KHNGF - Kuehne+Nagel: Not Getting Enough Credit

2023-07-28 16:44:26 ET

Summary

- Kuehne+Nagel is the world's number one sea and air freight forwarder, providing specialized solutions globally.

- We are drawn by the structural increase in demand for complex logistics solutions, the supply chain restructuring theme, and the potential for margin expansion outlined by the management.

- Kuehne+Nagel has set ambitious goals in its Roadmap 2026 CMD, which are not reflected in current market expectations in our view.

We present our note on Kuehne+Nagel (KHNGY), a global transport and logistics company based in Switzerland. We are drawn by the structural increase in demand for complex logistics solutions, the supply chain restructuring theme, and the potential for margin expansion outlined by the management. Moreover, we believe the market is not properly giving enough credit to the ambitious targets announced by the company. In this note, we will provide a brief overview of the business, analyze key issues and drivers, and assess the implications for investors.

Introduction to Kuehne+Nagel

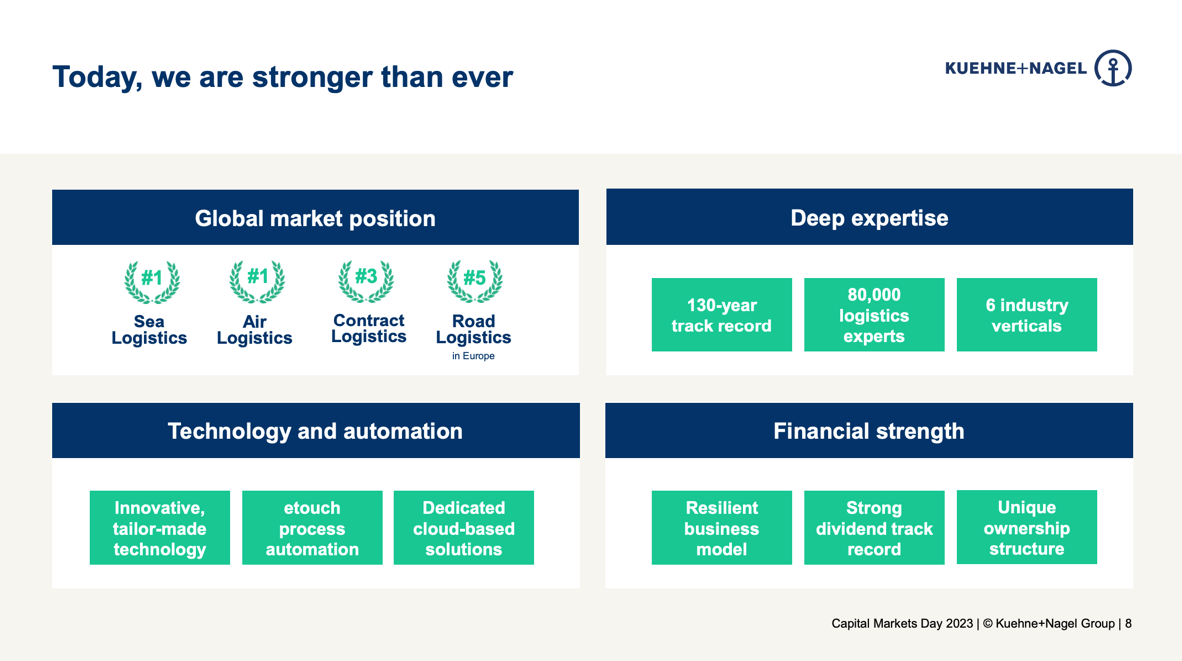

Kuehne+Nagel was founded in 1890 in Germany, and over the last 130 years has evolved from a traditional shipping company to a logistics partner offering specialized solutions globally. Kuehne+Nagel provides sea freight and air freight forwarding, contract logistics (warehouse management), and overland services. It is present in nearly 1300 locations all over the world connecting 100+ countries through its network and serving 400k+ customers. Kuehne+Nagel is listed on the SIX Swiss Exchange and has a market capitalization of CHF33.5 billion. It has a history of long-term value creation for shareholders, producing low double-digit total shareholder returns over the last 10 years. The Kuehne family remains the majority shareholder with Klaus-Michael Kuehne, the grandson of the founder, owning 53% of the shares, and the Kuehne Foundation holding 4.7%. The rest is free float.

The World’s Number #1 Sea and Air Freight Forwarder

Forwarders are asset-light businesses that do not own airplanes, ships, or trucks. They make supply chains flow and provide solutions for a variety of customers. The business relies on human resources rather than hard assets. Employee numbers are adjusted to address market dynamics. Forwarders have less earnings volatility, less fixed costs, and less operational leverage, and are better suited to navigate downturns without facing significant losses.

Kuehne+Nagel is focused on sea freight and air freight forwarding, which constitute ca. 80% of Group EBIT, and it is the global leader in terms of volume in both verticals. Before the acquisition of Apex , a Chinese air freight forwarder in a $1.5 billion deal in 2021, Kuehne+Nagel was larger in sea freight but now there is roughly an even split in terms of EBIT. In terms of sea and air freight market shares, Kuehne+Nagel is closely followed by DSV and DHL. The wave of M&A following the pandemic further consolidated market shares.

Q2'23 Results

Kuehne+Nagel reported solid Q2 results beating consensus expectations, with the main driver being Sea Logistics. Gross profit came in at CHF3.2 billion, as Air Logistics volumes fell 15% YoY and Sea volumes were flat. Sea Logistics reported better than expected volumes, yield, and lower costs. Traditionally the company does not provide any FY guidance but we believe this outperformance should drive sell-side consensus expectations for full-year results higher.

Roadmap 2026 - Company Website

{kind=link}

Investment Thesis

We are constructive on the structural outlook for freight forwarding demand. After the supply chain disruptions caused by the pandemic, as geopolitical tensions arise and the West decouples from China, many investors are concerned about the implications for freight forwarders. We see this as an opportunity . Despite the shorter distances, complexity should rise, which is a net positive for freight forwarders specialized in providing solutions and navigating complexity. Demand for forwarding depends more on the number of movements and complexity rather than the distance traveled. As more flows need to be processed and there are more issues to be solved i.e., more borders to cross, more documents to file, etc., forwarding services become more necessary.

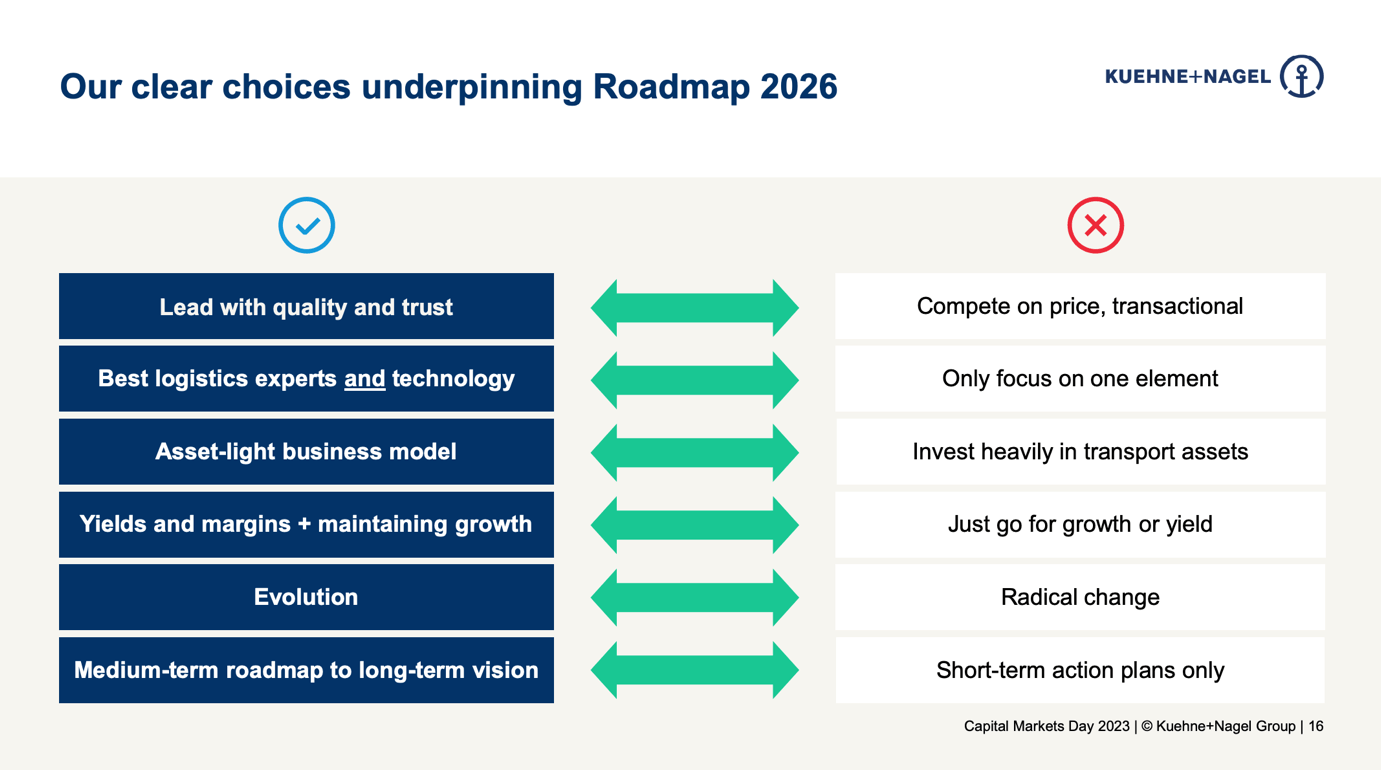

Kuehne+Nagel has been focused on volume growth rather than superior unit economics over the last decades, unlike its peer DSV. However, it is now implementing a new strategy shifting its focus to the Kuehne+Nagel Experience, driving gross income per TEU up. We believe the company is fully capable of delivering a service superior to peers and shifting towards higher value-added / less menial activities which are pricier and more profitable. This shift should also be supported by digitalization and improved technological capabilities, especially eTouch , reducing time spent on simple chores and allowing employees to solve more complicated problems more efficiently, and add more value.

We would like to note that the performance of Kuehne+Nagel is not only dependent on freight rates but depends more on the complexity of the logistics problems that need to be solved and the value added in the process by the forwarder. There was a spike in forwarders’ profits during and after the pandemic as supply chains unraveled. We believe this was also due to the complexity, severity, and number of supply chain problems that needed solutions, rather than due to the increase in freight rates. Simply put, the gross profit does not depend only on a markup percentage but on value-added. Eventually, as supply chains get more complex, and managers become more prudent in managing their supply chain risks, we believe forwarders will be a net beneficiary.

We are encouraged by the ambitious goals set in the Capital Markets Day – Roadmap 2026, which emphasize trust, customer, and employee experience. The company aims to drive EBIT growth higher mainly through providing an extraordinary customer experience that will lead to a higher margin especially from small and medium enterprises, less customer attrition, lower costs per transaction driven by digitalization, and growth in new markets. As per the guidance, EBIT should be in the range of CHF3.3+ billion by FY 2026. This is not reflected at all in sell-side consensus estimates which fail to give any credit to the plan announced by the company. Historically, Kuehne+Nagel has not underdelivered, and management is well-respected. We do not assume full achievement of the goals as we would like to see a “derisking” first, but we have higher forecasts than consensus.

Roadmap 2026 - Company Website

{kind=link}

Valuation

We forecast CHF2.8 billion of EBIT in 2026 or an average EBIT incremental improvement of CHF250 million per year from FY 2023 – which we forecast at CHF2.05 billion, vs a target at midpoint of ca. CHF3.3+ billion and vs. a 2022 EBIT of CHF3.8 billion. Our EBIT assumption is driven by modest top-line growth combined with margin expansion. We are 15% below the company’s midpoint target and still below the lower-end target.

Historically Kuehne+Nagel has been trading at a median of nearly 16x EBIT. By applying this multiple we arrive at an enterprise value of CHF45 billion in 2026. Using an equity risk premium of 6%, a risk-free rate of 2%, and a beta of 0.8, we get a cost of equity of 6.8%. As the company has a net cash position, we will apply the cost of equity as cost of capital. Discounting to the present, we arrive at an enterprise value of CHF37 billion. We add ca. CHF2 billion of net cash and get a market capitalization of CHF39 billion. This implies 17% upside and a share price of CHF323 / share or $372 / share.

The stock has done very well YTD and is up 26% like its main peer DSV. We believe there is still upside left.

Risks

Risks include but are not limited to a macroeconomic downturn, failure to properly integrate Apex after the incentive scheme period, an underperformance in growth due to the focus on profitability, inability to deliver on margin expansion targets, a decline in freight rates, increased competition, deglobalization, etc.

Conclusion

Based on what we believe is a misperception of the business model and the stock, combined with strong underlying fundamentals, an ambitious self-help program, low consensus expectations, and a compelling, although not screamingly cheap, valuation, we rate Kuehne+Nagel as a Buy.

For further details see:

Kuehne+Nagel: Not Getting Enough Credit