PKOH - L.B. Foster Company: Too Soon To Be Confident

2023-12-08 16:09:12 ET

Summary

- L.B. Foster Company, a small provider of goods and services, has struggled with mediocre financial performance in recent years.

- The company is undergoing a transition to focus on higher growth initiatives and higher margins.

- While there have been some improvements in revenue and cash flow, there are still concerns about the company's operating history and economic conditions.

In an ideal world, investors would only like the companies that make sense to invest in. I can't speak for others, but I do often run into a firm that I like conceptually but that I recognize does not make sense for investors to buy into. This always creates an internal struggle. But at the end of the day, you have to behave as rationally as possible if you want a chance of generating attractive returns in the stock market. One good example I could point to where this internal struggle took hold recently involves L.B. Foster Company ( FSTR ), a rather small and diverse provider of various goods and services with a market capitalization of only $221.3 million. Financial performance over the past few years has been mediocre at best. Revenue has remained virtually flat while profits and cash flows have suffered. Backlog had been growing. But as of now, it has shown some signs of weakness. The stock actually looks fairly inexpensive on an absolute basis, and management has been working to reinvent the enterprise. But when you consider both economic risk and how early the company is in demonstrating its transformation, now seems a bit early to be confident in these changes.

A company in transition

There are always certain industries or market segments that have appealed to me. The more mundane the space, the more interesting I find it. And what could be more mundane than rail related technologies, precast concrete products, and similar offerings. These are the types of products that L.B. Foster has grown to focus on since its founding in 1902. Before we dig deeper into the fundamental side of the business, it would probably be helpful for us to form a better understanding of what the company does and how it operates. Operationally speaking, it has three different segments .

The first of these is the Rail, Technologies, and Services segment. Last year, this accounted for 60% of the company's revenue. Through this segment, the company sells rail products such as insulated rail joints that are used for freight and passenger railroads and industrial customers; transit products such as fasteners, cover boards, and more; concrete ties; track spikes and anchors, and more. This segment is also responsible for producing friction management products and application systems for rail customers. The purpose of these products is to help customers save on fuel and improve the life expectancy of various operating assets. And lastly, the firm also sells railroad condition monitoring systems and equipment, wheel impact load detection systems, and other devices.

Next in line, we have the Precast Concrete Products segment. This was responsible for 21% of the firm's revenue last year. Through this unit, the company produces precast concrete products under the CXT brand name, with examples being protective storage buildings, concession stands, restrooms, and more. And finally, there is the Steel Products and Measurement segment, which was responsible for the remaining 19% of sales last year. This unit, according to management, produces a wide array of products such as fabricated steel and aluminum products that are used on highways and bridges, water well threading, turnkey solutions for metering and injection systems for the oil and gas industry, and more. It also provides various protective coating services for customers, largely consisting of those in the oil and gas space.

{kind=link}

Author - SEC EDGAR Data

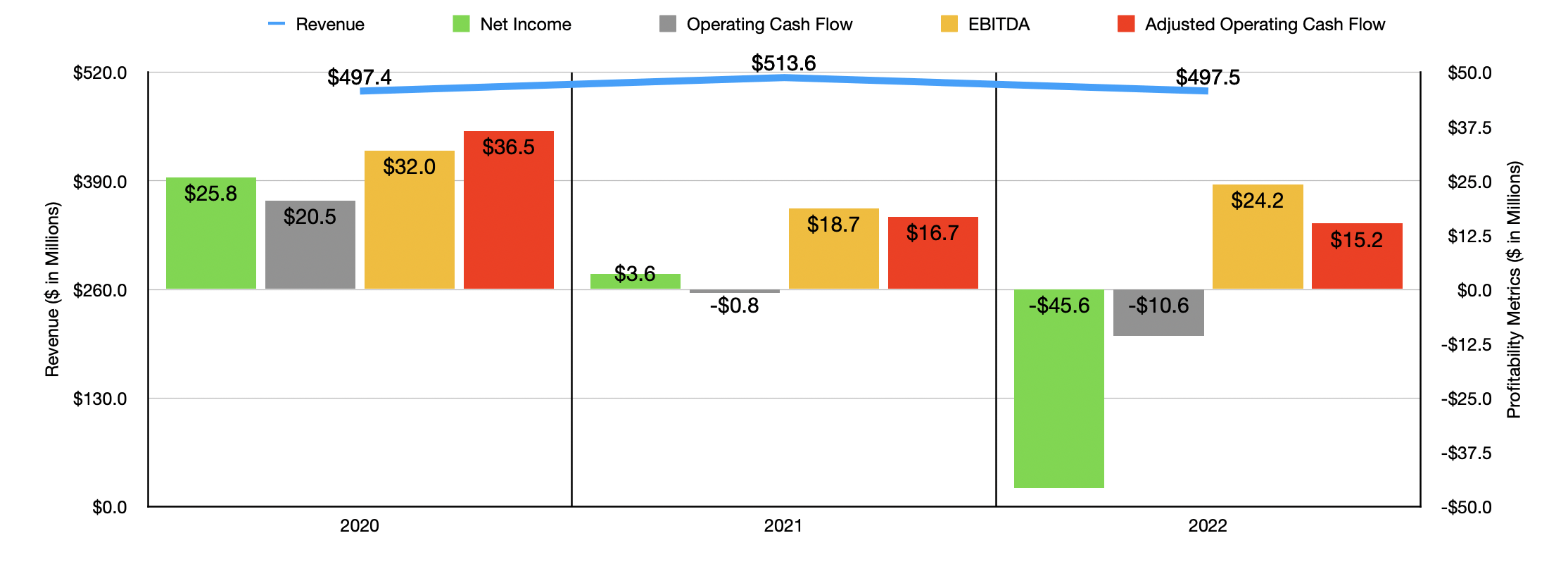

Over the past few years, financial performance achieved by the company has been rather disappointing. Revenue went from $497.4 million in 2020 to $513.6 million in 2021. But then, in 2022, sales pulled back to $497.5 million. However, you do need to dig a bit deeper to understand why this sales drop occurred. Because while the revenue decline is disappointing, when you understand the cause, the picture for the business does look up to some extent. For starters, two of the three operating segments did report an increase in revenue. The Rail, Technologies, and Services segment saw revenue inch up from $299.7 million to $300.6 million even as the firm's divestiture of its track components business pushed revenue down by $4.9 million. Organic growth of 0.9%, combined with another acquisition, helped to more than offset that decline. Even more impressive was the Precast Concrete Products business, which saw revenue skyrocket by 46.8% from $71 million to $104.2 million. One particular acquisition was responsible for $17.8 million of the sales increase. However, legacy businesses still reported a rise in revenue of 21.7% thanks to strong demand in the markets in which the company operates.

The big weakness for the business, then, came from its Steel Products and Measurement segment. Revenue plummeted from $142.9 million to $92.7 million. But even that was intentional. I say this because management sold off the company’s piling products business which was responsible for $60.8 million worth of revenue decline. Some aspects of the business actually performed remarkably well. The coatings and measurement unit of the company, for instance, reported a 37.7% spike in revenue because of strong demand.

{kind=link}

L.B. Foster Company

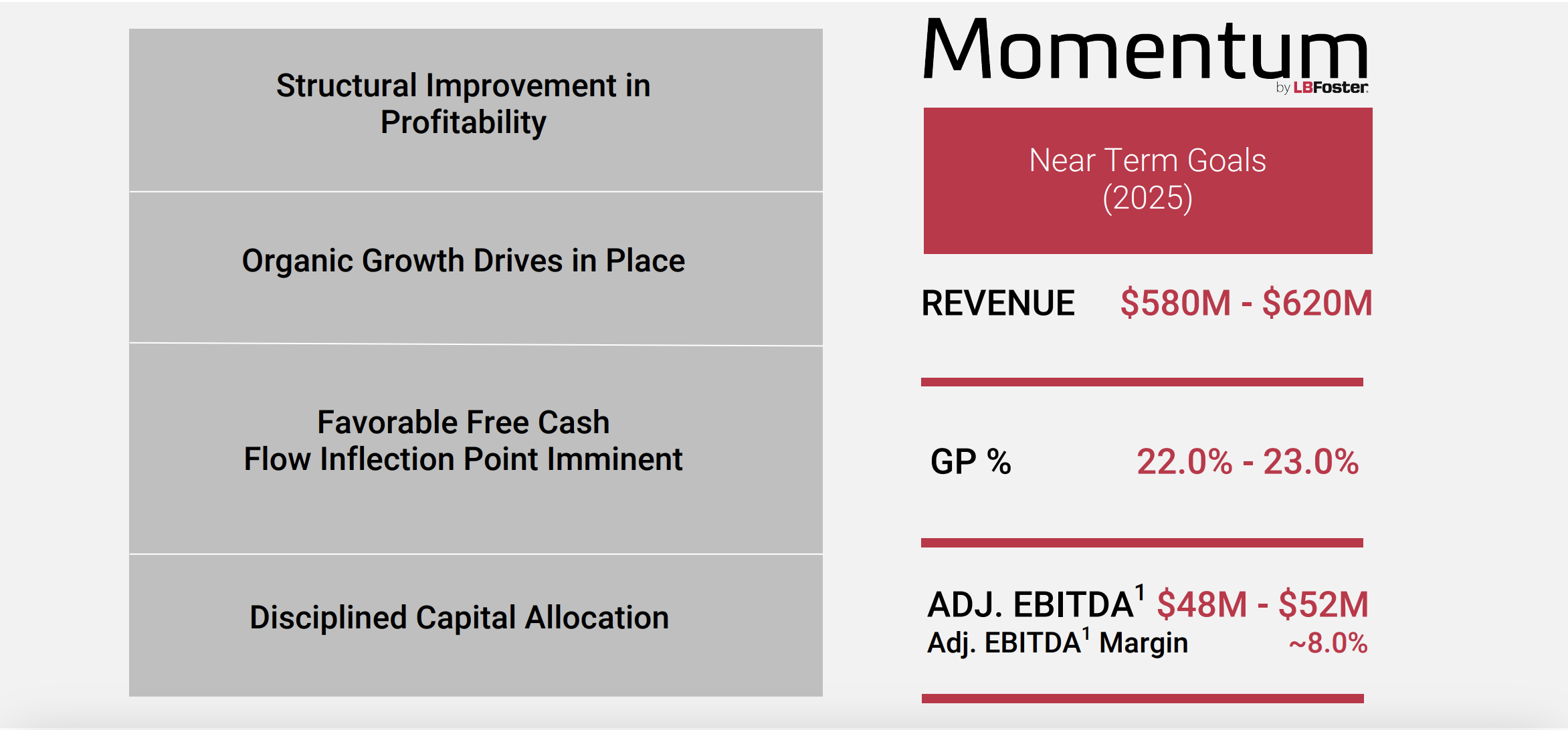

All of this has been part of a strategy aimed at reinventing the company. Management's goal is to focus on higher growth initiatives that offer higher margins. The objective, management said, is to see revenue grow moving forward, with the company targeting between $580 million and $620 million worth of revenue by 2025. However, bottom line results have been problematic. The company went from generating a net profit of $25.8 million in 2020 to generating a net loss of $45.6 million in 2022. The good news is that much of the company’s pain from 2021 to 2022 was driven by two very temporary things. First, impairment charges hit the business to the tune of $8 million. And more significantly, the company reported income tax expense of $36.7 million last year compared to the $1.1 million reported one year earlier. Other profitability metrics, like operating cash flow and EBITDA, have also shown weakness.

{kind=link}

Author - SEC EDGAR Data

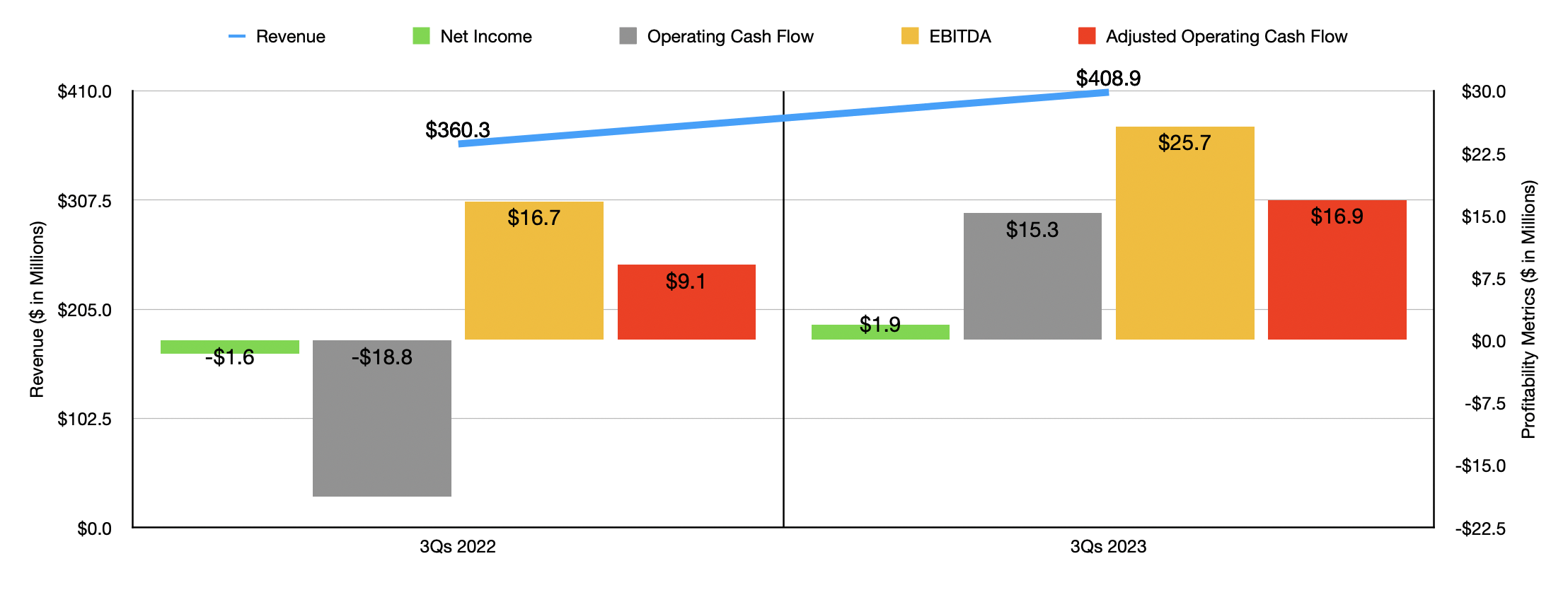

When it comes to the current fiscal year , we have seen a nice increase in revenue. Sales of $408.9 million represented a 13.5% increase over the $360.3 million reported one year earlier. Net profits of $1.9 million in the first nine months of this year marked a slight improvement over the $1.6 million loss reported one year earlier. But the real improvements involve cash flow. As you can see in the chart above, cash flow and EBITDA both fared quite well so far this year. However, in spite of new orders coming in higher this year than last year, backlog has fallen from $272.3 million at the end of 2022 to $243.2 million at present.

{kind=link}

Author - SEC EDGAR Data

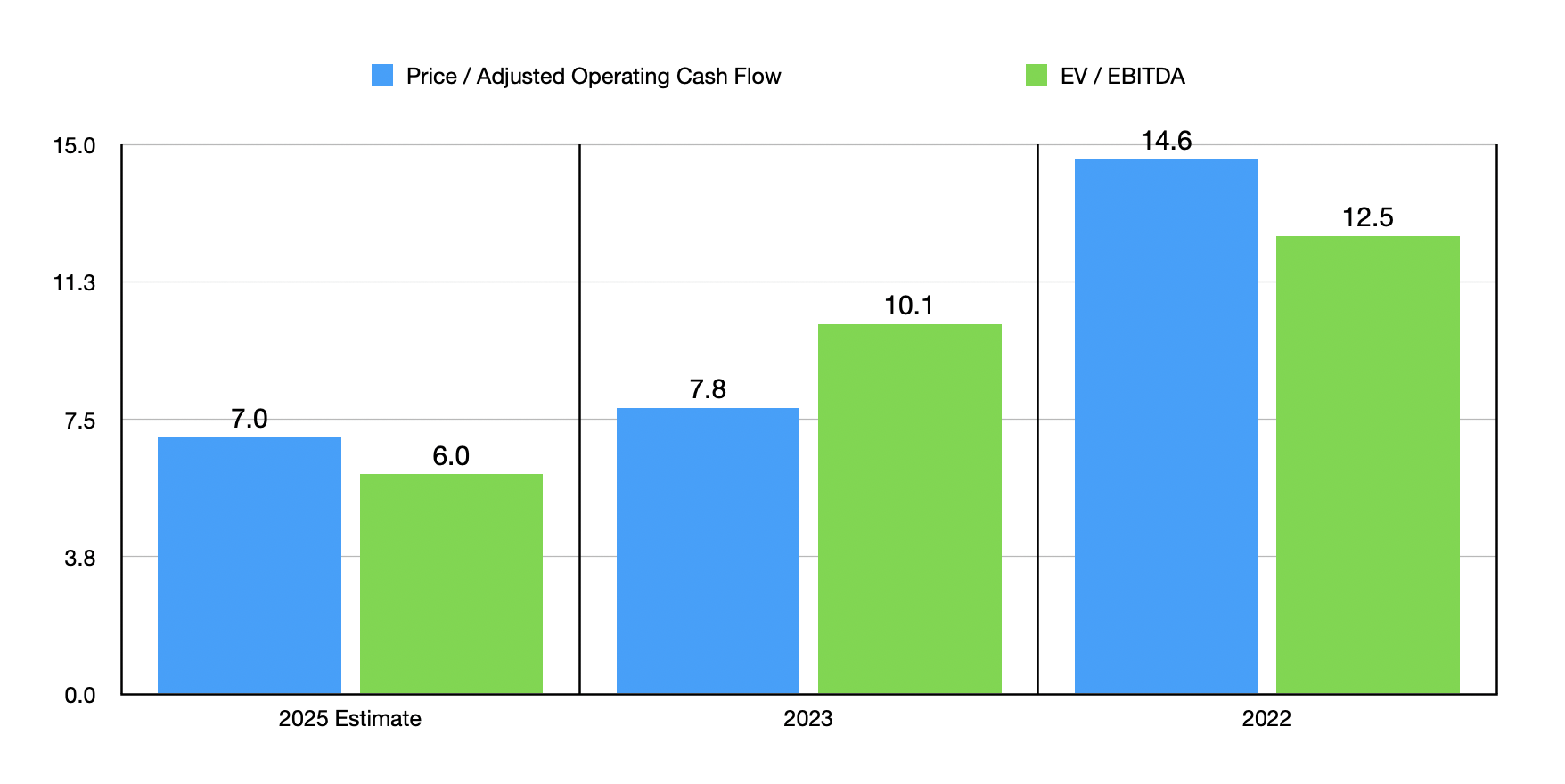

Management believes that these improvements will continue thanks to the transformation the company has undergone. They are forecasting EBITDA of between $48 million and $52 million each year by 2025. That would imply operating cash flow of around $31.4 million. As you can see in the chart above, this would result in the company getting quite a bit cheaper than it is today. But there's also a lot at risk between now and then. Broader economic concerns, combined with a rocky operating history for the company, makes this a gamble that investors don't have much reason to believe in right now. Using more recent estimates for 2023, I compared the company to five similar firms. On a price to operating cash flow basis, two of the five companies were cheaper than it. But when it comes to the EV to EBITDA approach, four of the five are cheaper.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| L.B. Foster Company |

| 7.8 |

| 10.1 |

| Park-Ohio Holdings Corp. ( PKOH ) |

| 11.8 |

| 9.0 |

| Mayville Engineering Co ( MEC ) |

| 8.4 |

| 8.4 |

| Tennant Co ( TNC ) |

| 11.8 |

| 9.1 |

| Graham Corp ( GHM ) |

| 7.7 |

| 18.0 |

| Mueller Industries ( MLI ) |

| 7.0 |

| 4.2 |

Takeaway

If everything goes the way that management believes that it will, I do think there will be upside for shareholders in a year or two. But because of the company's rocky operating history and broader economic concerns, I believe that there likely are more appealing prospects to bank on that bring with them less risk. Of course, if management can succeed in demonstrating continued improvements, my opinion on the matter will almost certainly change. But for now, the best I can give the company is a ‘hold’ rating.

For further details see:

L.B. Foster Company: Too Soon To Be Confident