KLIC - Kulicke and Soffa Industries Q1 Earnings: Wait On Q2 For More Visibility

Summary

- The semiconductor industry saw a quick recovery in stock prices, as earnings were better than expected, yet a troublesome Q1 (Q2 for KLIC) is ahead.

- Kulicke and Soffa Industries' latest earnings report revealed a book-to-bill ratio above one, which was absent since June 2021.

- Demand in general semi and memory needs to become more visible for further upside.

- Kulicke and Soffa Industries stock remains the cheapest compared to peers, additionally, the fortress balance sheet opens up more opportunities.

Kulicke and Soffa Industries ( KLIC ) has experienced a major change in sentiment since my last article about the company. Patience has been rewarded to shareholders that saw value in the fundamentals of the company. The stock has outperformed the S&P 500 by 40% and we are now coming closer to a more fair value. The semiconductor industry is still having some struggles and profitability is poised to take another hit in the next quarter.

Seeking Alpha

Q1 Beats EPS, Misses Revenue

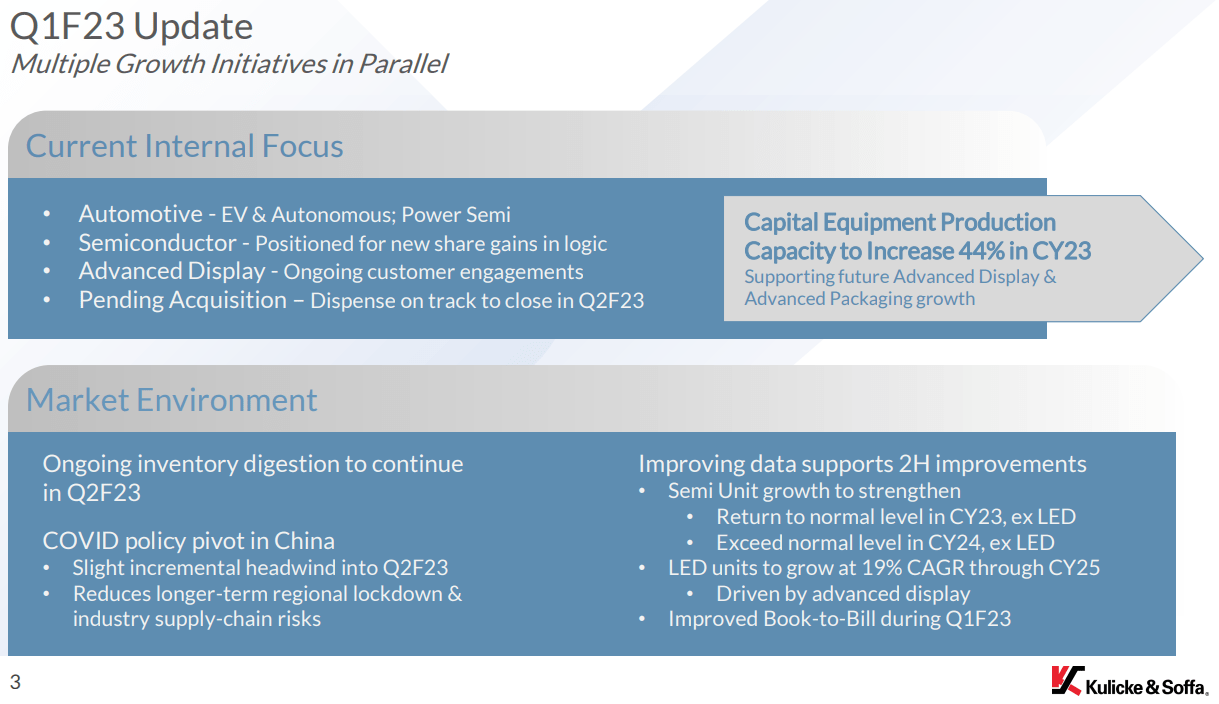

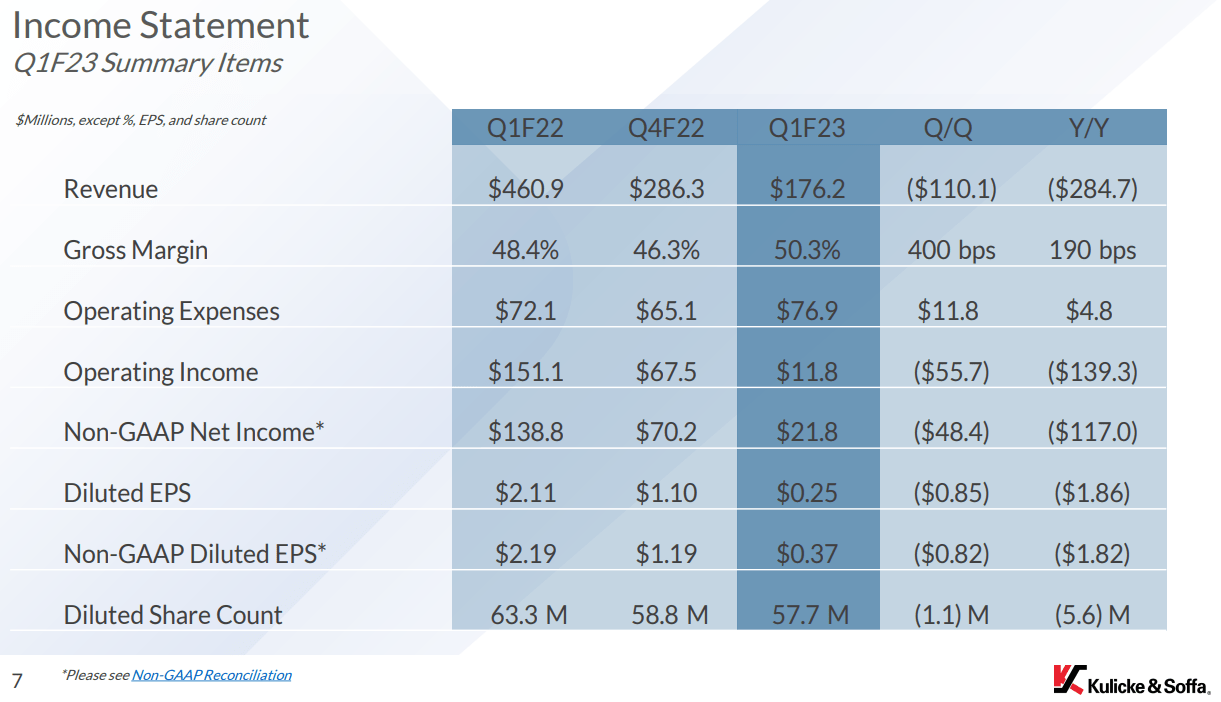

Kulicke And Soffa reported earnings on the 1st of February. Earnings per share came in better than expected at $0.37. Revenue of $176.23 million missed estimates. Investors took the news positively as the stock climbed 8% the day after. One of the main drivers was the announcement that the book-to-bill ratio exceeded one for the first time since June of 2021, which means demand is coming back on track and shows signs of normalization in inventory levels of customers. Book-to-bill ratio stands for the ratio of orders received to units shipped and billed.

Further, the increase in equipment production capacity is more good news. Instead of scaling down in bad times, it is important to expand capacity before the next semiconductor upward cycle, which will lead to long-term revenue growth. The recovery in China can definitely boost global demand and decrease the current inventory glut. Although KLIC's percentage of revenue out of China has decreased significantly from 61.8% to 32.8%, it is still a large chunk of revenue and it is possible there might be a rebalance with the reopening.

KLIC Investor Relations - 23Q1

{kind=link}

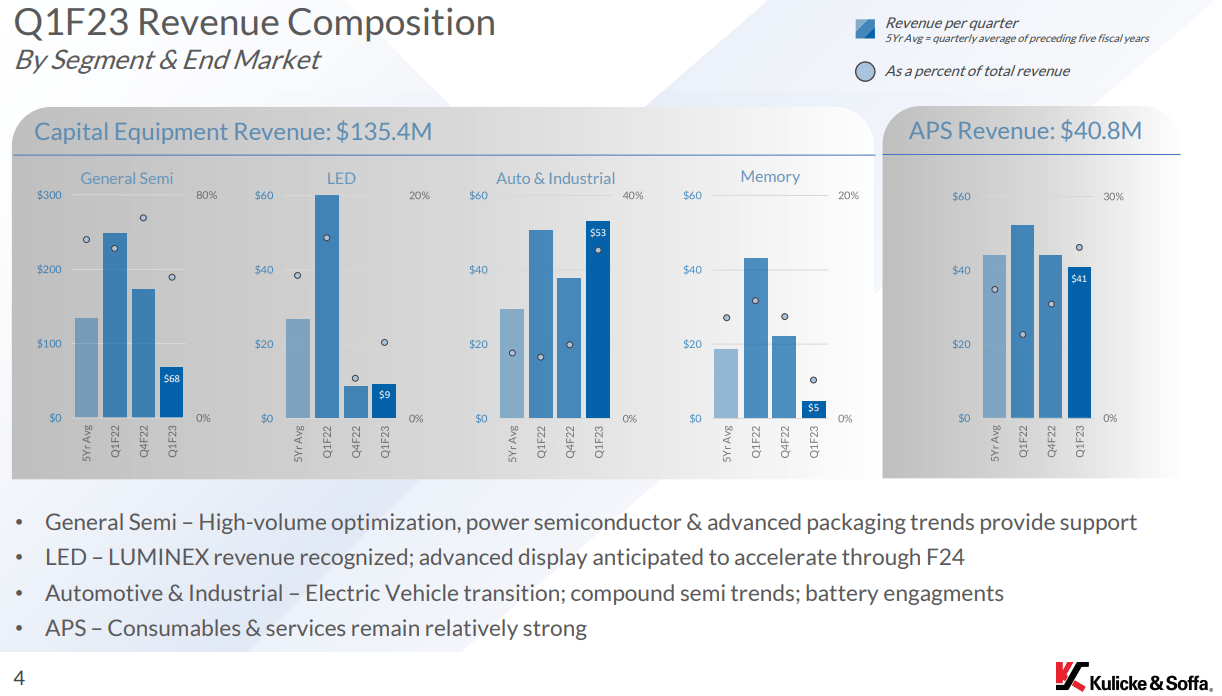

The new trend in the automotive and industrial sector stays resilient, while other segments are deteriorating. It was not unexpected, as we saw Micron's ( MU ) and Intel's ( INTC ) revenues decline at a fast rate, that the general semi and the memory business trend went downward. Yet, the LUMINEX systems, that support advanced LED assembly, are expected to see incremental demand in the following years. A normalization in the general semi and memory demand is still not clearly visible and next quarters should clarify what direction these segments will take.

KLIC Investor Relations - 23Q1

{kind=link}

Gross margins have increased in Q1, mainly due to a better product mix. The margins of the automotive products are better, additionally with a higher percentage of sales, it results in an overall gross margin increase. Therefore, prospects in profitability for 2024/2025 look promising and might beat the numbers in 2021/2022, at least if the demand in the automotive segment keeps strong.

KLIC Investor Relations - 23Q1

{kind=link}

Valuation

KLIC is not the only one that saw a change in momentum, the whole semiconductor industry moved upwards after better than expected earnings for the sector. KLIC's stock performance is low to average compared to peers.

Therefore, the company is still the most undervalued of the pack based on price-to-earnings and price-to-free cash flow. Though, it is clearly visible that profitability is getting weaker and weaker, as PE and PFCF are slowly increasing. Companies that can keep margins higher in the semiconductor downcycle will be rewarded the most and can possibly see more upside.

So far, KLIC has done a great job to keep margins higher, while the inventory glut in unraveling. Nonetheless, the outlook for Q2 is everything but good. Gross margin is expected to fall to 46% and non-GAAP EPS to $0.25. The hiring freeze has started and in the second half of the year demand should improve.

However, KLIC's liquidity is by far the strongest of all the semiconductor peers. The company has $550 million in cash and only $372 million in total liabilities. Hence, going forward M&A activity is valuable proposition to enhance synergies and growth. The acquisition of Advanced Jet Automation is on track to close in Q2 2023.

The CEO, Fusen Chen, mentioned in the earnings call :

In addition to parallel customer engagements and development programs, we remain on track to close the pending dispense acquisition as planned. As a reminder, this strategic acquisition provides additional access to adjacent-dispense opportunities in both semiconductor and electronics assembly. Collectively, these two areas represent a $2 billion addressable market and provide a new set of long-term opportunities.

In addition, KLIC can easily afford to buyback more shares and has room for future dividend increases. In the last trailing twelve months, 9% of the shares outstanding have been bought back.

Takeaway

At the moment, I rate Kulicke and Soffa Industries as a Hold. The semiconductor industry has risen fast, but not all troubles have disappeared. Q1 2023 (Q2 in case of KLIC) will be a very important quarter for most companies in the sector, so I would wait to buy more shares till we get more visibility on what the second half of the year will give. Demand has to normalize to see further upside.

While I give my Hold rating, I think the company is a good buy long-term. Compared to peers, KLIC still has one of the best value propositions in the market. But keep in mind there is some downside risk at current prices, be ready to average down.

In case we drop back to $40 levels, then I will be a buyer yet again.

For further details see:

Kulicke and Soffa Industries Q1 Earnings: Wait On Q2 For More Visibility