LRLCF - L'Oreal: You Won't Beat The Market With This Price

2024-01-06 07:25:51 ET

Summary

- L'Oréal is my go-to buy when the market drops.

- The beauty industry is resilient and L'Oréal is well-positioned for growth in luxury, wellness, and developing markets.

- The company's family ownership, experienced management, and strong financials contribute to its appeal.

- Valuation is currently too high, and beating the market with such prices seems unlikely.

- A wait-and-watch approach is the best option for quality-seeking investors.

My Thesis

I think L'Oréal (LRLCF) is one of the highest-quality businesses in the world. At the right price, I would buy it like it's Black Friday. The combination of diversification among different growing markets, high and stable margins, high returns on capital, advantages to size, barriers to scale, family-owned business, innovation, and strong brands are what every investor wishes for. It is not a coincidence that Fundsmith holds a significant chunk of L'Oréal in its portfolio; it is a superb company.

However, above 40 times earnings, the current price leaves no room to beat the market. In my view, investors will likely meet market returns or less at such prices.

I believe that at the right price, we will see low-risk outperformance for many years.

Industry & Business

In May, McKinsey published their beauty industry report , highlighting major growth avenues and initiatives that companies need to pursue for strong growth. We will see what the market demands and how L'Oréal aligns with those objectives.

L'Oréal holds the largest market share in the beauty industry, standing at mid-teens. It is the 1# or 2# competitor in each market segment: Skincare, Makeup, Haircare, Fragrances, and Hair Colour.

The company divides its business into four divisions: L'Oréal Luxe, L'Oréal Dermatological Beauty, Professional Products, and Consumer Products.

What I particularly appreciate about the beauty industry is its resilience, enduring economic turbulence. This is one reason I own Ulta ( ULTA ), for example, another high-quality compounder. This characteristic makes the beauty business highly desirable, providing decent free cash flow even in challenging economic conditions.

According to McKinsey, the market is forecasted to grow at a 6% annual rate, and L'Oréal is well-positioned to outpace that rate, as it has done in the past, whether through acquisitions or strategic market positioning. L'Oréal achieved a growth of around 9% CAGR in the last five years, and with its strong focus on beauty, I don't see that changing. The barriers to scale are massive, and if L'Oréal perceives a company as a threat, it could be a great catalyst for an acquisition. From the beauty report :

While the past decade has seen a number of new and independent labels benefit from steadily lower barriers to entry, growth beyond a successful initial run to achieve meaningful scale remains elusive for many. Out of 46 brands founded in or after 2005 with global retail sales of $50 million to $200 million by 2017, only five exceeded $250 million in global retail sales five years later, in 2022. Only two achieved global retail sales of more than $750 million.

Now, let's compare the McKinsey report with L'Oréal:

the true luxury and ultraluxury beauty market has the potential to double, from around $20 billion today to around $40 billion by 2027.

Approximately 35% of L'Oréal's revenue comes from the luxury segment, constituting the lion's share of its revenue and serving as a significant contributing factor for L'Oréal's anticipated growth.

Now, turning to another positive growth factor: wellness.

As consumers are increasingly engaging with beauty products and services to not only look good but also feel good, the lines between beauty and wellness are expected to continue blurring...

The melding of wellness and beauty will only become more pronounced in the years ahead, in line with an expected CAGR of 10 percent to 2027 for the wellness industry. This trend will represent an untapped opportunity for many, with first-mover advantage for the players that get it right.

L'Oréal has a high flyer in this segment, with The Dermatological Beauty division capturing 16% of revenue and growing by 29% in the first half of the year. The company emphasizes this segment significantly, a very positive initiative in my view.

Now, looking at growth by region, we see developing markets such as the Middle East and Africa projected to grow by a 12% CAGR to 2027, and Asia projected to grow at around 8%.

In the Middle East and Africa, L'Oréal experienced growth of more than 20% in the first half of the year, which is very positive in my view. In China, the growth was slower at 3%, which makes sense given the weak growth in this segment in the last couple of years.

Another important factor L'Oréal has to face is the e-commerce growth, with McKinsey projecting a 12% CAGR for the e-commerce segment. In my view, L'Oréal is well-suited to benefit from this trend, as around 30% of its sales are derived from online sales.

Management and owners

Another factor I appreciate about L'Oréal is the fact that it's a family-owned business. Research shows that family-owned businesses tend to outperform over the long term due to factors such as long-term thinking and conservatism. About 34% of the company is held by the Bettencourt Meyers family, which has a connection to the founder of L'Oréal, with his granddaughter serving as the Vice Chairman of the board.

{kind=link}

Regarding the management, both the CEO and the Chairman of the company have been with the company for decades, holding various roles within the value chain. I value this factor as they embody the culture that has made L'Oréal what it is. The CEO has held major positions in L'Oréal divisions, providing a wealth of experience.

The compensation structure is fairly standard, with metrics for compensation derived from sales and EBIT. There's nothing particularly special, such as ROIC, but there is a metric that factors in market share expansion, which is positive in my view.

Another important consideration is that both the Chairman and the CEO have spent most of their careers at L'Oréal, likely making a significant portion of their net worth in shares of L'Oréal.

The numbers I like

L'Oréal's growth is linear, indicating its resilience over the long term. Moreover, we can expect operating leverage as the company increases its EBIT margin by about 0.30% every year. Margins are stable as well, indicating the pricing power that L'Oréal possesses.

These high margins contribute to a factor I appreciate about L'Oréal, which is the return on capital. A high return on capital over a long period of time is a common trait among compounders. Michael Mauboussin conducted a recent study about the spread between the ROIC and the WACC, pointing out that if the spread is also growing, the results are excellent.

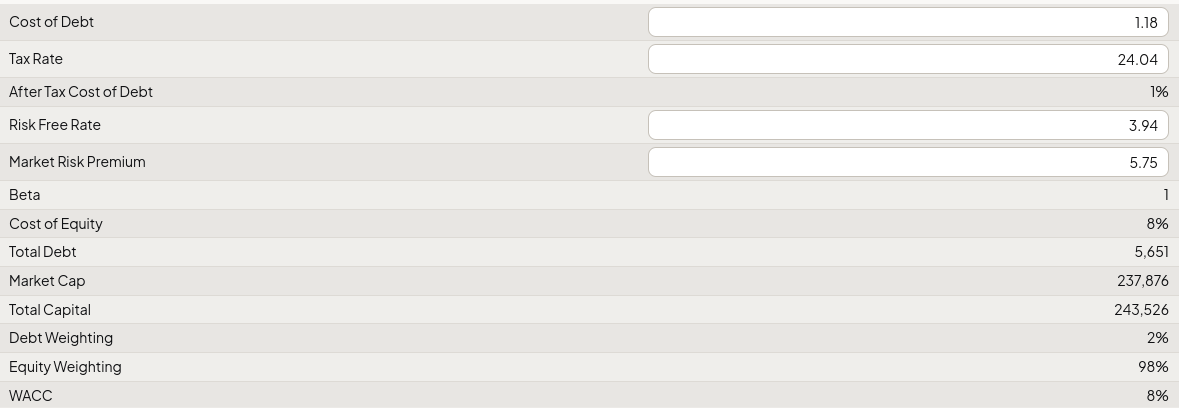

Here are the ROIC and ROCE figures for L'Oréal, both experiencing growth and significantly surpassing the 8% WACC (calculation detailed in the valuation section).

L'Oréal has a strong balance sheet in my view, with $3.4 billion in net debt, allowing it to cover its debt within less than one year of free cash flow. The current ratio stands at 1, and the debt/equity ratio is 35%. I see it as a robust balance sheet with no apparent threats.

In terms of returns to shareholders, the div yield is at 1.4%, reflecting the high valuation of the stock. However, L'Oréal pays out a significant amount of cash, with the payout ratio at 55%. Dividends per share grow at around 10% a year. Additionally, there are occasional buybacks, with shares outstanding decreasing by around 10% in the last decade.

Regarding L'Oréal, we received a financial review in September, in addition to the half-year results. Top-line growth was impressive at 12%, with like-for-like growth showcasing the robust resilience of this market during tougher economic times, especially with interest rates at their highest in years. The luxury segment experienced slower growth, aligning with the overall market slowdown. Dermatological Beauty showed outstanding growth at 28% like-for-like, proving to be a significant factor contributing to the overall positive performance. Latin America and the Middle East & Africa demonstrated exceptionally strong growth, both exceeding 20%, while Asia experienced declining sales, reducing the overall growth.

What's more interesting is that in Europe, where the economic situation is less positive than in the US, there was a remarkable 16% growth-an additional indicator of resilience. L'Oréal has also successfully completed the Aesop acquisition, further strengthening its luxury segment. In general, these results are positive in my view. However, despite the impressive growth rate, I would not classify the stock as a buy. The valuation is too high, even considering such growth, and I will now explain why.

Valuation

This is where things start to get challenging for buyers. Forty times earnings is too high, even for a high-quality, low-risk company like L'Oréal. I have no desire to pay such a high multiple, having experienced similar situations that resulted in losses. Unless there is truly significant growth, which is not the case here, I prefer to buy stocks when they are below their historical multiples. This provides potential for multiple expansion, but in this case, there's a risk of multiple contraction. A 1.6% free cash flow yield is also considered too expensive in my assessment.

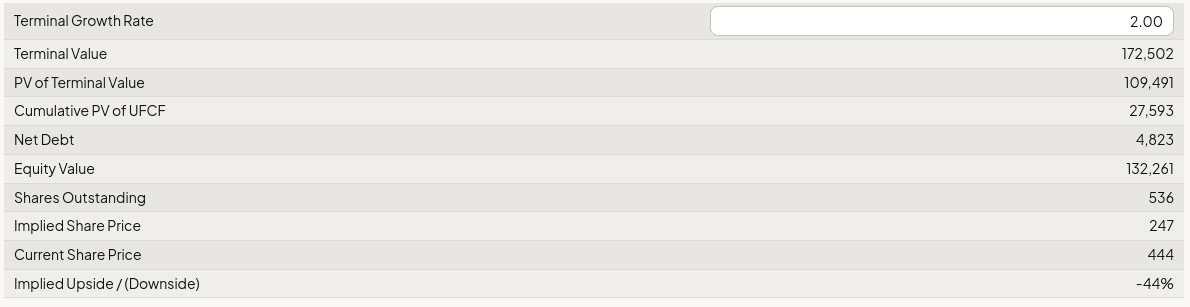

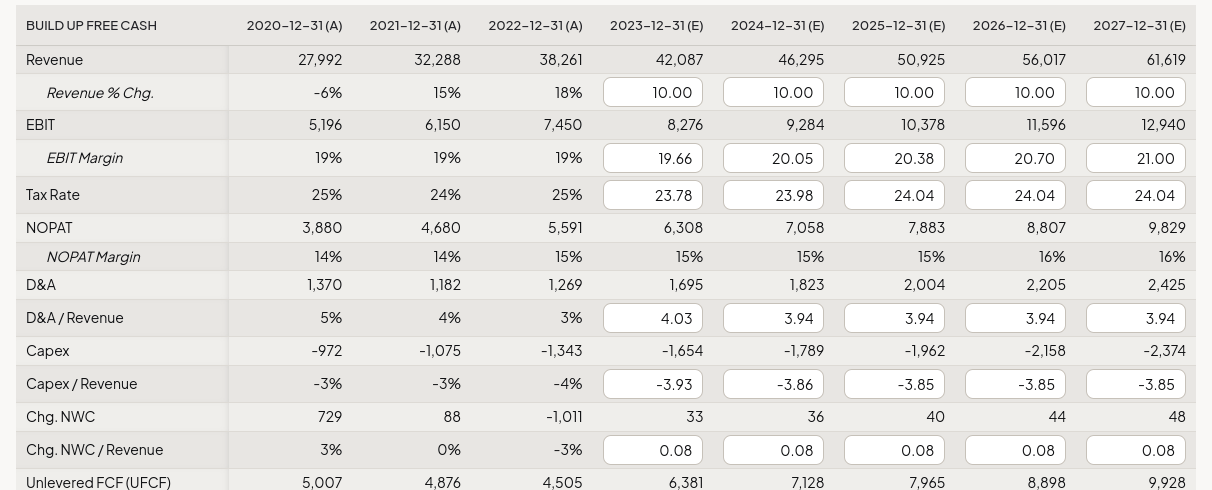

I don't believe we need a valuation model to conclude that the stock is not a buy right now, but let's assume some numbers for the sake of analysis: using a 2% terminal growth rate, a WACC of 8%, and approximately a 15% free cash flow margin. The variable here will be the growth rate. I will assume an optimistic growth rate of about 10% in revenues, with margin improvement each year. The derived result in this case is an intrinsic value of 247 euros. Based on the model, the stock is overvalued by more than 70%. Now, I wouldn't be so pessimistic, as L'Oréal has been trading at an expensive multiple for years and still managed to outperform to some extent. However, current prices are too high.

DCF (Finchat.io) DCF (Finchat.io) DCF (Finchat.io)

{kind=link}

{kind=link}

{kind=link}

Conclusions & Risks

L'Oréal is a low-risk company in my view; disrupting this outstanding business would be extremely challenging, and the likelihood is that it might a business get acquired before facing such a threat.

However, there are risks that I see, including rising competition from small and local brands that could potentially impact sales in certain regions. Additionally, making incorrect bets on markets poses a risk to market share, emphasizing the importance of strong management.

The risk of paying too much for acquisitions is present, with the fear of losing market share, potentially leading to goodwill writedowns and a loss of free cash flow.

The key risk to the thesis, in my opinion, is valuation. I can easily envision L'Oréal's stock remaining stagnant until earnings catch up, or the stock might simply drop. I believe there's a significant chance of a return to the mean considering the high multiple L'Oréal currently presents, possibly even in 2024.

I view the future of L'Oréal very positively. I expect L'Oréal to continue taking market share and increasing its margins, with the hope of making reasonable-priced acquisitions. The major aspects I am going to monitor will be growth above market rates and Return on Capital growth. Both are very important factors for L'Oréal's long-term success

Considering the risk/reward profile, I am currently rating this outstanding company as a hold. If the stock drops to around 30 PE, it could present a legitimate buying opportunity, but for now, a cautious approach and waiting may be prudent.

I'd be interested to hear your thoughts on this stock.

For further details see:

L'Oreal: You Won't Beat The Market With This Price