LRLCY - L'Oreal: An Incredibly High Quality Expensive Business

2023-06-30 04:44:29 ET

Summary

- L'Oreal is the premier beauty business, with over 30 brands contributing to a market-leading position.

- L'Oreal's growth has been consistent and robust in the last decade, with industry tailwinds expected to support this level going forward.

- Margins are equally attractive, with incremental improvements achieved.

- LRLCY stock is trading at a noticeable premium to its historical average. Although justified, this leaves no further upside in our view.

Investment thesis

Our current investment thesis is:

- L'Oreal is the leading beauty business, with 11 billionaire brands across the beauty spectrum.

- We believe continued industry tailwinds will support growth in the coming years.

- The industry is highly attractive due to sticky demand and the lack of impact from external factors.

- L'Oreal is currently trading at its fair value, implying no upside.

Company description

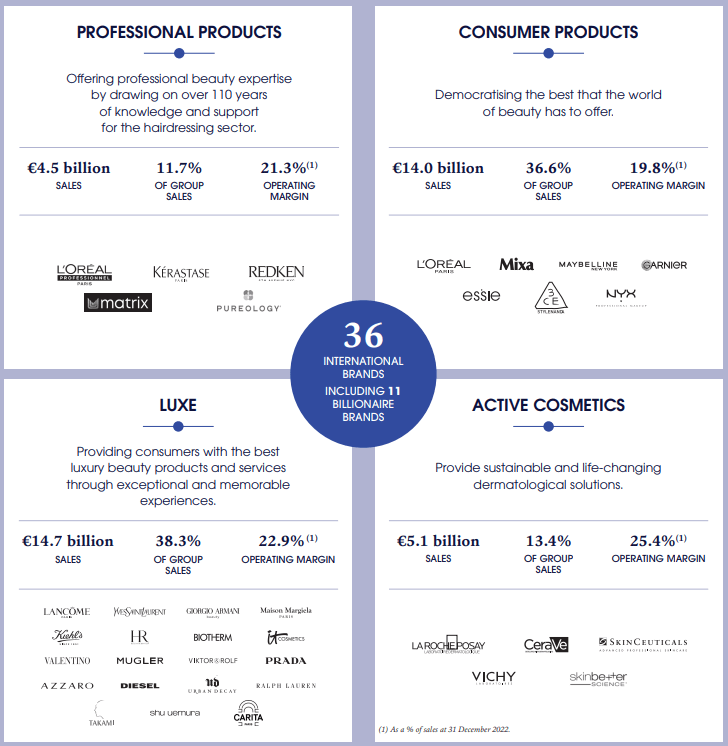

L'Oréal S.A. ( OTCPK:LRLCY ) is a global cosmetics manufacturer and seller, offering a wide range of products for both women and men. The company operates through four divisions: Consumer Products, L'Oréal Luxe, Professional Products, and Active Cosmetics.

Their product portfolio includes shampoos, skincare items, hair care products, shower gels, deodorants, and more.

L'Oréal sells its products under various well-known brands such as L'Oréal Paris, Garnier, Maybelline New York, Lancôme, Yves Saint Laurent, Kiehl's, and many others.

Most recently, L'Oreal acquire Aesop from Natura &Co ( NTCO ), paying $2.25bn , which implies a c.20x EBITDA multiple. Aesop is a business that has developed a strong cult following, through the development of quality products. It was the crown jewel in the Natura business (See our analysis here ) and we believe this is a good addition to the portfolio.

Share price

L'Oreal has broadly tracked the market in the last decade, generating a total return of 212%. This performance is a reflection of a continuation of the company's strong trajectory.

Financial analysis

{kind=link}

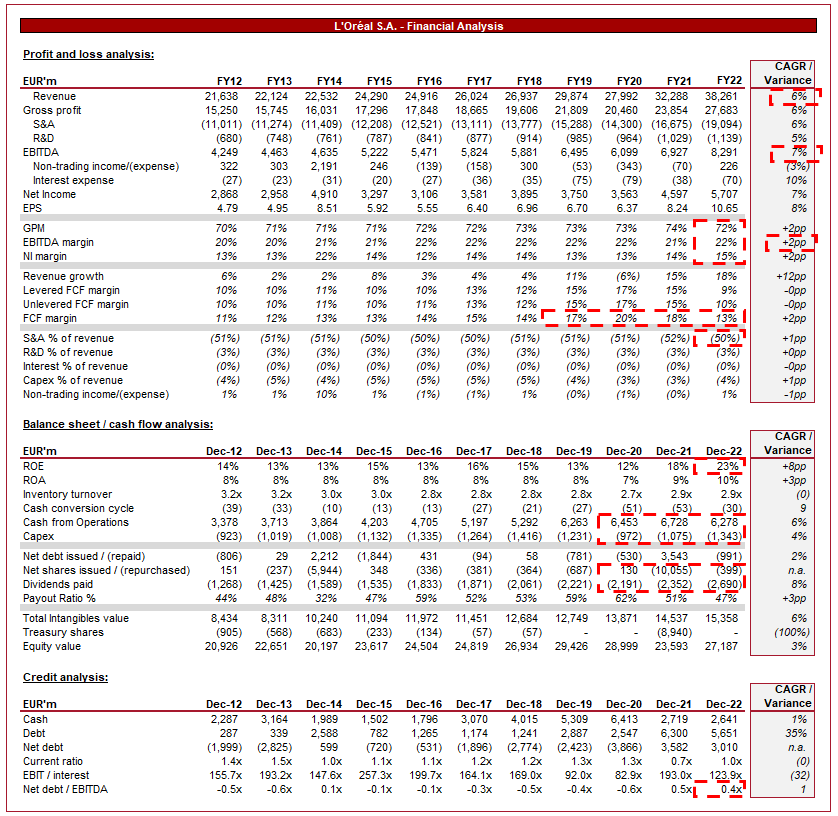

Presented above is L'Oreal's financial performance for the last decade.

Revenue & Commercial Factors

L'Oreal has grown its revenue at a consistent rate in the last decade, with only one period of negative growth. This is a reflection of its impressive resilience to external factors, allowing the business to sustainably win over time.

L'Oreal's revenue is well diversified across its 4 business segments, reducing concentration risk and allowing the business to exploit its deep expertise to expand into related segments.

{kind=link}

Business model

L'Oreal operates with a focused business model centered on creating beauty products. Unlike the likes of LVMH ( OTCPK:LVMHF ), the business is not expanding into related industries but instead in segments within the wider beauty industry. The business is a beauty powerhouse and has successfully positioned its group, through the 36 brands it owns (Plus Aesop), to capture many of the sub-segments within the market. Consumer, for example, is on the affordable side, whereas Luxe is premium. Active is health driven through a dermatological focus, whereas Professional Products is for the Professional Beauty industry.

L'Oréal maintains a strong competitive position in the beauty industry. The company benefits from its extensive product portfolio, deep expertise that only continues to expand as it acquires businesses and its global scale. L'Oréal has a strong presence in key markets worldwide and invests heavily in R&D to drive product innovation. Its sole focus on Beauty is likely attributable to its success, allowing the business to maximize the value of its industry expertise across its brands.

Beauty/Cosmetic Industry

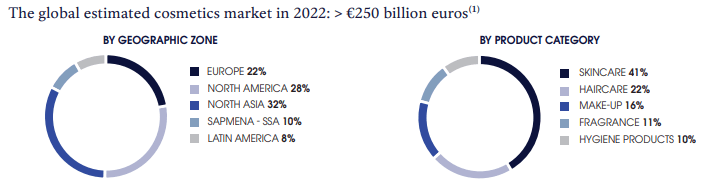

L'Oreal estimates that the cosmetics industry is over €250bn in size, primarily comprised of skincare sales. Growth in the market has been driven by Asia and LatAm, as demand for Western goods increases, as well as the lack of competitive alternatives.

{kind=link}

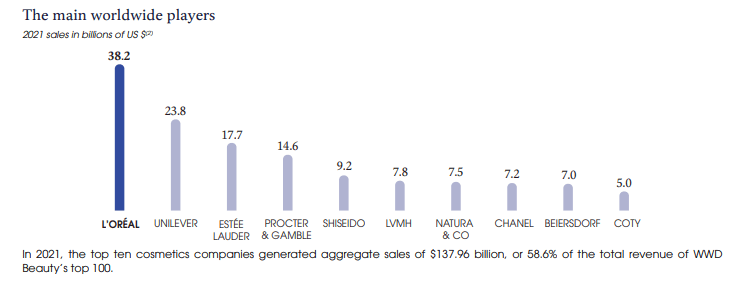

Within this market, L'Oreal is the dominant leader, with almost double the sales of the next largest competitor. Further, unlike these peers, L'Oreal is wholly focused on Beauty.

{kind=link}

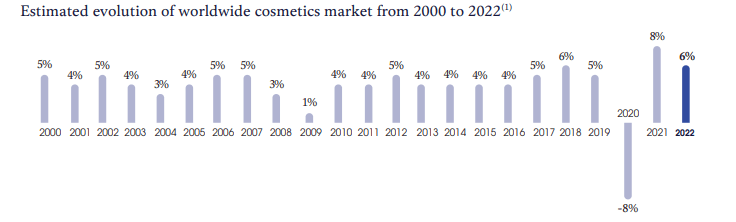

One of the primary factors that makes the cosmetic industry attractive is its relative lack of volatility. As the following graph illustrates, demand has remained consistent for over 20 years, only declining due to Covid-19. This suggests investors have no reason to fear recessions/downturns, or even inflationary pressure. This is due to the structural integration of these products into the lives of consumers. When individuals find a product they like, rarely are they switched or replaced. This contributes to recurring/sticky demand. Essentially inelastic demand. This allows L'Oreal to increase prices without a material impact on volume.

{kind=link}

Further, L'Oreal targets the most lucrative segment of the population. Beauty products are primarily purchased by Women, who make up more than half of the U.S. population, and control or influence 85% of consumer spending . As a result of this, winning over Women is critical to an industry with outsized returns.

The concept of well-being and self-care has gained prominence, leading to an increased focus on holistic beauty routines that prioritize mental and emotional wellness. This is driven by social signaling and a greater understanding of health and wellness. We expect this to support further growth in the coming years, as an increasing number of people purchase products such as skincare, with usage beginning at an earlier age.

In conjunction with the above, consumers are increasingly seeking natural and organic beauty products, driven by growing health and wellness awareness, as well as a growing hesitancy over the impact of lab-developed ingredients. L'Oréal has responded to this trend by expanding its range of natural and organic offerings which is likely a primary reason for the acquisition of Aesop.

The growth of e-commerce and digital platforms has facilitated the rise of direct-to-consumer channels in the cosmetics industry. Brands are now responsible for a large portion of marketing to customers and therefore are eager to eliminate the middleman. The benefits of scale are perfectly illustrated here as L'Oreal can exploit its expertise to implement this across its brands, maximizing value.

Influencer marketing has become a powerful tool for beauty brands to reach and engage with their target audience. Social media platforms, such as Instagram, YouTube, and TikTok, have become significant channels for beauty influencers to showcase products and share tutorials. We believe this represents a threat to L'Oreal more than a weakness. The business already dominated the historical social channels, be it TV or Print, but social media has a greater "grassroots" impact. What we mean by this is collaboration by consumers will always have a greater impact. This means if they consumer are interested in hyping a brand, no level of marketing can compete against a successful trend. Generally, brands that end up trending or are hyped are never the leading ones, as consumers always seek the next new thing. This leaves L'Oreal with a consistent quandary of expensive acquisition (Aesop) or a gamble on it fizzling out ( Becca Beauty ).

Opportunities

The men's grooming industry has witnessed significant growth in recent years, driven by changing societal norms and increased interest in personal care among men. We believe this segment will continue to grow, for many of the factors discussed above, representing a strong opportunity for L'Oreal. The key in this segment is to develop or acquire brands that resonate with men, as it is unlikely most of L'Oreal's current brands will.

Growth for L'Oreal will be derived from continued overseas expansion, as the business seeks to reach new consumers and expand its total addressable market. L'Oreal refers to this as glocalization; globalizing its brands while respecting local differences and catering to diverse consumer aspirations. We suspect this strategy will continue to be fruitful, as economic development in emerging markets grows the middle class.

Equally, there are risks with geographical slowdowns. Estee Lauder's ( EL ) share price tanked in recent months due to a slowdown in China. This remains a near-term risk to L'Oreal if the issues become contagious. We remain unconcerned long-term, however.

Further, innovation will continue to represent an area of growth, as R&D pushes the limits of what beauty products can achieve. L'Oreal's commitment is illustrated in its Capex and R&D growth in the last decade, which is a healthy ratio of revenue in our view to shore up future growth. The end goal will always likely be "solving" anti-aging, but there are various other avenues to exploit. This is also a risk for the business, as it could see brands become obsolete, but the advantage L'Oreal has is that it can acquire these competitors in many cases. The Aesop acquisition is the perfect illustration of this.

Margins

L'Oreal has attractive margins, with a GPM of 72%, EBITDA-M of 22%, and a NIM of 15%. Over the historical period, margin improvement has been gradual but a consistent achievement.

The attractive margins are a reflection of the industry, with low production costs while the premiumization of brands and the value proposition allow L'Oreal to demand high prices.

Due to the level of competition, L'Oreal is not in a position to increase prices too aggressively, but the lack of margin dilution due to inflationary pressures reflects an ability to pass on cost increases successfully, which is an extremely attractive trait.

Balance sheet and Cash Flows

L'Oreal's inventory turnover and CCC have remained flat across the historical period, reflecting an immense focus on operational management. We believe the business does have scope for improvement and should target a 3.5x turnover to maximize cash generation.

Speaking of cash flows, L'Oreal's free cash flow generation has been impressively consistent, again illustrating the robust business model.

L'Oreal's Management has been hesitant to utilize debt, with the company's ND/EBITDA ratio at only 0.4x. This gives the business flexibility to raise if required.

Distributions to shareholders have primarily come in the form of dividends, although the business has regularly conducted buybacks. Given the large cash depletion in recent years, we suspect the buybacks will not continue at the level seen in FY21.

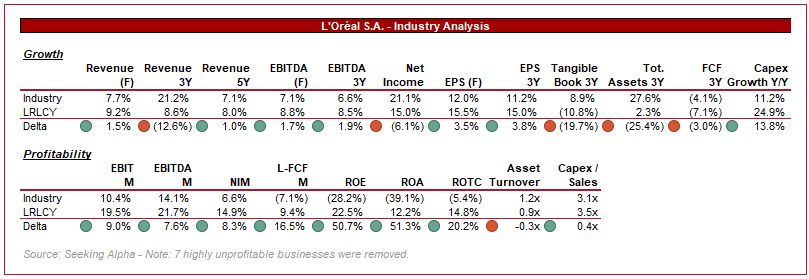

Industry analysis

{kind=link}

Presented above is a comparison of L'Oreal's growth and profitability to the average of its industry, as defined by Seeking Alpha ( 21 companies).

L'Oreal's dominance of this market is reflected in its financial performance, with the business outperforming on both growth and margins.

The expectation for margin superiority is clear. The business is the largest in the market, allowing for scale economies and a focus on high-margin business. However, given it is a mature business, we would expect weakness in growth relative to growth businesses.

Valuation

Valuation (Tikr Terminal)

L'Oreal is currently trading at 27x LTM EBITDA and 22x NTM EBITDA. This is a noticeable premium on its 10Y historical average.

The main bull arguments are:

- L'Oreal has significantly increased in scale while at least maintaining economics.

- Further development of its brands and new acquisitions

- Increased relative market share

- Improved margins.

We do believe L'Oreal warrants the premium valuation it currently has, however, we struggle to see upside beyond this. A NTM EBITDA multiple of 22.5-25x looks appropriate for a business of its current metrics.

Final thoughts

L'Oreal is a fantastic business. The company owns a wide range of brands across the key beauty segments, giving it an almost impenetrable position. The industry itself is highly attractive due to its resilience and the consistency of repeat purchases.

We believe industry trends will support continued growth at a similar level to what has already been achieved, with the potential for slight margin improvement.

With a quality business such as this, a discount is rarely on offer. We believe the company is trading at its fair value.

For further details see:

L'Oreal: An Incredibly High Quality Expensive Business