KHC - Kraft Heinz: The Lunchables Investment Thesis Isn't Tempting Enough

2023-10-11 16:00:00 ET

Summary

- KHC's sales volume has been directly impacted by the previously aggressive price hikes, worsened by the elevated interest rate environment and tightened discretionary spending.

- As more consumers increasingly choose private label products, the company's top and bottom lines may stagnate if the trend turns permanent.

- We also believe that KHC's school lunch story is not convincing yet, with consumers generally being more health conscious after the COVID-19 pandemic.

- While KHC used to be a dividend aristocrat until the cut in 2003, the stock may no longer be a viable dividend play here, due to its underwhelming 5Y Dividend Growth at -8.54%.

- With a potential downside of -12.5% from current levels, we do not recommend anyone to add here.

The KHC Investment Thesis Remains Highly Speculative

The Kraft Heinz Co. ( KHC ) is a stock that requires no introductions, with its two namesake products occupying many of the American consumers' grocery lists, namely the Kraft Cheese Singles and the Heinz Tomato Ketchup.

With cheese/ dairy products and condiments/ sauces comprising 13.1% (-1 points YoY) and 35.5% of its top-line in FQ2'23 (+2.9 points YoY), it is unsurprising that these two segments remain highly eponymous to the company's branding.

This also meant KHC's robust pricing power over the past few years of uncertainties, allowing the management to maintain its revenues at $6.72B (+3.7% QoQ/ +2.5% YoY) and gross margins at 33.6% (+0.9 points QoQ/ +3.2 points YoY) in FQ2'23, compared to FY2019 margins of 32.8% (-1.7 points YoY).

With a robust annualized Free Cash Flow generation of $3.42B in the latest quarter (+289% QoQ/ +956.7% YoY), the management has also been able to drastically deleverage its balance sheet to a long-term debt of $19.36B (inline QoQ/ -1.8% YoY) compared to FY2019 levels of $28.05B (-8.8% YoY).

However, with the inflation for food items almost peaking at 0.2% in the August 2023 CPI and KHC unlikely to hike prices any further, we may see its top-line growth stagnate moving forward.

The latter is to be expected, in our view, as the interest rate environment remains elevated, and the consumer discretionary spending tightened for groceries.

This is especially worsened by the widening price gaps between KHC's products and the private labels, as discussed by the management in the FQ2'23 earnings call:

Since second half of 2022... we have taken that pricing to protect our margins, and some branded competitors have not followed... Our price in Q2 as you saw was close to 11%, and the reason why we saw higher elasticity and higher volume decline as I said before is because of the expanded price gaps. ( Seeking Alpha ).

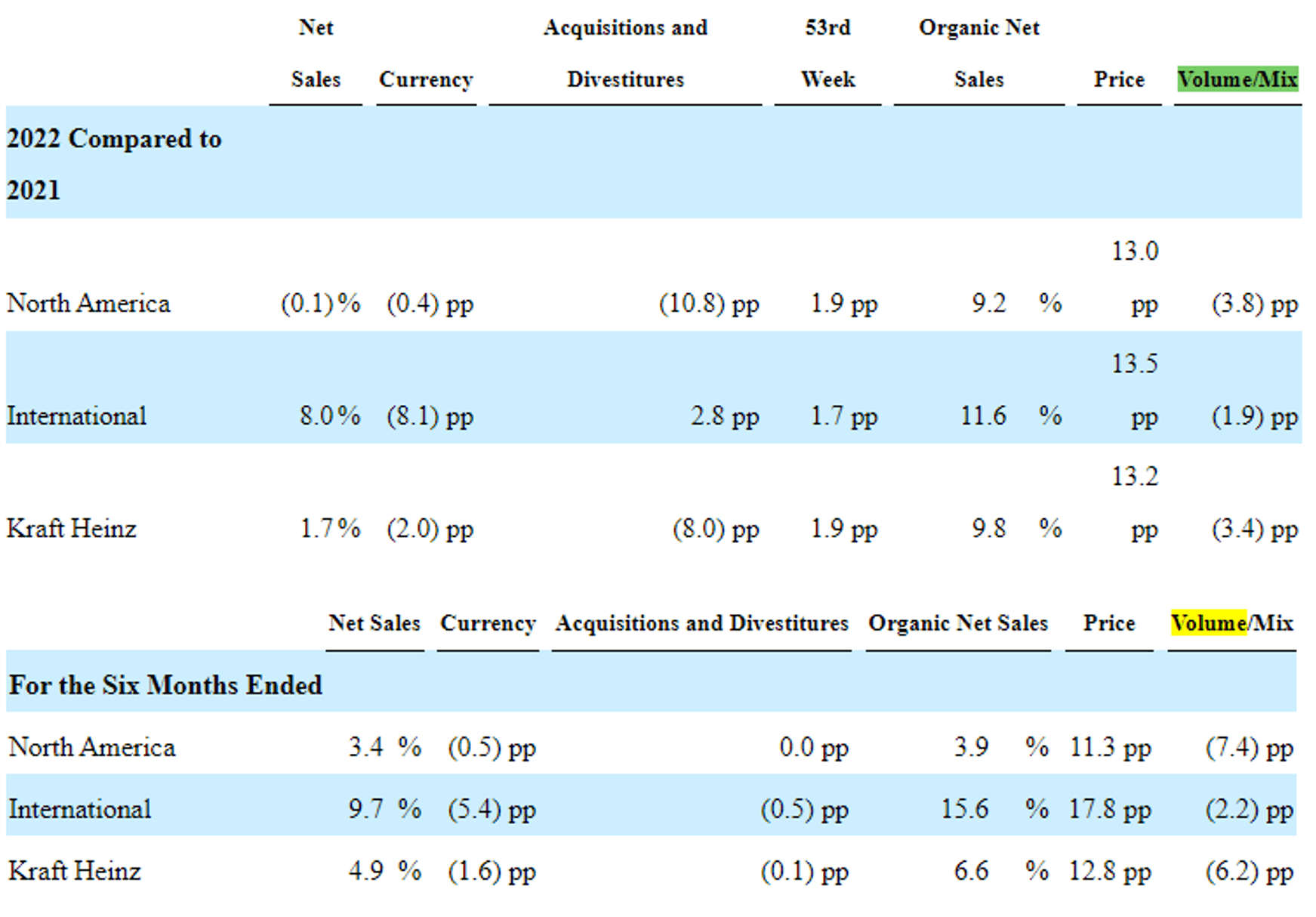

KHC's Volume Declines Since 2022

{kind=link}

As a result, it is unsurprising that KHC's sales volume has been consistently declining since 2022, triggering Mr. Market's pessimism about its prospects, as 73% of consumers increasingly choose private label products and 64% expressed their intention to "keep buying them even as the economy improves."

If the trend eventually becomes permanent, the company's top and bottom lines may stagnate indeed, potentially triggering further headwinds to its future stock performance.

Lunchables In School? We Do Not Think So

Perhaps this is why KHC has chosen to ambitiously embark on a new strategy to drive growth, namely Lunchables.

For context, the company has partnered with the National School Lunch Program [NSLP] to provide Lunchables to students across Pre-K and grade 12 in nearly 100K US schools for the 2023-2024 school year. Based on the US Department of Agriculture, the NSLP program was worth approximately $14.2B in 2019.

This number corroborates with the management's strategy of leveraging the $25B untapped school lunch market as a " penetration machine " toward improved retail sales.

In order to comply, KHC has already committed to making Lunchables more nutritious, by cutting sodium, sugar, and saturated fat while adding fresh fruits.

Assuming an eventual success, we may see its top-line drastically boosted over the next four quarters, since Lunchables comprise $1.8B or the equivalent of 8.6% of its annual sales.

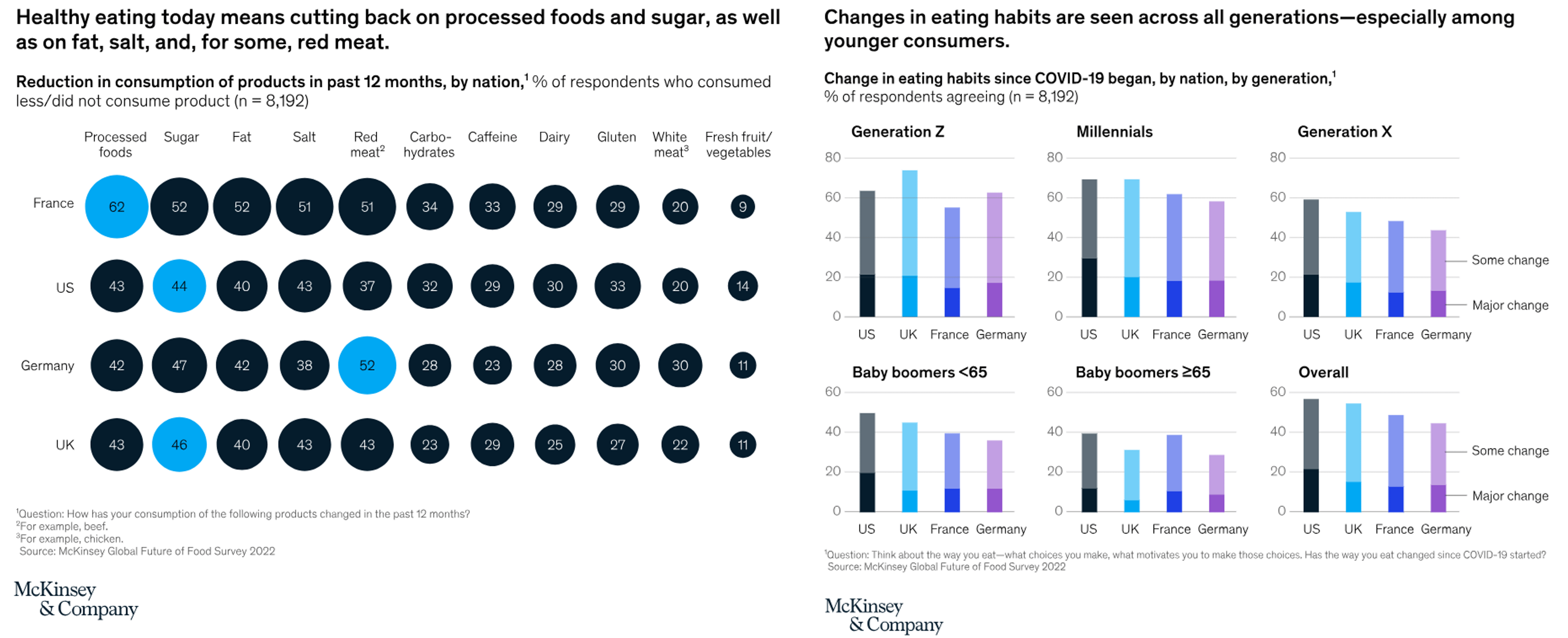

However, we believe that KHC's school lunch story may not be convincing yet, with consumers generally being more health conscious after the COVID-19 pandemic.

For example, a global research done by McKinsey & Company reported that approximately "50% of consumers across all age groups say healthy eating is a top priority for them."

A Survey On Healthy Eating By McKinsey & Company

{kind=link}

Most importantly, 43% of the American surveyed has opted for reduced consumption of processed foods in 2022, particularly prevalent for those between 11 and 58 years old, otherwise known as Gen Z, Millennials, and Gen X.

As a result of KHC's uncertain Lunchables prospects over the next twelve months, we prefer to reserve judgement until actual results are observed, especially given its minimal top and bottom line growth at a normalized CAGR of 0% and -3% between FY2016 and FY2022, respectively.

So, Is KHC Stock A Buy , Sell, or Hold?

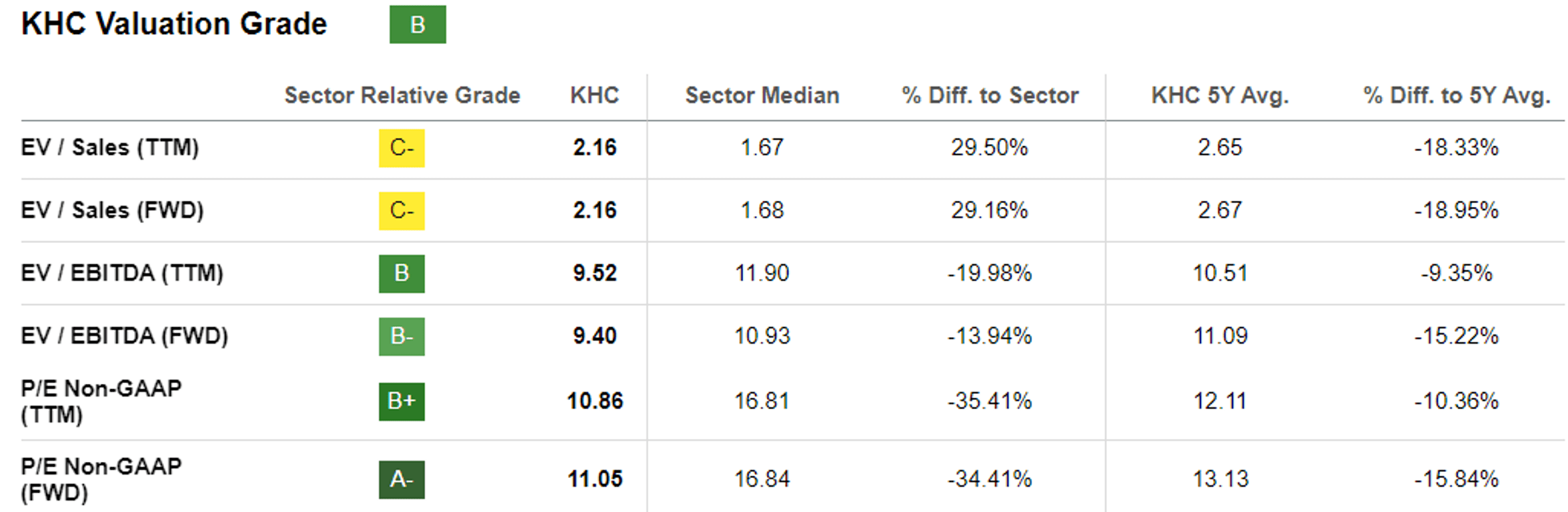

KHC Valuations

{kind=link}

For now, KHC trades at impacted FWD valuations compared to its 1Y means, 5Y means, and sector medians, implying Mr. Market's uncertainty about its prospects.

This is an interesting phenomenon, in a direct contrast against the projected improvement in its top and bottom line CAGR of +1.7% and +4.1% through FY2025, compared to its normalized levels over the past six years.

Then again, based on the consensus FY2025 adj EPS estimates of $3.14 and KHC's FWD P/E of 11.05x, we are also looking at an underwhelming long-term price target of $34.69, implying a minimal +8.3% upside potential from current levels.

While KHC used to be a dividend aristocrat until the reduction in 2003, it appears that the stock is no longer a viable dividend play here, due to its underwhelming 5Y Dividend Growth at -8.54% and TTM Free Cash Flow Yield to Dividend Yield Ratio at 1.16%. This is compared to the sector median of 5.62% and 1.63%, respectively.

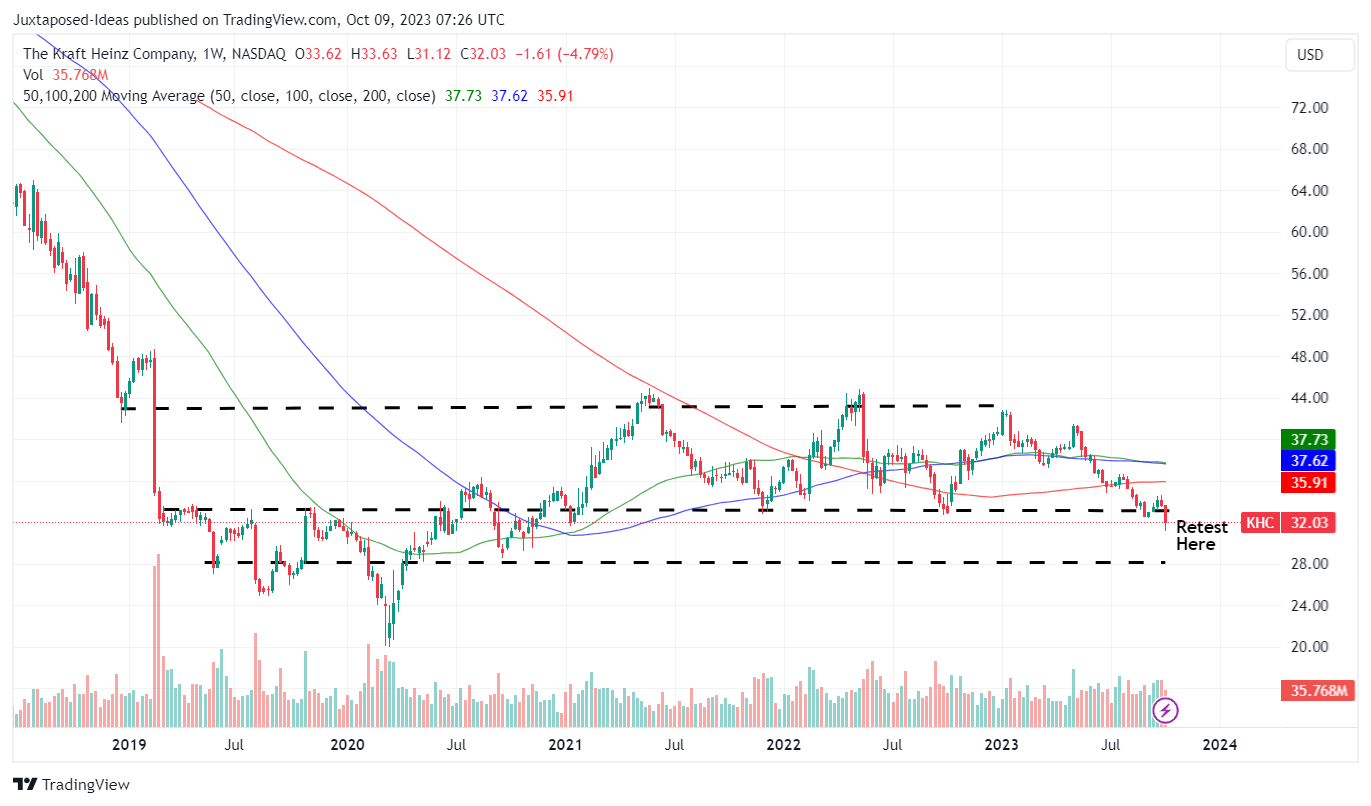

KHC 5Y Stock Price

{kind=link}

In addition, KHC has also failed to break out of its resistance levels of $44 thrice, while charting new highs and new lows since January 2023. With the stock now retesting its critical support levels of $32 at the time of writing, we may see more volatility in the near term.

Assuming that this level is breached, we may see a further retracement to $28, implying a downside of -12.5% from current levels.

As a result of its underwhelming prospect as a growth/ dividend play and the potential capital losses, we prefer to cautiously rate the KHC stock as a Hold (Neutral) here.

KHC's situation may get worse in the future.

For further details see:

Kraft Heinz: The Lunchables Investment Thesis Isn't Tempting Enough