STOHF - KYN: This Midstream CEF Can Add Income To Your Portfolio At A Discount

2023-04-17 08:38:51 ET

Summary

- Midstream partnerships and corporations are one of the best vehicles available for income-seeking investors and have long been popular among this cohort.

- KYN invests in a portfolio of these companies in order to provide a very high yield to its shareholders.

- The sector has lost a bit of its shine due to energy prices weakening, but the companies in the fund are quite stable.

- The fund pays an incredible 9.85% yield that it should be able to sustain going forward.

- The fund is currently trading at a very attractive discount to net asset value.

For many years now, one of the most popular investments among income-seeking investors has been midstream master limited partnerships. This is hardly surprising considering that these companies tend to enjoy remarkably stable cash flows that support their distributions, which tend to be among the largest of any sector. This is evident in the fact that the Alerian MLP Index ( AMLP ) currently yields 7.80%, which is substantially higher than the 1.57% yield of the S&P 500 Index ( SPY ). The distributions paid out by these companies also enjoy significant tax advantages, which can be quite appealing to investors in high tax brackets.

Unfortunately, there are a few problems with these companies. One of the most significant of these is that their unique tax advantages make it very difficult to include them in a retirement account. That is quite irritating because otherwise, they are among the best vehicles in the market for retirement income. The other problem with them is that it can be difficult to put together a diversified portfolio of these assets without having access to a considerable amount of capital, although the same can be said for pretty much any sector, or even the market as a whole.

Fortunately, there are some ways around these problems. One of the best of these is to purchase shares of a closed-end fund that invests in midstream partnerships. These funds are typically organized as corporations, so they avoid all of the tax problems and can easily be put into a retirement or other tax-advantaged account. These funds also avoid the problem that some Americans have with K-1 tax forms and midstream partnerships. Since these funds also pay out most of the distributions that they receive, investors still get the benefit of the exceptionally high yields paid by the sector. In fact, in some cases, a midstream closed-end fund can pay out a higher yield than any of the underlying assets, which only increases its appeal to income-seeking investors. Finally, as these holds will hold a variety of different midstream companies, an investor will obtain a diversified portfolio with one easy trade.

In this article, we will discuss the Kayne Anderson Energy Infrastructure Fund ( KYN ), which is a fund that specializes in the midstream sector. As might be expected, this fund boasts a very impressive 9.85% yield as of the time of writing so it both beats the broader index and gives us a very attractive source of income. I have discussed this fund before, but a few months have passed since that time so naturally a few things have changed. This article will therefore focus specifically on these changes as well as provide an updated analysis of the fund’s finances.

About The Fund

According to the fund’s webpage , the Kayne Anderson Energy Infrastructure Fund has the stated objective of providing its investors with a high level of after-tax total return. This is not particularly surprising for a midstream fund. One reason for this is that most of these funds invest either primarily or exclusively in common equity. This one is not an exception to this as the portfolio consists entirely of common equity, with a small allocation to cash:

CEF Connect

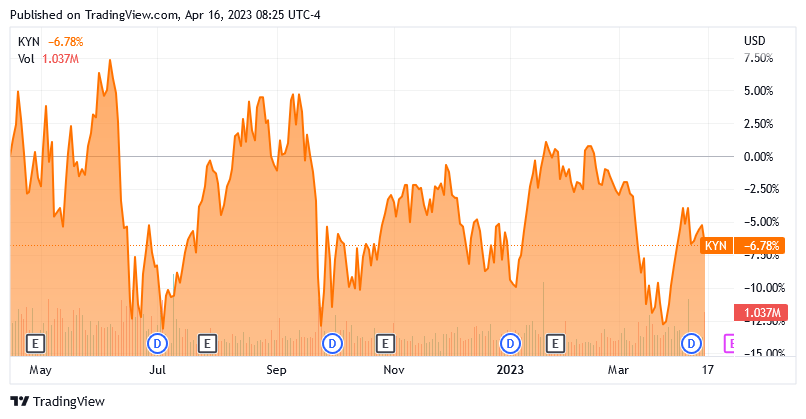

There may be a few readers that immediately point out that the fund has more than 100% allocated to common equity. This is because this fund employs leverage as a way to boost its returns, which we will discuss later in this article. The important thing here is that the fund invests only in common equity and does not include things like midstream preferred equity or debt. This is a total return vehicle as we typically invest in a company’s common equity both to receive the distribution that it pays out as well as the potential for capital gains as the issuing company grows and prospers. However, in the case of midstream companies, the majority of the return will come in the form of direct payments to investors as these companies generally have fairly slow growth rates and limited potential for capital gains. The fund will collect these distributions on behalf of its own investors and then pay them out, along with any capital gains that it manages to generate from its trading activities. The goal is for the fund’s own share price to remain relatively stable over time and all the profits from its investment activities get paid to the investors. It was unfortunately not that successful at this over the last year, as the fund is down 6.78% over the period:

{kind=link}

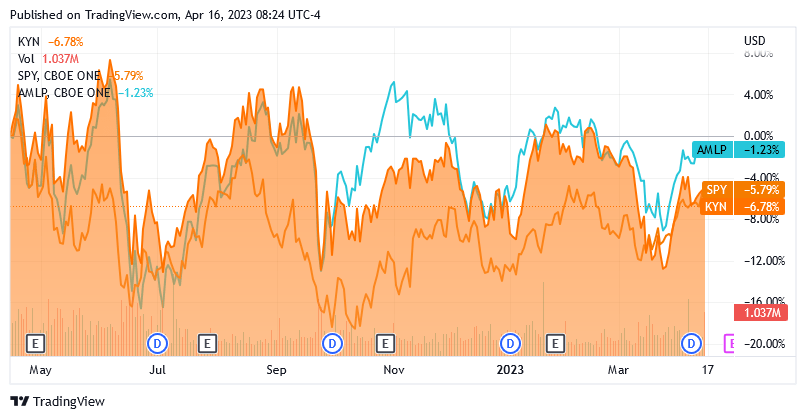

This is, unfortunately, a bit worse than both the S&P 500 Index and the Alerian MLP Index over the same period:

{kind=link}

However, the fund’s yield is substantially higher than that of the S&P 500 Index, so it did manage to beat that index in terms of total return. It did not manage to beat the Alerian MLP Index over the period, however. Both the closed-end fund and the Alerian MLP Index delivered positive total returns for an investor that reinvested all distributions over the twelve-month period, which is much better than the market as a whole. That is certainly something to be pleased about.

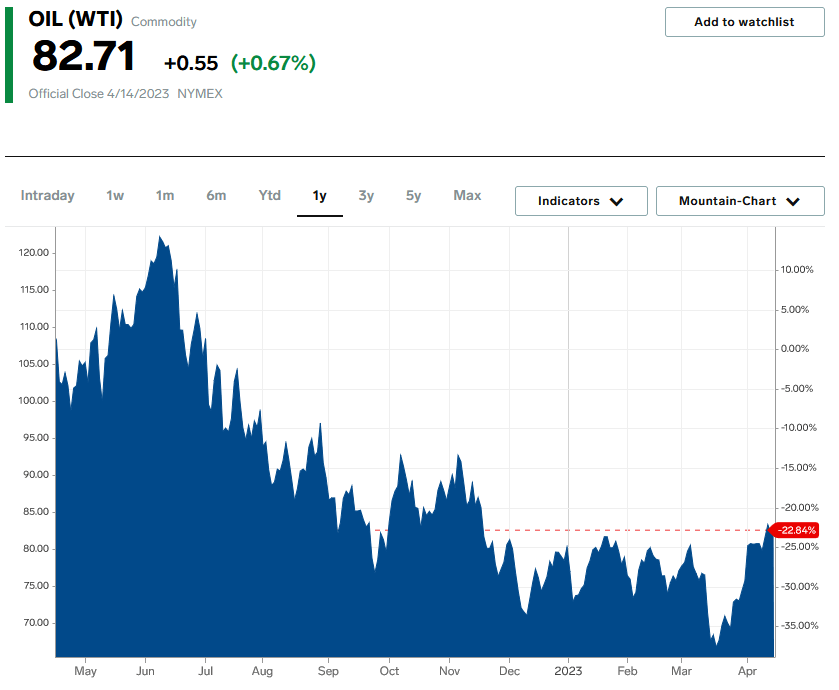

Of course, the entire energy sector generally beat the market over the past eighteen months. One of the biggest reasons for this is that the market had been in a massive bubble that caused everything except for the energy sector to be overvalued. As high oil prices started pushing up the profits of energy companies, the Federal Reserve raised rates and pricked the bubble, but energy companies were not affected because they are substantially undervalued , even today. Unfortunately, the shine has started to wear off a bit. Over the past few months, there have been growing fears of a near-term recession that has been pressuring energy prices. West Texas Intermediate crude oil is down over the past year, although it is actually up year-to-date:

{kind=link}

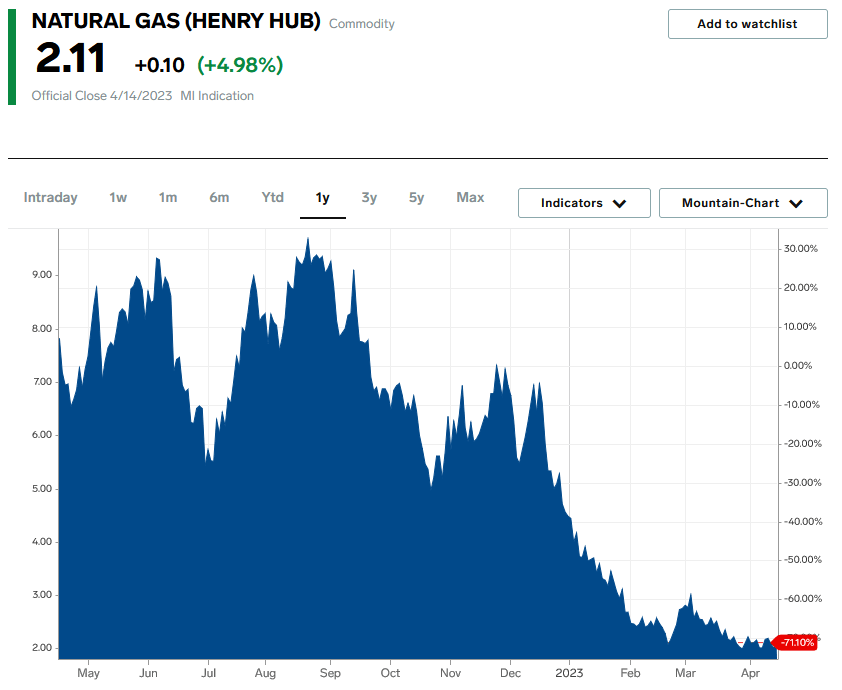

The situation is a bit worse for natural gas, as it is down a whopping 71.10% over the past twelve months, with a significant portion of that decline occurring since January:

{kind=link}

However, this has not really had an impact on the midstream companies that are held by the Kayne Anderson Energy Infrastructure Fund. As we can see here, 84% of the companies in the fund are midstream energy companies, with the rest being various types of electric utilities:

Kayne Anderson

This is a slight increase from the 83% that was invested in midstream the last time that we looked at this fund, but the difference is mostly academic. The fact that so much of the portfolio is invested in these companies is the reason why it should not be particularly affected by the decline in energy prices. This is because the cash flows of midstream companies are generally not affected by changes in energy prices due to the business model that these companies utilize. In short, a midstream company will enter into a long-term (usually five to fifteen years in length) contract with its customers. Under the terms of these contracts, the midstream company will provide transportation for the customer’s hydrocarbon resources using its infrastructure network of pipelines and other infrastructure. In exchange, the customer will compensate the midstream company based on the volume of resources that are transported, not their value. This business model thus provides a great deal of insulation against changes in energy prices. In addition, the contracts that a midstream company has with its customers typically include minimum volume commitments that ensure that the midstream company’s cash flow will not decline below a certain level if resource production or consumption declines, which may happen during a recession or during a period of low energy prices. This is why these companies are able to generate remarkably stable cash flows regardless of broader economic conditions. The stable cash flows are nice because they provide a great deal of support for the distribution. After all, it is easier for a company to budget a large regular expense (like its distribution) if it can be certain that it will generate a similar amount of cash flow next month. However, this does not prevent the market prices of many of these companies from declining in response to a decline in energy prices. As we have just seen though, they have generally held up pretty well despite the weakness in crude oil and natural gas prices.

As my long-time readers are no doubt well aware, I have devoted a considerable amount of time and effort over the years to discussing midstream companies here at Energy Profits in Dividends as well as the main Seeking Alpha site. As such, most readers should be familiar with the largest positions in the fund. Here they are:

Kayne Anderson

I have published multiple articles on all of these companies except for Western Midstream Partners ( WES ) and Sempra Energy ( SRE ) over the past decade. Thus, all of them should be relatively familiar to most of the people that are reading this. All of these companies except for Cheniere Energy ( LNG ) and Sempra Energy are midstream firms so they all use the volume-based contractual business model that was just discussed. Cheniere Energy largely does as well, since it sells the liquefied natural gas that it produces under long-term contracts with major energy companies like Equinor ( EQNR ). As such, it also has very stable cash flows, which is nice because the company has a lot of debt that it needs to get under control. As such, it does not have an especially high yield so it will not be providing as much income to the fund as the other companies listed here. Cheniere Energy does have tremendously strong growth prospects though due to the rising demand for liquefied natural gas, so it makes a lot of sense for the fund to be holding this company in the portfolio.

The fund has made very few changes since we last looked at it, although the weightings of the individual companies in the portfolio have changed dramatically. This could easily be explained by one asset outperforming another in the market though, so it is not necessarily indicative of the fund actively changing its positions. We do see that DT Midstream ( DTM ) was removed from the fund’s largest positions list and replaced with Sempra Energy. That is the only real change here of note. The fact that so few positions have changed in the past few months could lead one to believe that this fund has a fairly low turnover. This is certainly true as it reported a 28.20% annual turnover in the most recent fiscal year, which is incredibly low for a midstream equity fund. It is far below most of its peers in this category. This is important because it costs money to trade stocks, partnership units, and other assets. These costs are billed directly to the fund’s shareholders and as such create a drag on the portfolio’s performance. It also makes the management’s job more difficult because the fund needs to generate sufficient returns to overcome these added expenses and still have enough left over to satisfy the shareholders. As we saw earlier, this fund failed to accomplish this over the past twelve months as it underperformed the Alerian MLP Index, which is probably the best benchmark to use for this fund.

Leverage

As stated earlier in this article, the Kayne Anderson Energy Infrastructure Fund employs leverage, which is one of the methods that it employs to deliver a yield that is higher than that of any of the underlying assets. Basically, the fund borrows money and then uses that borrowed money to purchase partnership units of midstream companies. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed funds, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing at institutional rates, which are considerably lower than retail rates, this will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. This will generally result in the fund underperforming the index during bear markets, which is exactly what we saw earlier in this article. As a result of this, we want to ensure that the fund is not employing too much leverage since that would expose us to too much risk. I generally do not like to see a fund’s leverage exceed a third as a percentage of its assets for that reason. Fortunately, the Kayne Anderson Energy Infrastructure Fund meets that requirement as its levered assets only comprise 27.56% of the portfolio as of the time of writing. This is relatively in line with what many of its peers are running in terms of leverage, so overall the fund appears to be striking a fairly reasonable balance between risk and reward.

Distribution Analysis

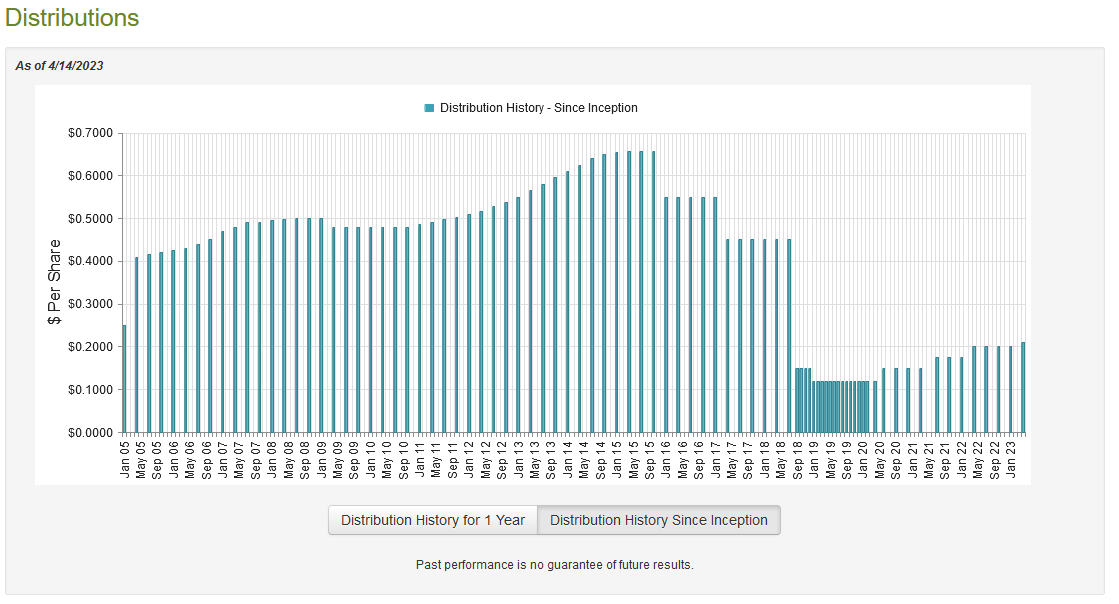

As mentioned earlier in this article, one of the biggest reasons why investors purchase midstream companies in the market is that they tend to have much higher yields than just about anything else. When we combine this with their overall stability, we can see how these firms can be a core holding in anyone’s income portfolio. The Kayne Anderson Energy Infrastructure Fund purchases these companies and then applies a layer of leverage to boost the effective return of the portfolio. As such, we can assume that this fund will likely have a very high yield itself. This is certainly true as the fund pays a quarterly distribution of $0.21 per share ($0.84 per share annually), which gives it a 9.85% yield at the current price. The fund has unfortunately not been very consistent about its payout over the years, although it has been increasing it since 2020:

{kind=link}

We see that the fund increased the distribution since the last time that we discussed it, which is certainly nice to see. Unfortunately, it still remains less than it had been prior to the pandemic. This is something that will likely concern investors that are seeking a stable and secure source of income to use to pay their bills or finance their lifestyles, but it is hardly unusual for a fund such as this. After all, back in 2020 the pandemic and resultant lockdowns caused the price of West Texas Intermediate crude oil to briefly hit its lowest price of all time and prompted many energy producers to drastically cut their production. Although the cash flows of most midstream companies were not really affected, they still canceled many of their growth projects and some even cut their distributions to focus on reducing debt and strengthening their balance sheet. This, unfortunately, is still necessary today due to environmental, social, and governance principles at some of the major asset management firms reducing the industry’s ability to raise capital as these companies are limiting their investment in traditional fossil fuel companies. Unfortunately, this probably means that we will never see this fund’s distribution reach the levels that it had prior to the pandemic. However, this is somewhat immaterial to anyone buying today. This is because new money will receive the current distribution at the current yield and is unaffected by any distribution cuts that the fund made in the past. The most important thing for someone today is ensuring that the fund can afford to sustain the current distribution.

Fortunately, we do have a fairly recent document that we can consult for our analysis. The fund’s most recent financial report corresponds to the full-year period that ended on November 30, 2022. This is curious because this is one of the few closed-end funds that publishes quarterly financial reports, but it has not yet published one for the three-month period that ended on February 28, 2023. I checked both the SEC database as well as the fund’s own webpage and neither has a publication on file that is newer than the annual report. This is unfortunate because it means that we will not have any information regarding the fund’s performance over the past five months or so. During the full-year period, the Kayne Anderson Energy Infrastructure Fund received a total of $109.858 million in dividends along with $366,000 in interest from the investments in its portfolio. However, $48.711 million of this money came from master limited partnerships and so is considered to be a return of capital and not investment income. Thus, the fund only reported $56.999 million in income. It paid its expenses out of this amount, which left it with $9.700 million available for shareholders. That is, admittedly, disappointing since we would have expected much more of the fund’s earnings to make it through to investors. The majority of these expenses were investment management fees, which was a major drag on earnings. As might be expected, the $9.700 million was not nearly enough to cover the $103.807 million that the fund actually paid out during the period. At first glance, this is likely to be concerning since the fund clearly failed to cover its distribution using net investment income.

However, the fund does have other ways through which it can obtain the money that it needs to cover the distribution. As already mentioned, the fund received $48.711 million in distributions from master limited partnerships that were not considered net investment income. That alone was not enough to cover the difference between its net investment income and the distribution, though. Fortunately, the fund had substantial capital gains during the period. It reported net realized gains of $83.081 million and had another $230.562 million net unrealized capital gains. Altogether, the fund’s assets increased by $327.543 million after accounting for all inflows and outflows. Thus, the fund actually managed to cover the distribution four times over. Overall, it does not really appear that we need to worry too much here as the fund’s distribution is quite secure. This explains the recent distribution increase as it is trying to get all of this money out to the shareholders as quickly as possible.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of a closed-end fund like the Kayne Anderson Energy Infrastructure Fund, the usual way to value it is by looking at the fund’s net asset value. The net asset value of a fund is the total current market value of all the fund’s assets minus any outstanding debt. This is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can acquire them at a price that is less than the net asset value. This is because such a scenario implies that we are buying the fund’s assets for less than they are actually worth. This is generally the case with midstream funds, and it is, fortunately, true with this one. As of April 13, 2023 (the most recent date for which data is currently available), the Kayne Anderson Energy Infrastructure Fund had a net asset value of $10.03 per share but the shares currently trade for $8.53 each. This gives the fund’s shares a 14.96% discount to the net asset value at the current price. This is a very nice discount that is quite a bit better than the 13.69% that the shares have had on average over the past month. Overall, this is a reasonable price to pay for this fund.

Conclusion

In conclusion, midstream master limited partnerships are an excellent way to get income due to their stable cash flows and high yields. The Kayne Anderson Energy Infrastructure Fund offers an appealing way to add this asset class to a retirement or other tax-advantaged account. The fund offers a reasonable portfolio consisting of most of the largest companies in the sector and boasts a fairly high yield that appears to be quite sustainable. The fund currently trades at a very nice valuation, so it could be worth purchasing today.

For further details see:

KYN: This Midstream CEF Can Add Income To Your Portfolio At A Discount