KLIC - Kulicke and Soffa Industries: Worsening Profit Margins And Declining Revenues

2024-01-02 03:35:14 ET

Summary

- Kulicke and Soffa Industries reported weak Q4 results, with declining revenue growth and worsening income margins.

- The company's memory market products failed to gain traction, and the management expects Q1 FY24 to remain challenging.

- KLIC is trading at a premium valuation, and the current price levels don't provide a favorable risk-reward profile.

Investment Thesis

Kulicke and Soffa Industries, Inc. ( KLIC ) is a global semiconductor and electronics assembly solutions provider headquartered in Singapore. In this thesis, I will analyze its fourth-quarter results along with its future growth prospects. I will also be analyzing its valuation at the current price level and the upside potential in its stock price. It has been experiencing stressed profit margins due to increased operating costs and declining revenues, and the recovery in the upcoming quarters doesn't seem evident; hence, I assign a hold rating for KLIC.

Company Overview

KLIC is recognized for providing advanced packaging solutions, including equipment and materials for the assembly and packaging of integrated circuits ((ICs)). It is known for its innovative semiconductor assembly equipment, which plays a crucial role in the production of high-performance electronic devices. It also offers a range of materials used in the semiconductor assembly process, contributing to the overall efficiency and reliability of electronic components, including bonding wires and advanced packaging materials to support the semiconductor packaging process. Its business can be segregated into four segments: ball-bonding equipment, wedge-bonding equipment, advanced solutions, and aftermarket products and services ((APS)).

Investor Relations KLIC

Q4 FY2023 Result

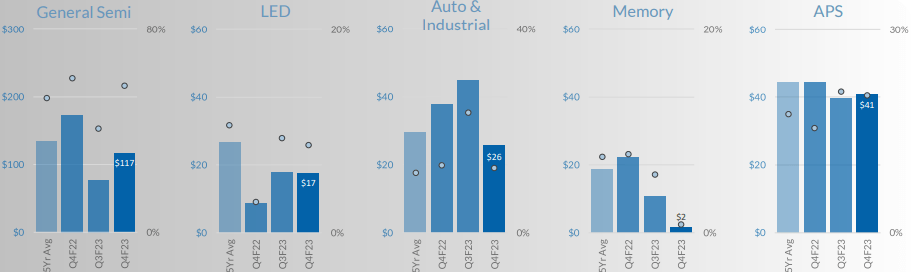

KLIC reported weak fourth-quarter results, with declining revenue growth and worsening income margins. As per my analysis, the ball bonder platform experienced a strong and sustained demand due to the company's consistent innovative product launches. However, its memory market products failed to gain traction among clients and primarily restricted revenue growth. The management expects the Q1 FY24 to remain challenging in the wake of a slowdown in the market.

{kind=link}

It reported total revenues of $202.3 million, a sharp decline of 29.3% compared to $286.3 million in the same quarter last year. As I mentioned earlier, the decline in memory products' sales and services primarily restricted revenue growth. I would like to highlight one point that the company is investing heavily in products catering to Artificial Intelligence ((AI)), which could open new markets for the company, but as of now, most of these products are at a development stage, and it would be too early to draw a conclusion, but it could be a revenue booster for the company in the coming years. The operating margins for the quarter stood at 9.6%, compared to 23.5% in the corresponding quarter last year. The deteriorating operational margin was a result of a significant decline in revenues and higher SG&A expenses. The increase in investment in AI research and development also contributed to the increase in operational expenses. The net income for the quarter was reported at $23.3 million, a massive decline of 64% compared to $64.9 million in the same quarter last year. This brings the diluted EPS for the quarter to $0.41, down from $1.10 in the same quarter last year. I think the company will continue to experience stressed profit margins given the higher inflationary environment and no material signs of significant revenue growth in the near future.

Now, let us have a look at its balance sheet. As of September 30, 2023, it reported cash and cash equivalents of $529.4 million . Along with this, it also has $230 million in liquid short-term investment. The company is a net cash company with no long-term debt. I think it has a robust balance sheet with significant room for fundraising in the future to boost growth without putting much stress on its balance sheet. The working capital days decreased from 465 to 448 days, representing an improved debtor cycle. The only worrying point was the increased inventory levels, which were a result of lower sales, but I think the increased levels are within safe levels and is not a major cause of concern.

Overall, the results failed to impress me on multiple parameters, including deteriorating profit margins and worsening sales growth. The Q1 FY24 guidance by the company doesn't instill much confidence either, with revenues estimated to be $170 million, representing a y-o-y decline of 3.5% compared to Q1 FY23 revenues of $176.2 million. The diluted EPS is estimated to be around $0.15, down from $0.25 in the same quarter last year. I think the guidance reflects that the upcoming quarters will remain challenging, and I think a recovery in the numbers can only be expected by the second half of FY24. The second half of FY24 is expected to witness interest rate cuts , as indicated by the FED in its last meeting. The rate cuts could positively impact the company's performance as they would result in increased spending by their clients on technological advancement due to lower interest expenses. This could pave the way for a revival in its revenue growth and put the company on the right track.

Valuation

KLIC is currently trading at a share price of $54.72, a YTD increase of 27.2%. It has a market cap of $3.14 billion. It is trading at a twelve-month trailing GAAP P/E multiple of $32.75x, compared to the sector median of 29.3x. This clearly reflects the fact that the company is trading at a premium valuation. The stock price has sharply increased after its fourth-quarter results, and current price levels don't provide a favorable risk-reward profile. I do not see a significant upside in the share price from current price levels, and I would not recommend initiating a fresh buying position.

Conclusion

The memory product segment has been the worst performing, but even the other segments didn't report strong revenue growth. The slowdown in the market and high inflation are expected to keep the revenues and profit margins stressed in the upcoming quarters. The company has the potential to capitalize on AI opportunities, but the majority of the AI products are in the development stage. The current valuation doesn't provide a favorable risk-reward scenario. Considering all these factors, I assign a Hold rating for KLIC.

For further details see:

Kulicke and Soffa Industries: Worsening Profit Margins And Declining Revenues