KUBTF - Kubota: Caution Warranted Heading Into An Industry Slowdown

2023-05-25 13:03:10 ET

Summary

- Kubota posted solid headline numbers in Q1.

- But fundamental concerns remain, particularly in North America.

- The stock’s YTD rally has priced in a lot of optimism, leaving more downside than upside from here.

Japan's leading farm machinery producer, Kubota ( KUBTY ), posted a mixed quarter despite the industrial headwinds globally. While strong wholesale sales numbers were the key highlight in Q1 , higher fixed selling costs and an unfavorable shift in the overall product mix clouded the profitability result. Also concerning are elevated dealer inventory levels, particularly for compact tractors, which will need to be cleared at some point. So even if wholesale sales continue to rise through the rest of the fiscal year, an eventual cutback of inventories (likely from FY24 onwards) poses a downside risk to the wholesale revenue growth algorithm. Continued North American weakness leaves Kubota’s full-year guidance (unchanged post-Q1) exposed to downward revisions should the yen-related tailwinds reverse in the coming months.

While the company’s ambitious long-term targets (RoE >10% and total capital return payout of up to 50%) are a step in the right direction, it hasn’t yet made meaningful progress toward achieving these numbers, particularly in key growth markets like North America and China. At the current low-teens P/E, the market seems a tad optimistic despite the weak manufacturing backdrop globally; hence, I would remain sidelined pending a meaningful pullback.

North American Weakness Clouds the Q1 Headline Result

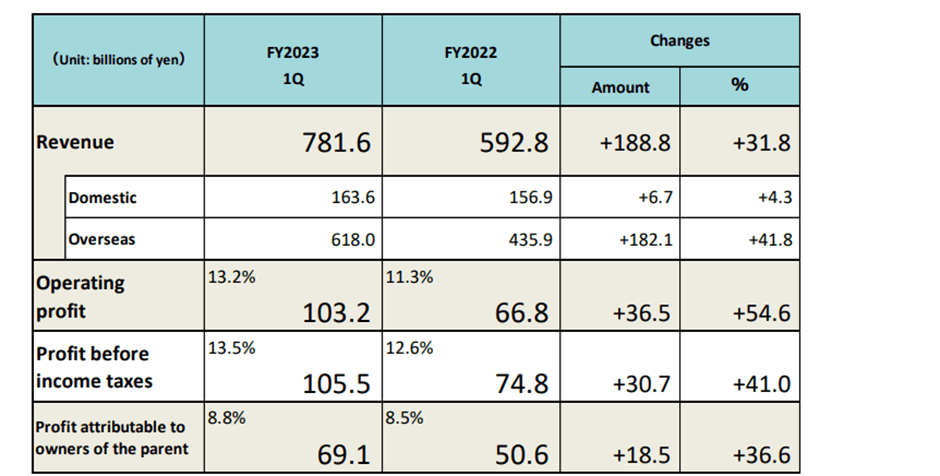

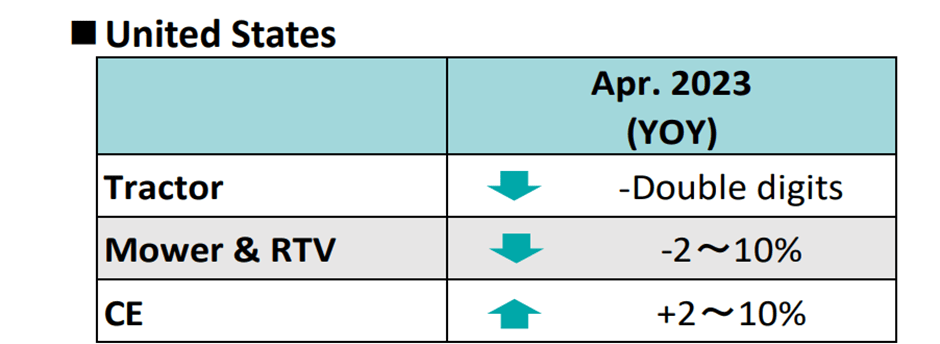

Headline Q1 sales were higher across the board for Kubota, driving operating profit growth of +55% YoY to JPY103bn. Digging deeper, however, there were spots of weakness in North America, the company’s biggest regional market, on the back of a deteriorating housing market and unfavorable weather-related seasonality. While overall retail volumes were down 4% YoY for the region, the housing-related categories saw the steepest declines at -12% YoY for compact tractors, followed by medium-sized tractors at -6% YoY. The construction side provided some offset at +15% and +20% for construction machinery and utility vehicles, respectively, though the downturn in manufacturing PMIs means caution is warranted on the outlook.

{kind=link}

Kubota

Also worth noting is the rising dealer inventory across Kubota’s businesses. The issue is particularly acute in small and compact tractors, where inventory is now running above pre-COVID levels. While some of the North American inventory build-up is likely down to logistics, it does raise the risk of inventory de-stocking going forward. The double-digit percentage decline in North American tractor volumes cited in the April monthly retail sales report is an early warning sign, in my view. Without a material improvement in leading indicators (e.g., manufacturing PMIs, which are running <50 in North America, Europe, and China), I suspect volumes will continue to disappoint.

{kind=link}

Kubota

Ambitious Mid to Long-Term Business Targets at Risk

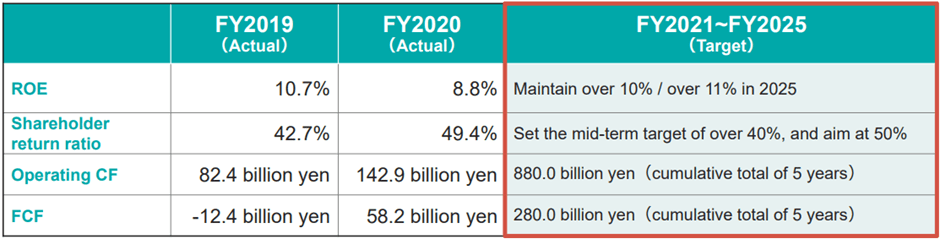

The North American weakness has negative implications for Kubota’s Mid-Term Business Plan 2025 and long-term targets through 2030, in my view. To recap, the 2025 plan outlines a five-year blueprint (i.e., over the 2021 to 2025 period) to achieve JPY2.3tn of revenue and operating profits of JPY300bn by 2025, setting the foundation for the 2030 targets. Additionally, management has pegged its cumulative free cash flow generation target at an ambitious JPY280bn and ROE of >11% (vs. 9-10% currently). The profits will be funneled into capital returns at a payout ratio of more than 40% through 2025 and up to 50% long-term. Assuming the company maintains its ~30% dividend payout, this would imply a 10-20% buyback allocation and further upside to the JPY 20bn buyback run-rate announced last year.

{kind=link}

Kubota

The key issue is the ambitious assumptions underlying Kubota’s mid-term plan. For one, management has called for a further expansion of construction machinery in North America across both compact and large-sized products (vs. mainly compact construction machinery currently). Management is also looking to replicate its Southeast Asian playbook (where its dealer network is a competitive advantage) via a localized and integrated supply chain to gain market share. But Kubota’s progress has been slow thus far, as its durability advantage in compact, low-horsepower products hasn’t quite translated into success at the higher end of the market. The declining North American retail volumes in Q1 don’t bode well for its ability to withstand a global manufacturing slowdown either. With US homebuilding likely to be pressured by higher rates for a while, the outlook is challenged.

{kind=link}

Kubota

FX Tailwind Poised to Ease, Weighing on Profitability

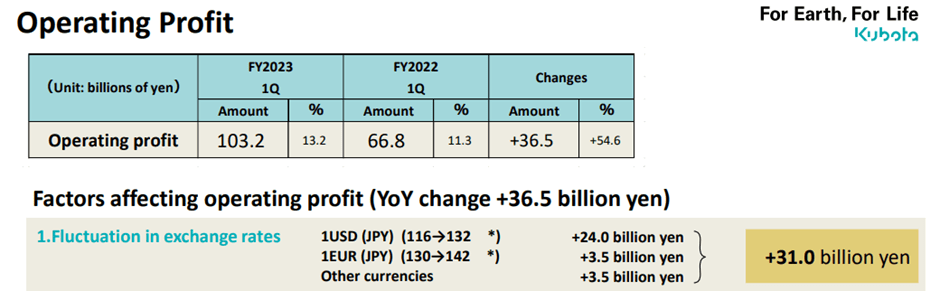

Japanese machinery stocks have been a surprise outperformer this year, and Kubota has benefited from the tailwind, rising in the low teens percentage YTD. While the fundamentals have played a part, a deeper look at the P&L drivers reveals that the weak yen has been a major contributor. Kubota’s Q1 report, for instance, revealed a JPY31bn gain from exchange rates (JPY24bn from the USD/JPY and JPY3.5bn from the EUR/JPY trend); excluding this one-off benefit, operating profit would have been flat YoY.

{kind=link}

Kubota

Kubota’s management team has set its FX assumptions for this year slightly lower than spot at JPY125/USD, so if the yen remains weak, expect more beat-and-raise quarters ahead. The inverse is also true, though, and an eventual reversal in the USD/JPY could result in earnings downside. Also concerning is how much additional leeway Kubota will have with regard to price hikes – with the yen already weakening significantly YTD and the new BoJ governor signaling toward policy changes ahead, the company’s earnings momentum may have peaked. And even if more guidance hikes do come through post-Q1, the stock price rally this year implies a fair bit of optimism is already priced in.

Caution Warranted Heading into an Industry Slowdown

Kubota may have delivered strong wholesale revenue numbers in Q1, but the near-term outlook is far from rosy. On the revenue side, dealer inventories remain a concern at the current high levels, leaving Kubota exposed to top-line pressure when dealers start their de-stocking cycle down the line. The broader North American market environment also remains weaker than management expectations, yet, Kubota has left its full-year guidance unchanged. Any near-term downside will have negative implications for the mid to long-term plan (RoE target of >10% and up to 50% capital return payout), while continued struggles outside of its Southeast Asia stronghold will weigh on its outlook as well. The valuation doesn’t offer much on the risk/reward front either at ~13x earnings and will be vulnerable to further downside should the slower manufacturing backdrop persist through the coming months.

For further details see:

Kubota: Caution Warranted Heading Into An Industry Slowdown