KHC - Kraft Heinz: Volume Declines Continue

2023-11-09 16:49:00 ET

Summary

- Pricing continued to drive Kraft Heinz's results in Q3, while volumes once again continued to decline.

- The strategy has been paying off with higher gross margins and profits.

- However, the company will start to lap price increases, and the focus will turn more towards volumes in 2024.

Back in March , I called Kraft Heinz ( KHC ) a boring, defensive stock, placing a “Hold” rating on it. Since then, the stock has retuned -10% versus a 12% gain for the S&P. More recently, in September I noted that volume should come more into focus as price hikes fade. Let's catch up on the ketchup maker.

Company Profile

As a reminder, KHC is a food and beverage company that owns some of the biggest brands in the world, including Heinz, Kraft, Philadelphia Cream Cheese, Oscar Mayer, Lunchables, and Velveeta. Its products and sold at grocery stores and other retail locations, while it also sells into the foodservice industry to places like restaurants and sporting venues. Its biggest category is condiments and sauces, accounting for about 15% of its sales.

Price Vs. Volume

In my prior write-ups, I discussed how price has been the big driver of KHC's sales growth, and this trend once again played out in Q3. For the quarter, the company saw its organic sales rise 1.7%, which is below the company's 2-3% long-term growth target and below analyst expectations of 2.8% growth. Price accounted for 7.1% of its growth, while volumes/mix declined -5.4%

In North America, organic sales fell -0.1%. Price rose 5.8%, while volume and mix were -5.9%. The company said much of its volume declines were in its meat business, where it is more focused on rebuilding profitability and protecting EBITDA dollars.

Discussing market share on its Q3 earnings call , President Carlos Abrams-Rivera said:

“Now turning to market share …, our actions plans are working. … As you can see, these investments are paying off. Looking at our U.S. dollar share, we have recovered from the low levels experienced earlier this year. As you recall, we faced expected headwinds after pricing 75% of our portfolio and the reduction of SNAP benefits earlier this year. We have planned for elasticity to return to more normal levels, and that's what we have seen. In July, at a point where volume losses in cold cuts were at their highest, we hit the lowest share levels of the year. Since then, we have improved volume as year-over-year price gap has narrowed. In Taste Elevation and Easy Meals …, we have steadily improved and are now gaining market share from branded players. If you recall from last quarter, our share loss was concentrated in 3 categories: cream cheese, cold cuts and kids single-serve beverage. Across cream cheese and cold cuts, we have seen recovery in share, particularly in the month of September … In kids single-serve beverage, our share continues to be pressured, primarily driven by the reduction in the SNAP benefits as well as lapping competitive out-of-stocks in the prior year.”

Internationally, organic sales rose 8.0%, with price increases of 11.6% helping fuel the gains. Volume mix was down -3.6%.

In emerging markets, the company saw 10% organic sales growth. It noted its LatAm and Mideast businesses were strong, while Asia has some softness. While emerging markets outpaced overall international sales, this appears to be below expectations, as last quarter the company said second half growth should be closer to the 23% growth for emerging markets it saw in Q1. Instead, emerging market growth was even slower than the 11% it saw in Q2.

The foodservice industry was another area of growth I’ve discussed, and on that front, the company saw approximately 9% growth in the channel. The company is growing share in this channel, particularly internationally.

Overall, KHC grew revenue just over 1% to $6.57 billion, which missed the analyst estimates of $6.7 billion. Adjusted EPS rose 14% to 72 cents, topping the 66-cent analyst consensus.

Gross margins improved 568 basis points to 34.0%

Adjusted EBITDA rose 12% to $1.57 billion. North American EBITDA grew nearly 15% to $1.39 billion, while International adjusted EBITDA climbed nearly 7% to $259 million.

Looking ahead, the company said its organic net sales growth would come in at the low end of its prior outlook of between 4-6%. However, it raised its full-year expectations for adjusted EBITDA growth, taking it to 5-7% from a prior outlook 4-6%, or 6-8% growth. Adjusted EPS is now projected to be between $2.91-2.99, up from previous guidance of $2.83-2.91.

Overall, it was a mixed quarter from KHC. Price continues to drive sales at the expense of volumes. Right now, this strategy has been working, as it has led to higher gross margins and more robust profits despite the volume declines.

However, the volume declines were not enough to overcome pricing this quarter from a sales perspective, leading to negative organic sales growth in North America. The company claims the worst of its volume declines are behind it and there was an improvement sequentially, but the impact of pricing is also coming down as well.

Emerging markets results, meanwhile, clearly were disappointing as well. The rebound in growth the company expected did not happen, which it seemed to blame on issues around Indonesia and Ramadan. That’s now two quarters in a row of disappointing emerging market growth, however. This was downplayed on the company's earnings call, but is something to watch moving forward.

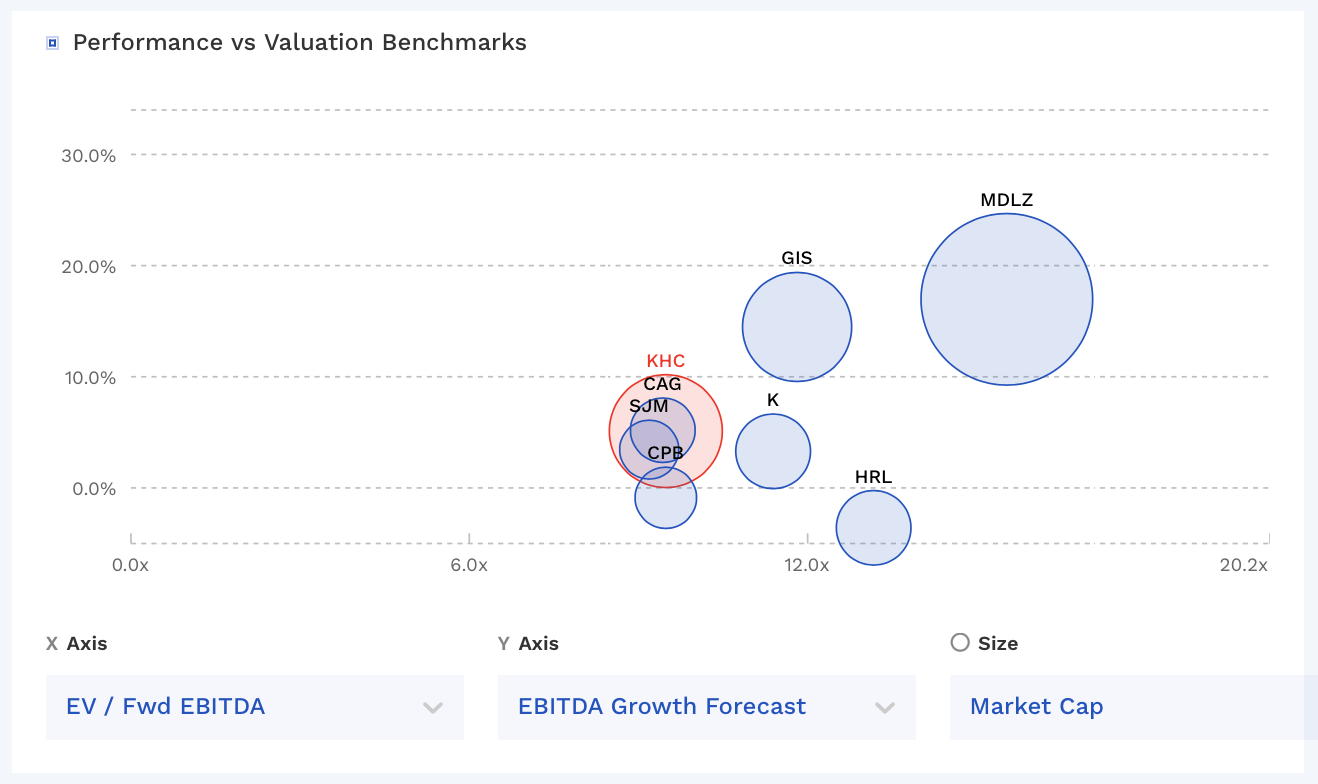

Valuation and Dividend

KHC stock currently trades around 9.5x the 2023 consensus EBITDA of $6.30 billion and 9.3x the 2024 consensus of $6.43 billion.

It trades at a forward PE of 11.2x the 2023 consensus of $2.96 and 10.9x the 2024 consensus of $3.02.

It's projected to grow revenue by 1.1% this year and 1.0% next year.

The company currently pays a quarterly dividend of 40 cents, good for a yield of about 4.8%. It has paid out the same dividend since 2019, after cutting it from 62.5 cents.

Through the first six months of the year, its payout ratio using net income is 70%. Using free cash flow, it is 80%. Its leverage was 2.9x at quarter end.

With its leverage just under its 3.0x target, the dividend looks safe.

KFC is among the cheaper food product companies out there, and the company has historically traded between a 10-15x EV/EBITDA multiple.

{kind=link}

Conclusion

Moving forward, KHC is going to have to continue to navigate price versus volume. 2024 should be a lot different than 2023, with price increases slowing down, putting more of an emphasis on a volumes recovery. For its part, the company is expecting to see volume growth at some point in 2024. It has a new CEO coming in, and recovering lost volumes may not be that easy.

From a valuation standpoint, the stock trades around the same multiple as many of its low growth peers and below recent historical levels. However, given that interest rates are much higher today than a few years ago, I feel these slow growth consumer staple names should trade at a discount compared to when interest rates were at near historical lows for so many years.

At this point, I feel the stock is pretty close to fairly valued and the dividend looks safe. I lean a bit more bearish on the time as I think the volume-price story could be more difficult next year, but given that the valuation isn’t stretched and the nearly 5% dividend yield, I think “Hold” remains the proper rating for now.

For further details see:

Kraft Heinz: Volume Declines Continue