KHC - Kraft Heinz: Value Trap Or Cheap Enough To Keep Holding?

2023-09-13 16:16:47 ET

Summary

- Kraft Heinz is a mediocre company that is trading at a fair price of 13.1x TTM P/E due to its stagnant total revenue growth.

- The company has done well reducing debt in recent years but their low 5.4% ROIC makes it hard to meaningfully leverage returns for equity investors.

- With cash flow from operations (adjusted for impairments) of $3.8 billion over the past five years, the 25% spent on capex would imply an FCF yield to shareholders around 6.9%.

Shares of Kraft Heinz ( KHC ) remain in the dumpster at 13.1x TTM P/E due to stagnant volumes and a still high debt load. I have sadly been an owner of Kraft Heinz since 2018 with an average cost base of around $59.95. It is not a big holding for me (less than 1% of my portfolio) as I just decided to dip my toe in when the stock price started to fall in 2017 a couple years after the merger of Kraft and Heinz when the impairments started to affect earnings.

Kraft Heinz's profitability is subpar and the company has not been quick enough to pay off the debt in my opinion and this will affect net income available to shareholders for years to come as interest rates have risen. While the company's International sales are growing, North America is struggling as consumers switch to healthier and more local brands. It would be hard for Kraft Heinz to transform itself at this stage even with more acquisitions and I have given them 5 years of attempts. That being said, the stock price is the cheapest it's been and while the company is stagnant at 11.7x forward P/E, investors are not paying much for growth.

This article will look at an analysis of Kraft Heinz over the past 5 years to get a sense of potential equity returns as we adjust for non-cash impairments to focus on cash flows implying a 6.9% yield. I am almost ready to pull the plug on Kraft Heinz if it wasn't for the current valuation. One always have to be cautious of a value trap though and Kraft Heinz could be a good example with its low 5.4% ROIC. According to 13A filings, Berkshire Hathaway (BRK.A) (BRK.B) still owns 422.64 million shares or around 34.5% of Kraft Heinz's stock as of February 2023 but had sold off 88.0 million shares since previously reporting 510.70 million shares in February 2022. The slow sales from Berkshire might be a signal they are starting to lose hope in Kraft Heinz too.

Latest Quarterly Results

In Kraft Heinz latest Q2 2023 quarterly results the company reported sales of $6,721 million which were up 2.6% compared to the prior year quarter. For the six month period, Kraft Heinz reported sales of $13,210 million which was up 4.9% from the prior year. The company's International segment drove the growth up 8.5% and 9.5% for the quarter and six month period, respectively, which compares to relatively flat growth in the North America segment of 0.8% and 3.4%, respectively.

Unfortunately, these revenue gains came primarily from price increases with volume suffering across the board. For the full year 2023, Kraft Heinz expects organic sales growth of 4 to 6% versus the prior year. Adjusted gross profit margin is now expected to expand 150 to 200 basis points versus the prior year (as compared to the company's previous expectation of 125 to 175 basis points) driven by price increases and efficiencies. All of this will lead to constant currency adjusted EBITDA growth of 4 to 6% versus the prior year (or 6 to 8% when excluding the impact from lapping a 53rd week in 2022). Adjusted EPS is expected to be in the range of $2.83 to $2.91 (includes a negative $0.06 impact from lapping a 53rd week in 2022). As the $2.87 midpoint of management's forward guidance, this implies Kraft Heinz is trading at an 11.7x forward P/E.

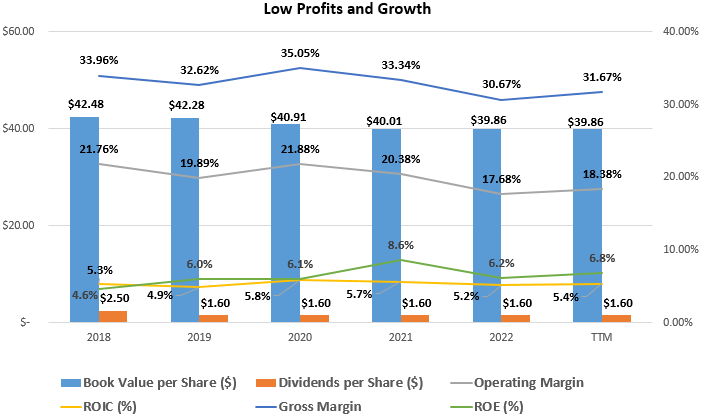

Low Profits and Slow Growth

Kraft Heinz's brand portfolio has allowed the company to achieve what I can only describe as mediocre returns to investors. But, as always an investor's return is based off what you are paying for that equity on the balance sheet in the stock market. The below figures adjust for 2018's massive $15.9 billion net impairment for the year as well as other impairments across the years (a total of $25.8 billion over the 5 year period). These adjusted figures show Kraft Heinz achieving average return on equity and return on invested capital of 6.4% and 5.4%, respectively, over the past five years. This level of profitability is well below my rule of thumb of 15% ROE and 9% ROIC, making me question, in my opinion, if the company is able to maintain and continue to increase its intrinsic value in Kraft Heinz's mature industry stage.

Historic Profitability & Growth at Kraft Heinz (compiled by author from company financials)

{kind=link}

How is the Cash Flow?

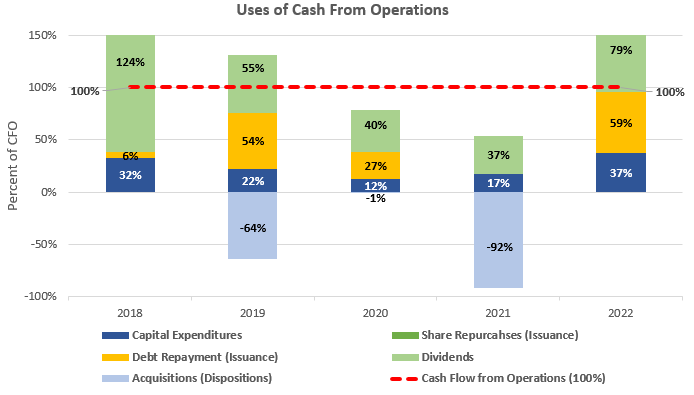

Strong businesses with good brand portfolios such as Kraft Heinz are able to generate cash beyond what is needed to fund sustainable operations. As can be seen in the graph below, capital expenditures have averaged only 25% of cash flow from operations over the past decade which is a good figure and what I would expect from a well-branded consumer staple company.

Kraft Heinz has been a net seller of brands and assets with net divestments of $6.8 billion from 2018 to 2022. Notable divestments from Kraft Heinz over the past few years have been the Cracker Barrel to Parmalat in Canada in 2019 ($1.2 billion), various non-core brands in India in 2019 ($655 million) to Zydus Cadila, and then further divestments/perpetual licenses of cheese brands Kraft and Velveeta in additional to a 3-year license of the Philadelphia brand cheeses, respectively ($3.3 billion) to Groupe Lactalis in 2021. These large divestments are behind the discrepancy between total revenue growth and organic/adjusted growth rates from management that exclude these segments. I normally add acquisitions in a cash flow analysis if they are a regular part of the capital budget, but regular divestments such as those from Kraft Heinz are not sustainable long-term and were mainly for the company to paydown debt while streamlining its portfolio.

Cash Flow Analysis ((compiled by author from company financials))

{kind=link}

With capital expenditures only taking up on average 25% of cash flow from operations over the past decade, this leaves approximately 75% to be returned to investors in the form of dividends and share repurchases. With average cash flow from operations of $3.8 billion over the past five years, this 75% would imply free cash flow to shareholders of $2.8 billion for a decent 6.9% free cash flow yield at the current $41.2 billion market capitalization. The only problem is that there is little to no growth with Kraft Heinz, except for managements "organic growth" figures so this 6.9% might be all investors are getting. Total Revenues in 2018 were $8.9 billion, which is a slight decrease over the period of a -0.9% CAGR to the current $8.6 billion TTM revenue figure.

High Debt and Low ROIC to Leverage

Debt levels at Kraft Heinz stem from the historical merger which formed the company and have improved slightly over the past 5 years from $30.8 billion of total debt in 2018 to $20.0 billion in the latest quarter. With a current financial leverage ratio of only 1.82x in the most recent quarter and operating profits providing a decent interest coverage level of 5.5x for a consumer staples company.

While the company's capital allocation policy has not contained any share repurchase programs, Kraft Heinz has not been issuing shares in order to pursue expensive acquisitions either. In my opinion, this shows management and the board of directors behaving responsibly trying to pay down debt with excess cash flows and the previously mentioned divestitures discussed in the cash flow analysis. While debt has decreased significantly from 2018 levels, it is still high on a relative basis to competitors such as Unilever who carries a similar $20 billion of outstanding debt but has a market cap that is around 4x higher that Kraft Heinz.

Capital Structure at Kraft Heinz (compiled by author from company financials)

Also important when looking at Kraft Heinz's use of debt is that the low 5.4% ROIC discussed earlier is barely leverageable as the cost of debt for Kraft Heinz is high. When one divides interest expense in the TTM period by the average debt over the period, it looks like Kraft Heinz debt costs around 4.6% so this is tight, especially in a market where interest rates are getting more expensive to rollover. These same figures for Unilever show a cost of debt around 3.5% which is much more lower than the 18.9% ROIC Unilever is earning.

Getting a Sense of Valuation

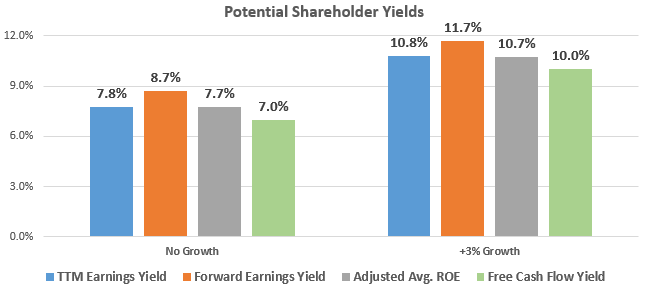

Kraft Heinz's 13.1x TTM P/E ratio and forward P/E of 11.7x discussed earlier in the quarterly results can also be expressed as 7.8% and 8.7% earnings yield, respectively. I also always like to examine the relationship between average ROE and price-to-book value in what I call the Investors' Adjusted ROE. It examines the average ROE over a business cycle and adjusts that ROE for the price investors are currently paying for the company's book value or equity per share.

With Kraft Heinz earning an average ROE (adjustment for impairments) of 6.4% since 2018 and shares currently trading at a price-to-book value of 0.84x when the price is $33.56, this would yield an investors' Adjusted ROE of 7.6% for an investors' equity at that purchase price, if history repeats itself. This is slightly below the 9% that I like to see, but adding a 3% growth rate to represent this mature company growing alongside global GDP, could increase this potential total return up to 10.6%. This conservative 3% growth is below managements 4-6% organic sales and EBITDA guidance for the current year discussed earlier but I remain hesitant due to long-term total growth and divestitures. Below is a table outlining the potential earnings yield estimates from this investors' adjust ROE figure as well as the cash flow and earnings yields discussed.

Potential Shareholder Yields from Kraft Heinz (compiled by author from market data and company financials))

{kind=link}

Takeaway for Investors

Kraft Heinz is a mediocre company that is trading at a good price of 13.1x TTM P/E. The company has been making divestitures in recent years and total unadjusted revenue growth has been fairly flat, so growth is questionable. Fortunately, investors are not paying much for growth at current prices. The company has done well reducing debt in recent years but their low 5.4% ROIC makes it hard to meaningfully leverage for equity investors causing the company to trade at only 0.84x book value. With a 6.9% cash flow yield and dividend of 4.8%, one has to believe in management's organic growth prospects of Heinz core brands across North American and International markets to remain an investor. I will keep a close eye on Kraft's volumes as I continue to hold and collect the dividend.

For further details see:

Kraft Heinz: Value Trap Or Cheap Enough To Keep Holding?