LRLCF - L'Oréal: Robust Growth Momentum With Aesop Acquisition A Key Catalyst

2023-10-25 16:51:46 ET

Summary

- LRLCF reported impressive Q3 results with organic sales growth of 11.1% and total sales of 10 billion euros.

- The company saw growth across all divisions and regions, with strong performance in the Consumer Products and Dermatological Beauty segments.

- LRLCF's recent acquisition of Aesop is expected to drive substantial growth in the Chinese market and improve its overall outlook.

Summary

Following my coverage of L'Oréal ( LRLCF ), I recommended a buy rating due to my expectation that LRLCF's growth and margins would recover towards normalcy. This post is to provide an update on my thoughts on the business and stock. I reiterate my buy rating for LRLCF due to its strong current quarter performance, which has shown robust growth across its product range and operating regions.

Investment thesis

For the third quarter, LRLCF reported impressive results , with organic sales growth of 11.1% and total sales of 10 billion euros. The LRLCF group also saw an 11.1% increase in like-for-like sales. Volume and value have both continued to rise, contributing to this remarkable performance. The LRLCF Dermatological Beauty and Consumer Products Divisions, in particular, performed exceptionally well, and growth was seen across every division.

The Consumer Products segment grew by 13.4% year over year in the third quarter, while the Dermatological Beauty segment grew by 28.1%. Both new and old markets shared in this expansion equally. CeraVe has expanded significantly across the globe, particularly in North America. The company's management also emphasized that they had not noticed any degradation in their product.

Organic sales growth for LRLCF was in the double digits in all of the company's major regions in the third quarter: Europe growing 16.2%, North America growing 11.8%, Latin America growing 25.4%, and SAPMENA-SSA growing 23.7%. Consumer goods and dermatological beauty both did well in Europe, with La Roche-Posay and CeraVe contributing to the success of the latter. The Consumer Products division enjoyed the benefits of robust innovation in North America, particularly in the makeup category centered on YSL and Armani. All Latin American countries saw double-digit growth in both volume and value, with Mexico and Brazil particularly impressive. Both the Consumer Products division and L'Oreal Dermatological Beauty's CeraVe product line contributed significantly to SAPMENA-SSA's overall growth in the skincare market. The use of cosmetics also returned to pre-pandemic levels.

The performance of the company's sales channels has been strong. Sales for the company increased by double digits, both virtually and physically. In particular, the success of Lancôme on Amazon (AMZN) which was launched in early 2023. Since 2022, online shopping in mainland China has also been doing well, expanding at a double-digit rate.

LRLCF also announced on August 30 that it had finished the acquisition of Aesop , a luxury skincare and fragrance brand with strong growth prospects, especially in the Chinese and international travel retail markets. As a result, I believe this acquisition will experience substantial growth in China over the next few quarters, significantly improving its outlook.

Valuation

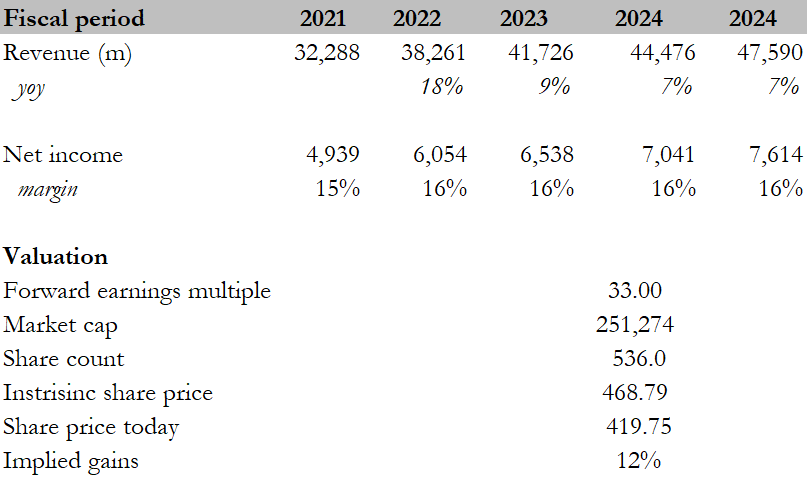

My target price for LRLCF based on my model is approximately $468. This valuation is influenced by several pivotal factors. To start, LRLCF's third quarter showcased commendable financial performance, with both organic sales growth and like-for-like sales expanding at double-digit rates. Even in the current environment where inflation remains subdued, the company's leadership consistently emphasizes the growth in both volume and value, suggesting the inelastic nature of their product. Moreover, LRLCF's success isn't limited to a single region; a majority of its primary markets are experiencing double-digit growth in organic sales, emphasizing its global resonance. Beyond traditional brick-and-mortar outlets, LRLCF's digital commerce is thriving, especially in China, where online sales are expanding at a notable double-digit rate. This growth trajectory in China gains further significance with LRLCF's recent acquisition of Aesop, which possesses substantial growth potential in the Chinese market. Coupled with LRLCF's robust online sales in mainland China, this acquisition positions the company strongly in the world's second-largest economy.

{kind=link}

Peers include Reckitt Benckiser Group (RBGLY), Haleon (HLN), and PZ Cussons (PZCUF). When examining these peers, the median forward price-to-earnings [P/E] multiple stands at 16.38x. Their expected growth rate for the upcoming twelve months is pegged at 2%, and they have a median net margin of 14.27%. In contrast, LRLCF boasts a forward P/E multiple of 30x, an anticipated growth rate of 9%, and a net margin of 15.34%. Given LRLCF's superior performance across all these metrics compared to its peers, it's reasonable to conclude that LRLCF deserves to trade at a higher valuation. In my previous post, LRLCF was trading at a forward P/E of 33x. Considering the company's strengths and the strategic steps it has undertaken, which I detailed earlier, I believe it should continue to trade at this 33x multiple which is also in line with its historical average. By applying this multiple, the price target for LRLCF is $468.79, representing a potential upside of 12%. Based on this analysis, I continue to recommend a buy rating for LRLCF.

Risk

A potential downside to my buy recommendation for LRLCF is its elevated forward P/E multiple, which can be a double-edged sword. Due to its premium valuation, LRLCF carries the responsibility of consistently delivering strong financial results. Should LRLCF's future performance fall short of market expectations, its forward P/E could experience a substantial decline, especially when considering that the median for its peers is 16.38x, which is half of LRLCF's current multiple. Even a modest 10% correction in its valuation could have a pronounced effect on its stock price, potentially erasing the anticipated 12% upside and bringing it down to a neutral position.

Conclusion

LRLCF delivered a standout performance in the recent quarter, showcasing impressive organic sales growth and robust total sales. Both the Dermatological Beauty and Consumer Products Divisions exhibited significant growth, underscoring the company's strength across its portfolio. LRLCF's global footprint is evident, with all major regions experiencing substantial organic sales growth. Their sales channels, both digital and traditional, have seen consistent growth, further bolstered by the strategic acquisition of the luxury skincare brand Aesop, which promises significant growth potential in markets like China. When compared with peers, LRLCF's anticipated growth rate and net margin clearly surpass them, making its forward P/E multiple justified. Given the company's strengths and the strategic initiatives it has embarked upon, I firmly believe in its potential for further appreciation. Hence, I continue to recommend a buy rating for LRLCF.

For further details see:

L'Oréal: Robust Growth Momentum With Aesop Acquisition A Key Catalyst