KLIC - Kulicke And Soffa: High-Quality Business Experiencing Severe Headwinds

2023-07-31 15:18:26 ET

Summary

- Kulicke and Soffa Industries is a high-quality business with solid revenue growth, profitability metrics, and a strong balance sheet.

- The company faces severe headwinds due to a challenging macro environment and difficult comps after a revenue spike in 2021.

- Valuation analysis suggests minimal upside potential, making it advisable to wait on the sidelines and assign a "Hold" rating.

Investment thesis

Kulicke and Soffa Industries ( KLIC ) is a high-quality business demonstrating all the fundamentals I seek in companies: solid revenue growth, secular expansion of profitability metrics, and a strong balance sheet. But the company experiences severe headwinds due to the challenging macro environment, which adversely affects the end markets. Moreover, comps are difficult to beat after a massive revenue spike in 2021. According to my valuation analysis, the stock has minimal upside potential. All in all, I prefer to wait on the sidelines and assign the stock a "Hold" rating.

Company information

Kulicke and Soffa Industries designs, manufactures and sells capital equipment and tools for assembling semiconductor devices, including integrated circuits [ICs], high and low-powered discrete devices, light-emitting diodes [LEDs], and power modules.

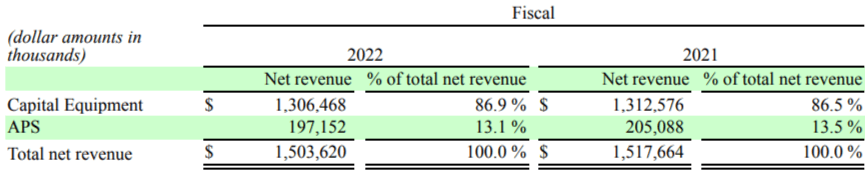

The company's fiscal year ends on September 30. KLIC operates in two segments: Capital Equipment and Aftermarket Products and Services [APS]. According to the latest 10-K report , the Capital Equipment segment's sales comprise about 87% of the total.

{kind=link}

Financials

Over the past decade, KLIC demonstrated a solid 12% revenue CAGR with a significant improvement in profitability metrics as the business scaled up. While the gross margin did not expand significantly, the operating margin more than doubled. That means the company has efficiently managed growth and benefited from the economies of scale effect. The free cash flow [FCF] margin ex-stock-based compensation [ex-SBC] has been quite volatile over the past decade, but generally also significantly improved.

{kind=link}

I like the company's high R&D-to-revenue ratio, which means the management is committed to innovation and building long-term shareholder value. Over the past decade, the company also significantly decreased its SG&A to revenue ratio, which is exactly the economies of scale effect.

KLIC's wide profitability margins enabled the company to build a fortress balance sheet with almost no debt. KLIC is in solid net cash of $687 million, and the covered ratio is well above a thousand. Liquidity ratios are also in excellent shape. A solid FCF enables the company to balance paying out dividends and reinvesting in growth. The company pays out about 18% of its net income, and the forward dividend yield is currently at 1.28%. The dividend yield looks low, especially in the current environment when the risk-free rate is above 4%. On the other hand, the past five year's dividend CAGR is at an impressive 44%, which looks very attractive. The company also conducts share buybacks.

Seeking Alpha

The latest quarterly earnings were released on May 3 , when KLIC topped consensus estimates on revenue and the bottom line. Revenue demonstrated a 55% YoY decline due to the difficult-to-beat comps after a spike in FY 2021. The Capital Equipment segment's revenue decreased 60% YoY due to a lower volume of customer purchases, primarily in the general semiconductor, LED, and memory markets. This was due to the overall uncertainty in the macro environment, which explains the weakness of end markets. The top-line weakness inevitably led to downward pressure on profitability metrics. While the gross margin was relatively resilient, with less than four percentage points decrease, the operating margin decreased multiple fold.

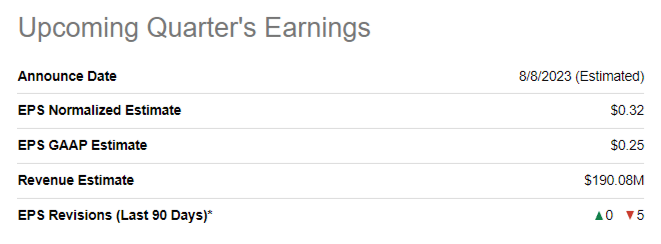

The upcoming quarter's earnings are scheduled on August 8. Headwinds are still in place, and the quarterly revenue is expected to decline 51% and the adjusted EPS to decline from over $2 to $0.32.

{kind=link}

It is apparent that headwinds are severe for the company, and I expect the rebound to be slow. The macro environment is still challenging, and global credit conditions are still tightening. On the other hand, the company's balance sheet looks strong enough to weather the storm even over multiple quarters. Secular trends are favorable for the company, but I expect it will take multiple quarters to recover stellar profitability metrics.

Valuation

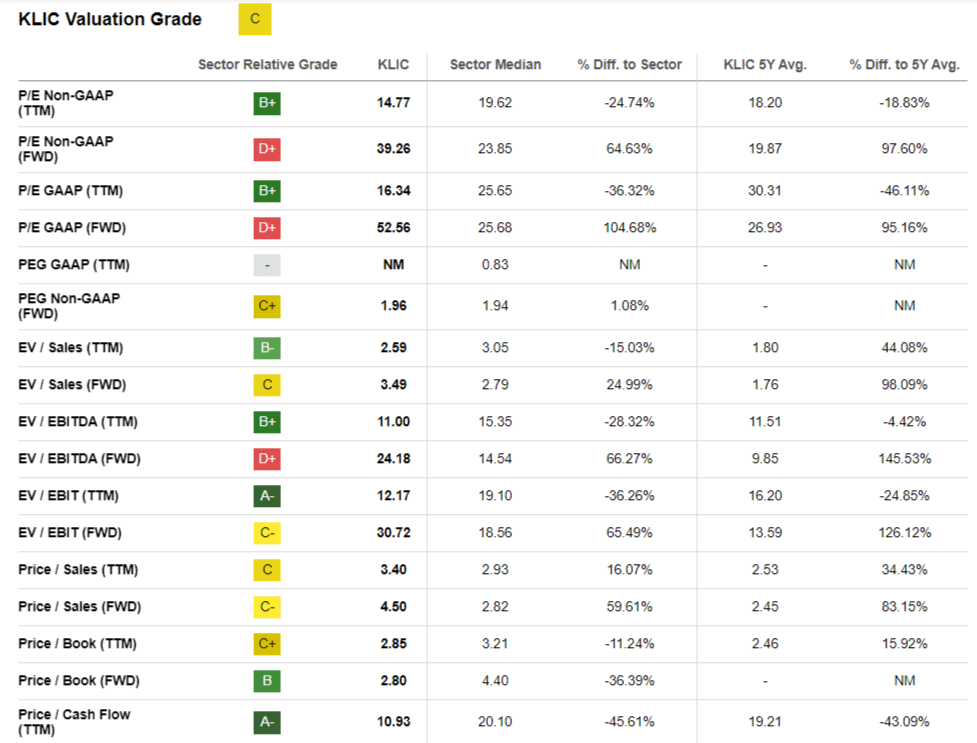

The stock rallied 38% year-to-date, significantly outperforming the broad U.S. market. Seeking Alpha Quant assigns the stock a "C" valuation grade, which is somewhat average. Indeed, the results of the comparisons with the sector median and five-year averages are mixed.

{kind=link}

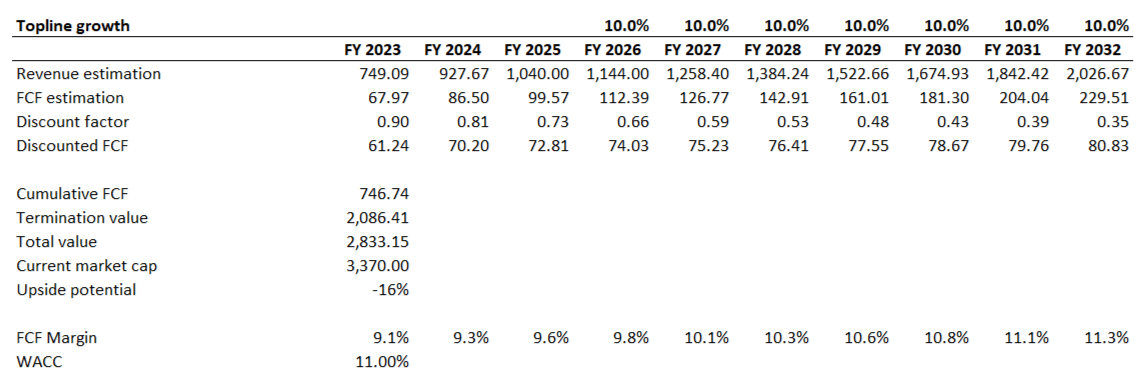

Valuation analysis based on multiples is apparently insufficient here. I want to proceed with a discounted cash flow [DCF] approach. Due to the volatility in the company's financial performance, I use an elevated 11% WACC as a discount rate. I have earnings consensus estimates available up to FY 2025, and for the years beyond, I project a 10% revenue CAGR. The FCF margin was quite volatile over the past decade, so I implement a ten-year average and expect it to expand by 25 basis points yearly.

{kind=link}

As you see, based on the discounted value of future cash flows, KLIC looks overvalued. But if we add up the substantial net cash position of about $687 mln, the current market cap looks fair. That said, I can conclude that the stock is reasonably priced with a limited upside potential based on the given underlying assumptions.

Risks to consider

As a growth company, KLIC's stock price significantly depends on the ability of the company to sustain aggressive revenue growth and expand profitability metrics as the business scales up. If the company fails to deliver the expected revenue growth or profitability ratios do not expand as projected, this might lead to investors' disappointment and stock sell-off. Quarterly earnings and near-term guidance revisions are usually the biggest catalysts for growth stock movements, whether positive or negative. That said, potential investors should be ready to face significant volatility.

As a technology company, KLIC faces significant risks of technology obsolescence and disruption. To build long-lasting competitive advantages, the management has to be committed to innovation and differentiating the company's offerings over the long term. KLIC's management mitigates this risk by heavily investing in R&D.

According to the latest 10-K report, the company generated about 95% of its sales outside the U.S. That said, KLIC faces substantial risks related to international trade. The foreign exchange risk is massive, making the company's earnings vulnerable to foreign exchange rate fluctuations. KLIC is also vulnerable to potential changes in international trade rules, policies, and tariffs.

Bottom line

To conclude, KLIC is indeed a high-quality business, and I like the management's commitment to innovation and its long-term mindset. But headwinds are very strong, and I expect it will take multiple quarters for the financial performance to rebound. Moreover, the valuation does not look attractive at the current stock price level. That said, I assign KLIC a "Hold" rating.

For further details see:

Kulicke And Soffa: High-Quality Business Experiencing Severe Headwinds