AIQUF - L'Air Liquide: Fully Valued Quality Compounder

2023-11-28 06:45:32 ET

Summary

- Air Liquide is a leading multinational industrial gases company with a high-quality business model and strong track record of value creation.

- The industrial gases industry has attractive fundamentals, with high barriers to entry, pricing power, and resilience during downturns.

- The green transition presents new opportunities for Air Liquide, particularly in renewable hydrogen and carbon capture and storage.

- We believe the stock is fully valued at 25x forward EPS, and we issue a hold rating.

We present our note on Air Liquide, a leading multinational industrial gases company, with a hold rating. We appreciate Air Liquide's high quality business model, resiliency, and defensiveness, but we find the company fully valued at this share price. We will provide a brief overview of the company, analyze the firm's business model and key value drivers, discuss recent results, value the equity, and lay out the investment case and risks.

Introduction to the company

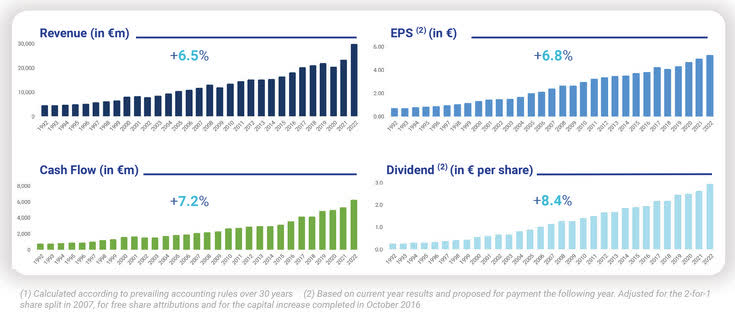

Air Liquide is a world leader in gases, technology, and services for health and industry. Oxygen, nitrogen, and hydrogen have been at the core of the firm's activities since its founding in 1902. The company has more than 2 million industrial customers all over the world including craftsmen, small and medium enterprises, and corporates across various sectors such as chemicals, energy, steel, automotive, aerospace, food, pharmaceuticals, etc. In addition, Air Liquide supports more than 1.9 million patients in hospitals and at home. The company is listed on Euronext Paris and is a CAC40 constituent. It has a current market capitalization of ca. €91 billion. Air Liquide has an excellent track record of value creation for shareholders.

High quality business model - Unregulated utilities

We find the industrial gases industry fundamentals highly attractive. The market is global and highly concentrated/oligopolistic, having experienced a wave of consolidation in the mid-late 2010s. The largest players: Linde , Air Liquide (ca. 30%), and Air Products have a combined market share of nearly 70%, followed by a tail of smaller players. The market has high barriers to entry given the high capital intensity, the required technical expertise needed in handling gases (more complex than other chemical processes), and significant network effects related to pipeline infrastructure. Outsourcing to industrial gas companies vs. internal production has clear benefits including the lack of capex, little operating risk, and better efficiency. In addition, the products are mission-critical to a wide variety of industries, particularly in manufacturing processes. The favorable market structure and unique value proposition allow for pricing power, consistent high margins, high cash generation, and good returns on capital. The sector is highly resilient even during downturns, thanks to guaranteed payment long-term (as long as 15+ years) contracts. strong pricing, and cost optimization. The industry has been growing well above GDP and industrial production at mid-single digits compound annual growth rates, driven by base volume growth, new projects, pricing, and M&A. As a result, industrial gas companies have vastly outperformed the chemicals sector and broader indices.

{kind=link}

Navigating the green transition

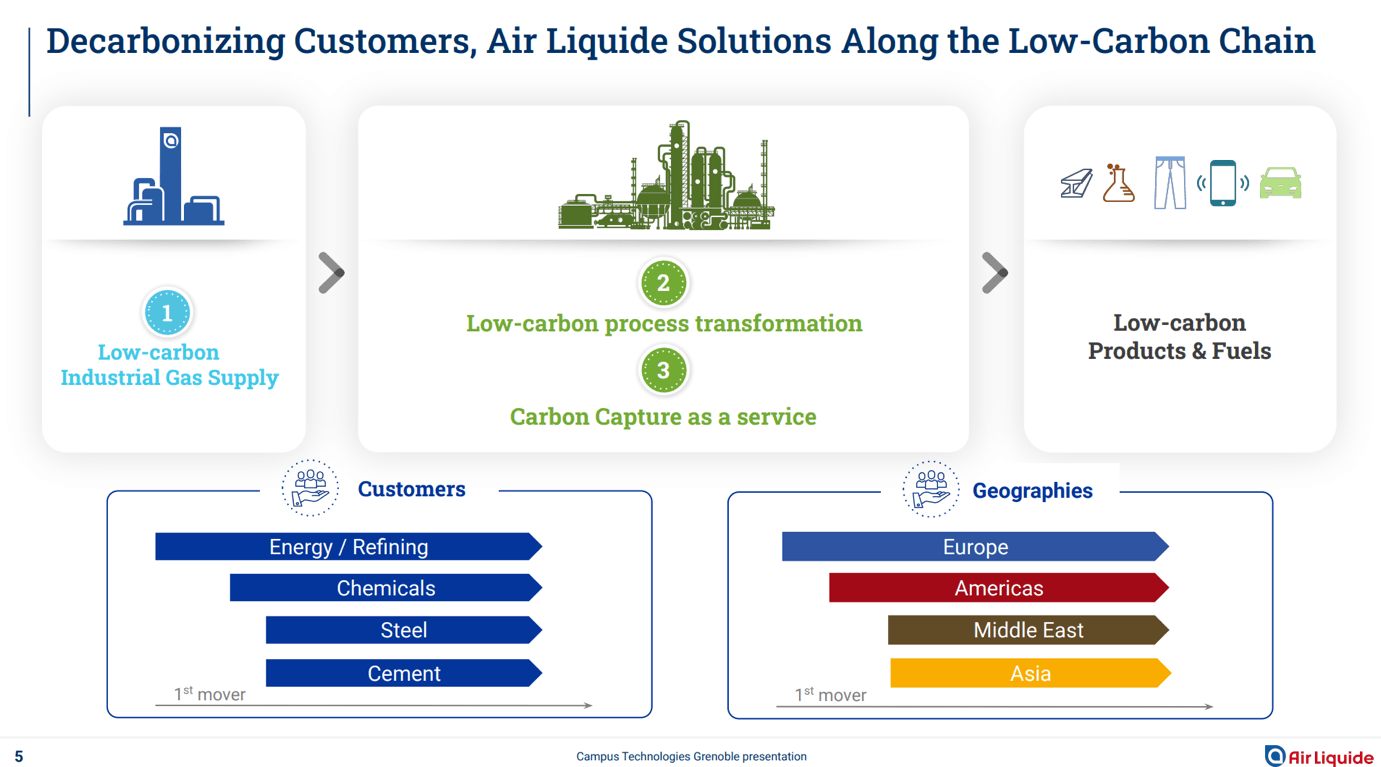

The green transition presents new opportunities for the industrial gases sector. Major players have invested in developing renewable hydrogen capabilities, building on their long experience and deep know-how. They are likely to play a role in the merchant market and capture a share of the more than a hundred billion dollars hydrogen market. Air Liquide is particularly well positioned in hydrogen thanks to its massive hydrogen pipeline network and plans a three-fold increase in hydrogen revenue. Moreover, carbon capture and storage gasification will significantly increase the demand for oxygen (likely a $20 billion+ opportunity as per analysts), creating another major opportunity. In addition, biomethane i.e., renewable natural gas represents an attractive opportunity, especially for Air Liquide which is present across the value chain and a leader in the sector.

{kind=link}

Q3 results

Q3 results came in line with sell-side equity consensus expectations. Sales dropped by 17% vs the previous year due to lower energy prices pass-through and foreign exchange effects. Electronics and large industries declined while industrial merchant and healthcare grew strongly. Guidance for the fiscal year was maintained and both operating margin and net profit margins are expected to rise with net profit being ca. 20% higher. We view the non-surprising results positively.

Outlook, valuation, and investment recommendation

We value industrial gas companies using EV/EBITDA and PE multiples. Our forecasts are largely in line with sell-side analyst consensus expectations. We forecast mid-single digits top-line growth (higher than industrial production) over the mid-term driven by volume expansion, new projects (including green transition-related ones), and pricing. We project €29.1 billion of sales in FY2024, assuming 5.5% growth supported by healthcare and electronics recovery, and €7.5 billion of EBITDA, at a 26% EBITDA margin with more than 100 basis points of improvement, supported by mix and cost optimization. We moreover forecast a net income of €3.6 billion and EPS of €7 per share. This implies a forward EV/EBITDA ratio of 13.4x and a forward PE ratio of 25x. This falls to nearly 23x in FY2025e as the EPS grows to €7.6 per share. We forecast €2.7 billion of free cash flow in FY2024 implying an FCF/EV yield of 2.7%. Air Liquide is trading at a slight PE and EV/EBITDA premium to Air Products and a more than 15% PE discount and 20% EV/EBITDA discount to Linde.

We forecast a mid-term EPS growth of mid-high single digits and we believe the current valuation is fair. The current PE ratio is in line with the 5-year average of 25x and the EV/EBITDA ratio is slightly higher than the 5-year average of 12x (with largely similar underlying growth rates). We value Air Liquide at 25x EPS25e implying a ca. 9% return. Being a more defensive name, we believe the stock could underperform more cyclical chemical sector stocks given the YTD outperformance vs the sector. While we believe Air Liquide is an excellent business, we have a hold rating on the stock given the unappealing IRR. We would definitely like to own the shares at a different valuation.

Risks

Downside risks include but are not limited to worse-than-expected macroeconomic conditions negatively impacting end markets, worse-than-expected pricing leading to lower sales (especially in healthcare), higher than expected interest rates given the growth profile, delays in clients' investments projects, suboptimal allocation of capital including value destructive M&A, foreign exchange risk including a weaker USD against the EUR, increasing risk-on investor behavior leading to underperformance vs cyclicals, etc.

Conclusion

We have a neutral rating on Air Liquide and do not find the risk/reward appealing at this share price. The company remains on our European quality compounders list, and we will monitor it and revisit the investment case in the future.

For further details see:

L'Air Liquide: Fully Valued Quality Compounder