LRLCF - L'Oréal: Further Upside After Strong 2022

2023-03-17 13:40:46 ET

Summary

- L'Oréal's strong 2022 results gave it like-for-like compounded annualized growth of 7.3% in sales and 9.0% in EBIT across 2019-22.

- The company grew faster than the market in all geographies and categories, including in China, and faster than Estée Lauder.

- L'Oréal expects the Beauty market to continue an average annual growth of 4-5%. We believe this means its EBIT will grow at about 9%.

- L’Oréal shares have a 34.1x P/E and an 1.6% dividend yield, largely justified by its proven resilience and strong potential.

- With shares at €383.70, we expect a total return of 30% (10.2% annualized) by 2025 year-end. Buy.

Introduction

L'Oréal SA (LRLCY) released 2022 results on February 9. Since then L'Oréal shares have been roughly flat (up 1.3%), having risen by more than 27% since their last trough in November 2022 but up only 6% from a year ago:

{kind=link}

Our current Buy rating on L'Oréal followed an upgrade in March 2022. In the one year since our upgrade, L'Oréal shares have gained 14.9% (including dividends).

L'Oréal has continued its strong structural growth. Across 2019-22, on a like-for-like basis, sales have grown at a CAGR of 7.3% and EBIT has grown at a CAGR of 9.0%. Price/mix has remained a key contributor to sales growth, and EBIT margin expanded again in 2022 despite elevated inflation and an accounting change. Just as importantly, L'Oréal grew faster than the market in all geographies and categories, including in China. L'Oréal has executed much better than arch-rival Estée Lauder ( EL ) recently. Management expects the Beauty market to continue growing at 4-5% annually on average, which we believe can generate a 9% EBIT growth. L'Oréal shares have a 34.1x P/E and an 1.6% Dividend Yield. Our forecasts indicate a total return of 30% (10.2% annualized) by 2025 year-end. Buy.

L'Oréal Buy Case Recap

L'Oréal is the #1 global Beauty company by sales, involved in every product segment and region:

| L'Oréal Sales & EBIT Breakdown ( 2 022 ) Source: L'Oréal results release (2022). NB. Active Cosmetics division renamed Dermatological Beauty as of 2022 results. SAPMENA-SSA = South Asia Pacific, Middle East, North Africa & Sub-Saharan Africa. |

Our investment case on L'Oréal' has been based on the following:

- The Beauty market will continue its strong structural growth, as an aspirational category for consumers, helped by growing demand from Asia (especially China) and premiumization (especially in Skincare)

- L'Oréal has strong global franchises built on leading brands, high-quality products, scale, innovation and marketing capabilities, and will continue to grow sales faster than the market thanks to these advantages

- L'Oréal will also grow its earnings faster than sales with natural operational leverage. We believe L'Oréal's EPS CAGR will be close to 10% over time

- Compared to its main rival Estée Lauder, L'Oréal has a more broad-based portfolio and a lower concentration in Prestige and Skin Care products, which means L'Oréal has lower growth but is lower-risk

COVID-19 was negative for L'Oréal, disrupting Travel Retail and reducing demand in areas such as Make-up and Haircare. However, L'Oréal sales rebounded strongly to surpass pre-pandemic levels in 2021, and that strong momentum has continued into 2022.

L'Oréal Structural Growth Continuing

L'Oréal's stacked 3-year like-for-like ("LfL") sales growth accelerated each quarter in 2022, from 19% in Q1 to 26% in Q4, though year-on-year growth slowed due to stronger prior-year comparables:

| L'Oréal LfL Sales Growth By Quarter (2020 - 22 ) Source: L'Oréal company filings. |

Across 2019-22, L'Oréal sales have grown at a LfL CAGR of 7.3%, with a 4.1% decline in 2020 due to COVID-19 followed by two years of double-digit growth:

| L'Oréal Sales Growth (2010 -22 ) Source: L'Oréal company filings. |

Each region contributed positively to 2019-22 LfL sales growth, with North Asia having grown at 34.0%, Emerging Markets regions at 31.6%, North America at 24.9% and Europe at 11.4%.

Price/mix has remained a key contributor to sales growth. In 2022, LfL sales growth split roughly one third each between volume (34% of LfL sales growth), price (33%) and mix (33%).

2022 sales likely still represented less than L'Oréal's full potential, due to the lingering effects of COVID-19. Travel Retail has not yet returned to normal (with international air travel volume still 25% below 2019 levels as of December ). Europe and the U.S. were affected by the Omicron variant in early 2022, and China was affected by a COVID surge from December following the end of its "zero COVID" policy. In addition, 2022 price increases were "mostly" in H2, which means their full-year impact has not yet appeared in financials.

L'Oréal EBIT has grown at a LfL CAGR of 9.0% in 2019-22, better than LfL sales growth each year, as EBIT margin continues to expand from natural operational leverage:

| L'Oréal EBIT Growth (2010 -22 ) Source: L'Oréal company filings. NB. LfL EBIT growth estimated using LfL Net Sales growth & margin changes. |

L'Oréal reports in Euros, and currency added more than 1% to reported sales and EBIT CAGR in 2019-22.

L'Oréal 2022 Results Headlines

L'Oréal's 2022 P&L, compared with the prior year and 2019, is as follows:

| L'Oréal P&L (2022 vs. Prior Years ) Source: L'Oréal results releases. |

Gross Margin fell by 153 bps in 2022 as reported, but by only 65 bps excluding currency. Substantial input cost inflation, which affected all industries in 2022, was about two-thirds offset by price increases and mix shift in L'Oréal's case.

EBIT margin still rose 41 bps in 2022 as reported, as cost margins for R&D, Advertising & Promotion and SG&A each shrunk (though A&P spend still grew 13.9% in Euros on a year-on-year basis). On a comparable basis, excluding an accounting change where some software costs were expensed instead of capitalized, EBIT margin rose 60 bps in 2022.

EPS growth was helped by both a 4.0% reduction in the share count (largely due to the repurchase of 22.6m shares from Nestlé ( OTCPK:NSRGY ) in December 2021) and a lower tax rate (22.8%, vs. 23.7% the year before). The tax rate is expected to return to "slightly below 24%" in 2023.

L'Oréal Outgrowing the Market

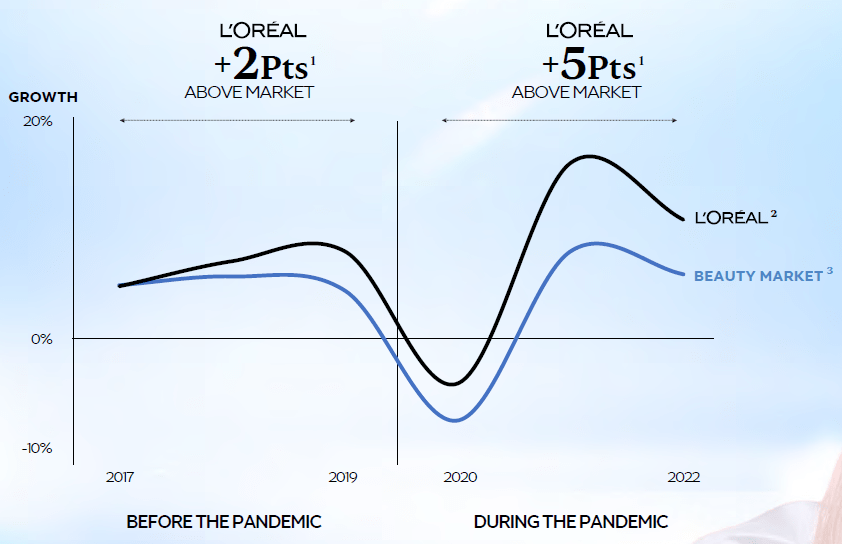

Just as importantly, L'Oréal grew faster than the market, with a LfL sales growth of +10.9% compared to market growth of around 6%. L'Oréal has grown faster than the market by about 5% annually since the pandemic, compared to an outperformance of about 2% in 2017-19:

{kind=link}

As CEO Nicolas Hieronimus said on the earnings call :

"We outperformed across all geographic zones, divisions, and categories for the second year in a row."

For example, on a LfL basis, among each of L'Oréal's divisions:

- Consumer Products grew 8.3% vs. market's 6%

- L'Oréal Luxe grew 10.2% vs. market's 8%

- Professional Products grew 10.1% vs. market's 5%

- Dermatological Beauty grew 21.9% vs. market's 9%

In mainland China, L'Oréal sales rose 5.5% on a LfL basis, even as the market shrunk in 2022 due to COVID-related disruptions.

L'Oréal's success in growing faster than the market can be attributed to a number of factors, including its brands, marketing and innovation. Distribution appears to have played a particularly key role, with L'Oréal performing well both online and offline. In 2022, L'Oréal's brick-and-mortar sales grew 11.7% LfL, benefiting from shoppers returning to physical retail after the pandemic, while e-commerce sales still grew 8.9% to 28% of the group total. Similarly, management attributed its success in China partly to a double-digit growth in e-commerce.

L'Oréal Executing Better Than Estée Lauder

L'Oréal has executed much better than arch-rival Estée Lauder recently.

L'Oréal's LfL sales growth of 8.1% in Q4 2022 compared to EL's 11% organic decline in the same quarter. EL's sales in Domestic China fell by single-digits that quarter, and its Travel Retail sales in Hainan also suffered from both the pandemic's hit to traffic and elevated inventory levels from prior quarters. Moreover, EL sales fell "single-digit organically" in the U.S. and CEO Fabrizio Freda acknowledged EL did "continue to lose share in the quarter".

For its FY23 (ending 30 June 2023), EL is guiding to sales that are flat or down 2% organically, and it expects Non-GAAP EPS to fall by 27-29% year-on-year. By contrast, L'Oréal appears to be expecting both sales and EPS growth.

Market Growth Should Give 8% EBIT Growth

Management expects the Beauty market to continue growing at 4-5% annually on average, in line with its long-term historical average (including a CAGR of about 5.5% across 2019-22):

{kind=link}

This may be conservative, at least for the near term given 2022 was still negatively affected by COVID-19. In addition, we believe the rise of the Chinese beauty market, helped in recent years by e-commerce and online media, as well as a partially similar development of the India market, can mean a higher growth rate for an extended number of years.

Even if we assume a 5% market growth, a 2% L'Oréal outperformance (in line with 2017-19) and EBIT growing 2% faster than sales (in line with 2019-22, which are difficult years), L'Oréal will achieve an EBIT CAGR of 9%.

Is L'Oréal Stock Overvalued?

At €383.70, relative to 2022 financials, L'Oréal shares have a 34.1x P/E and a 2.3% Free Cash Flow ("FCF") Yield:

| L'Oréal Earnings, Cash Flows and Valuation (2019 - 22) Source: L'Oréal company filings. |

We believe L'Oréal's current valuation multiples are largely justified because of its proven resilience and strong future potential, though in our forecasts we assume a small de-rating to a 32.5x P/E.

Working capital meant a cash outflow of €1.0bn in 2022, reducing FCF by about 20%. Management attributed this to prudent inventory build-up to mitigate logistic disruptions as well as higher input costs, and predicted L'Oréal "should not see this type of increase or at least of this magnitude this year".

For 2022, L'Oréal raised its annual dividend by 25%, from €4.80 to €6.00, representing a Dividend Yield of 1.6%. (In addition, shareholders of two full calendar years or more will receive a 10% loyalty bonus.) This represents a conservative Payout Ratio of just 53%. L'Oréal also bought back €500m of its shares in 2022.

L'Oréal had €3.0bn of Net Debt at 2022 year-end, largely a legacy of the €8.9bn repurchase of shares from Nestlé in December 2021. We expect it to return to Net Cash in the next few years.

L'Oréal continues to hold a 9.44% stake in Sanofi, worth €10.7bn at current prices. L'Oréal's share of Sanofi earnings is partially captured in the P&L through Sanofi dividends received.

CapEx is expected to increase from 3.5% of sales in 2022 to 4% in 2023.

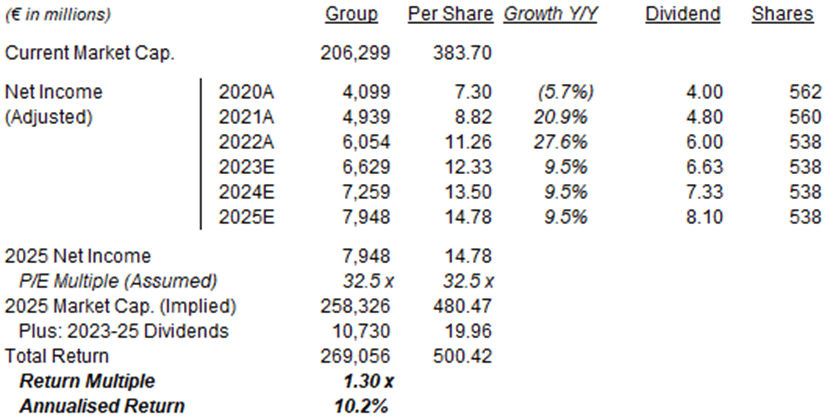

L'Oréal Stock Return Forecasts

We update our 2022 EPS forecast with the actual figure, and raise our 2023 forecast slightly. We now assume:

- 2022 EPS was €11.26 (we expected €11.05)

- 2023 Net Income growth of 9.5% (was 6.5%)

- From 2024, Net Income to grow at 9.5% each year (unchanged)

- 2022 share count of 538m (unchanged)

- From 2023, the share count to be flat (unchanged)

- Dividend to grow at 10.5% each year (unchanged)

- P/E of 32.5x at 2024 year-end (unchanged)

Our new 2025 EPS forecast of €14.78 is 5% higher than before (€14.11):

{kind=link}

Our dividend forecasts implies that the Payout Ratio will reach 55% in 2025.

With shares at €383.70, we expect an exit price of €480 and a total return of 30% (10.2% annualized) by 2025 year-end.

Conclusion: Is L'Oréal Stock A Buy?

We reiterate our Buy rating on L'Oréal stock.

For further details see:

L'Oréal: Further Upside After Strong 2022