KRO - Kronos Worldwide Has The Cash To Survive This Cycle - But Will It Thrive?

2023-03-29 09:30:58 ET

Summary

- KRO is a conservatively financed TiO2 manufacturer paying a consistently high dividend with no long-term debt maturities until September 2025.

- Investors may be drawn to the company as it is cyclical trading around 52-week lows, but I believe shares are fairly valued at current prices.

- As the company is projecting worse operating results y/y, a better buying opportunity may be available later this year.

Executive Thesis

Kronos Worldwide ( KRO ) has been facing headwinds, with increased energy costs in 2022 eating into margins, and with a global economic slowdown decreasing demand for its products. As the chemicals industry is known to be cyclical, KRO trading at 52-week lows seemed of interest. Although the company offers an attractive and steady dividend, is conservatively financed and will likely sell its products for years to come, I would like a larger margin of safety before purchasing shares. Indeed, the company is projecting to operate at 80-90% of manufacturing capacity for the first half of 2023, when it has historically operated at or near 100% capacity in normal economic conditions. The market may offer a better buying opportunity later this year, if losses continue and the economic outlook does not improve.

Company Overview

Kronos Worldwide is a titanium dioxide manufacturer which operates multiple manufacturing plants in both Europe and North America. Titanium Dioxide (TiO2) is a chemical mainly used as white pigment for a wide range of products including paints, plastics, paper and even beauty products. The company considers the chemical a "quality of life" product because as countries become more developed, they tend to purchase more TiO2. The market of the product is also a good general barometer for the overall health of the global economy, as sales track global GDP growth . The company believes it is the lead provider of the product in Europe and also sells in North America and to a lesser extent the rest of the world.

The company produces the product in two different ways, a sulfate process, and a chloride process. The different processes require different inputs for production, and the sulfate process requires ilmenite and sulfuric acid. Of note, the company also operates an ilmenite mine in Norway, which it expects to be productive at least until 2050 allowing for vertical integration for years to come. The company also has a long-term goal of increasing chloride process production, as waste and energy use in this method is reduced.

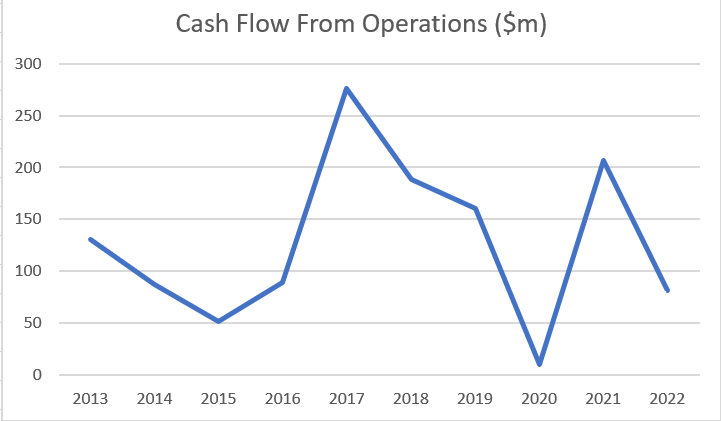

Well Covered Dividends

{kind=link}

As we can see from the chart above, dividend policy has been relatively conservative over the last 5 years, with surplus able to cover for years when the dividend is not covered by free cash flow. As the company has $327 million in cash and cash equivalents on its balance sheet, a current ratio of 3.8, and an unused $211 million revolver at the end of 2022, KRO can easily survive any prolonged downturn and even continue paying the dividend when running a deficit. It's worth noting, though, the company seems fiscally conservative and has $421 million in debt maturing in September 2025. Therefore, it might be prudent to suspend the dividend to allow for more flexibility in deleveraging and/or refinancing in this higher interest rate environment.

Competition Grows Slowly

Management believes one of their competitive advantages is their proprietary technology, the high barriers to entry into the industry, and the long lead times to construct new facilities. In monitoring their competitors, there has been minimal expansion of production other than with debottlenecking programs.

The company tends to spend around $15 million per year on research and development and $60 million per year on capex. Despite these investments in improvements, there have not been material increases in cash flow from operations over the years. This indicates that the company likely does not have a strong moat and must keep spending on improvements just to remain competitive.

{kind=link}

Of note though, one of their largest competitors, LB Group, is slowly growing capacity over the next few years with a target of 200 thousand metric tons of additional TiO2 production. For reference, KRO produces around 500 thousand metric tons of the product per year. If other larger competitors unexpectedly invest in greater production, this could erode KRO margins and return for shareholders.

Competitors (Kronos Worldwide 10K 2022)

Fairly Valued at Current Market Prices

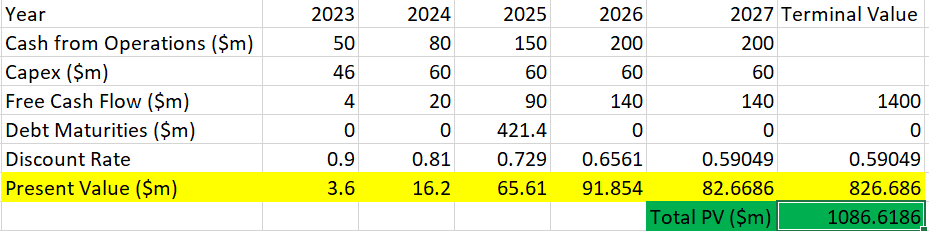

The company is projecting worsening y/y operating cash flow in 2023, related to macroeconomic headwinds affecting demand. The company also projected $46 million in capex in 2023, with $60 million being the typical amount spent in normal conditions. There are no plans for growth other than debottlenecking, which has historically not shown to be a significant driver of revenue or free cash flow growth for the company. Therefore, in my terminal value calculation, I assumed no growth. I believe a terminal value calculation is justified here, as the company will likely continue to operate for many years to come, as their products are industrially important, and demand is expected to increase. I projected a recovery to $140 million of free cash flow by 2026 as the economy recovers and the business normalizes, and that this would stay relatively constant on average over time. This is reflected in my model below, which puts fair value at approximately $1.1 billion or $9.40/share.

{kind=link}

Risks

No Plans for Growth

The company has no plans to expand capacity via new factories and insinuates it can remain competitive with current debottlenecking initiatives. As mentioned previously, one of their largest competitors is expanding capacity by 200,000 metric tons, and any further competition expansion could erode margins.

Large Established Competitors

Although it is unlikely that there will be new entrants into the field of TiO2 manufacturing, there are many other larger well-established competitors who are constantly researching and spending to improve efficiency and quality. Their largest competitor is Chemours ( CC ) a spin-off of the chemicals giant, DuPont ( DD ). This erodes shareholder value realization, as the company needs to spend just to maintain competitive operations.

Concentrated European Operations

The company is highly exposed to the European market, with 45% of 2022 sales in the region and 65% of production in the region projected for 2023. Any strength in the USD could adversely affect sales numbers but may be partially offset by reduced European operating expenses.

Energy Intensive

Manufacturing of the product requires a large amount of electricity and natural gas, so future climate change initiatives may erode margins, or require expensive changes in manufacturing processes. The company also cites increased energy costs in Europe as one of the reasons it reduced production capacity in the second half of 2022.

Conclusion: Fair Company, Fair Price

I would consider KRO a fair company selling at a fair price at the current market quotation of $8.75, with an estimated value of $9.40 according to our models. As the company is in an industry with high barriers to entry, and it manufactures an industrially important product, it's likely KRO will generate cash flow for investors for many years to come. The high (8.68% at the time of writing), historically well-covered dividend is a definite draw for income-oriented investors, and I think investing at current market quotations will do fine in the long run. That being said, the company is anticipating worse y/y operating income for FY 2023 concentrated in the first half, and it might be prudent to suspend the dividend temporarily. Investors may be able to purchase shares at discounted prices if this occurs, or if operating income is worse than anticipated this year.

For further details see:

Kronos Worldwide Has The Cash To Survive This Cycle - But Will It Thrive?