SKM - KT Corporation: Perhaps Not So Boring Anymore

Summary

- We believe that ARPU trend reversal and subsidiaries going public are catalysts likely to move the stock.

- KT is a cheap stock, likely due to the lack of exciting growth story. But things may soon change, thus providing an opportunity for investors.

- However, the lack of killer apps prevents users from seeing the full extent of 5G capabilities.

- Moreover, competition may intensify in high-growth businesses, such as the data center market.

Investment Thesis

5G reversing the declining ARPU trend and high growth subsidiaries going public might drive KT's stock price. In addition, KT's cheap valuation might present an opportunity at the current price.

Getting to Know the Company

Established in 1981, KT Corporation ( KT ) was once known as Korea Telecom Corp, a wholly government-owned telecommunications company. However, by 2002, the Korean government no longer owned the shares, and later the company changed its legal name to KT Corporation.

{kind=link}

Amid a prolonged period of stagnated growth, telcos, including KT, look beyond a traditional business model to drive their growth trajectory. For instance, KT plans to accelerate its transformation from a telco into the so-called digico (digital platform company) by developing high-growth businesses, such as cloud/IDC and AI Contact Center ((AICC)). As a result, the company aims to double its digital-related service revenue to $10 billion by 2025.

KT's Growth Strategies (Company)

{kind=link}

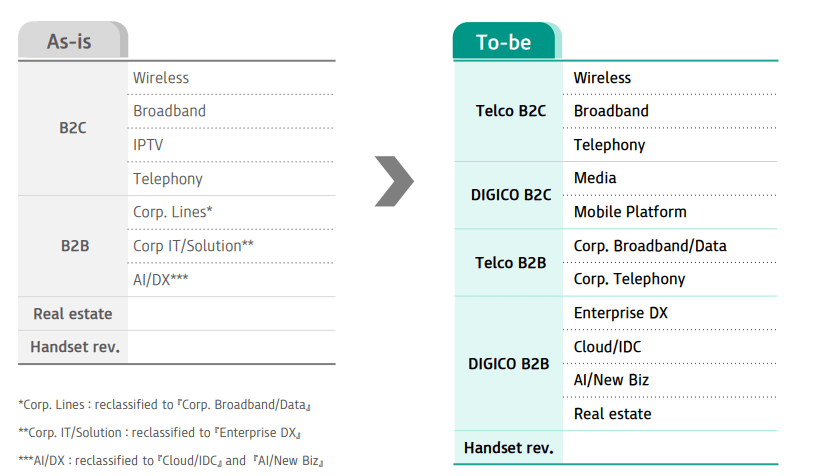

You can see in Figure 3 how KT reclassified its reporting structure to better reflect its growth strategies.

New Reporting Structure (Company)

{kind=link}

Moreover, KT owns a wide range of subsidiaries, including a credit card business (BC Card), a satellite broadcasting provider (SkyLife), and a real estate company (KT Estate).

What Moved the Stock?

KT's stock price was moving as if it was not going anywhere. It was trading at around $20-ish in 2011 before bottoming to below $7 in March 2020. Since then, the stock has picked up and is trading at $14 per share.

We compared the stock price with the quarterly service revenue change and found that tepid service revenue growth hampered its stock price.

Stock Price vs. Service Revenue Growth (Vektor Research, Yahoo Finance)

Although 4G technology rose in popularity in the early 2010s, ARPU has steadily declined because the OTT services overshadowed more expensive services, such as voice calls. Moreover, competition from MVNOs puts pressure on ARPU. Worse, telephony no longer serves as a primary communication medium, declining 9% annually from 2011-2021. And the stock price reflects the trend.

Wireless and Telephony Growth (Vektor Research)

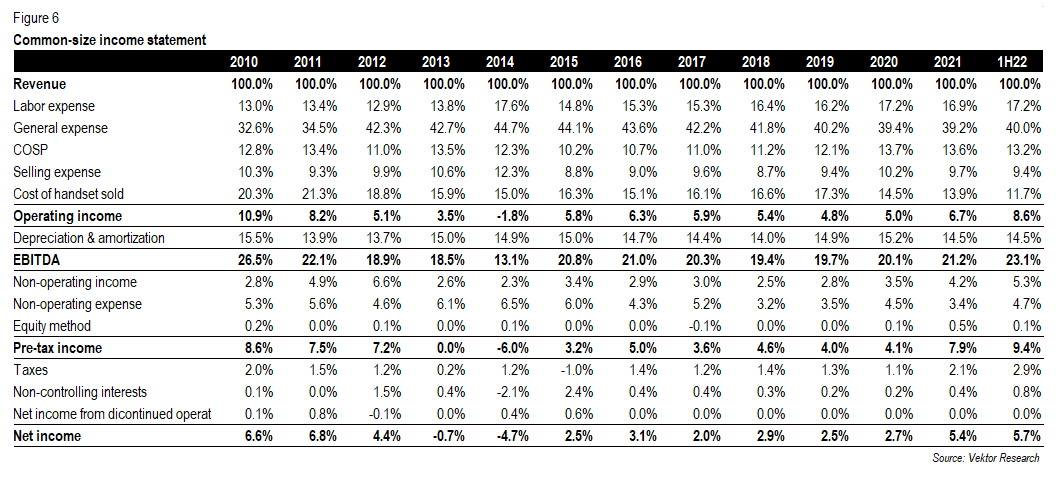

Moreover, our common-size analysis of KT's income statement suggests that increasing labor and G&A expenses put pressure on operating margins. In our view, tepid growth and operating margin erosion had made investors stay away from the stock.

Common-size Income Statement (Vektor Research)

{kind=link}

But now the share price has picked up. Is KT a BUY? We believe that there are three key points important for consideration.

1. 5G Underpinning ARPU Recovery

As we mentioned earlier, ARPU was in a declining trend. But we notice that it started to pick up in recent quarters thanks to users moving to 5G premium plans. In our recent article titled "SK Telecom: Looking Beyond the Traditional Business Model," we wrote that about a third of wireless subscribers were 5G users in Korea, thanks to aggressive rollout by operators. Please read our article for more analysis on the wireless industry in Korea). Such efforts started to bear fruit as more users adopted 5G, and operators began to reduce their marketing expenses.

ARPU Started to Pick Up (Companies)

And now, the idea is to offer more differentiated 5G plans to consumers to increase adoption further. For example, SK Telecom (NYSE: SKM ), or SKT, offers 5G plans ranging from KRW40,000 to KRW90,000 to "cater to more customers' needs."

When asked about the possibility of a 5G mid-range pricing scheme, CFO Young Jin Kim said that KT is also preparing for such a scheme to "provide more choice, more expanded choice to the customers." While 5G subscribers will likely downgrade to more affordable plans, such a strategy will further ramp up 5G adoption. SKT's CFO Jin-won Kim also acknowledged that customers could downgrade to lower plans as more price plans are available, but added that the more critical part is accelerating 5G migration.

In the near term, we believe that the 5G mid-range pricing scheme might slow ARPU recovery in exchange for more 5G adoption. But long-term, ARPU should improve, as the appetite to move to premium plans is already there, in our view. For example, KT recorded positive wireless ARPU yearly growth for six consecutive quarters, and SKT followed behind with five quarters (see Figure 7).

Nevertheless, the full extent of 5G capabilities remains unseen thanks to the lack of killer apps. For example, when 4G came around, YouTube and Instagram were gaining popularity, and leveraging 4G plans to access those apps makes sense. Thus, we believe that once those killer apps are widely available, consumers will be willing to pay more.

2. Unlocking Subsidiaries' Value Through IPO

During the 2Q22 earnings call, the CFO believes that B2B business is a "very critical growth driver for the company." He went on to mention three growth strategies through B2B:

The first one is expanding into a new business area by adding digital on top of our telco capabilities. Second is to gain an upper hand and dominance in the DX market, DXI, the different businesses and companies by really tapping into the digital segment where we could actually leverage the potential that we have with the strong underpinning of our telco capabilities. And third is providing a customized DX model by providing a differentiated offering for each of the customer segments.

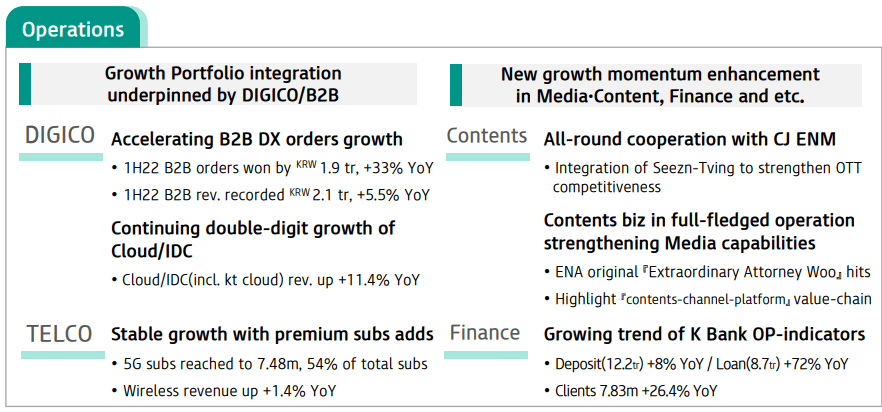

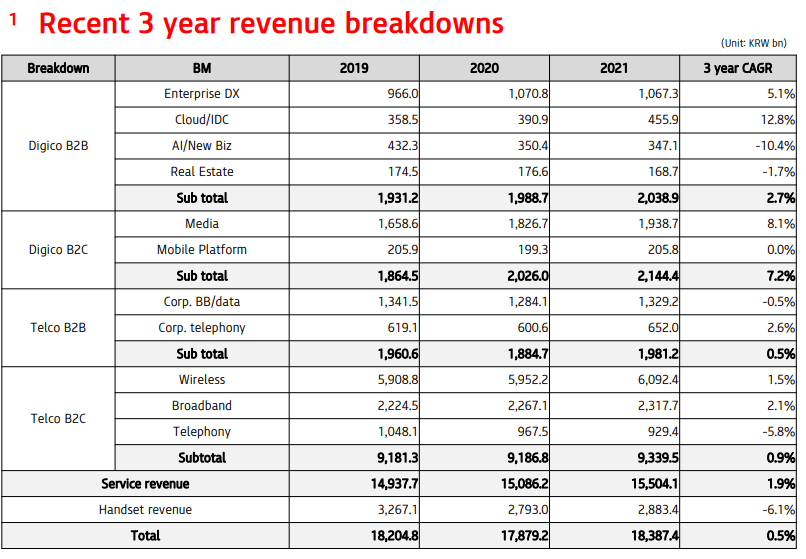

Digitalization remains the core theme of KT's growth strategy. For example, in the last three years, Digico B2B and B2C businesses drove KT's service revenue (see Figure 8).

3-year Revenue Breakdown (Company)

{kind=link}

To cater to surging data demand, KT builds data centers, operating 14 IDC in Korea. Although the Cloud/IDC business only contributed about 3% to KT's service revenue in 2021, it drove revenue growth (see Figure 9). KT Cloud aims to grow its revenue from KRW460 billion to KRW2 trillion by 2026, implying a 34% annual growth. But investors should not immediately take it at face value, as KT's data center business is growing only ~13% per year.

IDC/Cloud Contribution to Service Revenue Growth (Vektor Research) Revenue from IDC/Cloud Business (KRW Billion) (Companies)

Earlier this year, KT decided to spin off the IDC/Cloud business into KT Cloud, hoping for it to be "more competitive in the cloud and data centers market." And further expansion is underway. For instance, KT Cloud is building a 26 MW hyper-scale data center in Seoul, aiming to develop additional 100 MW data centers by 2025.

As cited in the Korea Economic Daily , AWS took over half the cloud market share in South Korea, followed by KT Cloud with 20%. And selling a minority stake to a strategic partner or going public is on the cards.

Unlocking subsidiaries' value through IPO seems to be KT's plan. Another example is KT's efforts to push its digital banking unit, K Bank, to go public this year, possibly raising $10 billion. SK Group also seeks to execute a similar strategy by listing SKT's cybersecurity spin-off, SK Shieldus ($2.79 billion), and mobile app store One Store ($149.9 million). By contrast, the IPO was cancelled due to "weak investor interest."

We like KT's strategy because it allows the high-growth subsidiaries to become more independent, and more money from IPO will help them expand their businesses.

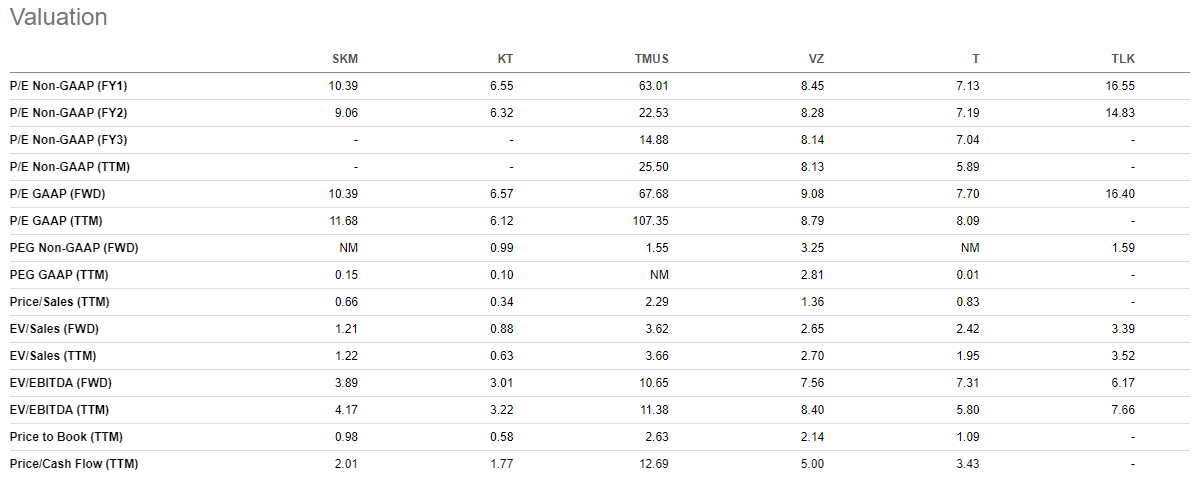

3. Cheap Valuation

KT's forward EV/EBITDA and P/E stand at only 3x and 6.6x, respectively, obviously a bargain compared with its peers. Indeed, stocks are cheap for a reason. But as mentioned before, 5G reversing the ARPU trend and subsidiaries going public might drive the stock.

Multiple Valuation (Seeking Alpha)

{kind=link}

Figure 10 shows that the market was paying more than $20 per share with the same EPS as now. But the difference is that KT only trades at ~$14 per share. Thus, at the current price, KT might present an opportunity.

But one may ask why these catalysts have not yet been fully priced into the stock. In our view, compared with its significant investment, 5G only slightly drove telcos' revenue, and only recently, ARPU finally went up. While the ARPU trend reversal is a good sign, we believe that consumers will realize the full extent of 5G capabilities once killer apps are available. But as we wrote in the "What Could Go Wrong?" section below, the question of when those apps will be available remains.

Second, KT's plan to unlock its subsidiaries through IPO has not yet materialized. And it remains to be seen whether those businesses can maintain their growth trajectory after IPO.

Financial Analysis

KT and SKT have comparable revenue growth at 4%. However, please note that SKT's figure in 2020 was before the horizontal spin-off, resulting in negative growth in 2021. In 2Q22, KT slightly edged its competitor with 4.7% (Y/Y), higher than its 10-year historical revenue growth of 1.6% per year.

Revenue Growth (Companies, Vektor Research)

However, EBITDA margin-wise, SKT led the pack, while KT was at the bottom, especially in 2Q22, when KT's margin dropped. Labor and general expenses were the main culprits behind margin erosion.

According to KT's CFO, the cloud and IDC business typically generates above-average margins. But as demand surged, the company hired more employees, dragging down margins.

EBITDA margins (Companies, Vektor Research)

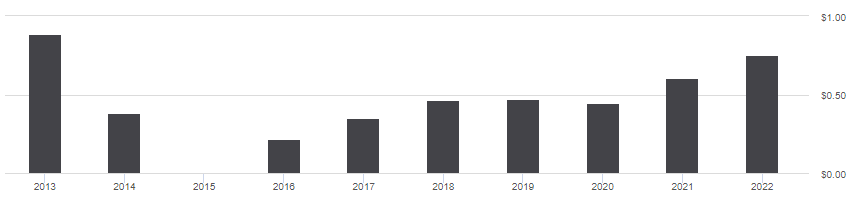

KT has been a consistent dividend payer for seven years, with an excellent 5% yield. However, SKT has been a more consistent free cash flow generator than KT in the last ten years.

KT's Dividend per Share (Seeking Alpha) FCF (KRW Billion) (Companies, Vektor Research)

{kind=link}

What Could Go Wrong?

Unavailability of Killer Apps to Fully Leverage 5G Capabilities. The appetite to move to premium plans is already there. But the full extent of 5G capabilities has not yet been felt by consumers. The question remains of when the long-awaited killer apps will be available.

More competitors in the growing businesses. Like KT, other telcos are also focusing on high-growth digital businesses. For example, SKT established the AIVERSE business, which includes subscription and metaverse businesses. Moreover, as data demand surges, competitors are looking to enter the Cloud/IDC market. As a result, as the Korean Data Center Council put it, the Korean commercial data center market is likely to transform into a fragmented one, with intensifying competition among operators.

Recap

KT's stock price has been going nowhere in the last few years. Indeed, a tepid growth rate and declining operating margins have hampered the stock, in our view. But soon, things might change. First, 5G users migrating to premium plans have reversed the declining ARPU trend, which should help drive KT's service revenue growth. But, in our view, the full extent of 5G capabilities has not yet been felt due to the lack of killer apps. Second, unlocking subsidiaries' value through IPO should benefit KT as they will become more independent, and more money will help their expansions.

Lastly, we believe that KT's valuation is cheap. Although the low multiples are due to a lack of exciting growth story, investors should start considering KT. For now, we assign a HOLD rating for KT before we come up with a target price. If you have any thoughts, please do not hesitate to comment below.

For further details see:

KT Corporation: Perhaps Not So Boring Anymore