KHNGF - Kuehne + Nagel: A Solid Company With A Fair Price Tag

Summary

- FY2022 results were outstanding.

- The company is being run very efficiently and profitably.

- DCF model with a recessionary environment implemented shows that the company is fairly valued.

- There could be a better entry point due to the uncertain economic environment.

Investment Thesis

With the release of what I would consider very good full-year financial results , I wanted to take a look at Kuehne + Nagel International AG ( OTCPK:KHNGY ) in more detail to see what the future might look like for the company with all the macroeconomic uncertainties and how its revenues might be affected if we do see a recession coming in the next year or two. I have modeled a 10-year DCF valuation, taking into account current revenue growth that the company has achieved and modeling a recession for the next 3 years and then a recovery, with all these assumptions inputted, I would not be opposed to starting a position in the company at these prices, however, there may be more uncertainties in the future that can bring down the price a bit more, giving a better entry point.

Revenues Depend on the Future of Logistics

It seems that the company had a very good FY2022, with revenues increasing by 20% y-o-y, suggesting the industry is doing very well, but can this be sustained going forward with all the economic tightening? In this article, I propose a different view where the growth will stall for a bit because of a recession, which brings down revenues for the next two years and recovers later on. There are many different opinions on what the future of logistics looks like. Some say the demand will fall due to rising fuel costs, rising tensions that can divert trade and affect supply chain stability, lack of automation and standardization, and environmental impacts and sustainability issues.

On the other hand, there are opportunities for the digitization that streamline the experience for customers, leveraging data analytics and artificial intelligence, continuing rise of e-commerce and online shopping with fast deliveries can fuel the growth even further.

The pandemic lockdowns might have helped fuel a boom in online shopping, which brought in over $4.28T in 2020, $4.9T in 2021, and is expected to be around $5.42T in 2022 and over $7T by 2024. The lockdowns have altered the culture of shopping more towards e-commerce and it seems like everyone likes it this way more as logistic companies become more efficient over time. I recently had to get some documents mailed from Europe to Mexico, I got them within 3 days!

I expected a slowdown in online shopping in 2022 with more people being allowed to leave their homes and shop in person, but that did not seem to be the case. It seems like the new normal is going online shopping.

The company has also unveiled its successor to The Roadmap 2022, which was a massive success. The Roadmap 2026 will aim to strengthen the company's earnings power and will focus on 4 main sectors of development and improvement, the customer experience, the competitive advantage of digitization which has played a big role in revenue generation, sustainability solutions, and further growth plans that will focus on high-margin services.

There is a lot of positivity in the logistics industry in the future, and it outweighs the negative in my opinion. With everything that has happened in 2022, the company still managed to deliver very good results. The Ukrainian crisis over the last year did not seem to make a huge impact. The industry seems to be very resilient.

However, I do not want to be an optimist. My style is more conservative when it comes to the valuation of companies and I will proceed with a bit more caution when considering what will happen in 2023 and 2024 in terms of interest rate hikes and a potential recessionary period.

Financials

The company has amassed a good chunk of cash over the year and still has a very small amount of debt on the books. The company could get involved in some M&As with that amount of cash, however, they did mention they will be quite selective in the process as the company mentioned they are focusing on organic growth, digital transformation, and other long-term strategies to enhance customer experience and sustainability.

{kind=link}

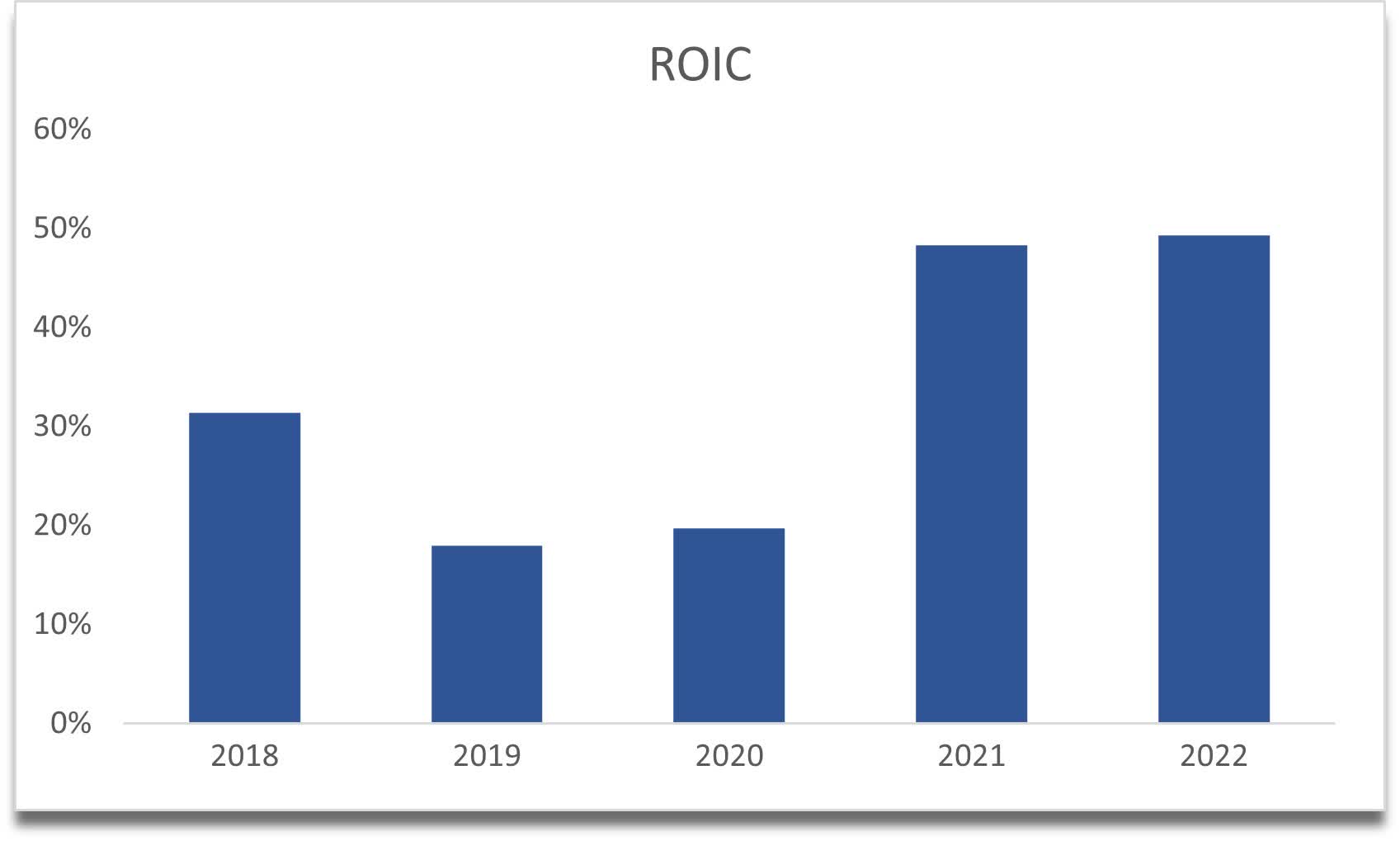

The low cash ratio does not bother me because they have been achieving outstanding figures on profitability and efficiency, mainly ROIC and ROCE.

ROIC has been hovering around 48% in the last 2 years and ROCE well over 200%. ROCE saw a huge increase in 2 years. These are amazing numbers, and I would pay a premium to own a company that is as efficient as Kuehne + Nagel.

ROCE (Kuehne + Nagel IR website)

{kind=link}

FY2022 saw growth in EBIT of 28% while revenues grew by 20%. The company has managed to reduce costs and other operating expenses which helped it achieve such a great result.

{kind=link}

The company also achieved a conversion rate of 34% which was well above their target of 25%-30% by 2026 and well above the 16% that they wanted to achieve by 2022.

The conversion rate measures how efficiently the company converts its revenue into profit after paying for operating expenses. A higher conversion rate means higher profitability.

One thing to note is that back in Q3, the management said that the median EBIT estimate for 2023 of CHF2.3B is conservative, which looks like they are right as they have been beating expectations all year long, I would expect EBIT to come in at higher than CHF2.3B.

These metrics tell me that the company is very well managed and does demand a premium in my opinion. The company is very efficient in using all of its resources which will translate into a higher value for shareholders in the future.

DCF Valuation

I approached this model with more of a conservative outlook than what I have outlined above in terms of how the logistics industry will grow in the future. I will rather be more conservative than overpay for a great company, which would lead to suboptimal returns.

With that said, the first two years of revenue growth sit at 5% indicating a slight slowdown in growth due to some economic factors but then picks back up to around 8% and levels off at around 4% for the rest of the years giving me an average growth for the next 10 years of 5.6% for the base case outcome.

I also wanted to include what would happen if we do see a recession in the next 12-24 months. For this outcome, seeing that in the last 10 years, the company only experienced 3 declines in revenue, I went ahead and modeled similar for the next 3 years, where the revenues decrease by 7% in 2023 and 2024 and decrease by 5% in 2025 and then increasing by 10% for the next couple of years and slowing down to mid-single digits for the remainder giving me 2.6% average growth.

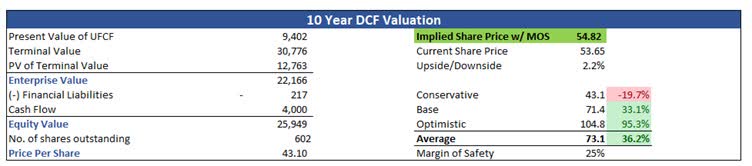

To give me a range I also modeled a simple optimistic case that grows at an average of 7.7% a year for the next 10 years, slightly higher than the base case. On top of these estimates I also like to put in a 25% margin of safety on the final valuation and with that, the company's implied share price is $54.82, which means the company is fairly valued at these conservative estimates.

{kind=link}

Closing Remarks

As I said at the beginning of the article, I would not be opposed to starting a position at these price levels. The company seems to be running very smoothly and the management is very capable of running it. There are quite a few optimistic scenarios out there that can propel the revenue growth of the company further, with the implementation of advanced technology which will further improve efficiency. The company has already beaten its own goals for 2022 by a long mile, they could probably do that again by 2026, if everything goes according to plan.

What can stop me from investing in the company currently is the uncertainty of the macroenvironment globally, which can affect growth in many different ways. The next year or two will be crucial, and I am fine with waiting it out a little bit as the stock markets may continue their leg down yet again and could provide a great entry point for new investors and long-time investors alike. I have the stock on my watchlist and I will keep watching the global economy like a hawk as I would like to have some certainty that the inflation rate is actually coming down to decent levels and that interest rate hikes will level off and come down, but right now I can wait.

For further details see:

Kuehne + Nagel: A Solid Company With A Fair Price Tag