KHC - Kraft Heinz: The End Of The Turnaround Story

2023-10-10 07:05:40 ET

Summary

- Kraft Heinz's turnaround plan has failed to meet expectations, with the stock continuing to perform poorly relative to peers.

- The declining gross margin is a cause of concern as brand pricing power is one of the most important competitive advantages in the sector.

- Free Cash Flow headwinds are also limiting the potential upside going forward.

After years of high hopes, Kraft Heinz's (KHC) turnaround plan seems to have failed to live up to the expectations. For the past 3 years (since I first covered the stock), KHC share price has delivered returns at par with the Consumer Staples Select Sector SPDR® Fund ETF ( XLP ), even though the stock has lost nearly two-thirds of its value in the 2017-19 period.

But even if we ignore the events from 2017-19 time frame, KHC stock has become extremely volatile when compared to other high quality consumer staple businesses. We could see this in the graph above, where KHC has deviated massively from the XLP over the past 3 years, just to end up in the same place as the sector ETF.

Nonetheless, KHC's global footprint and its iconic brand portfolio have been enough of a reason for many value investors to consider the stock as a very cheap alternative to the high quality names in the space.

Seeking Alpha

As it became obvious 3-years later, this has been a mistake and I am still of the opinion that Kraft Heinz has little to offer in terms of expected shareholder returns.

Stalling Turnaround

As Kraft Heinz share price stabilized post the disastrous 2017-19 period, the company has embraced a new strategy, oriented towards its iconic brands and product segments where the company has strong competitive advantages and room for growth.

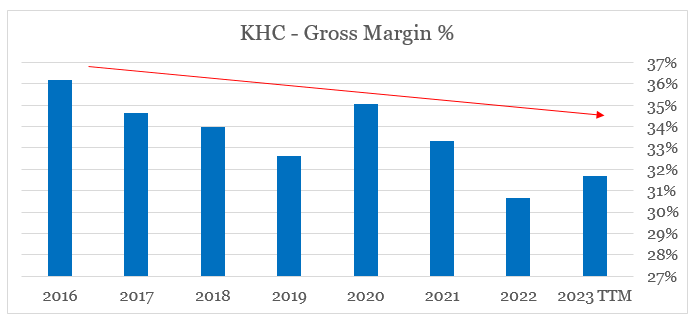

In this process, the management has been busy optimizing its portfolio which naturally leads to higher profitability. In this case, however, Kraft Heinz gross margin has been steadily declining.

prepared by the author, using data from SEC Filings

{kind=link}

The reason why I am laser focused on gross margins when it comes to fast-moving consumer goods (FMCG) business is because it is the best proxy for the price premium achieved through branding.

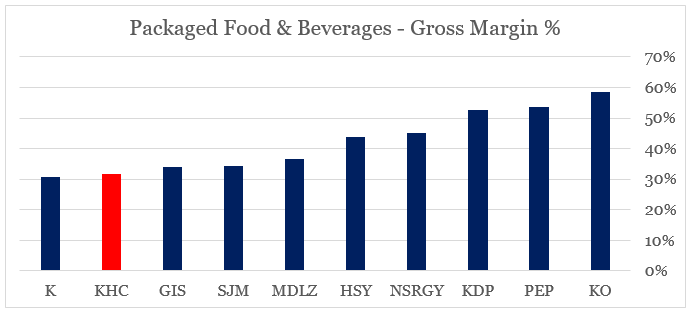

This notable decline in gross margins is partially explained by the recent inflationary pressures, which have been a headwind for profitability for companies in the sector. In the case of Kraft Heinz, however, this has now led the company to become one of the lowest gross margin producers in the expanded peer group we see below.

prepared by the author, using data from Seeking Alpha

{kind=link}

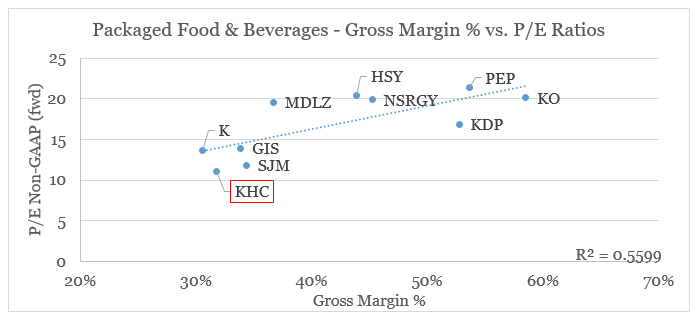

Usually, a company in this situation will focus on achieving higher asset turnover in its effort to retain high return on capital. But this is easier said than done and as a company with global footprint and very wide product portfolio, KHC has very limited ability to offset its margin declines with higher asset turnover.

That is why, on a cross-sectional basis within the sector, gross margin still exhibits a very strong relationship with Price-to-Earnings multiples and KHC is at the bottom left-hand corner.

prepared by the author, using data from Seeking Alpha

{kind=link}

Mixed Performance

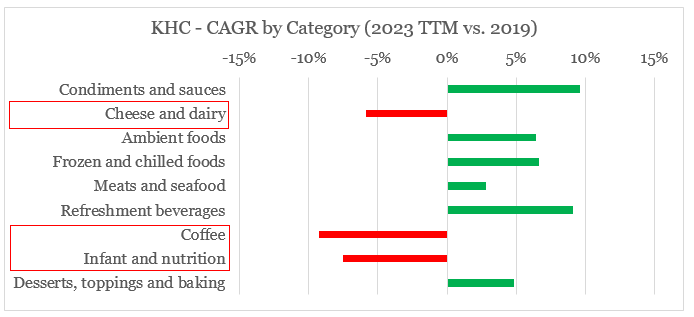

Although some areas of Kraft Heinz brand portfolio have been growing in recent years, the overall performance is mixed. Cheese and diary, Coffee and Infant and nutrition segments, for example, noted significant declines on an annual basis since 2019. Indeed, recent divestments, such as the sale of the company's Natural Cheese Business, have played a major role in these declines, but at the same time KHC has been very active in the acquisitions front as well.

Condiments & sauces and refreshment beverages have been the key areas of focus for Kraft Heinz management, but revenue increases in these areas were hardly enough to offset the declines.

prepared by the author, using data from SEC Filings

{kind=link}

* CAGR - Cumulative Annual Growth Rate

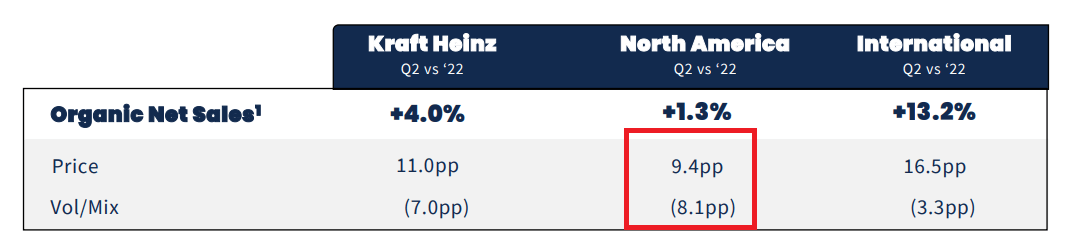

For a company that has been heavily involved in divestments of non-core assets and very active on the M&A front, one would expect that KHC would have significant pricing power. Unfortunately, this does not appear to be the case as recent price increases in North America are already leading to massive drop in volumes and deterioration in the price mix.

Kraft Heinz Investor Presentation

{kind=link}

This is a very recent event for KHC as the company did not experience the same drop in volumes during 2022, when pricing measures were initially implemented.

Kraft Heinz Investor Presentation

{kind=link}

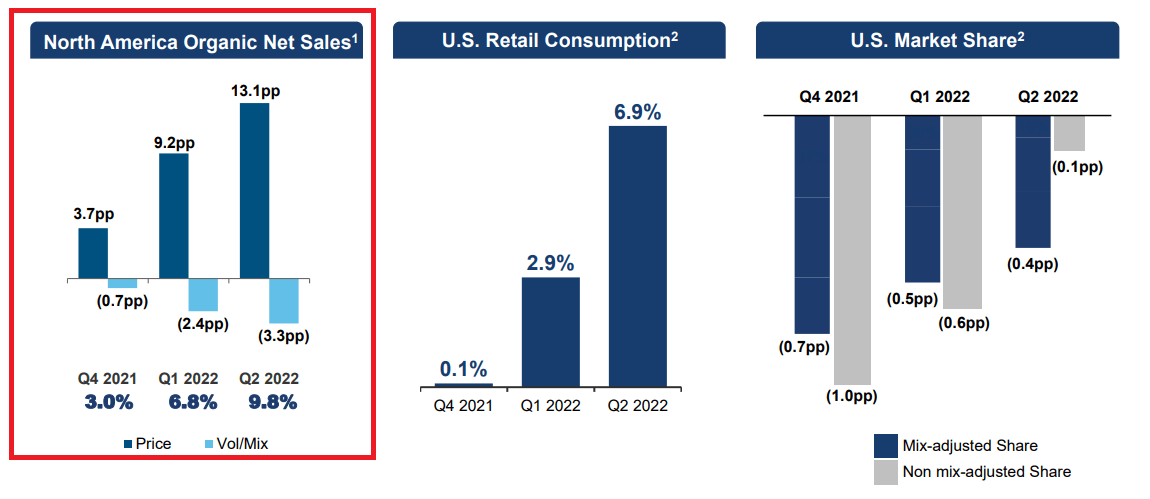

Naturally, this brought some investors' optimism, but the excitement is now quickly fading as volume declines become a reality.

Yes, we lost share in the second quarter , but this was a headwind we expected, as we priced above the market. Here's the good news - the pricing is done - and even with elevated price gaps, we aren't losing incremental share to private label.

Source: KHC Earnings Transcript Q2 2023

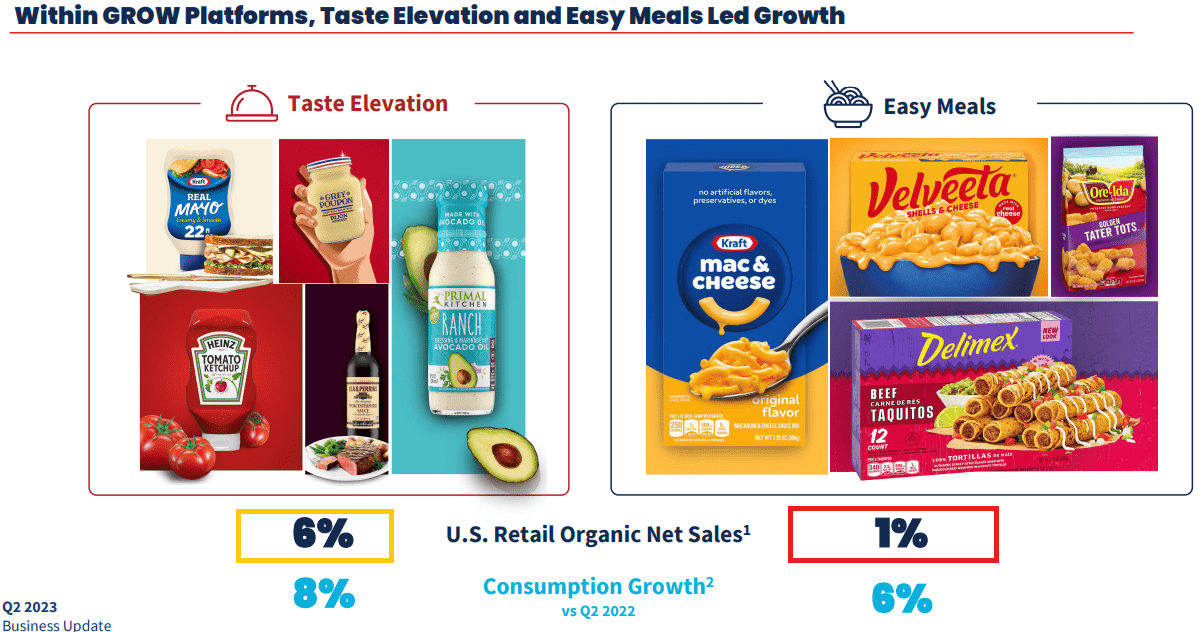

On a segmented basis, taste elevation and easy meals were the key growth areas during the latest quarter with organic net sales of the latter being only 1%.

Kraft Heinz Investor Presentation

{kind=link}

The impressive 6% growth in the taste elevation segment also came as a result of Kraft Heinz recent M&A deals, which were aimed at reinvigorating growth.

Kraft Heinz Investor Presentation

Overall, Kraft Heinz portfolio offers little room for further price increases as volumes are already suffering and even though some product segments are showing signs of recovery, performance of the overall brand portfolio would likely remain challenged.

The Cash Flow Perspective

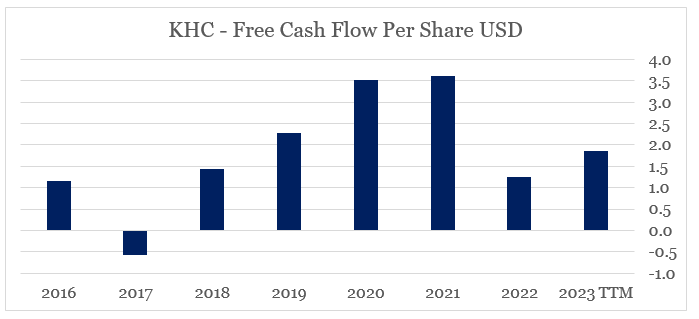

Kraft Heinz's free cash flow per share dynamic we see in the graph below does not correspond with stability that one would expect from a high quality FMCG business.

prepared by the author, using data from SEC Filings

{kind=link}

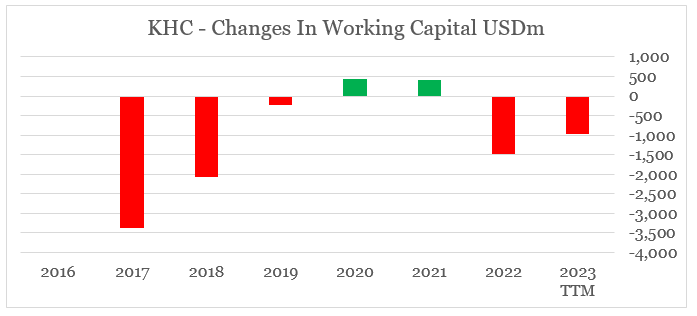

During the 2020-21 period, KHC experienced significant pandemic tailwinds from the unprecedented demand of its products. On top of the higher margins we saw above, the company was also able to significantly reduce its working capital requirements and thus record a temporarily higher free cash flow.

As we see in the graph below, however, this trend has already reversed in 2022 and changes in working capital would likely be a headwind in 2023 as well.

prepared by the author, using data from SEC Filings

{kind=link}

Usually, this is not a bad thing as higher working capital requirements are associated with higher revenue growth, but in the case of KHC this is not the case.

prepared by the author, using data from SEC Filings

{kind=link}

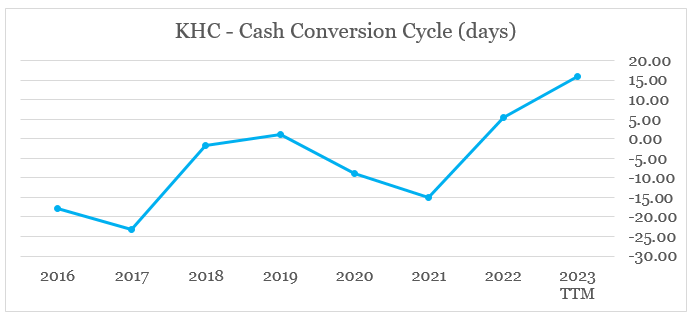

The company's cash conversion cycle has deteriorated significantly in 2022 and so far in 2023 as both Days Sales Outstanding and Days inventory Outstanding increased significantly.

prepared by the author, using data from SEC Filings

{kind=link}

This is surprising given the recent portfolio optimization which should have led to lower inventory turnover and not the opposite.

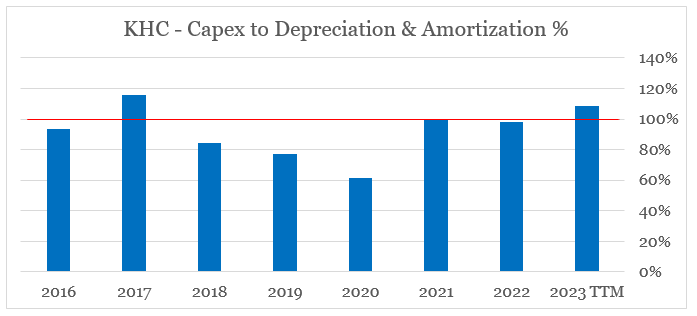

The last tailwind for Kraft Heinz Free Cash Flow that is no longer there is the company's reduced capital expenditure. Although the annual amortization of acquired intangibles is skewing the Capex to Depreciation & Amortization Expense ratio we see below, KHC is now forced to spend significantly higher amounts on Capex which puts further pressure on Free Cash Flow.

prepared by the author, using data from SEC Filings

{kind=link}

The same holds true for Advertising Expenses, which could ultimately be beneficial for the brand portfolio, if done properly.

Management seems to be making a step in the right direction with its intention to increase advertising spend and capital expenditures.

Source: Seeking Alpha

Any positive impact from this higher spending, however, would likely take years to provide any meaningful impact on profitability and growth.

Conclusion

After years of poor shareholder returns and significant share price volatility, Kraft Heinz is in not in a good position to outperform the sector. The bloated brand portfolio is still causing problems and the company is slowly becoming a low margin producer. Free Cash Flow tailwinds are also fading and this will bring more downward pressure for the share price, even if margins stabilize in the coming year.

For further details see:

Kraft Heinz: The End Of The Turnaround Story