. 27, 2023-- The Kraft Heinz Company [Nasdaq: KHC] ["Kraft Heinz" or the "Company"] today announced that the Board of Directors approved a share repurchase program authorizing the Company to repurchase up to $3 billion of the Company's outstanding shares of common stock through December 26, 2026.

Under the share repurchase program, the Company intends to repurchase shares with excess cash after allocations for disciplined capital spending, including investments to support organic growth in key areas of its business, payment of an attractive dividend, maintaining a targeted Net Leverage 1 of approximately 3.0x, and evaluation of strategic opportunities, including acquisitions, divestitures, and partnerships.

"In the third quarter, we hit a milestone in our transformation - reaching our targeted Net Leverage 1 of approximately 3.0x. A stronger balance sheet, along with advancements we have made across the business, gives us further conviction behind our strategy and the belief that company shares are an attractive investment opportunity," said Kraft Heinz CEO and Chair of the Board Miguel Patricio.

If we use an unadjusted long-term debt-to-EBITDA ratio, the company now sits at around 3.5 X

{kind=link}

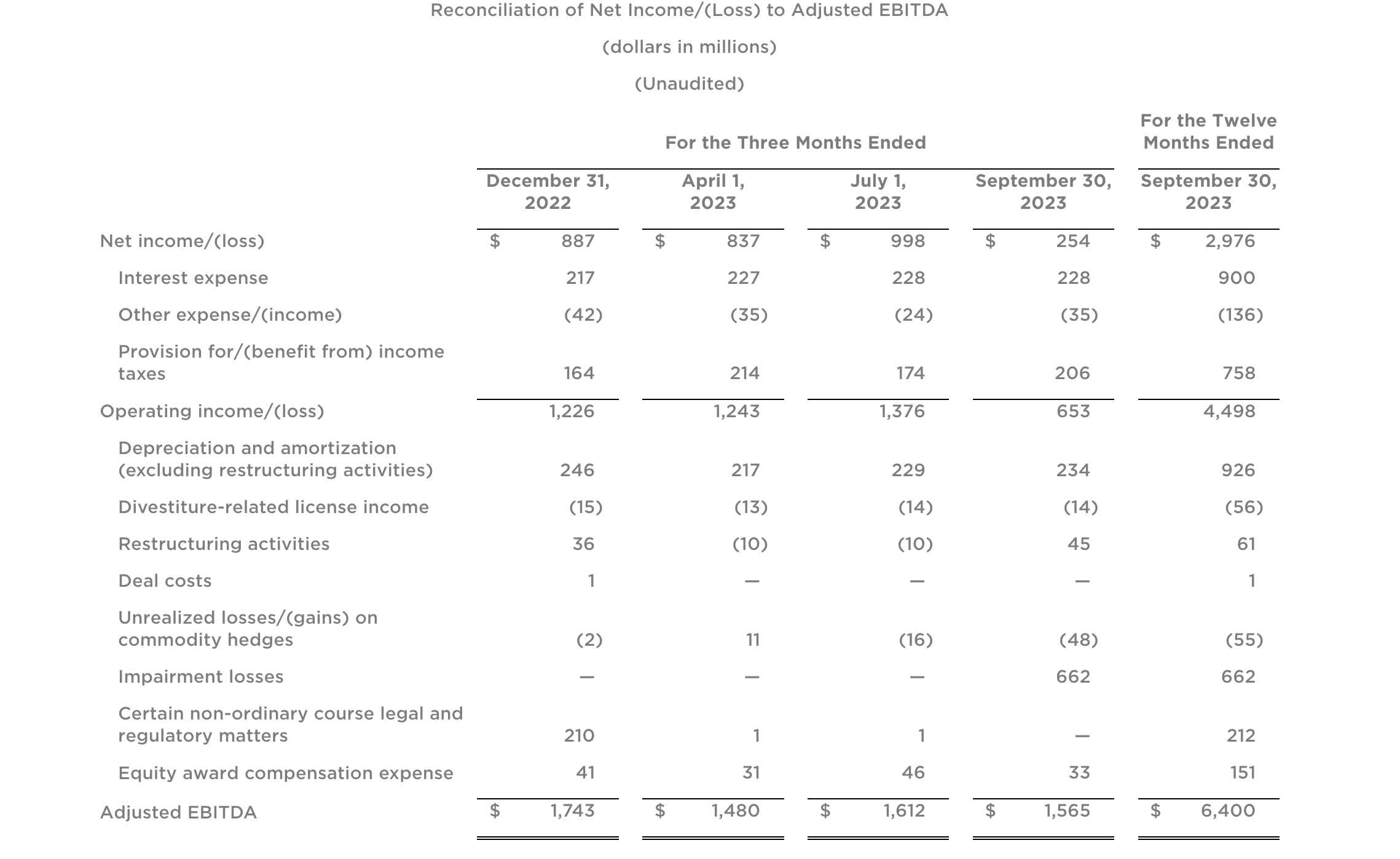

Looking at Kraft Heinz's adjusted EBITDA numbers from TTM, the amount sits at $6.4 Billion.

Adjusted EBITDA is defined as net income/(loss) from continuing operations before interest expense, other expense/(income), provision for/(benefit from) income taxes, and depreciation and amortization (excluding restructuring activities); in addition to these adjustments, the Company excludes, when they occur, the impacts of divestiture-related license income, restructuring activities, deal costs, unrealized losses/(gains) on commodity hedges, impairment losses, certain non-ordinary course legal and regulatory matters, and equity award compensation expense (excluding restructuring activities).

Looking at net leverage, defined as :

- Long-term debt = $19.270 Billion.

- Minus $1.052 cash and cash equivalents.

- Equals $18.826 Billion net leverage.

Therefore the net leverage ratio according to Kraft Heinz estimates sits at $18.826 Billion/$6.4 Billion = 2.94 X net leverage ratio. Looking good.

Most recent quarter analysis

Before looking at some of the most recent quarter numbers in greater detail, we can see that revenue has now stabilized and begun to tick back up. The growth is welcome and should only continue now that debt reduction goals have been met.

irkraftheinzcompany.com Q3 presentation

{kind=link}

Net leverage, as touched on earlier in the article is the key to unlocking initiatives 1 and 2. Now that the company can slow down on debt repayment, it can begin to reinvest in the business and focus on organic growth.

Versus 2022

ir.kraftheinzcompany.com Q3 results

{kind=link}

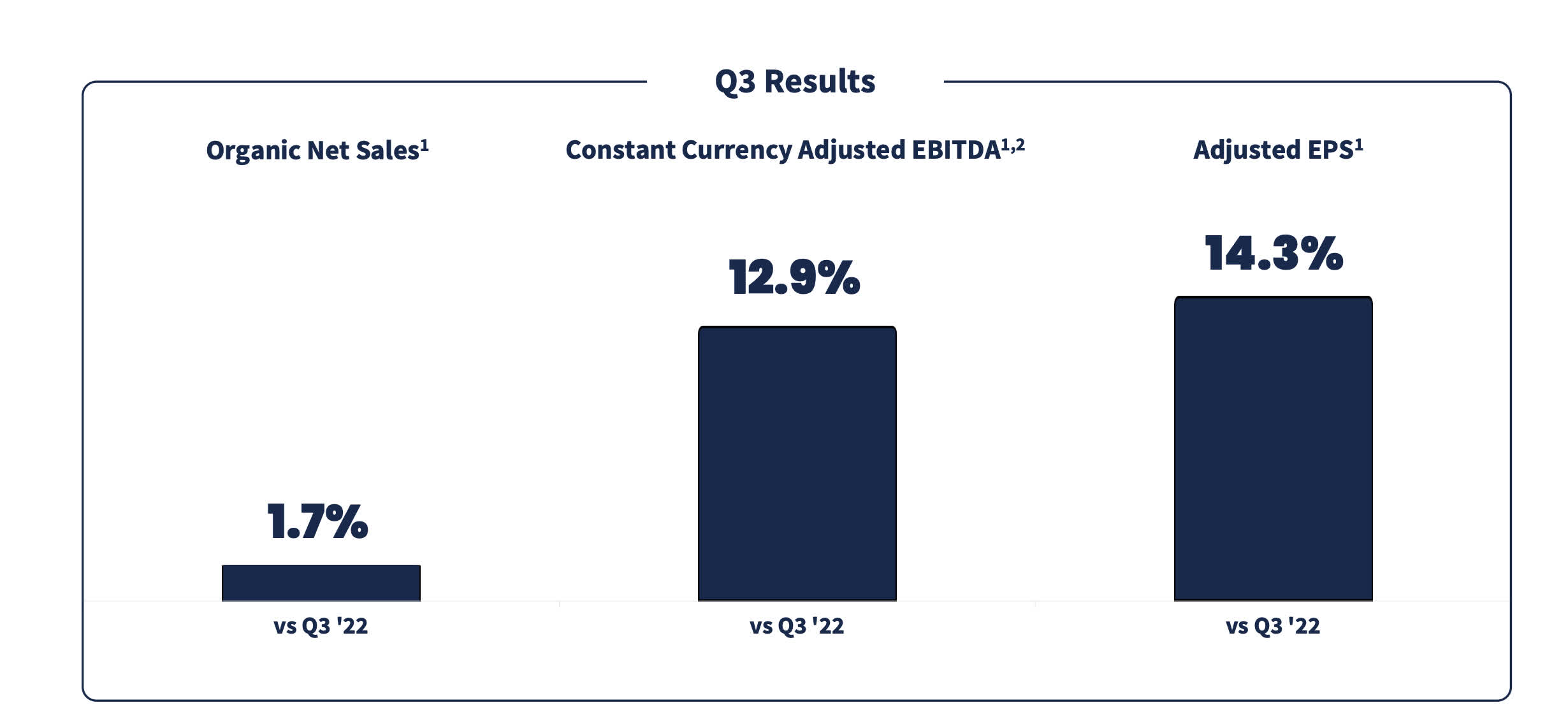

Looking at the numbers on adjusted EBITDA and earnings growth quarter over quarter, we see now that the company is consistently trending positive. This emergence from divestitures, right-sizing, and write-offs to growth and re-investment is the beginning of the company turning the corner.

For those paying attention to EBITDA and adjusted EBITDA, the earnings have always been there. Now the stock will also hit PEG screeners as having an ultra-low PEG ratio even though it's more of a transition period than it is true earnings growth. Either way, the current situation is more healthy and more optimistic.

Organic growth

ir.kraftheinzcompany.com Q3 results

{kind=link}

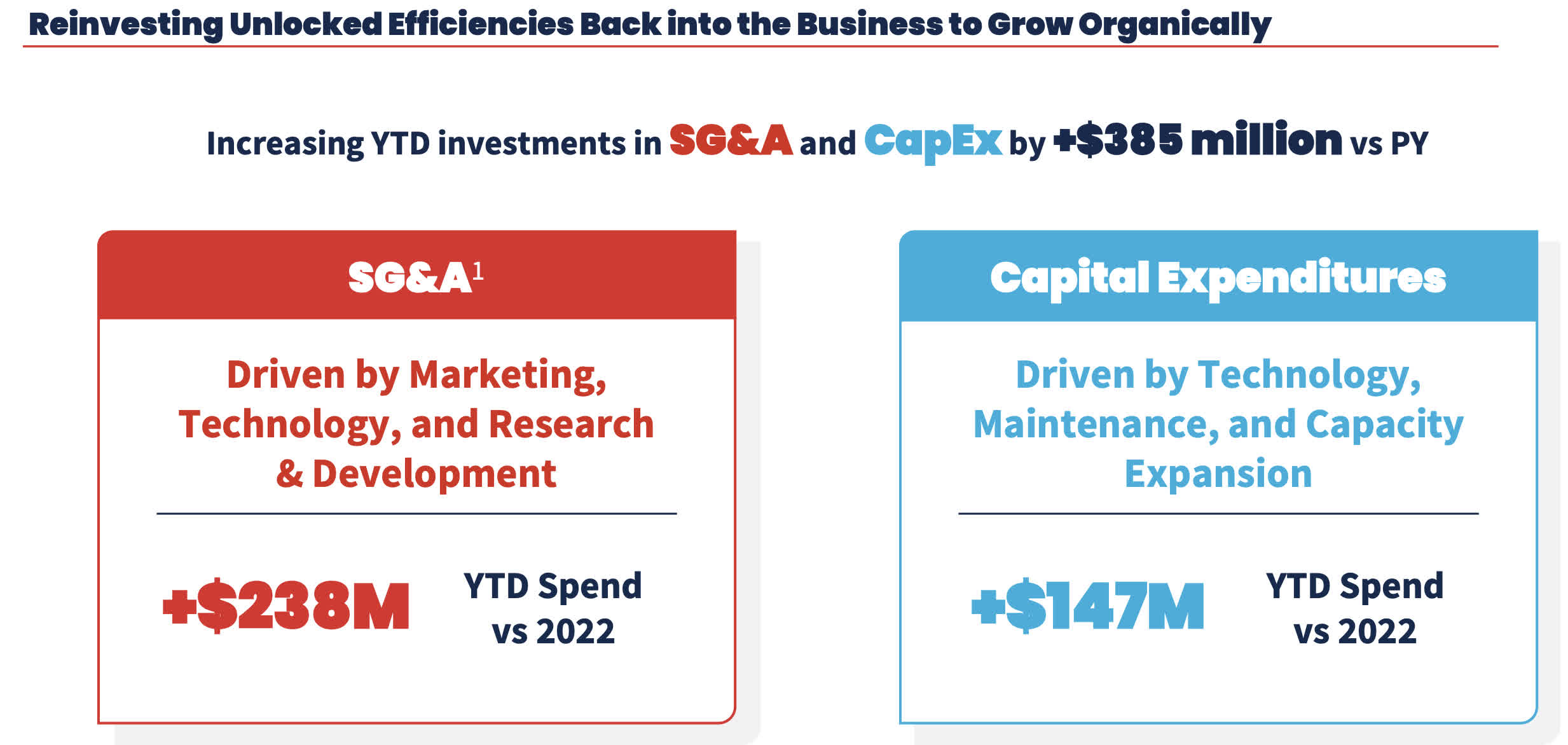

The above all culminated in an increase of USD $385 million in company reinvestment. This is allocated as $238 million to SG&A and a $147 million increase to CAPEX. CEO Miguel Patricio and 3G had the reputation of cost butchers before the merger and during the early stages. Now that the company is stabilizing, it can actually add employees and reinvest in operations.

Balance sheet deep dive

Long-term debt

Graphing the trajectory of long-term debt, we can see that Kraft Heinz really got out the shovel post the 2018 impairment charge, reducing post-merger debt by 1/3rd.

EBIT to net interest coverage

EBIT to net interest expense coverage ratio is now equivalent to 5.13 X. With analysts and credit rating agencies using this as a key factor in assessing a company's ability to service interest payments, 2 X is the minimum acceptable ratio. At 5+ X and significant equity interest from cash-rich Berkshire Hathaway, this is one of the last company debt situations I worry about even though the debt levels are still quite high.

The next debt maturity seems to be coming in May 2024 to the tune of 550 million Euros, or about $601.7 million.

Predicting about $3 billion in free cash flow in 2024 and a forward dividend payment of USD $1.963 Billion, should leave an extra $ 1.03 Billion on the table for buybacks and reinvestment.

A frozen dividend set to grow

The next shoe to drop by year's end will hopefully be an increase in the dividend per share. It has been frozen since the impairment. Consumer defensive, staples, and industrials are typically predictable dividend growers. Once the cash flow and balance sheet are under control, there should be no reason why Kraft Heinz can't be a consistent dividend grower from here on out.

Valuation

Below is the "Buffett Owner Earnings" analysis of fair value based on 2023 numbers and then adjusted for analyst 2024 estimates, with analysts bumping up earnings by at least 2%.

| 2023 |

| net income |

| 2988 |

| plus depreciation and amortization |

| 958 |

| minus capex |

| 1063 |

| discounted at risk-free rate 5.5%= fair market cap |

| 52418 |

| divided by shares outstanding [1226 million] |

| 42.75 |

Trading at 88% fair value to 2023 GAAP earnings

| 2024 |

| net income |

| 3047.76 |

| plus depreciation and amortization |

| 958 |

| minus capex |

| 1063 |

| discounted at risk-free rate 5.5%= fair market cap |

| 53504 |

| divided by shares outstanding [1226 million] |

| 43.64 |

While I previously looked at Kraft Heinz using the Graham Number and an adjusted EBITDA per share basis being that the company was undergoing write-offs and debt reduction, now we can begin to look at the company on a simple GAAP earnings basis. The stock is slightly undervalued using a 5.5% risk-free rate and a Warren Buffett "Owner Earnings" discount model. Using 2024 earnings has a fair price of around $43.64/share. But with rates possibly falling, cuts will expand multiples.

Risks

Inflation stays sticky. We'll know by the rate cuts what the Fed sees in the data. If March is a non-cut, then we can't be clear about the future of inflation for this sector. Consumer staples are some of the most affected by inflation as they can only pass so much of the cost of goods sold to the consumer.

{kind=link}

Gross margins on a TTM basis are improving, but have a ways to go to hit the numbers of 2016. Watching gross margins quarter by quarter in the consumer staple names will tell us exactly which way inflation is going. Don't forget, if the cost of goods sold drops 20% but the company only cuts prices by 10% or less, then inflation has done more good than harm to the company from a long-term perspective.

Summary

In light of deflation predictions, possible rate cuts, and funds/institutions rebalancing from the Fab 7 to value, many low P/E, and high dividend payers could be popular targets. Kraft Heinz has been a dog if you've been in it for 5 years or more. This could be the year to get in. Not just Kraft Heinz but several consumer staple stocks. If inflation recedes, you could see a lot of earnings beats and nice dividend increases in this sector. Buy.

For further details see:

Kraft Heinz: Stock Set To Hit Low P/E Screeners With Improved GAAP Numbers