LH - Laboratory Corporation: Paring To Hold With Profitability Capital Efficiency Headwinds In Sight (Rating Downgrade)

2023-04-06 03:13:22 ET

Summary

- LabCorp has some homework to do as Covid-19 revenues pare back sharply.

- The return on its investments made into such growth isn't sustainable, meaning it must look for new growth initiatives.

- Added to that, an effort to diversify its top-line geographically is required for the same reasons.

- Valuation upside isn't likely unless capital efficiency and profitability drastically improve.

- Net-net, rate it a hold.

Investment Summary

I'm paring back my rating on Laboratory Corporation of America Holdings (LH) to a hold after surmising that the bullish thesis has run its course for now. LH's annual performance in FY'22 reveals forward-looking headaches to its growth, investment opportunities, capital efficiency and valuation upside. For instance, top-line revenues decreased 770bps YoY to ~$14.9Bn, underlined by a 750bps decline in Covid-19 turnover. This, compared to a 250bps increase in turnover for its underlying business. Covid-19 income is diminishing rapidly and there will be a heavy investment required to offset this and maintain a $3Bn operating run rate.

Still, there are positives. Book value per share increased ~3.75% YoY, up 47% since FY'19. Further, management approved a $195.2mm dividend payout to shareholders 2022 and approved a $2.5Bn buyback program of which c.$1.1Bn of stock [4.7mm shares] was repurchased during the period. Added to this, LH reports a Q4 FY'22 backlog of $16.3Bn, of which ~30% is expected to convert to the top-line in FY'23. Collectively, the tangible return for equity holders was 18.38%, despite the negative 12.4% TTM stock performance and narrow c.40% gain for the last 5 -years.

However LH's current market multiples don't stack up in my opinion. With Covid-19 and U.S. based revenues causing some issues, profitability and returns on new capital may remain under pressure. Further, the investment required to fund growth strategies in new markets could be costly to shareholders, and is likely to compress LH's valuation. A performance anomaly is required, and LH has a way's to go in that regard from my analysis. Here I pare back my view on LH to neutral, at a $260 valuation, just 13% margin of safety on a 9% projected earnings yield. At the current level of risk, current market multiples and projected FCFE contraction, I'd be looking for a higher forward earnings yield than LH's 9%, even considering the impeding dividends and $1.1Bn buyback just approved. I'd want more than 13% upside too. Rate hold.

Fig. 1

{kind=link}

The key facts

In the balanced view from the points raised earlier, it is my expectation LH will incur similar headaches given the below factors.

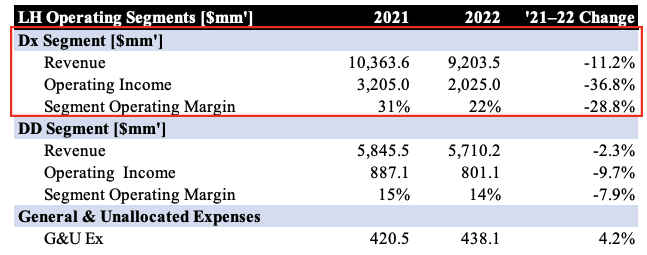

One, the company's divisional breakdown shows its diagnostics ("Dx") segment, that makes up 61% of top-line revenues, incurred double-digit YoY declines in turnover, and 36.8% clip in operating income [Figure 2]. The gap stems from geographical allocation of the portfolio, with the bulk of income derived in the U.S. vs. internationally. This might have potential FX benefits, but it's yet to show.

Two, as a negative, it was the. core Dx business that slipped and will likely continue to do in the mid-term, as Covid-19 sales begin to diminish rapidly. This is an issue, as I see reasonably flat operating income growth looking ahead, impacting returns on new capital, as discussed later. U.S. requisition volume was also lower at 7.5%, again, the bolus of downside incurred from Covid-19 sources of income. Hence, geographical distribution of revenue played a large factor. This was also the case for the drug development ("DD") arm with Covid-19 revenue exhibiting a $100mm drop to $5.7 Bn.

In that vein, the key factors for LH are as follows:

- Is LH really a company capable of generating $3–4+ in operating income on an ongoing basis without the Covid-19 tailwinds? If not, it may be valued at an appropriate P/E discount to peers (currently 43%).

- Despite the 7.7% revenue decrease, inventories were booked higher by 17.2% YoY to $470mm. This, despite widespread markdowns in Covid-19 inputs across the industry. This tells me more free cash flow was diverted to inventories and could signal a) poor use of capital or b) real effects of inflation.

- The concentration risk for its top line is fairly obvious now. U.S. concentration was a major factor in revenue downside, acknowledged by the company. It needs to focus on expanding growth and investment initiatives outside of the U.S. to hedge this risk. But, the execution risk means there's no guarantee it will succeed in doing this.

- General and unallocated expenditures were up 4.2% YoY on a tighter revenue line. This is certainly not ideal. Alas, the question is, can LH bring these numbers down, with a forecast top and bottom-line growth this year.

Fig. 2

{kind=link}

Three, I'd say it's important to consider these additional points below to balance the equation. They involve the Clinician Laboratory Fee Schedule ("CLFS") and the Physician Fee Schedule ("PFS"):

- Around 9% of the company's Dx revenue was reimbursed under the CLFS, and ~0.4% under the PFS. Both are up from FY'21.

- More importantly, it expects 1.2% in total PFS reimbursement this coming year. The total PFS rule increase is 2%, and further increases would be net positive for LH. Further to this, it expects another $38.6mm increase in CLFS revenue for specimen collection this year.

- It's not unreasonable to expect this to happen given the broad increase in service costs to wholesalers and end-customers. If it continues, this could provide a potential long-term tailwind.

Four, it's difficult to contain the disappointment in profitability for LH's equity investors. The large drop in post-tax earnings spurred a 45% downdraft in return on equity ("ROE") and return on assets ("ROA") to 12.7% and 0.6% respectively [Figure 3]. We are now tasked to pay nearly 2x book value (at 12.7% trailing ROE), making my estimated 26% forward investor ROE less attractive at just ~13%.

Fig. 3

{kind=link}

Five, LH's headaches look beyond revenue distribution. It is also losing leverage from a loss in capital efficiency. Specifically, for LH to see a comeback back above valuations seen in FY20–21', a much higher percentage of net operating after tax ("NOPAT") has to be reinvested to sustain the rate of return on its capitalized investments.

Look at it this way. For LH to maintain current level operations, we could assume annual OpEx at $2.25Bn and net CaPex of ~$3Bn would remain in situ with no change into perpetuity. LH's return on its existing capital would also equal its cost of capital, with no investments into new capital made ever again. There'd be no company growth. Here, we'd have a firm doing $14.8Bn in sales, expect a c.9% net profit margin, valued potentially at $20Bn market cap, with retained earnings expanding year on end into perpetuity. But no YoY earnings growth.

Two obvious problems here, 1) this doesn't generate any additional corporate and shareholder value, and 2) LH's Covid-19 revenues are diminishing rapidly anyway. So, in order to command an investment today LH has to pivot strategy and divert capital toward unlocking long-term value. But growth always comes at a cost. What cost, specifically? Less residual earnings available for investors at the end of the year. Lower share of the profits, basically, meaning less income, and valuation pressures. Instead, cash has been diverted back into the business to generate a return on new capital, hopefully above the hurdle rate.

Therein lies the problem . As investors, we want as much of the generated earnings as possible, available to us as free cash flow. Firm's that generate high returns on capital reward their investors with tremendous free cash flows and warrant valuation upside. Plus, this should grow over to grow the marks on our positions. For a firm to command investment today, it shouldn't have to pull too much FCFE away from investors to grow future profits. In other words, each new investment it makes should generate a return greater than what it cost shareholders .

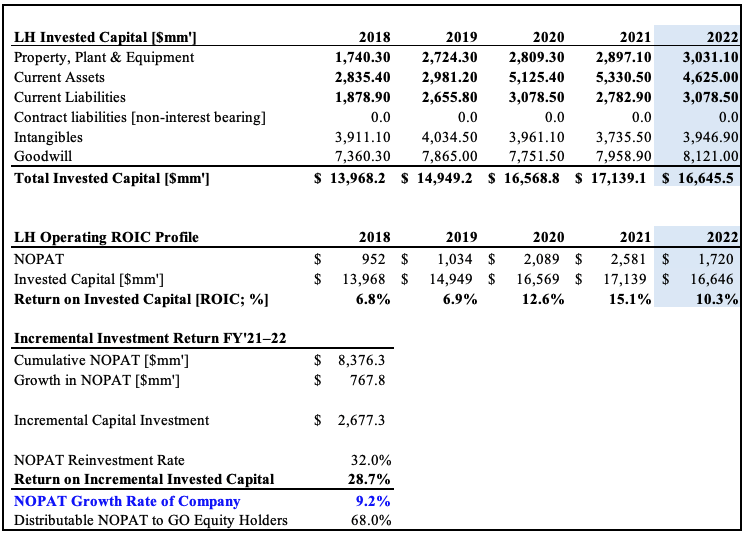

Over the past 5-years, LH has generated an incremental return on new capital of 28%. The cost to investors – 32% of post-tax earnings were reinvested back into the business to achieve this – meaning net 4% less free cash flow available to equity holders. One could argue 28% isn't terrible, and I'd agree. But, it came at a 4% net cost to shareholders, so it's hard to justify. Unless these numbers improve over the coming 5-years, growth is going to come at a substantial cost to shareholders into the future as well. Hence, the stream of future cash flows available to investors is less, hurting the firm's valuation.

Alas, LH's return on invested capital is a critical and defining feature in the investment debate. It has fallen 7.4 percentage points since December FY'21 [Figure 4] while the investment into maintenance and new capital has increased significantly. It's important to remember that ROIC is a function of invested capital turnover, NOPAT margin, and unit economics. To that point, LH's decreasing invested capital turnover points to capital inefficiency on the growing investment base. At the same time, the downturn in NOPAT margin is driving rates of return lower, demonstrating profitability hurdles it must overcome to justify current market multiples [Figure 5].

As such, it's tremendously important to recognize:

- With management's 7% revenue growth forecast (I am OK with this and see similar numbers) this could deliver a 45% increase in bottom-line growth in my estimation, given it is starting from a low-base. This could reflect well in the share price if the market rewards this recovery.

- Further, there's an issue in risk/reward calculus. I've calculated the company's WACC hurdle at 13%, and FY'22 ROIC came to 11.4%. Remember, a firm's growth only creates value if the ROIC beats the hurdle. So, it needs a 14% or higher ROIC this year for the 45% earnings growth to actually create shareholder value.

- But, as mentioned, this would require an improvement in capital efficiency and substantial profit growth, not unfeasible, but hard to obtain on the margin and required investment to do so.

Fig. 4

{kind=link}

Fig. 5

Data: Author, LH 10-K's

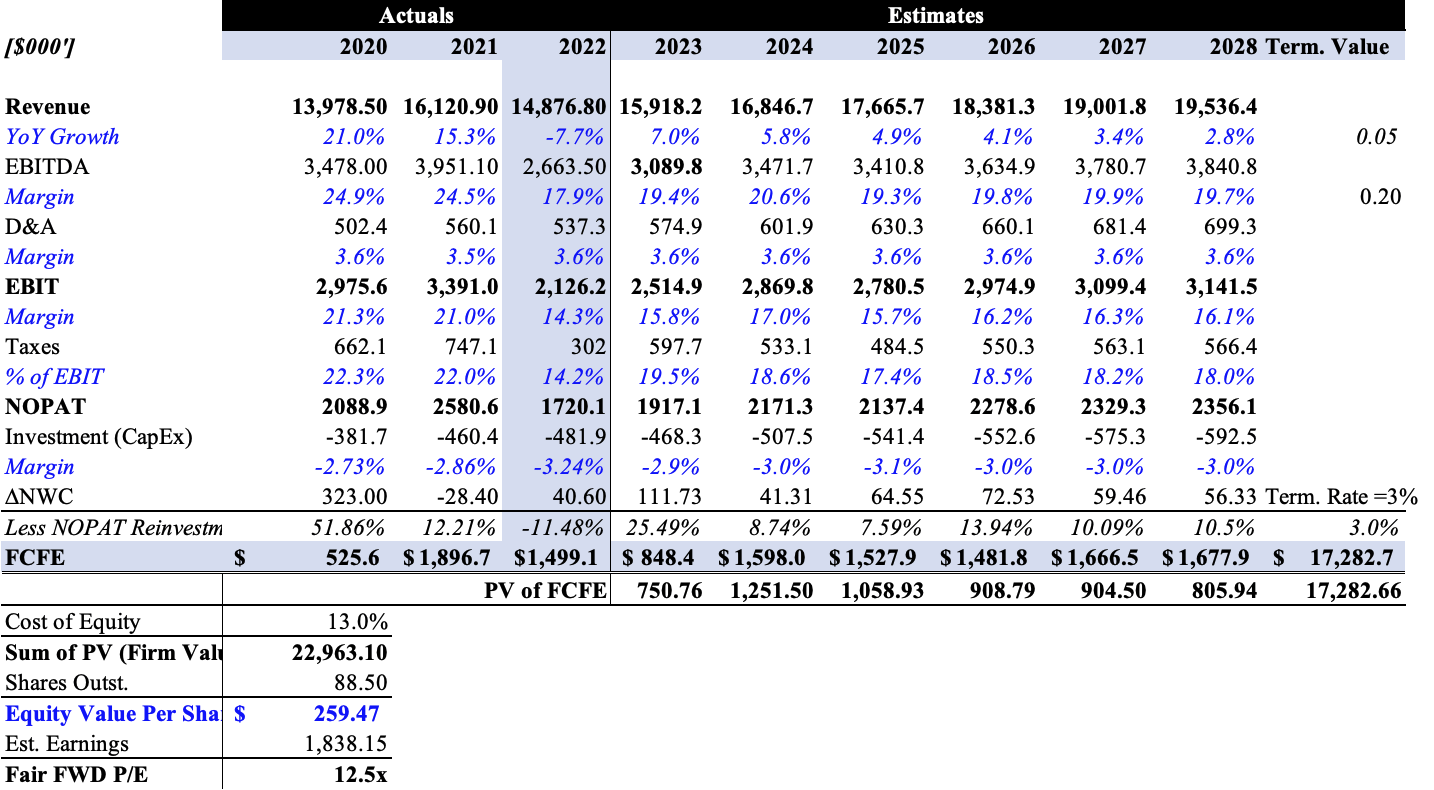

Looking to FY'22, $1.16Bn was also spent on strategic acquisitions. As a result, in view of the potential synergies and revenue/EPS accretion, OpEx will be booked higher as well. Notably, the core offerings are now broader across services. However, a bulk of this investment is spent on diversifying customers and turnover into international markets, and LH will continue putting the balance sheet to use to do so. Problem is, this could become value destructive, if the return from acquisition-sourced income doesn't stack up. It's therefore important to consider management's additional $1.1Bn capital budget to approved buybacks from this year. This has no expiration, so could be slow, could be accelerated. Further, CapEx is expected at ~3% of revenue in FY'23 [I project the same at 2.9%) calling for $468mm in my estimates, down from $480mm a year ago, but above $381mm in FY'19, sealing my point.

Smoothing the returns on investments out over the long-term, and outside of the pandemic to normalize Covid-19 factors, the incremental ROIC is commendable at 28.7% as mentioned. [Figure 6]. But as noted, it came at a 4% net cost to shareholders. LH has become more profitable, with 9.2% ($767mm) upside in NOPAT since FY'18, on the $2.7Bn reinvestment of post-tax earnings to achieve this. A good portion (68%) of this has flown through to the bottom-line as free cash flow to equity holders. As I've said, in LH's case, it's best to look at free cash flow as what's left as post-tax earnings after reinvestment for future growth (FCFE). On the one hand, FCFE has grown from $525mm in FY'20 to $1.5Bn last year. However, on higher variable and acquisition/restructuring costs, combined with CapEx and OpEx requirements, I have projected LH to struggle with FCFE growth, estimating $848mm this year, not seeing a full recovery in growth until FY'28 (Figure 7).

Fig. 6

{kind=link}

Valuation

Finally, LH's valuations aren't supported by any directional bias long or short in my estimation. On one side, a 7.5–9% forecasted forward earnings yield and 1.25% dividend yield are respectable measures to go by. But this is balanced with LH trading at 12.5x forward earnings with my estimates of intrinsic value, versus consensus' 16x. I'd certainly value LH at market value higher than what it's market right now, at $22.9Bn using the DCF in figure 7. I also see the broad market retaining a longer-term upward structure and LH to continue seeing some profitability upside down the road. Hence, I'd value the company at $260 per share today. Buybacks could be another tailwind for per-share valuations, dividends as well.

But this is a margin of safety of just 13%, and I'd want a much higher earnings yield than 9% to compensate for this. Not to mention the dislocation in earnings multiples between my estimates and consensus. Consequently, I see the stock valued at 12.5x forward earnings as mentioned, in-range, but behind the market's pricing of 16x forward P/E. In my view, the 13% upside potential doesn't make sense at this number.

Fig. 7

{kind=link}

In Short

I had been bullish on LH in November of FY'22. LH stock had taken out my previous $260 target, but hasn't maintained that rally, and is in a downward trend. The factors raised here do a good job in explaining the market's reasoning for this, in my estimation. Really, it's a story of capital efficiency and profitability for LH, where it would benefit from diversifying its top-line geographically, shy away from further investment related to Covid-19 income, focus on driving its return on investments above the cost of capital, and deliver a better performance in its legacy businesses. I still see it fairly valued at $260, or 12.5x forward earnings, despite the headwinds baked into this assumption. Net-net, reiterate to hold.

For further details see:

Laboratory Corporation: Paring To Hold With Profitability, Capital Efficiency Headwinds In Sight (Rating Downgrade)