HRL - Kraft Heinz: The Intrinsic Value Of Owner Earnings

2023-05-16 19:06:05 ET

Summary

- Buffett has significant paper losses since Kraft Heinz first hit Berkshire's 13F, but it appears he still sticks to the thesis.

- This article breaks down the Kraft Heinz investment thesis, using Warren Buffett's "Owner Earnings" calculation of intrinsic value.

- This article references Robert Hagstrom's Book, The Warren Buffett Way, Buffett personally congratulated Hagstrom on the accuracy of his analysis on his own thought processes.

- Considering the undervaluing of the assets, I would still consider Kraft Heinz to be the cheapest in the packaged foods segment.

- Robert Hagstrom previously worked under legendary investor Bill Miller at Legg Mason and is one of the few experts on Warren Buffett.

Kraft Heinz turnaround

The turnaround story of Kraft Heinz ( KHC ), getting their costs in order and bringing the business back to profitability and growth has been well covered on Seeking Alpha. They are paying down debt and reconfiguring the business to sustain better cash flow. Many have questioned what Warren Buffett has seen in Kraft Heinz and what he continues to see. Buffett has held his stake since the merging of the two packaged food giants, seemingly reinforcing his belief in the business and the brand. My last coverage of the stock can be found here from January 2023.

What he likely sees is a beloved brand and a moat. Maybe the margins aren't where they should be, and that's where 3G Capital comes in regarding restructuring. For those familiar with Robert G. Hagstrom's The Warren Buffett Way , he breaks down how Buffett discounts future cash flows to the present. Kraft Heinz is a buy here. Let me demonstrate why.

The chart

For the fellow bottom fishers out there, I have had my reel cast and line in the water for quite some time. Since the big drop around 2018, this stock has remained flat, swimming near its bottom down somewhere between 50-60% at any given time. To me, that represents close to a double your money opportunity if we believe that Warren Buffett's original valuation of the company holds merit.

What they do

A succinct description of the business from Kraft Heinz's most recent 10-K :

We sell certain products under brands we license from third parties. In 2022, brands used under licenses from third parties included Capri Sun packaged drink pouches for sale in the United States. We also grant certain licenses to third parties to use our intellectual property rights in select jurisdictions. In 2021, in our agreements with an affiliate of Groupe Lactalis ("Lactalis"), related to the sale of certain assets in our global cheese business, we each granted the other party various licenses to use certain of our and their respective intellectual property rights in perpetuity, including perpetual licenses for the Kraft and Velveeta brands for certain cheese products.

We also own numerous patents worldwide. We consider our portfolio of patents, patent applications, patent licenses under patents owned by third parties, proprietary trade secrets, technology, know-how processes, and related intellectual property rights to be material to our operations. Patents, issued or applied for, cover inventions ranging from packaging techniques to processes relating to specific products and to the products themselves. While our patent portfolio is material to our business, the loss of one patent or a group of related patents would not have a material adverse effect on our business.

Owner earnings & intrinsic value

I hear copious amounts of quotes on the internet about "all stocks are the present value of future cash flow". This invariably leads to the discounted cash flow models we used during our MBA studies combined with the capital asset pricing model or CAPM. The Warren Buffett Way points out that the particular way Warren Buffett discounts a stock's cash flow is unique by comparison. It focuses more on a moat.

The moat is fairly easy to find when a company has depreciation and amortization expense roughly equal to or greater than capital expenditures. This indicates a company that laid out a good chunk of capital in the beginning, and now only has to continue an outlay roughly equivalent to their ongoing depreciation and amortization. The inverse of this would be a company where capital expenditures continue to outstrip depreciation and amortization by a wide margin, which would be a highly competitive business that is ever increasingly expensive to run.

If we do a back-of-the-napkin average for a company that is 33% depreciation of real property at 27.5 years, 33% equipment at 7 years, and 33% amortization of goodwill at 15 years on average would result in a 17.25-year blended depreciation schedule for tangible assets. So in this case, a company shouldn't have to replace much more than 1/17 of their tangible asset base [or less depending on the amount of intangible assets related to amortization] to be efficient and have a burgeoning moat.

From the book

From Hagstrom's book, net income is first adjusted to add back in depreciation and amortization, which is different than EBITDA, this still accounts for interest and taxes, two very real expenses to a business. Then you subtract capital expenditures. If capex is huge in comparison to D&A, the business will pencil out less valuable, if equal or close to it, then you have an efficiently run business.

Hagstrom also points out that Buffett did not believe in the CAPM required rate of return that incorporates market risk. If the business still has good earnings after adding in D&A and subtracting out capex, then the 10-year treasury risk-free rate is all that was needed.

Kraft Heinz discounted value

All data TTM courtesy of Seeking Alpha

| KHC numbers in millions except per share items | |

| VALUE | |

| NET INCOME | |

| |

| + D&A | |

| |

| - CAPEX | |

| |

| OWNER EARNINGS | |

| |

| DIVIDED BY 10 YEAR TREASURY RATE DISCOUNT [3.46%] | |

| |

| SHARES OUTSTANDING | |

| 1227 | |

| PER SHARE VALUE | |

| |

| COMPANY VALUE | |

| $68.7 Billion |

With Kraft Heinz valued at a market cap of $49 Billion as of current, this leaves a 40% upside to fair value. The calculus on this was far better when Buffett helped put the deal together as the risk-free rate was lower at that time. Capital expenditure at the merger was also only $399 million. What was thought of as overvaluation at the time would look very fair considering these items in retrospect.

The balance sheet and current assets vs LT debt

Harkening back to Peter Lynch's advice on the easy way to look at a balance sheet. We want to see long-term debt trending downwards and current assets trending upwards. With current assets being the source of capital to extinguish debt and grow the business, this analysis is simple and logical. The Kraft Heinz chart is not ideal, but the turnaround is apparent. Current assets are trending flat while long-term debt is on a nice downward trajectory. This balance sheet motive is clear and looks better every quarter.

Competition

Now let's run the same comps on General Mills ( GIS ), Conagra ( CAG ), and Hormel ( HRL ) using the Buffett "owner earnings" discount and see how the industry is priced. Please note the value cell is the discounted owner earnings divided by the current shares outstanding. The current cell is the current per share price.

My own excel, data from Seeking Alpha

{kind=link}

Just looking at these three comps, you can see where Warren Buffett would be attracted to the packaged food industry and consumer staples. All of these brands have been established and operate efficiently with Capex running nearly parallel to depreciation and amortization. All appear undervalued on this metric with General Mills at 50.9% undervalued, Hormel at 29% undervalued, and Conagra at 18% undervalued.

These stocks may never be priced at Buffett's intrinsic value, but the margins of safety are fairly wide in this industry regarding the present values of future cash flows. This is especially true when compared to the 10-year Treasury. When the Warren Buffett Way was running this calculation on The Washington Post and Geico, the 10-year Treasury was double digits! Bill Gross just shed a tear.

Margin trends

The operating margin has dropped a bit, but CAPEX is also tapering off and D&A is flat. If margins stabilize to tic up with inflation subsiding and CAPEX continues downward while D&A remains flat, the business is improving from the Buffett owner earnings perspective.

Competition ROA

The argument over book value having potential for a lot of value extraction can be seen here in return on assets. Although operating margins are similar across the industry, Kraft is having a more difficult time getting a good return on their assets. If turned around to total optimization, they should be able to double or possibly triple their return on assets getting it closer to General Mills' 9%.

One glaring issue for Kraft Heinz versus General Mills is interest expense. Kraft is in the $900+ million range while General Mills is in the low $300 million range per annum. The cost of revenue for Kraft Heinz is also about 3% higher than General Mills at 69% vs 67%. Working on paying down debt, optimizing the sales team, SG&A, and improving the supply chain should get Kraft Heinz closer to their turnaround goal.

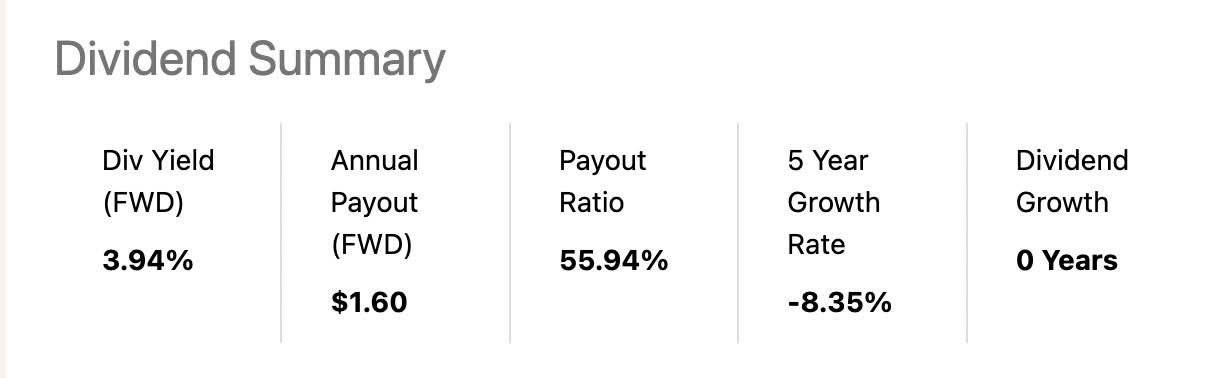

The dividend trends

{kind=link}

The yield is nice, but we will certainly have to wait for dividend growth. Once inflation subsides and costs of goods and operations are brought under control, this could be a nice dividend growth stock. Let's see the competition yields:

| STOCK |

| YIELD |

| CAG |

| 3.62% |

| HRL |

| 2.73% |

| GIS |

| 2.39% |

Even with dividend growth of the others considered, Kraft Heinz is still top of the class at 3.94%. Let's look at the price growth charts of these companies that have been delivering dividend growth to their investors:

Here we can see Kraft Heinz has been the clear laggard of the bunch with only 24.52% total return during the comp period. Keep in mind though, Kraft Heinz is the only one in the bunch priced at book value, basically 1 X or less for the last few years. The assets are priced as they are for now, due to underperformance. This is a clear upside opportunity versus competition representing a coiled spring once margins get better and debt reduced.

Catalysts and future plans from Q1

First Quarter Highlights from the Q1 presentation:

• Net sales increased 7.3%; Organic Net Sales(1) increased 9.4%.

• Gross profit margin increased 62 basis points to 32.6%; Adjusted Gross Profit Margin(1) increased 126 basis points to 32.8%.

• Net income increased 7.1%; Adjusted EBITDA(1) increased 10.3%.

• Diluted EPS was $0.68, up 7.9%; Adjusted EPS(1) was $0.68, up 13.3%.

The gross margins are up, certainly from inflation subsiding and the supply chains right siding. The company has been able to beat on the top and bottom lines in one of the better prints they've had in a while. As debt is further reduced, the bottom line should improve:

{kind=link}

Net interest expense has fallen quarter by quarter as debt pay-down has remained a priority.

{kind=link}

Since the increase in the float during the 2020 Covid supply chain crisis, the company has instituted buybacks again. They have reduced the float by 3.6% over the last 2 years. I would welcome more buybacks versus a dividend increase as the business is still very undervalued.

Specific risks from the 10-K

As per the 10-K:

-

We operate in a highly competitive industry.

-

Our success depends on our ability to correctly predict, identify, and interpret changes in consumer preferences and demand, to offer new products to meet those changes, and to respond to competitive innovation.

-

Changes in the retail landscape or the loss of key retail customers could adversely affect our financial performance.

-

We must leverage our brand value to compete against private label products.

-

Berkshire Hathaway ( BRK.A )( BRK.B ) has the ability to exert influence over us and significant influence over matters requiring stockholder approval.

The final risk is more of a benefit than a worrying disclosure. Charlie Munger and Warren Buffett influence the business and we can assume they make recommendations as to how to return capital to shareholders. If we see buybacks happening before dividend raises, the management team at Berkshire must be hinting that buybacks are the way to go first. A nice reduction in the float will provide an excellent runway for consistent dividend growth in the future.

Conclusion

With the highest yield of the packaged food comps, debt being reduced and margins hopefully improving from a subsiding of inflation, Kraft Heinz is a good long-term value. The stock is the second cheapest of the group, but also one not trading at the top of the chart. I concede General Mills looks great, I just have reservations about buying the top of a chart. Previous articles of mine have priced Kraft Heinz based on a modified Graham Number. The stock is undervalued on that basis as well due to the low price-to-book.

Considering the undervaluing of the assets, I would still consider Kraft Heinz to be the cheapest due to the underperformance of the assets. Once the management starts operating on par with comps, the stock should have plenty of upside. I, therefore, leave you with the above chart.

If you run the "owner earnings" model on other sectors, you'll notice CAPEX outstripping D&A by much wider margins. This would result in lower business valuations for this model. We are getting the assets cheap, but with a lot of debt. Be patient and let it be paid down and costs to come under control. I'm waiting patiently. Kraft Heinz is still a buy and it appears Warren Buffett continues to stick to the thesis. The consumer staples sector is one of the most efficient from a cash flow perspective.

For further details see:

Kraft Heinz: The Intrinsic Value Of Owner Earnings