LH - Laboratory Corp.: Rate On Capital Deployed Contracting Hold

2023-09-14 03:20:18 ET

Summary

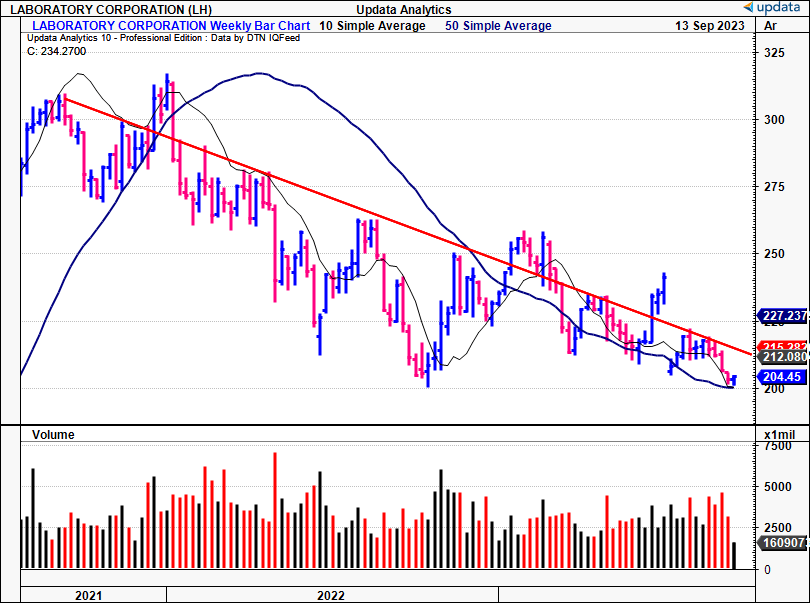

- Laboratory Corporation of America Holdings is selling at its lowest range since 2021, continuing a 2-year downtrend.

- LH's economics have weakened since the pandemic, producing low returns on capital deployed.

- The company's competitive advantage period has been shrinking, and its valuation factors suggest limited upside.

- Net-net, reiterate hold.

Investment summary

Since the June publication , there have been multiple investment updates for Laboratory Corporation of America Holdings (LH), but the central themes remain in situ. LH now sells at its lowest range since 2021, in continuation of a 2-year downtrend [Figure 1]. Brief snapback rallies along the way haven't furthered the bid, and have struggled for continuation beyond resistance. There's good measure for this too-its numbers were strong throughout the 'pandemic-era', but have pared right back since. Most critically to this report, it has ~$169/share invested in business capital, returning ~$18/share in TTM post-tax earnings, simply unattractive economics.

This report will unpack all these points in greater detail, linking back to the broader hold thesis. The facts pattern shows investors may have more selective opportunities to allocate capital, and that now mightn't be the right time to buy LH. Net-net, reiterate hold.

Figure 1.

{kind=link}

Facts pattern of reiterated hold thesis

1. Latest developments-Q2 FY'23 insights

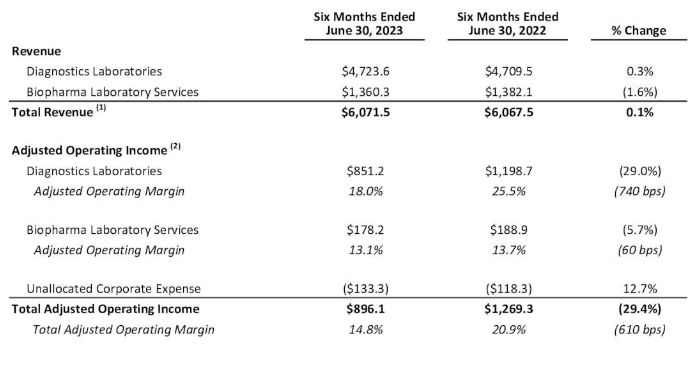

LH clipped revenues of $3Bn in Q2 , up 380bps YoY on adjusted earnings of $3.42/share and FCF of $177mm. Sales in H1 came to $6.07Bn, flat on last year, as seen in Figure 2. However, COVID testing revenues continue to decline, making it difficult for LH to report growth numbers, 1) off the higher base in '22, and 2) with an entire reporting segment almost absolved. Given numbers posted this YTD, management revised guidance to $12.25Bn at the top, calling for 3% upside at the upper bound. It is eyeing earnings of $13-$14/share and FCF of $800mm-$1Bn on this.

Figure 2.

Source: LH Q2 Investor Presentation

{kind=link}

There were several divisional takeouts from the quarter, namely:

- The base business grew 12.7% YoY (10.8% with FX baked in), despite an 88% fall in COVID testing revenues. The Ascension lab management agreement contributed ~5% to the upsides in Q2.

- For the YTD, diagnostics revenues were $4.72Bn, c.30bps higher on last year. Diagnostics booked $2.34Bn for the quarter, and pulled this to $410mm in operating income on a 17.5% margin, a compression of ~550bps YoY.

- The biopharma lab services division did $699mm of business and grew 3.1%. Around 2% of this was from the core business, with a c.100bps FX tailwind. LH holds a positive outlook for its biopharma labs segment. The increase in organic revenue was partially balanced by headwinds in the supply chain of non-human primates ("NHP"), which impacted its early development research business downstream.

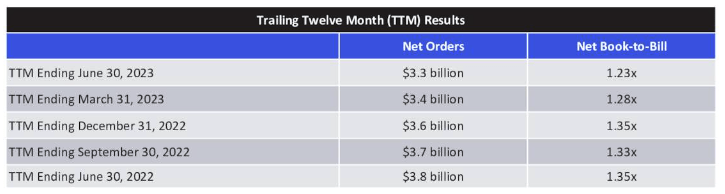

The trailing book-to-bill ratio was 1.23 leaving the quarter, down from previous quarters back to 2022 [Figure 3]. But keep in mind, that a ratio above 1.0 is preferred, signifying demand is outstripping orders shipped.

Figure 3.

Source: LH Q2 Investor Presentation

{kind=link}

As to the firm's capital allocation, LH did utilize a fair amount of cash last period. The major trends included:

- LH invested $103mm towards CapEx , which is expected to account for ~3.5% of its base business revenue for the year.

- The company also allocated $137mm towards acquisitions and distributed $65mm in dividends during this period.

- It didn't repurchase any shares (unlike in previous quarters), but LH did authorize $1Bn for buybacks, due to start in Q3 and wrap up by year-end.

- Whilst not investment related, I'd also point out the company's LaunchPad initiatives are on track to deliver $350mm in cost savings over the next 3 years (per management). Additionally, LH plans to eliminate $25mm in stranded costs throughout the enterprise in Q3, stemming from the recent spin-off of its Fortrea business.

In fact, it's likely important to consider how LH will report its operating segments from hereon in. It shed some light on this on the call:

Moving forward, we'll report our laboratory services business under two segments, LabCorp Diagnostics Laboratories and Labcorp biopharma laboratory services. Biopharma laboratory services consists of two businesses: our Central Laboratories business, which represents about 70% of segment revenue and Early Development Research Laboratories, which although smaller, is also a leader in the market."

2. Analysis of economic performance

Growth-in terms of sales, profits and cash flows-has been flat the last few years, despite all the COVID-19 inclusions. I also rhapsodized in the last publication the lack of value-add on offer in buying LH at this stage. Similar trends were observed in the 12 months leading up to Q2.

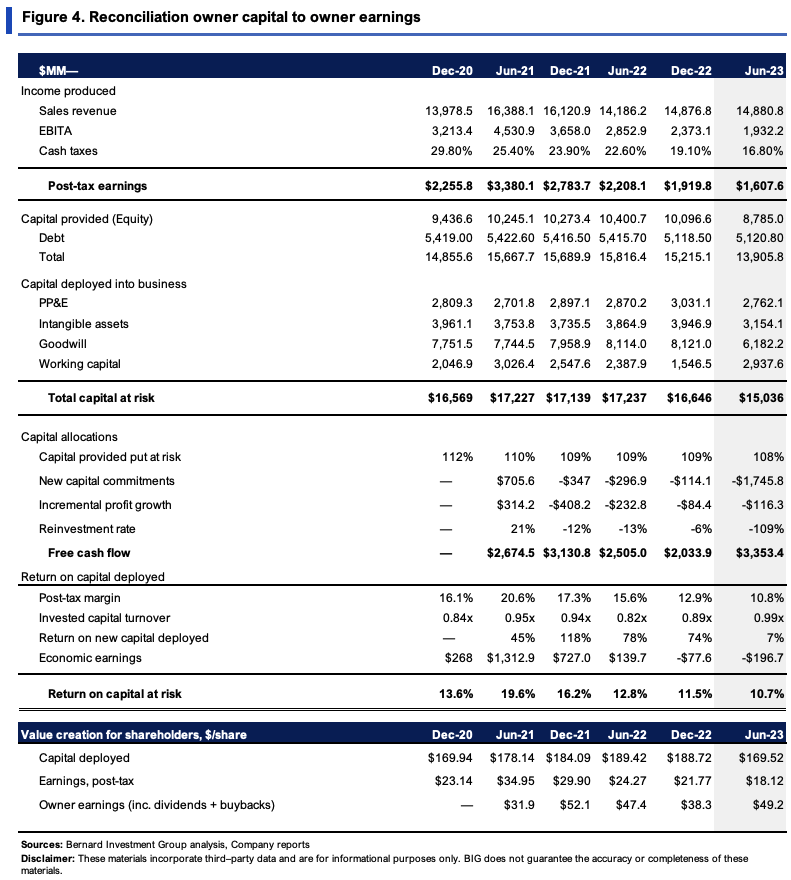

Figure 4 outlines the firm's economic levers from 2020-2023 on a rolling TTM basis. Note that it spun off $3.35Bn in FCF after the Fortrea carve out.

Right away, we see that LH has $169.50/share capital invested. There's $15Bn deployed that's needed to run the business at this current state. Around $18.10/share in post-tax earnings were produced on this last period, just 10.7% return on investment. Not attractive in my view.

A useful thought exercise helps explain why:

- Say you bought a business. Say it had $1,000 of business capital, and you paid $1,000 to acquire it (EV/IC = 1x). Say you also had a required rate of return of ~12%, in line with market averages. This hurdle rate exists because it's the opportunity cost. You'd need your new business to produce c.$120 of earnings into perpetuity (12% ROIC) for it to add value to your portfolio (the mathematics changes when introducing a time horizon and growth rates). The business is worth $1,000 (120/0.12 = 1,000) This business has a P/E of 1,000/120 = 8.3x. If it were $80 or 8%, the business would be worth $667 to you (80/0.12 = 667) despite a higher multiple (1,000/80 = 12.5x).

- More importantly, those earnings should be reinvested by the business, provided there is an investment runway (buy more inventory, more machinery, etc.). If all the earnings are recycled back in, you'd need the business to produce another 12% on these new investments. So, the $120 investment (drawn from $120 of earnings) should increase profits by 12% to $134.40. At the same 8.3x multiple, the business is now worth $1,115 (8.3x134.4 = 1,115.50). If earnings grew at an 8% ROIC, the business would be worth just $1,080.

- Provided there was the opportunity too, the business earnings/cash flows (or a portion of) should be reinvested again at a minimum 12% return to compound the company's intrinsic value.

- The longer a firm can reinvest its cash flows at above-market rates, the longer its competitive advantage period will remain in place. Buffett labelled this the moat.

In fact, LH's competitive advantage period has been shrinking since 2022. The reasons are clear-no growth at the margin, and capital turnover at ~1x. The capital turns I can accept. But you'd expect higher margins on LH's unit sales to square off with LH's economics, being a lab services business and all.

Should this continue in tandem:

- You'd be paying $204/share to buy LH as I write;

- Owning $169/share of business capital;

- To get $18.10/share in earnings after-tax, just 10.7% return on the firm's business capital.

- Say the hurdle rate is 12% (long-term market averages). Growth is destructive to LH's valuation in this case-the rate of earnings on capital required to run the business is below the hurdle rate. Stock returns closely track business returns over time, so this is tremendously important to the debate.

{kind=link}

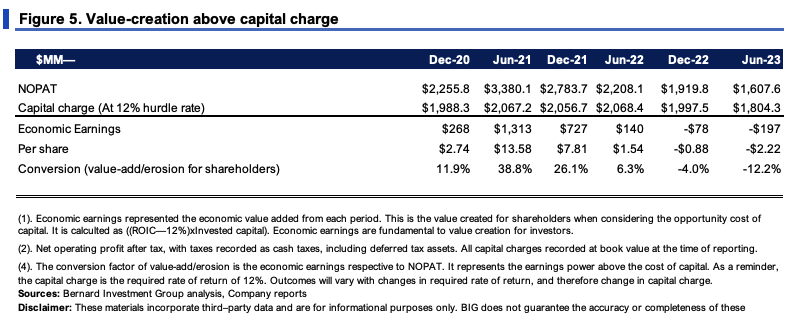

The waning of LH's competitive period is seen in Figure 5. Pay attention to where it says ' economic earnings '. These quantify all profits above the required rate of return, 12% in this instance. Anything positive in economic earnings is desired, along with a positive conversion factor. Since late 2022, it's been all economic losses for LH and its owners. This, despite positive growth in sales.

{kind=link}

3. Value drivers

The key drivers of LH's operations these past 3 years are seen in Figure 6. I've shown the change in M&A as a percentage of the change in sales, the same with the other capital requirements.

BIG Insights

Critically, sales growth is up 1%, with an average operating margin of 15%. Operating margin has been unstable, and declining. Plus, each new $1 in sales required an additional $0.955 in capital requirements (reduces to $0.04 including intangibles). Still, this is almost a 1-for-1 increase in capital requirements with growth in sales.

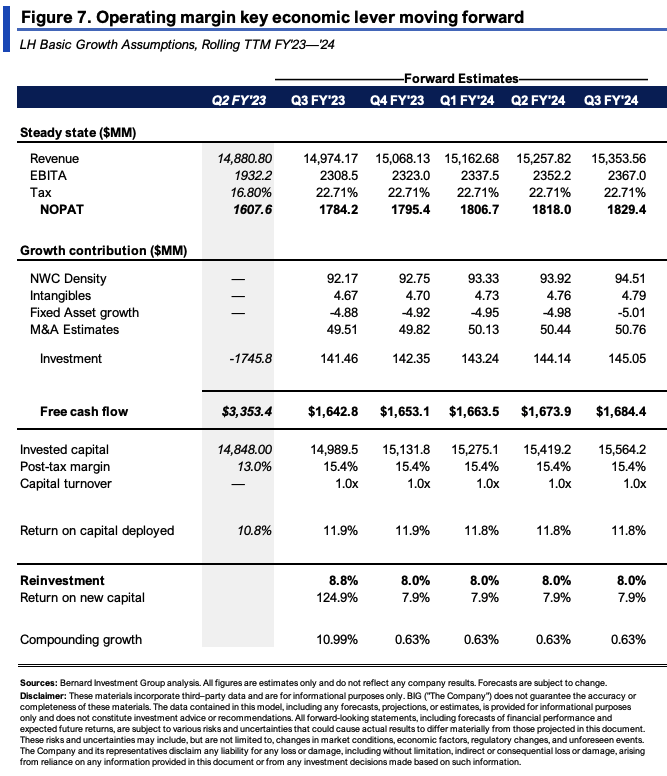

A thoughtful exercise is to carry these assumptions forward as a steady state or operations. Figure 7 does this, and assumes sales will remain constant at 1% growth, operating margin will be flat, and M&A will average 53% of the change in revenues.

Should this occur:

- LH would invest ~$140-$145mm per quarter on top of its current asset base ($500-$560mm annualized).

- It could spin off $1.6-$1.65Bn in FCF, a step above management's FY'23 forecasts.

- The earnings rate on capital deployed would still be below 12%, and it would compound its intrinsic value at 0.63% on average into FY'24.

This squares off with earlier findings, in that LH's current state of operations isn't accretive to shareholder value above what investors can achieve elsewhere with similar risk.

{kind=link}

4. Valuation factors

Several critical points are useful in the valuation facts pattern. For one, the stock sells at ~15x forward earnings and 13x forward EBIT. You're getting an 8% forward cash flow yield at these multiples.

But consider that, 1) LH has created just $2 in market value for every $1 in net asset value, and 2) it trades at an EV/invested capital of 1.5x. This tells me investors aren't pricing these LH's assets to throw off piles of cash into the future.

Comparing the ROIC/hurdle rate and EV/IC ratios is also useful. Both show a return on investment produced from LH's capital. One shows business returns, the other shows market returns. Comparison of the two shows what kind of growth is priced into LH's market value. A figure below 100% is desirable. You can see that's not the case here with LH.

BIG Insights

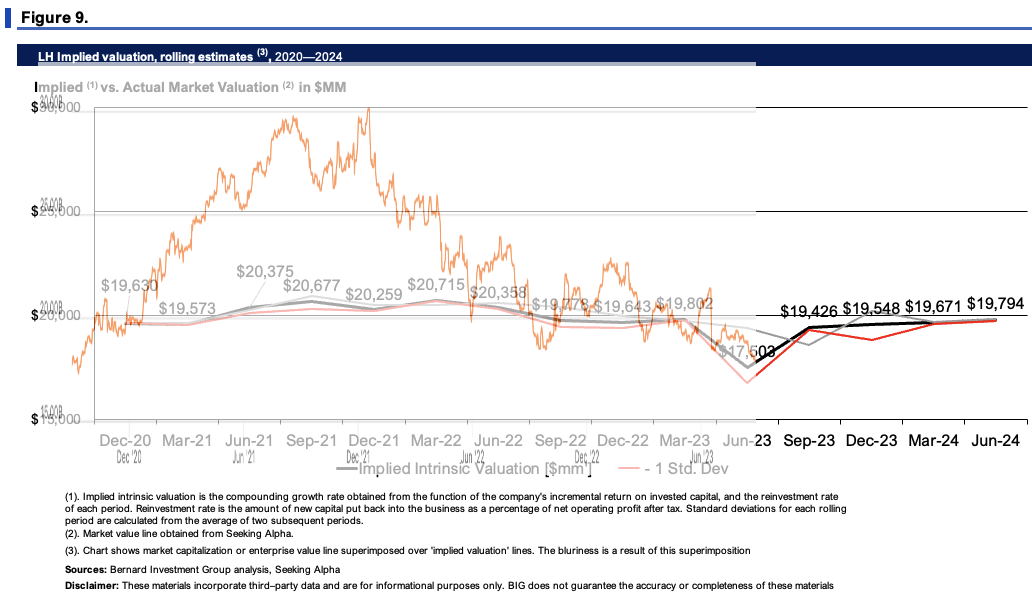

Two other sets of analyses corroborate these findings. The first is shown in Figure 9. This compounds LH's market value at the rate of its ROIC and reinvestments. LH was trading at lofty premiums across 2020-'21 (along with 99% of the entire market) but in classic economic fashion, has reverted sharply back to its implied intrinsic value. Based on the calculus, it would appear the market has valued LH appropriately at its current mark.

{kind=link}

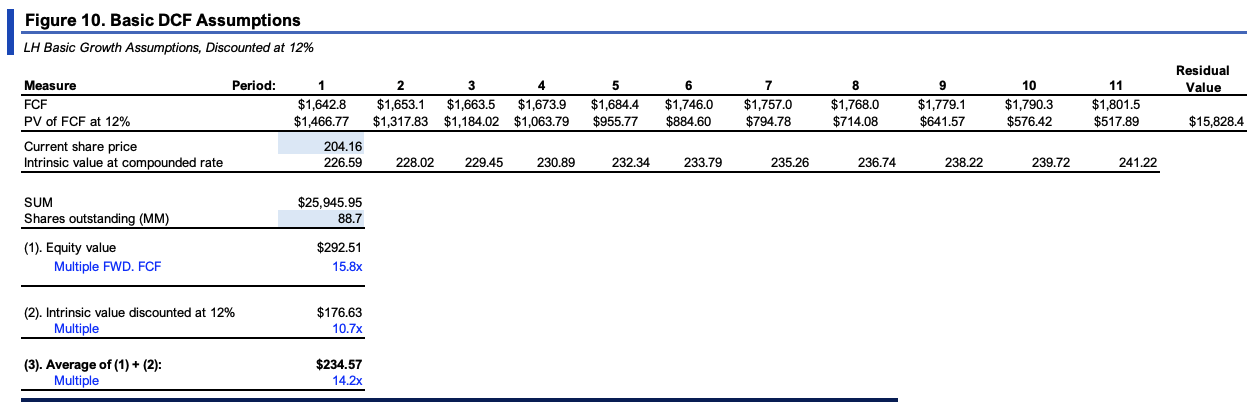

The second projects LH's cash flows out to FY'28 using the steady state numbers outlined earlier, then discounts this back at the 12% hurdle rate. It also does this from the current share price. An average of the two measures spits out an implied value of $234/share, or 14x FCF, a ~15% value gap. Not the broadest margin of safety, and limited upside on the initial investment ($31/share off $204/share investment as I write). This further supports a neutral view.

{kind=link}

In short

Whilst there are multiple investment updates to discuss, the central theme remains for LH: it must navigate its way out of the post-COVID era. Just like so many healthcare names, sales and cash flows have pared right back since we left the pandemic-era. There's no question LH is a great company-strong market share, great core offerings, that kind of thing. It's just not the right time to buy it in my view. Not when there's multiple selective opportunities available right now. In that vein, reiterate hold.

For further details see:

Laboratory Corp.: Rate On Capital Deployed Contracting, Hold