DTM - KYN: It May Be Beneficial To Add Shares Of This CEF To Your Portfolio Today

Summary

- Midstream partnerships and similar companies are great investments for retirees due to their stability and high yields.

- Kayne Anderson Energy Infrastructure Fund, Inc. invests in a portfolio of these companies in order to provide its investors with a high level of total return and income.

- The closed-end fund underperformed the broader index over the past six months, but it also includes renewable energy companies and others to take advantage of the energy transition.

- The Kayne Anderson Energy Infrastructure Fund's 8.92% yield appears quite sustainable going forward.

- The fund is currently trading at an attractive discount to the net asset value.

For many years now, one of the most popular investments for income-seeking investors has been midstream master limited partnerships and corporations. This makes a deal of sense as many of these companies boast considerably higher yields than just about anything else in the market bolstered by incredibly stable cash flows that are independent of conditions in the broader economy. These two characteristics work to make these some of the best vehicles for generating income in retirement.

Unfortunately, there are some problems with them. One of the biggest problems is that there are various tax problems that can arise with including a partnership in a tax-advantaged account, such as an individual retirement account. In addition to this, it can be difficult to put together a diversified portfolio of these assets without having access to a considerable amount of capital. Fortunately, there is a way to overcome these problems. That is to invest in a closed-end fund ("CEF") that specializes in investing in midstream companies. These funds are quite nice because they provide easy access to a professionally-managed portfolio of assets and can utilize a variety of strategies that allow them to pay out a higher yield than any of the underlying companies actually possess.

In this article, we will discuss the Kayne Anderson Energy Infrastructure Fund, Inc. ( KYN ), which is one fund that can be used to easily add this asset class to your portfolio. This fund yields 8.92% as of the time of writing, which is certainly high enough to turn most heads and is easily enough to provide a solid income to any investor. I have discussed this fund before, but a few months have passed since that time, so obviously, a few things have changed, including the release of the fund’s annual report. As such, this article will focus specifically on these changes as well as provide an updated analysis of the fund’s finances.

About The Fund

According to the fund’s webpage , the Kayne Anderson Energy Infrastructure Fund has the stated objective of providing its investors with a high level of after-tax total return. This is not particularly surprising, considering that this is an equity fund. In fact, the KYN fund is entirely invested in common equity:

CEF Connect

Undoubtedly, some readers may point out that the fund’s allocation to common stock exceeds 100%. This is because this fund is employing leverage as part of its investment strategy. We will discuss that in more detail later in this article. The important thing for our purposes right now is that the fund is entirely invested in common equity.

As Kayne Anderson Energy Infrastructure Fund, Inc. is an equity fund, it is logical that it would be focused on total return as opposed to other goals. This is because common equity is by its very nature a total return vehicle. After all, people that purchase common equity are typically interested in receiving both dividend income and capital gains. To that end, this fund does state that it aims to deliver most of its returns in the form of distributions to its investors. This implies that the fund’s shares will likely be fairly flat in the market as the fund will be paying out all of the returns that it generates via the distribution. This has certainly been the case over the past six months, as Kayne Anderson Energy Infrastructure Fund, Inc. has been almost completely flat:

{kind=link}

We can see that the fund is only down 1.10% over the trailing six months period. When we include its distribution in the return, investors would have made money overall in this period. That is certainly much better than many other things in the market.

The fact that the fund’s share price is not particularly volatile does not mean that investors cannot enjoy the benefits of compounding. In fact, if one were just to reinvest the distribution, the position will steadily grow over time even with a flat share price. An investor doing this would also see their income grow over time as more shares are accumulated even if the fund’s distribution remains flat. In fact, that is the recommended strategy for investing in a fund like this and it carries the added benefit that you can just turn off the reinvestment when you need the income to cover your bills or other reasons.

As the name of the fund implies, the Kayne Anderson Energy Infrastructure Fund aims to achieve its objective by investing in shares of energy infrastructure companies. The fund does not directly define these but in general, it considers an energy infrastructure company to be the same sort of company that most readers likely do. In short, the fund includes midstream pipeline operators, renewable energy companies that sell their power under long-term power purchase agreements, electric and natural gas utilities, and similar things. These companies play a very important role in getting energy resources and other things from the fields where they are extracted from the ground to the end-user or to local distribution companies.

As my long-time readers are no doubt well aware, I have devoted a great deal of time and effort to discussing these companies at Seeking Alpha over the past decade. As such, most readers are likely to be very familiar with the largest positions in the fund. Here they are:

Kayne Anderson

I have published numerous articles on all of these companies except for Western Midstream Partners ( WES ) over the years, so they should certainly be familiar to regular readers. For the most part, these are among the best midstream companies in the energy industry, with the notable exception of Cheniere Energy ( LNG ). While Cheniere Energy is certainly a company worthy of investment dollars, it is not a midstream company. It is one of the biggest producers of liquefied natural gas in the world, which positions it very well given the very strong fundamentals for liquefied natural gas.

One of the defining characteristics of midstream companies is that they enjoy remarkably stable cash flows regardless of the conditions in the broader economy. This is because of the business models that these firms utilize. In short, midstream companies enter into long-term (usually five to ten years in length) contracts with their customers. Under these agreements, the midstream company provides transportation and storage of the customer’s natural resources using its infrastructure network. The customer compensates the midstream company based on the volume of resources handled, not on their value. This provides an enormous amount of protection against the sometimes volatile nature of commodity prices. This is reinforced by the fact that these contracts specify a certain minimum number of resources that must be sent through the midstream infrastructure, which provides protection against the possibility of a volume decline and the resultant impact on cash flows.

Cheniere Energy has a similar business model, despite not being a midstream company. Cheniere Energy essentially sells a contractually specified quantity of liquefied natural gas to its customers at a contractually specified price. That provides it with very stable cash flows, as well.

The fact that these companies have very stable cash flows provides a number of advantages to income-focused investors. One of the most important of these is that it provides a great deal of support for the distribution that a given company pays out. After all, it is a lot easier for management to budget and pay out a fairly large proportion of the company’s cash flows if there is a great deal of confidence that the company will generate a similar amount of money next year. It is very similar to a salaried employee buying a house with a mortgage as their salary gives them a great deal of confidence that they can afford the mortgage for a number of years.

There have been minimal changes to the fund’s largest positions list since we last reviewed it. In fact, the only change is that TC Energy ( TRP ) was removed and replaced with ONEOK ( OKE ). This is not necessarily a bad change since ONEOK is one of the largest natural gas-focused midstream firms in the United States. That positions it well to take advantage of the strong forward demand growth for natural gas that we are likely to see all over the world over the next decade or two. The fact that so few positions have changed in the fund over the past few months may immediately lead one to assume that this fund has a fairly low turnover. This is certainly true as the Kayne Anderson Energy Infrastructure Fund has a 28.20% annual turnover, which is the lowest turnover that I have ever seen for an energy fund and it is fairly low for an equity fund in general. The reason that this is nice to see is that trading equities or other assets costs money that is billed to the fund’s shareholders. This creates a drag on the fund’s performance and makes things more difficult for its management as they need to generate a sufficient return to both cover these added expenses and still deliver a return that is acceptable to the fund’s shareholders. That is a difficult task that few actively-managed funds manage to achieve.

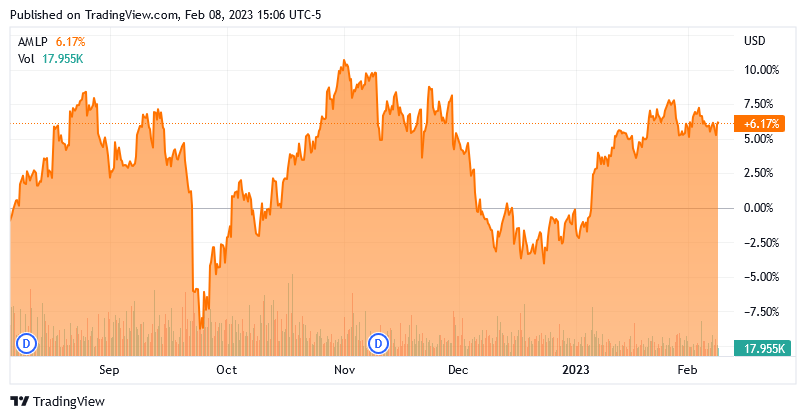

This one unfortunately did fail to beat its comparable index fund over the past six months. As we can see here, the Alerian MLP Index ( AMLP ) is up 6.17% over the period:

{kind=link}

That is a better performance than the Kayne Anderson Energy Infrastructure Fund managed to deliver over the same period, as we saw it deliver a slight loss. Although the Kayne Anderson closed-end fund does boast a higher distribution yield, that is not sufficient to make up the difference. With that said, the index only includes master limited partnerships but the closed-end fund includes corporations. If we refer back to the largest positions list that was presented earlier, Targa Resources ( TRGP ), The Williams Companies ( WMB ), Cheniere Energy, ONEOK, and DT Midstream ( DTM ) are all corporations and so will not be included in the index. That will create a performance difference in and of itself. In addition, the closed-end fund includes utilities and renewable companies that are not in the MLP index. In fact, only 83% of the Kayne Anderson Energy Infrastructure Fund is midstream companies and not all of them are master limited partnerships:

Kayne Anderson

Therefore, the two assets are not directly comparable, but admittedly the Alerian MLP Index is the one that most people would consider to be the best alternative to the closed-end fund. It is disappointing that it underperformed the index over the past six months, but it is important to note that both utilities and renewable companies performed far worse than midstream companies did over that period so that likely played a role here. The fact that these assets are included in the fund does set up the Kayne Anderson Energy Infrastructure Fund to be a better investment for the energy transition that is likely to play out over the coming decades than the index fund so potential investors may want to keep that in mind. I discussed this in more detail in my previous article on this fund, which is linked in the introduction.

Leverage

As stated earlier, the Kayne Anderson Energy Infrastructure Fund employs leverage. That is the reason that the fund’s common equity exposure exceeds 100% of its assets. This is one of the methods that a closed-end fund can use to deliver a higher yield than its assets possess, which we also see with this fund as it has a higher yield than the MLP index. Basically, the fund is borrowing money and using those borrowed funds to purchase shares and partnerships of midstream corporations, partnerships, and other assets. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the overall yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are significantly lower than retail rates, this will usually be the case.

Unfortunately, the use of debt is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much debt since that would expose us to too much risk. I do not generally like to see a fund’s leverage exceed a third as a percentage of its assets for this reason. As is the case with most midstream funds right now, the Kayne Anderson Energy Infrastructure Fund fulfills this requirement. As of the time of writing, the fund’s levered assets comprise 27.13% of the portfolio. This is a reasonable ratio that represents a fairly attractive balance between risk and reward. As such, it does not appear that we have too much to worry about with respect to the fund’s leverage at present.

Distribution Analysis

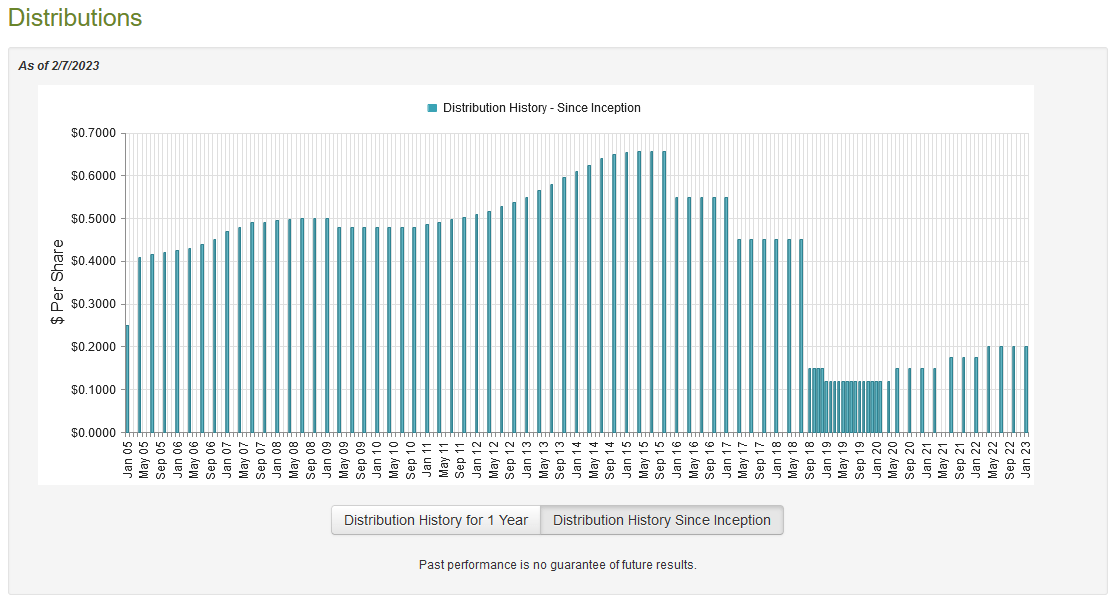

As stated earlier in this article, the Kayne Anderson Energy Infrastructure Fund has the stated objective of delivering its investors a high level of after-tax total return. In order to achieve this, it invests in a portfolio of master limited partnerships and other energy infrastructure companies that frequently boast fairly high yields. The fund then applies leverage to boost its portfolio yield and pays out its returns and gains to its investors. As such, we can probably safely assume that this fund will have a fairly high distribution yield. This is certainly the case as it currently pays out a quarterly distribution of $0.20 per share ($0.80 per share annually), which gives the fund an 8.92% yield at the current price. Unfortunately, Kayne Anderson Energy Infrastructure Fund, Inc. has not been particularly consistent about this payout over its history. In fact, the distribution has varied a lot over the years:

{kind=link}

The fact that Kayne Anderson Energy Infrastructure Fund’s distribution has varied so considerably over the years could prove to be a turn-off for those investors that are looking for a safe and secure source of income that they can use to pay their bills and finance their lifestyles. This is certainly not unusual for a closed-end fund that focuses on the energy infrastructure sector, however. After all, we have seen a number of these companies cut their payouts during the energy bear markets of 2015 and 2020. The fund would naturally have to reduce its own distributions since these events resulted in less money coming into the fund. Fortunately, we have seen it begin to hike its distributions over the past two years as the industry has recovered and some midstream companies have benefited from strong equity appreciation and raised their distributions. However, the fund’s past is not necessarily very important to an investor that is purchasing shares today. This is because anyone buying today will receive the current distribution at the current yield. Thus, the most important thing is the fund’s ability to maintain its current distribution.

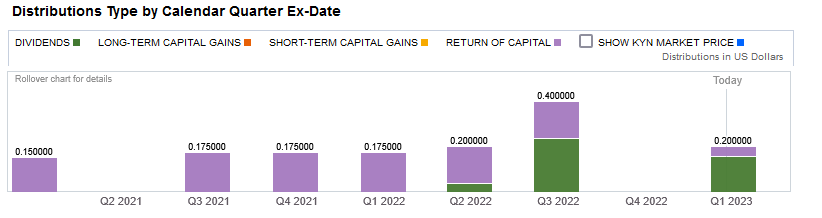

Unfortunately, a look at the distribution classification does not invoke a great deal of confidence. Here it is:

{kind=link}

As we can see, the fund has made a considerable amount of return of capital distributions over the past two years. This is concerning because a return of capital distribution can be a sign that the fund is returning the investors’ own money back to them. This is obviously not sustainable over any sort of extended period. However, there are other things that can cause a distribution to be classified as a return of capital. For example, the distribution of money received from a master limited partnership would be classified in this way as would the distribution of unrealized capital gains. These are both things that this fund may be doing, especially considering the strong appreciation that midstream companies have delivered over the past two years. As such, it is important that we investigate exactly how the fund is financing its distributions in order to determine how sustainable they are likely to be.

Fortunately, we have an incredibly recent document that we can consult for that purpose. The fund’s most recent financial report corresponds to the full-year period that ended on November 30, 2022. This is a more recent document than we had the last time that we looked at the fund and it should provide us with a great deal of insight into how the fund handled the somewhat challenging market that dominated 2022. During the full-year period, the fund received a total of $109.858 million in dividends and distributions along with $366,000 in interest from the investments in its portfolio. However, $48.711 million of this was considered to be a return of capital, and another $4.514 million was considered to be a capital gain. These distinctions come from the fact that the fund invests in master limited partnerships, which are taxed differently than corporations.

Overall, the fund had a total reported investment income of $56.999 million during the full-year period. It paid its expenses out of this amount, leaving it with $9.700 million available for investors. Obviously, this was nowhere near enough to cover the $103.807 million that the fund paid out in distributions. At first glance, this is likely to be concerning but we need to investigate further.

After all, there are other methods that the fund can use to obtain the money that it needs to pay its distributions. As we have already seen, the fund received $53.225 million from the master limited partnerships in its portfolio which was not considered to be reportable income. In addition to this, the fund had capital gains during the period. It reported net realized gains of $83.081 million and had another $230.562 million net unrealized gains.

Altogether, the fund’s assets increased by $321.543 million over the year after accounting for all inflows and outflows. Thus, Kayne Anderson Energy Infrastructure Fund, Inc. obviously earned far more than it needs to cover the distribution. Overall, there does not appear to be anything to worry about here. The distribution is reasonably safe.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of a closed-end fund like the Kayne Anderson Energy Infrastructure Fund, the usual way to value it is by looking at the fund’s net asset value. The net asset value of a fund is the total current market value of all of the fund’s assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can acquire them at a price that is less than the net asset value. This is because such a scenario implies that we are buying the fund’s assets for less than they are actually worth. That is certainly the case with this fund today. As of February 7, 2023 (the most recent date for which data is available as of the time of writing), the Kayne Anderson Energy Infrastructure Fund had a net asset value of $10.27 per share but the shares actually trade for $8.97 per share. This gives the fund’s shares a 12.66% discount at the current price. This is better than the 11.93% discount that the shares have traded at on average over the past month and, frankly, anytime a fund is trading at a double-digit discount, the price is quite acceptable. Thus, the price is right here.

Conclusion

In conclusion, energy infrastructure companies such as midstream partnerships, corporations, and other energy companies that use a similar business model are among the most attractive investments for those individuals that are seeking income. These companies enjoy remarkably stable cash flows through any business environment, which can be important considering the uncertainty that we are facing in today’s economy.

Kayne Anderson Energy Infrastructure Fund, Inc. invests in a portfolio of these companies and pays out its gains and income to the investors, which allows it to boast an impressive 8.92% yield at the current price. Kayne Anderson Energy Infrastructure Fund, Inc. appears to be easily able to maintain this distribution and is trading at an attractive discount right now, so it could be worth adding some shares to your portfolio.

For further details see:

KYN: It May Be Beneficial To Add Shares Of This CEF To Your Portfolio Today