VNTR - Kronos Worldwide: Depressed Cyclical At Below Replacement Value

2023-04-17 13:36:16 ET

Summary

- Kronos Worldwide is a boring business facing temporary challenges. We believe the recent drop in its share price warrants a second look at the investment credentials.

- The company produces titanium dioxide, which is a crucial input for, among others, paints, cosmetics and coatings.

- While the TiO2 industry is fiercely competitive, the demand for its products is expected to grow fast in the coming years.

- The company is trading at depressed valuations and investors get paid an attractive dividend as they wait for the cycle to turn.

- Our analysis suggests that KRO has limited downside and the possibility of an attractive return if the cycle turns. We, therefore, believe KRO shares offer an attractive risk/reward profile.

Introduction and Thesis

Kronos Worldwide ( KRO ) recently entered our watchlist as the recent results disappointed investors, leading to a sharp fall in the share price to approx. $9.08 per share. Many investors have a bearish view of the company and approx. 11% of the company's stock is shorted. This pessimism toward the company reflects in an EV/EBITDA multiple of 6x and a Price/Sales ratio of 0.5x. We believe that it is therefore a good time to revisit the company and the attractiveness of the share as a possible contrarian investment.

When considering Kronos’ shares as for potential investment, we have to stress that this is not a compounding business, where you can store the share certificates in your coffee tin and forget about them. As Peter Lynch explained, when investing in cyclical companies, timing is crucial. We aim to buy cyclical companies on assets and sell them on earnings. Kronos comes across as one such opportunistic trade, in our view.

Company Overview

Kronos Worldwide is a leading global producer and marketer of value-added titanium dioxide pigments . The company was founded in 1916 and is headquartered in Dallas, Texas. It is listed in the Chemicals sector of the NYSE. It currently has a market cap of $1.062 billion and an enterprise value of $1.177 billion, indicating low levels of indebtedness.

TiO2 is a white pigment playing a key role in the production of paints and coatings, plastics, papers, fibers as well as in specialties such as cosmetics, pharmaceuticals, glass, and ceramics. The principal natural source of titanium dioxide is mined ilmenite ore.

Their product is sold across the world, but Kronos’ customers are primarily based in Europe (45%) and North America (39%) . TiO2 is used in coatings (50%), plastics (29%) and paper (8%). The production of TiO2, as with most commodities, is fiercely competitive and cyclical. Their major competitors include The Chemours Company ( CC ), Tronox Holding PLC ( TROX ), Lomon Billions Group and Venator Materials PLC ( VNTR ).

The company is controlled by the descendants of the late industrialist Harold Simmons . The majority of the company is owned by Valhi ( VHI ) (50%) and NL Industries ( NL ) (31%), the latter in turn is also majority owned by Valhi (83%). Valhi is owned by Contran Corporation Investments (92%), which is the family’s investment vehicle.

Kronos is trading at approx. 0.59x Revenue/Enterprise Value, which is less than half that of their competitor Tronox Holdings. This multiple is also in line with their competitor Venator Materials. Venator Materials, however, is a much worse company. Over-indebted and nearing bankruptcy, Venator has a market cap of $41 million and an enterprise value of $1.036 billion. The last year the company posted a profit, was in 2017. In our view, Kronos should trade at significantly higher multiples than Venator.

Market Overview

While the market for TiO2 products is cyclical and volatile, research company Facts & Factors projects it to grow at a rate of 5.9% p.a. between 2021 and 2026, as the demand for coatings and cosmetics grows faster than the global GDP.

The market is expected to be worth $27.9 billion by 2026. Our calculations suggest that Kronos supplies approx. 9% of the global titanium dioxide demand. In the near term, however, volume demand for the products has softened given the fears about a global recession. At the same time, producers experienced considerable price inflation in costs for energy, materials, labor, and services during 2022. This put pressure on the industry.

It is not easy to ‘time’ the turn of the cycle, but our analysis of the capex cycles of the 4 large listed titanium dioxide producers revealed that the last 3 years' capex was approx. 20% lower than that of the preceding 3 years. Capex was also marginally below depreciation. This, we believe, indicates a relatively low level of replacement of supply, despite growing demand. Several competitors are also struggling financially. Most notably, Venator Materials is over-indebted and nearing bankruptcy. This might suggest that the turn of the cycle could be near.

Financial Results

The 2022 10-k was released earlier this month. The company reported a net loss of $19.9 million in Q4, which spooked the market.

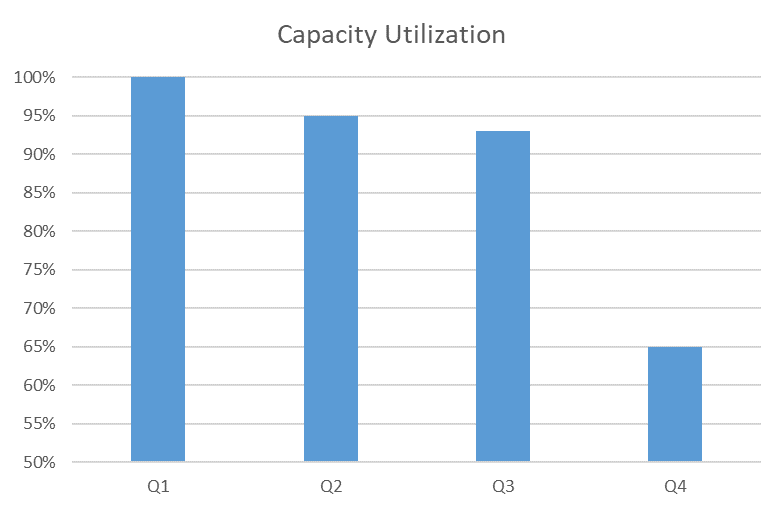

TiO2 sales volumes were a whole 40% lower in the fourth quarter of 2022 as compared to the fourth quarter of 2021, as businesses curtailed their spending and battened down the hatches as they expected a global recession. In response, Kronos dropped their capacity utilization to 65% in order to rationalize inventory levels.

{kind=link}

Capacity Utilization (10-K)

Average TiO2 selling prices at the end of the fourth quarter of 2022 was still healthy in our view, coming in 16% higher than the end of 2021. For the 2022 financial year, the group earned revenues of $1.9 billion, which was in line with their 2022 sales. However, margins came under pressure as the company struggled with high energy prices and freight costs. Our analysis suggests that the recent operating margins of 7% are very depressed, especially when compared to peak cycle margins of 28% in 2011 and 20% in 2017.

Operating Margins (Tikr)

Kronos posted an RoE of 10.9%. This is slightly below its long-term average of 11.1%. The lackluster RoE, we believe, is reflective of the competitive nature of commodity businesses. Cash conversion was also under pressure, as the group had built up inventory levels after depleting inventories in 2021. Current inventory levels (144 days) are slightly above long-term levels (127 days). The group’s balance sheet is however very healthy, currently holding $327 million in cash and with long-term debt of only $424 million. The group earned 8x its interest, even with depressed margins.

Assessment of Downside Risk

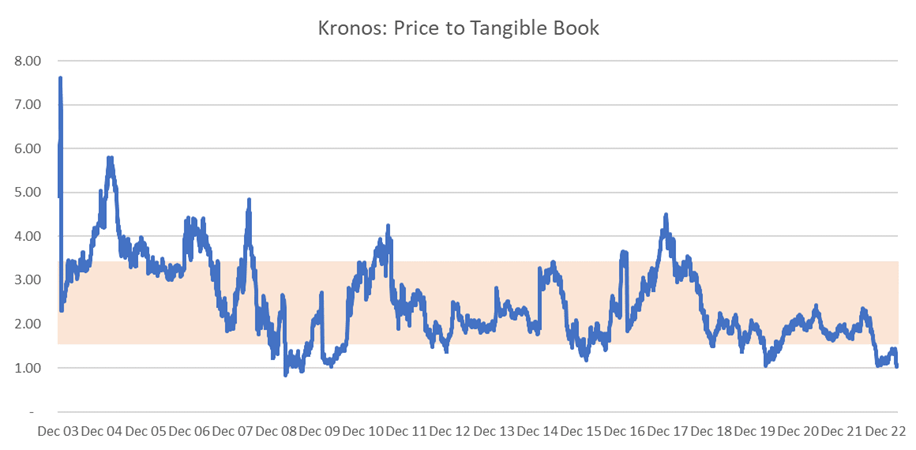

The core of Kronos’ attractiveness as a potential investment is that the downside risk is mitigated by a very low price relative to assets. Upside optionality will be provided if the cycle turns. The share price is currently trading in line with the tangible book value of the assets. The company has a tangible book value of $957 million, compared to a market cap of $1.062 billion. Tangible value primarily consists property, plant and equipment, as well as inventory.

Higher inflation rates globally suggest that the book value of the assets is conservatively valued. In our view, establishing a new plant today will cost significantly more than what it did historically. We believe buying the share near this value provides downside protection. History agrees with us. Since 2003, the company has only traded at a lower multiple of tangible book value 1% of the time over the last 20 years. Historically, such depressed multiples indicated that the bad news was priced in, and buying the share at these levels resulted in very good returns over the next 3 years.

{kind=link}

Price to Tangible Book Value (10-K, Tikr)

Will this time be different? As pointed out, we believe the business' balance sheet is strong enough to withstand the downturn in the cycle. We also believe that the cycle's turn is inevitable, because the products Kronos and its competitors make are absolutely necessary for several industries.

There are no substitutes for TiO2 in products such as paints and cosmetics. It is also a small part of the total cost of input for their clients. We are confident that the downturn is cyclical and not structural.

Assessment of Fair Value

We valued Kronos on a DCF basis. This is provided and discussed below.

{kind=link}

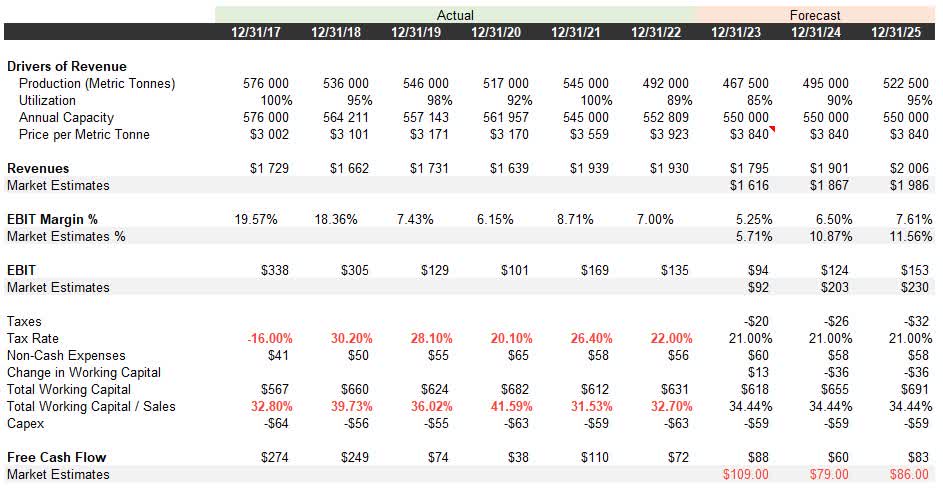

Kronos' capacity has been stable at around 560,000 metric tons per year for almost a decade. This is explained by their capex program, which only aims to maintain capacity and not expand. Historically, they have run at about 97% capacity. This dropped in 2022 due to the challenges discussed above. We believe that 2023 will still run at low utilization rates, because of the excess inventory that has to be worked out of the system. We expect utilization rates to normalize by 2025 as demand normalizes.

For the market price per metric ton, we have taken spot prices as they most closely reflect the current market environment and we do not believe we have an edge in forecasting commodity prices. Using these assumptions, our calculated revenue in 2025 is very close to the market's expectations.

The market seemingly expects EBIT margins to increase to 11.56% by 2025, but it is our view that this is too aggressive. We assume EBIT margins will continue to be under pressure in the next year, as low utilization rates lead to a negative impact through operational leverage. We expect margins to normalize to their long-term average of 7.6% by 2025. After adjusting for taxes, non-cash expenses, working capital changes and capex, we estimate free cash flow to be $88 million in 2023, $60 million in 2024 and $83 million in 2025. These estimates are conservative relative to the average of the market's estimates. Finally, we used these estimates to calculate our assessment of fair value:

Author's DCF Calculations

In line with history, we expect no capacity increases. We have assumed a perpetual growth rate of 4.5%, which aligns with our inflation expectations. Using our estimation of WACC, which we have cross-checked with industry standards we calculate a value of the firm of $1.77 billion. Adjusted for debt and outstanding share count, we arrive at an assessed value per share of $14.51. This compares to a market price of $9.08 at the time of writing, which leaves a 59.82% potential upside.

Other Factors

It is worth noting that analysts expect EPS of $0.42, $0.96 and $1.23 for 2023, 2024 and 2025, respectively. This implies a very bleak outlook for 2023, which we tend to agree with. We believe it is this bleak outlook and their emphasis on the short-term issues that lead to the share price offering value. The share is currently trading at 7 times 2025 earnings (as expected by the market). To give this some context: over the previous 20 years the company traded on an average multiple of 14x forward earnings.

The company is also trading at a significant discount to private market takeover comparables. In 2017, Tronox Limited agreed to acquire the titanium dioxide business of Saudi Arabian company Cristal for $1.67 billion. According to our analysis, this reflects in a 2x Price to Book Value multiple and 10x EV/EBITDA multiple. This is significantly higher than Kronos' 1.13x Price to Book Value and 6.4x EV/EBITDA multiple.

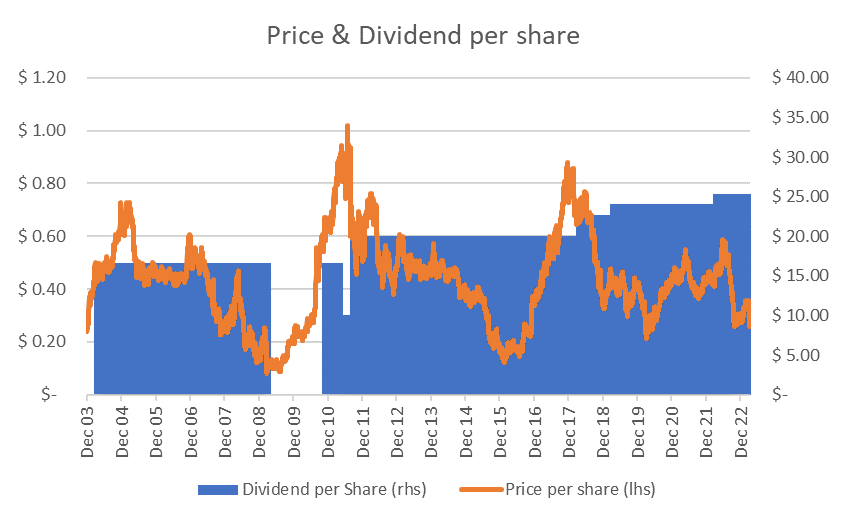

A benefit of having a controlling-family shareholder is that the company pays out 84% of its profits. Unlike many other commodity products, the family is not investing back into a below-average business. Capex typically matches depreciation. The company has also not issued shares over the past 10 years.

In the latest year, the company paid $88 million in dividends and spent a further $2 million on buybacks. The shares are trading on an 8.8% dividend yield, so investors are paid to wait the cycle out.

{kind=link}

Price & Dividend per Share (10-K, Tikr)

Risks

There is, of course, a risk that the dividend is cut to bolster the balance sheet in the event of a severe downturn. This previously occurred in 2008-2010. However, if you analyze the price per share from 2008 to 2011, Kronos came out of that crisis very strongly.

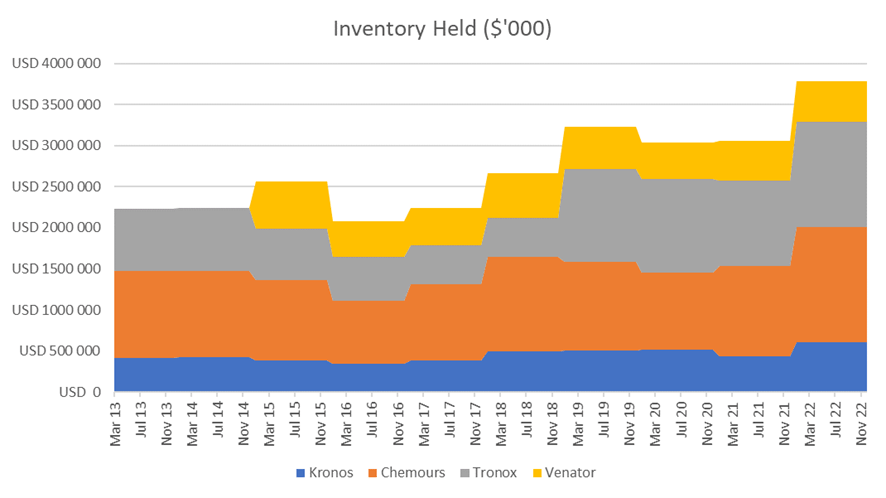

A current risk worth highlighting is the build-up of inventory in the industry. This was discussed above and is the result of a short-term decrease in demand. However, these inventory levels would need to be reduced before we can expect an uptick in the cycle. We will be monitoring this closely in the coming quarters.

{kind=link}

Elevated Inventory Levels (10-K, Tikr)

Conclusion

Kronos operates in a very competitive commodity industry, that is currently experiencing a downturn. The market correctly recognized the cyclical headwinds and punished the company's share price. We believe that, in doing so, the market might have overreacted.

The company is trading at record-low multiples of tangible assets, which should mitigate the downside risk. While waiting for an uptick in the demand, investors get rewarded with a handsome dividend. For investors who are comfortable investing in cyclical companies, we believe the share offers a good margin of safety and the possibility of an attractive return if the cycle turns. It remains one to monitor closely though, as this is an opportunistic trade.

For further details see:

Kronos Worldwide: Depressed Cyclical At Below Replacement Value